glider3834

-

Posts

965 -

Joined

-

Last visited

-

Days Won

3

Content Type

Profiles

Forums

Events

Posts posted by glider3834

-

-

Just now, SafetyinNumbers said:

If they bought the shares back, we would find out within the first 10 days of December.

-

35 minutes ago, SafetyinNumbers said:

If Fairfax added or reduced its TRS position this month what would you think?

Keep in mind we wouldn’t find out until February and the news would accompany earnings so if it does happen it will be difficult to tell how the market takes it.

There was a cross of ~216k shares last Tuesday at the close which is why I’m asking.

we have no idea who the parties are to this trade but is it hypothetically possible Fairfax could reduce part of their TRS position & in turn purchase the underlying shares directly from counter-party - could they do this under a block trade exemption to NCIB with security regulator clearance?

I am just thinking if the 2% repurchase tax kicks in on 1 Jan then this would be an opportune time to do it.

-

3 hours ago, newtovalue said:

i think @glider3834 has it right - tax losses make tons of sense

This is what i found

Under subsection 88(1.1) of the Income Tax Act, non-capital losses of a subsidiary corporation may be carried forward and deducted in computing the parent corporation's taxable income, but only in a taxation year of the parent that following the winding-up of the subsidiary.

Subsection 88(1) of the Income Tax Act applies where a “taxable Canadian corporation” has been wound-up into a parent taxable Canadian corporation that owns at least 90% of the shares of each class, immediately before the winding-up

-

19 minutes ago, UK said:

This is interesting, thanks! But do I understand this correctly: is it some extra 4 M for them to spend for a 500 M or say 75 M, at a rate of 15 per cent, in possible tax benefits for FFH:)? If this is true, then this deal is more than a ten bagger just on this tax benefit basis:)))

yes but look its been a terrible investment for Fairfax so its really its just extracting something of value - turning a lemon into lemonade in a sense - they will need to call time on the turnaround at some point if there is no traction there & I hope thats sooner rather than later

-

1 hour ago, Viking said:

I agree. And I do not understand all the anger with the posts on Farmers Edge. Can anyone explain to me what Fairfax is doing and more importantly why they are doing it? What are the financial impacts? Clearly more information is needed to properly assess this announcement. My initial read is this is a nothing burger. But i remain open minded.

Yes, Farmers Edge was a terrible investment. It has been clear for at least a year that the end of this investment is near. Sayonara.

viking I am no tax expert but Farmers Edge had circa C$500M in non-capital tax losses at end of 2022 & that number would be higher now & if FFH can acquire all the shares (they currently have 61%) for around C$4M by my rough math, then if turnaround fails & they then choose to wind up this sub, then Fairfax the parent corp I think could use those tax losses applying whatever appropriate tax rate. Farmers Edge hasn't recognised any tax asset due to its ongoing cash burn.

I think as well as a private co. they would have lower running costs than a public co. Its end of tax year as well so given minority investors are likely sitting on tax losses there is probably intuitive sense to the timing.

They have a new CEO who is trying stuff but its not showing up in any revenue numbers , its possible Fairfax will want to give him more time but the recent financing of C$6.37M feels like it has almost been calculated to the dollar- thats my impression anyway.

-

4 hours ago, UK said:

I think there may also be a contingency, tax planning objective here, in the event the turnaround is not successful

-

1 hour ago, MMM20 said:

The bad news...

IPO Bound Go Digit Gets Show Cause Notice, Multiple Advisories From Insurance Regulator

14 Nov'23

Insurtech major Go Digit General Insurance, which is gearing up for its initial public offering (IPO), has received a show cause notice and multiple advisories from the Insurance Regulatory and Development Authority of India (IRDAI) last month, the company said in a new addendum to its draft prospectus filed with the Securities And Exchange Board of India (SEBI).

The development comes at a time when the company’s IPO is yet to receive final approval from the SEBI even after Go Digit refiled its draft red herring prospectus (DRHP) addressing certain concerns that the market regulator had raised earlier.

Go Digit revealed that the show cause notice from IRDAI has alleged non-disclosure of change in the conversion ratio of the CCPS issued by Go Digit Infoworks Services (GDISPL), the parent of Go Digit General Insurance, to FAL Corporation.

FAL Corporation is a part of Canada-based Fairfax Financial Holdings, which is one of the major investors in Go Digit.

“In terms of the Notice, the change in the conversion ratio of 6,300,000 CCPS issued by GDISPL to FAL Corporation, from ‘1 CCPS for 2.324 equity shares’ to ‘2.324 CCPS for each equity share’, which was reflected by way of an amendment to the JV Agreement dated August 11, 2022, is a material change to the information furnished at the time of applying for registration to the IRDAI,” the company’s regulatory disclosure to SEBI said.

As per the notice, Go Digit was expected to provide the details of such change to the IRDAI but it did not furnish the “full particulars”. Hence, IRDAI has also alleged that the startup is in violation of Section 26 of the Insurance Act.

If an adverse order is passed against Go Digit and its officers responsible for the non-compliance, the insurtech unicorn would be slapped with a maximum penalty of INR 1 Lakh for each day during which such failure continues, or INR 1 Cr, whichever is lower, the addendum mentioned.

Besides, IRDAI has also issued certain advisories and cautioned Go Digit on a few aspects.

The advisory notice has been issued for failing to take the insurance regulator’s approval for the change in remuneration of its Chief Executive Officer (CEO) on the account of the change in ESAR 2018 (employee stock appreciation rights scheme) to ESOP 2018 (employee stock option plans) and for failing to inform IRDAI of the retrospective grant of ESARs prior to the date of grant of the company’s certificate of registration.

“In the event the IRDAI is not satisfied with our responses or we fail to adhere to the advisories and cautions issued by the IRDAI, we may be subject to warnings, show-cause notices and/ or penalties in the future, which would, amongst other things, adversely impact our brand and reputation,” Go Digit said in its regulatory disclosure to SEBI.

Meanwhile, the IRDAI has also cautioned the startup to ensure due care and correct disclosures in the offer documents, of the position in relation to the commission on long-term policies and that acquisition costs incurred in the year, among several other advisories issued.

It is pertinent to note that Go Digit filed its DRHP with the SEBI in August last year. Within months, it also received the IRDAI’s approval to launch the IPO in November last year though SEBI had kept the IPO in ‘abeyance’.

In March this year, the startup refiled the DRHP with the market regulator for its $440 Mn, addressing the latter’s concerns about its ESOPs.

In the latest filing, Go Digit said its erstwhile Go Digit – Employee Stock Appreciation Rights Plan, 2018 has been amended and changed to ESOP 2018, pursuant to the resolutions passed by the board and shareholders on March 21, 2023 and March 27, 2023, respectively.

Founded in 2017 by Kamesh Goyal, Go Digit offers insurance policies across verticals including motor vehicle, health, travel, and property. Besides Prem Watsa’s Fairfax, the startup is also backed by prominent names such as Sequoia, cricketer Virat Kohli, and actor Anushka Sharma.

Go Digit’s IPO comprises a fresh issue of shares worth INR 1,250 Cr and an offer for sale (OFS) of 109.45 Mn shares.

I would expect them to pay the fines & move along, but these delays to IPO are frustrating, but on the flipside IPO conditions now in India look better than late 2022 https://www.business-standard.com/finance/personal-finance/india-emerges-as-global-leader-in-the-number-of-ipos-in-2023-123110600198_1.html and it does allow Digit to include their latest financials for Jun-23 quarter in their IPO application showing Digit's improving profitability

-

I guess will allow Fairfax to free up around $200M to invest in higher return debt instruments

-

this article is relevant to discussion on valuation

https://www.insidepandc.com/article/2cdgrj2sqw8zb25mjo2yo/specialty-lines/ipc

-

6 hours ago, vinod1 said:

suspect almost everyone on this board would disagree with this: the role of luck. Assume covid never happened, where do you think Fairfax would have been? It would still be doing much better than in the past. Nearly half of the earnings power increase was from the side effects of Covid - the shock, monetary response, the inflationary follow up and the interest rate response. If instead, let us say Covid did not happen, we still have zero interest rates, then where would Fairfax earnings power have been? Many of the things you mentioned as brilliant would not have occurred. We would still be bitching about Prem.

I wrote a bit a long winded reply but main point I would say is that we have to give Fairfax credit for their fixed income mgmt - luck plays a role but you have to put yourself in a position to take advantage - they saw more value in the optionality of holding cash over stretching for the limited yield on offer.

-

one potential driver of future earnings will be future additional impact on EPS if/when they acquire additional shares from minority interests in Odyssey, Brit, Allied - as premium growth slows & they can build excess capital in subs, they should be in better position to generate cash to pay divs to holdco &/or buy out minority interests IMHO

-

30 minutes ago, Viking said:

I received a response to my question to RBC regarding why they valued Fairfax at 1 x BV. Copied below is their response. I was impressed they got back to me.

----------

On Nov 8, 2023, at 6:41 AM:Hi (Viking),Fairfax has never traded with the peers you are citing (most of the time has been below book in recent years). I think there are a few factors to consider including Fairfax being a more complex business vs. some peers in terms of where they write business, international (not U.S. or Bermuda based), larger non-insurance exposures that can have volatility, larger equity exposures, track record, not trading on major U.S. exchanges, little analyst coverage. I don’t dispute your points but these are a few reasons (those could change over time) – not about the fundamentals of the business right now. Thanks for the email.Best,Scottthanks viking its interesting how price can drive narrative

-

this is an interesting article on Pacwest deal for KW & FFH which shows it was a strategic acquisition & looks like portfolio is performing as expected

'The loan portfolio Kennedy Wilson assumed has remained healthy despite the many market headwinds that unfolded over the past 18 months due largely to rising interest rates. Whitesell said there are zero losses in the portfolio as a result of low leverage and a strong asset management team that actively works with borrowers to rebalance loans as needed. The portfolio is facing some looming maturities, with about half of the loans positioned for an immediate paydown and the rest expected to receive extensions, according to Whitesell.'

-

7 hours ago, Munger_Disciple said:

A couple of question for Fairfax experts:

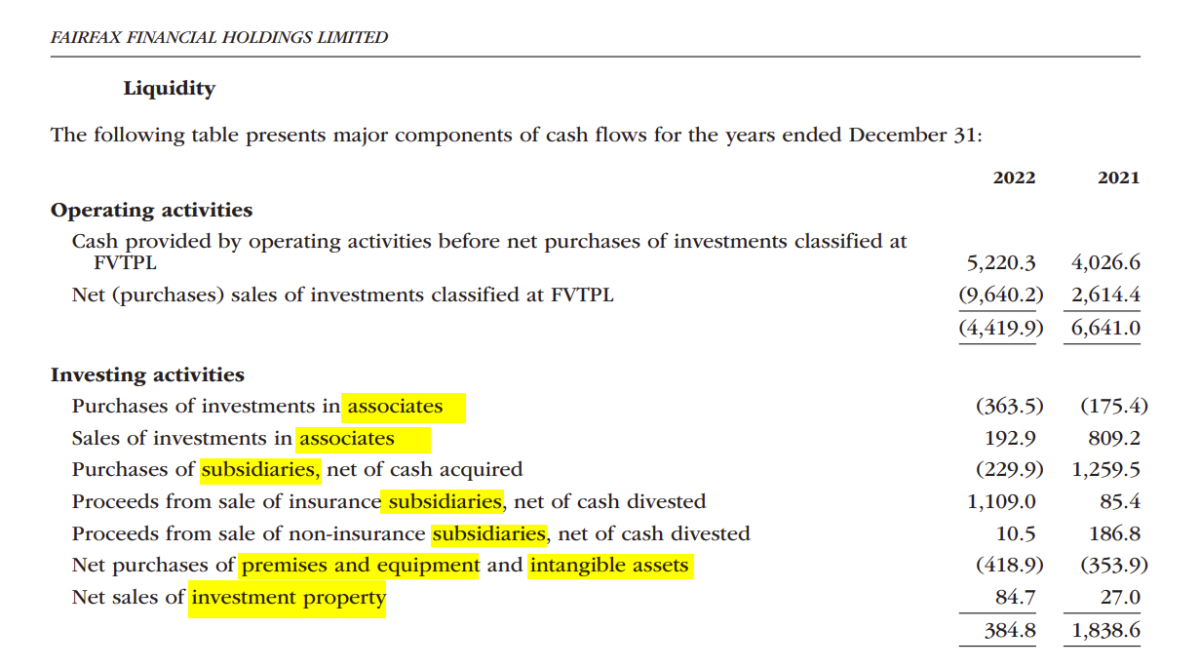

- I was going through the cashflow statement in Q3 report. At first glance, it seemed odd that the cashflow from operations for the first nine months was negative $1B. Then I realized it was due to the line item called "Net purchases of investments classified at FVTPL". I would think purchases of investments would belong in investing activities, not operating activities? Is it related to adoption of IFRS?

- Why do they classify share buybacks into two separate line items, i.e., purchases for treasury and purchases for cancellation?

Thanks in advance.

I am not an expert but I think under IFRS 9 if Fairfax's business model is managing certain financial assets for changes in fair value (see below) it would classify them at FVTPL assets - purchases & sales of these FVTPL investments appear under operating activities.

These FVTPL designated investments are different to investments in associates, subsidiaries, real-estate, P&E or intangibles (see below) where purchases or sales of these assets appear under investment activities.

-

2 hours ago, SafetyinNumbers said:

The original institutional investors (OMERS, Fidelity and Markel, I think) who negotiated this deal on behalf of minority shareholders are the ones who have let us down. In theory, they were counting on themselves to be buying to close the discount every three years to avoid this dilution. Unfortunately, the key decision makers are probably out of their jobs and there isn’t any capital for stocks outside their benchmark.

This is the first performance period where it’s meaningful so let’s see what they do. FWIW, they have bought more than enough stock back at lower or similar prices to offset the dilution but I think most people think about it like you do.

3 hours ago, This2ShallPass said:Performance fee is much worse. Calculated with BV and paid in discounted shares. For this perf period, Fairfax is going to get 60% more shares. Say Fairfax should get $1M in perf fee as an example - they should have got only 47k shares but will get 77k!!

Minority investors are getting fleeced, no way around it. Either they should start a SIB before Dec to close the gap somewhat (not going to happen) or this adds to the other cases of them treating minority investors poorly.

I think Fairfax can only take perf fee in shares up to 49% ownership

'In no instance will Subordinate Voting Shares be issued to satisfy the Performance Fee if, after such issuance, Fairfax and its affiliates would own more than 49% of the outstanding equity capital of the Company on the date of issuance.'

-

8 hours ago, SafetyinNumbers said:

Is there anyway to assess midyear or is there only an annual update?

Yes would be good to know - I suspect they want to finish their actuarial review of y/e reserves before they publish an official number, having said that they probably update this number during the year, as they need to determine what dividends they can pay to the holdco from the insurance subs.

-

13 hours ago, SafetyinNumbers said:

Is Bradstreet and the fixed income team at Fairfax the GOAT?

I am not sure if I have said this before so apologies if I am repeating myself, but I met Brian Bradstreet at the FFH dinner in the year after Fairfax had the big CDS win, he really came across as very down to earth - maybe not what you would expect from someone who had helped Fairfax make $2B or so on their CDS bet. I asked how he knew about the issues at AIG & he said it was there if you read the footnotes. My takeaway from this brief conversation was here is a guy with who doesn't have a big ego & who really does the work & that honestly impressed me.

-

looks to be Grivalia's largest luxury hotel investment

With an investment approaching 300 million euros, Grivalia Hospitality inaugurated yesterday, with the participation of the Prime Minister , Kyriakos Mitsotakis , the head of Fairfax, Prem Watsa, and prominent names from the business and artistic worlds, the first luxury tourist complex One&Only in Greece and one of the three planned by the Kerzner International group in our country.

-

8 hours ago, StubbleJumper said:

That is very interesting. That's some great optionality for FFH. At this stage, 8% isn't even an outrageous financing cost, so they can sit back for a few more years and see how the business goes at Ki and how the yield curve evolves, and then if both of those turn favourable, a redemption could make sense (or not!).

SJ

SJ yeh agreed - I dug into this a bit because I hadn't been able to understand the shareholding structure for Ki

-

17 minutes ago, SafetyinNumbers said:

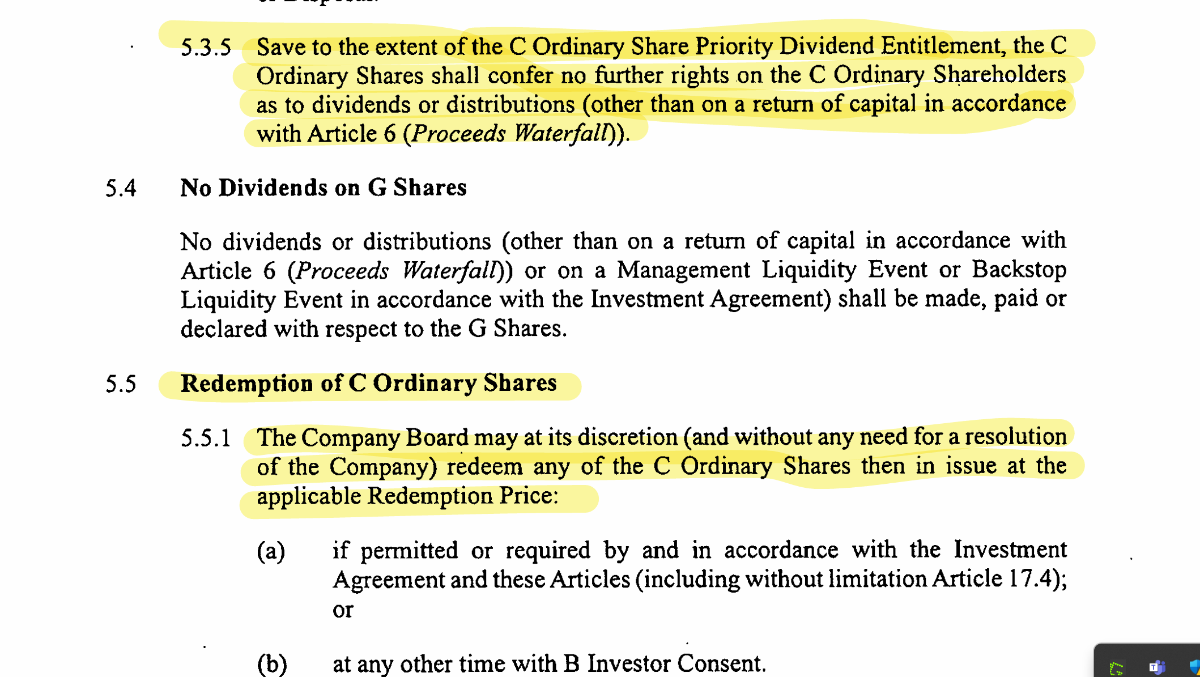

This is very interesting. Does Fairfax own the same class of shares as Blackstone directly or a different class with different terms?sure breakdown is Brit has 100M Ord A shares (1 vote each), Blackstone have 150M Ord B shares (0.64 vote each) and 250M Ord C Priority Div shares (non voting); and key execs have 80K Ord G shares (non voting)

-

Just looking at Articles of Association public filing from Ki Financial https://find-and-update.company-information.service.gov.uk/company/08821629/filing-history?page=1

With Ki, Brit has approx 20% economic ownership & 51% voting power.

But interesting is that it looks like Blackstone's C shares (approx 50% of outstanding shares) carry a fixed 8% priority dividend entitlement, but are also redeemable by Ki (see below).

Assuming Ki was able to redeem and cancel these C shares from Blackstone , it would increase Brit's ownership from 20% to 40% approx.

Terms of Investment Agreement 19 September 2020 between Blackstone, Brit etc don't appear to be available, so we don't have all the information here.

Recently Ki has been getting more traction in the follow market, so its worth considering what Ki could be worth and what Fairfax's ownership stake could be.

https://www.reinsurancene.ws/ki-teams-with-travelers-aspen-to-expand-digital-follow-capacity/

-

2 hours ago, SafetyinNumbers said:

Thanks for sharing! Probably why the stock was up almost 5% last week while the Greek market was flat.

-

JP Morgan expects significant upside for Eurobank's shares , recognizing that the acquisition of an additional 7.2% (29,710,012 shares) in Hellenic Bank , thus reaching 55.3% and pending the approval of the regulatory authorities that will now make it a subsidiary of the group, will act as a positive "catalyst" for the systemic bank.

In this light, the American house significantly increases the target price for the Eurobank share to 2.60 euros from 2.25 euros previously , with an "overweight" recommendation

-

1 hour ago, petec said:

Really? Did I miss something?

check out https://www.bnnbloomberg.ca/greece-s-eurobank-plans-to-expand-overseas-wealth-management-1.1942573

Fairfax 2023

in Fairfax Financial

Posted

Just on this subject of competitive advantages I would say their dealmaking in their core insurance business has resulted in a lot of shareholder value since they started. - they will trade in & out of insurance businesses & have generated billions in capital gains from ICICI Lombard, First Capital, Eurolife FFH, C&F Pet, Ambridge, Digit etc.