glider3834

-

Posts

965 -

Joined

-

Last visited

-

Days Won

3

Content Type

Profiles

Forums

Events

Posts posted by glider3834

-

-

11 hours ago, jeyfox said:

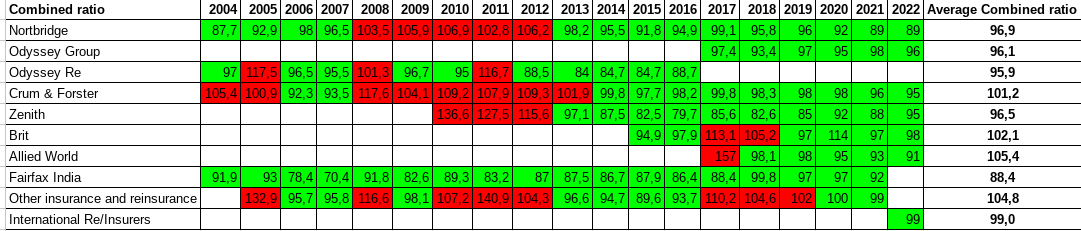

Fairfax did a great job on improving the combined ratio since 2004 on all of its insurance entities.

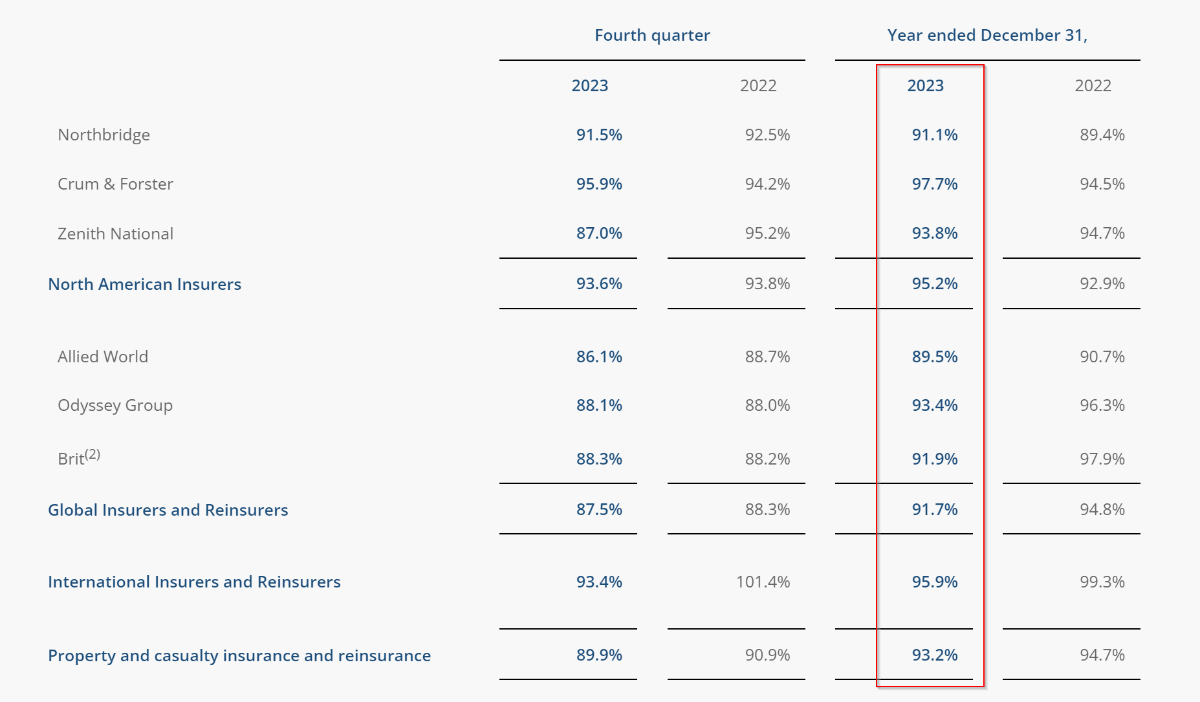

cheers - you might want to also update with 2023 below

what does the Fairfax India CR relate - I assume thats not FIH?

Just with Allied, Fairfax recorded only half a year's premium in 2017 so that throws the combined ratio for 2017 and also warps the avg CR number as seasonally the cat losses are usually concentrated in 2H.

In terms of CR I would look at averages in 5 year increments as well as trend in underlying CR along with qualitative info eg over last 12 mths Brit has been significantly reducing its property cat exposure

-

https://www.theinsurer.com/viewpoint/embracing-2024-allied-worlds-european-platform/

“Our growth is not just about expansion, but about strategic adaptation. I joined Allied World in 2008 and have witnessed an amazing transformation from a small team to a global force, with $6.5bn in gross written premiums, over 1,600 employees and 26 global offices.”

For the European operations, the focus has been growing the teams and the business in a measured, profitable way.

-

Looking at GIG transaction again, I believe based on fair value of acquisition consideration, Fairfax is effectively paying ~ P/B 2.2x for Kipco's stake.

100% implied equity value for GIG based on below is ~US$1.63B & GIG's shareholder equity at 30 Sep-23 was ~US$742.5M, which works out to implied P/B multiple of 2.2x

US$756M fair value of acquisition consideration is lower than US$860M headline number for two reasons

1. Initial US$200M upfront, cash payment is to be reduced by dividends Kipco received after 1 Jan'23.

2. Fairfax also has a payment deed for four annual instalments of US$165M (or US$660M) in aggregate which Fairfax records at its fair value ie discounted present value.

At 30 Sep-23, Fairfax measured the fair value of acquisition price at US$740M - this has now increase slightly to US$756M at the time of closing. But the workings for how this US$740M is calculated is shown below & helpful.

-

Looking at income from associates & non-insurance subs, its worth thinking about Grivalia Hospitality & BIAL which are significant investments. IMHO we haven't seen their normalised earnings/cash generation power reflected in Fairfax's results yet, because both have just completed major capex investment projects in 2023 & as they ramp up they are still operating below capacity in terms of passenger traffic (BIAL) and in terms of occupancy (Grivalia). Grivalia only opened the doors on its biggest resort this November https://www.linkedin.com/pulse/what-does-prem-watsa-gain-from-greek-tourism-thetotalbusiness

Also Fairfax has increased its ownership share in both businesses over the last 12 mths -so I am hoping in AR to see some clues as to how these might contribute to results in the coming year/s.

-

4 hours ago, Haryana said:

You are adding dividends as if they were paid at the end.

They were paid annually at the beginning of each year.When you account for that, the CAGR comes at ~16.5%.

Please see if you agree, time value of dividend.I assumed no reinvestment of divs (eg assume you pop dividend money in a no interest account each year and leave it there and add it to your share gains over period) - which appears thats how Fairfax got their CAGR calc of 11.7% for 2017-2022 but feel free to double check.

You do see total return measures that include reinvested divs, so I think assuming no reinvestment like Fairfax do is more conservative.

-

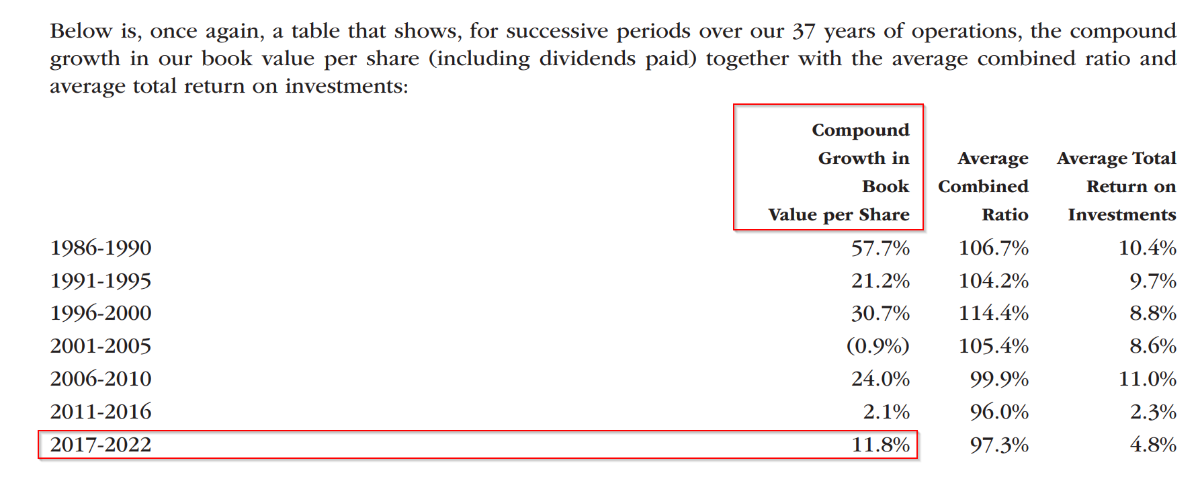

So Fairfax's book value per share (BVPS) CAGR growth (incl dividends) for 2017-2022 period was 11.7%

If we now update & look at 2017-2023 period, I get BVPS CAGR (incl dividends) as 15.5%

Calc below

=(1009.65*/367.4)^(1/7)-1 = 15.54%

*2023 YE BVPS 939.65 + 70 divs = 1009.65

-

8 minutes ago, treasurehunt said:

Yeah, seems ridiculous on the face of it. But I hope Prem goes into some detail about Exco tomorrow; I'd love to find out more about this investment!

I was hoping a silver lining with all this, is Fairfax delves a bit more into telling us about its private businesses including AGT - but lets see

-

1 hour ago, MungerWunger said:

MW questions to management for tomorrow's earnings call:

https://d.muddywatersresearch.com/content/uploads/2024/02/Fairfax_MWQuestionsForQ423Call.pdf

- so appears no questions on Digit valuation specifically or IFRS 17 from what I can see

- MW thinks that Warren Buffet wouldn't have paid the same multiple for Gulf Insurance so Fairfax must have overpaid - I think this is speculating. Also Warren Buffet reportedly paid a higher multiple of 2.86xBV to minority interests to take control of Geico. to https://www.washingtonpost.com/archive/business/1995/12/04/a-23-billion-question-on-buffetts-geico-buyout/0c880b8a-d509-4121-b2ac-e50c28a7603a/

Gecio shareholders, she said, got a buyout price of 2.86 times Geico's book value of $24.44 per share as of June 30. The average price recorded for other deals involving property-casualty insurance companies, she said, has been only 1.5 times book value. Book value is a measure of a company's intrinsic value.

-

this is interesting, I didn't realise this but apparently Carson Block is the founder of zeroes tv where he did his interview on Fairfax

https://www.zer0es.tv/about-us/

About Carson

Carson Block, founder of Zer0es TV, is a successful short-seller who has spent his career calling out corporate frauds, through his company Muddy Waters Research. From lawyer to hedge fund researcher and entrepreneur, Block’s experience, particularly in China, laid the foundation for his prominent short-selling career.

-

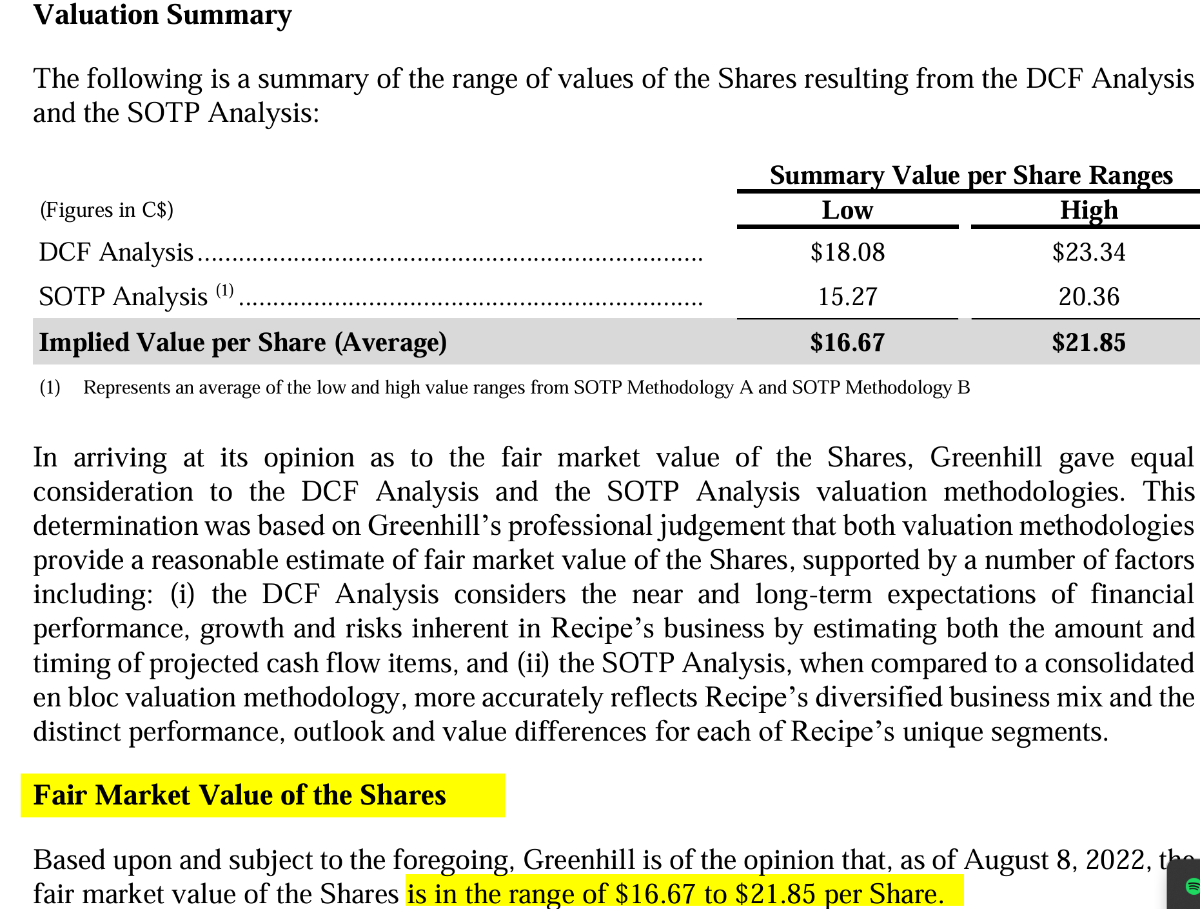

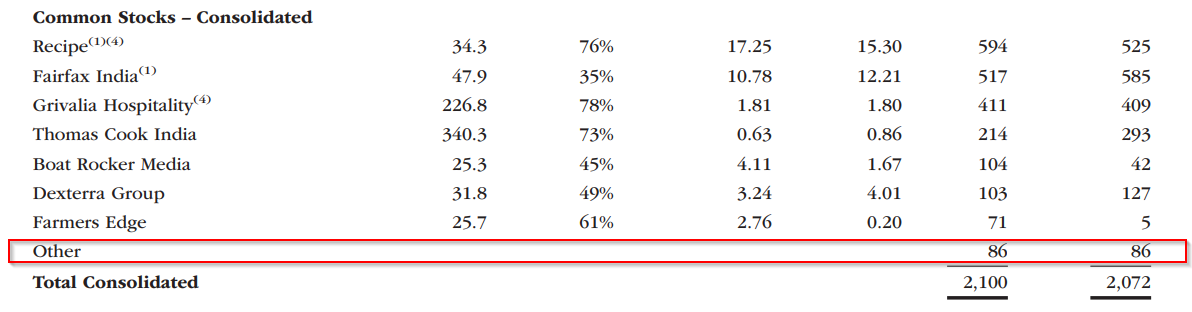

It looks like Fairfax's take private, acquisition offer of CAD $20.73 (US$15.30) for Recipe was within the fair market value range provided by independent valuators Greenhills (see below) who were appointed to give a fairness opinion on the transaction to Recipe's Sellers/Minority Shareholders ie not Fairfax.

The offer price also appears to be close to the mid-point of the discounted cash flow (DCF) analysis valuation for the Recipe's shares and this is what Fairfax use for their market price for Recipe for FY2022.

-

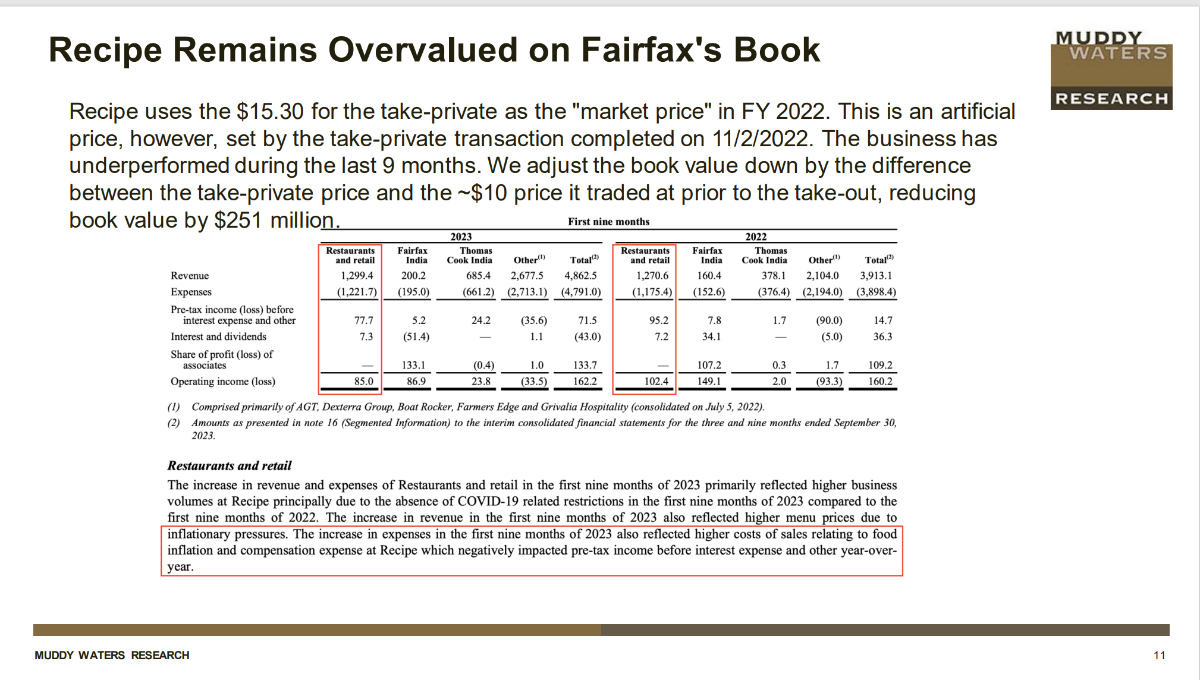

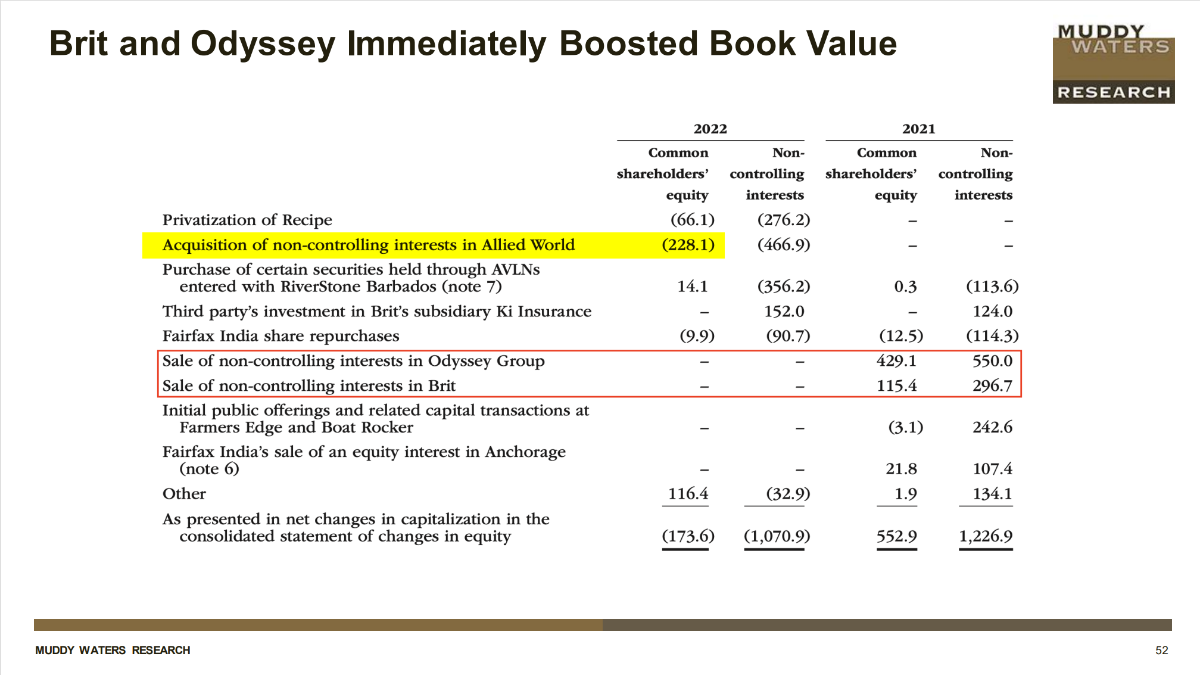

the repurchase of minority interests in Allied World in 2022 (highlighted in yellow) reduced book value, but I can't find this in MW report

-

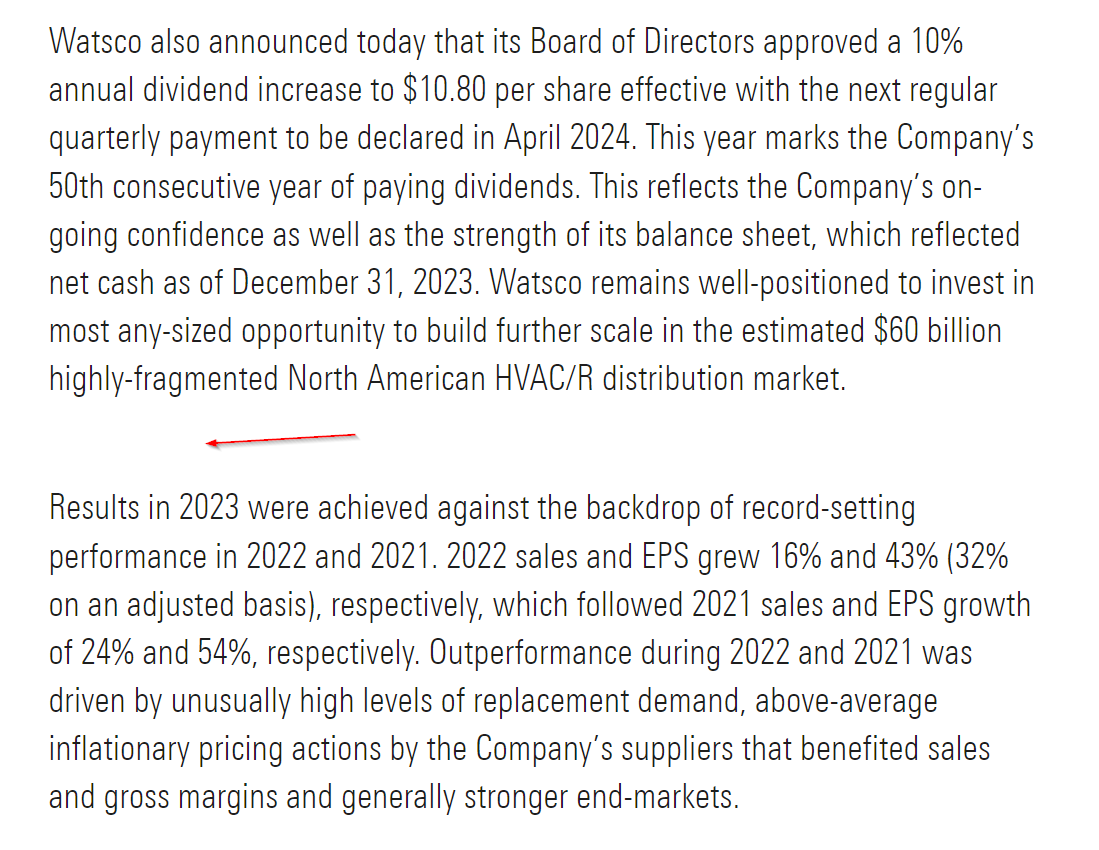

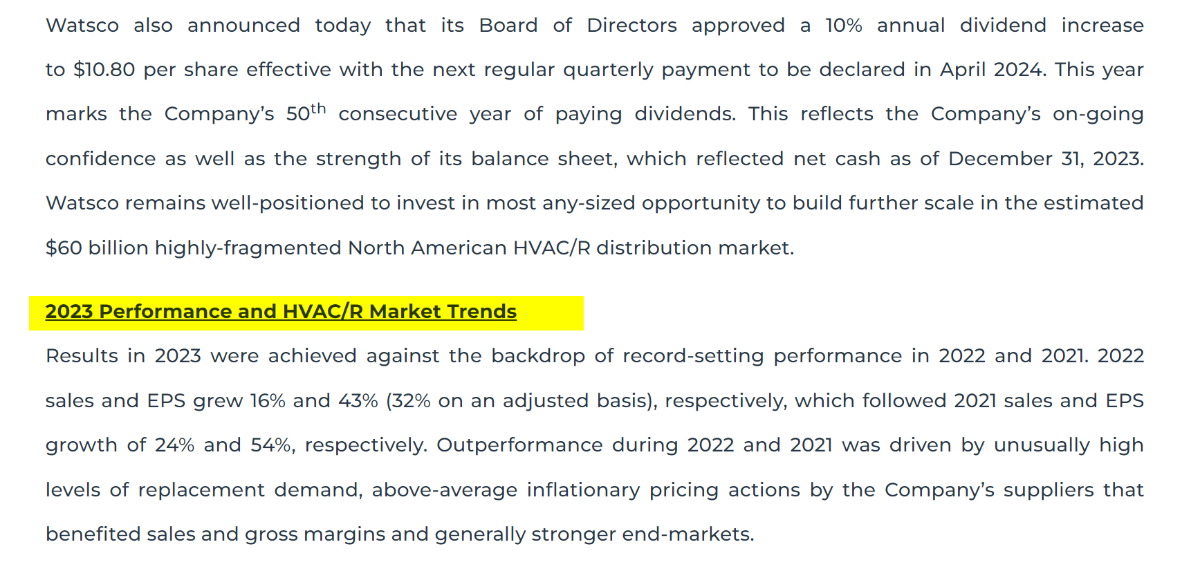

Here is a press release for Watsco on morningstar site & the underlined words are also missing as well - so it looks like this is a system wide issue

-

51 minutes ago, Hoodlum said:

That is not a good look. I have a hard time understanding how that could have been a typo.

it could be coding error

-

58 minutes ago, Tommm50 said:

I notice a significant difference in the percentage change in the stock price on the OTC U.S. stock and Fairfax on the Canadian exchange. I'd guess it's the forex rate difference between U.S. and Canadian dollars but the seems like a lot. Any comments?

I would suspect CAD weakening close to 1% against USD

-

3 minutes ago, SafetyinNumbers said:

I agree. I sent an email to the company. Hopefully, they follow up. I dismissed the Morningstar conspiracy theories but now I wonder.I just sent an email to morningstar as well

-

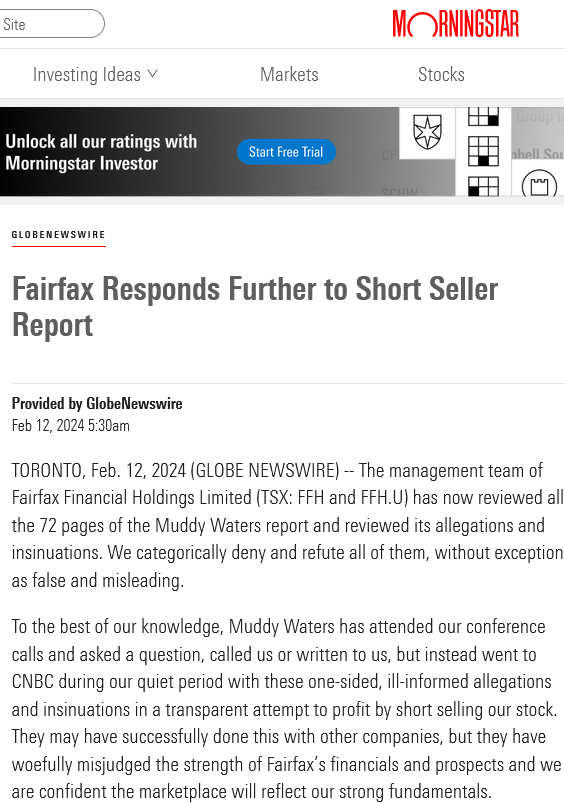

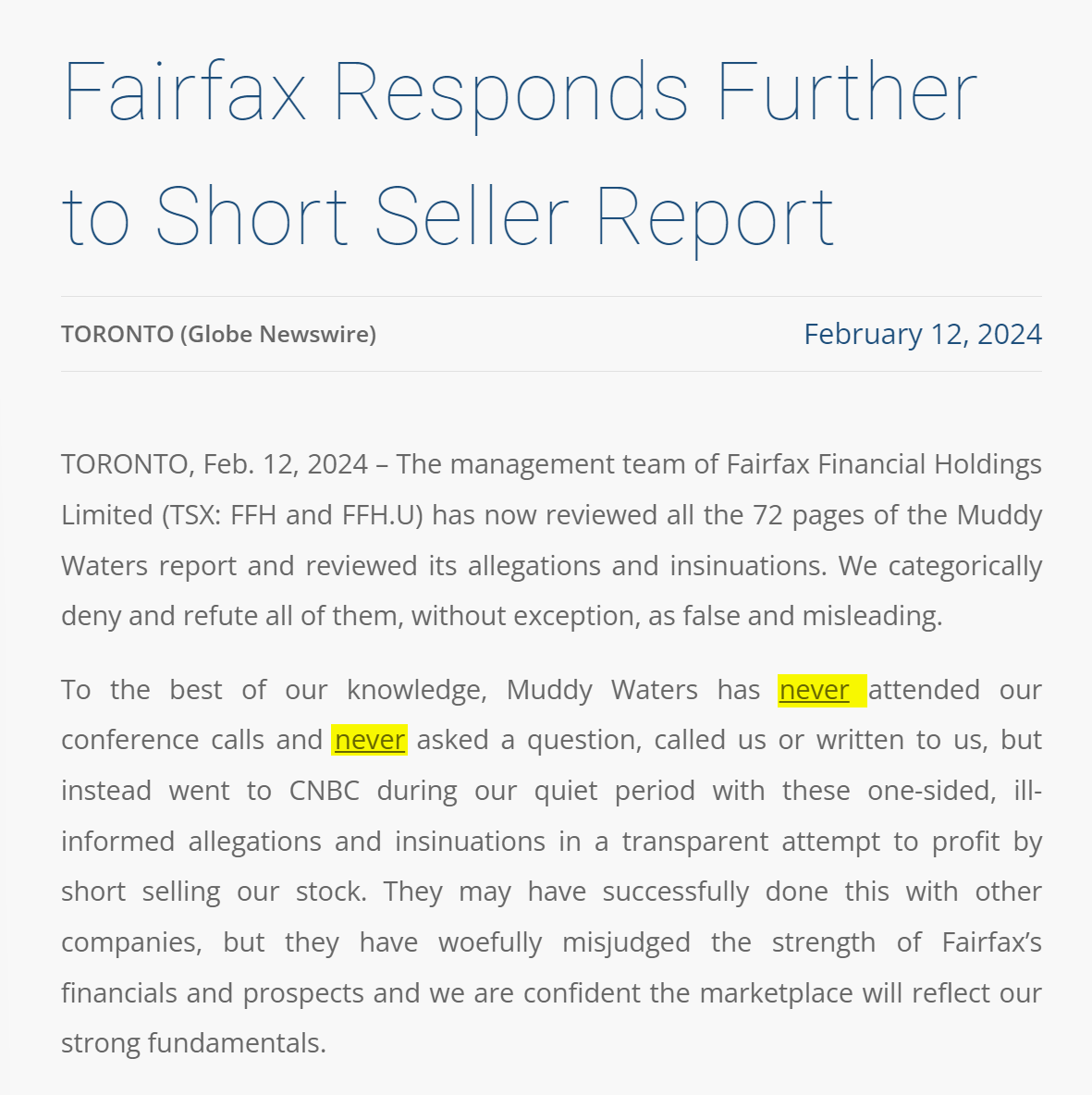

3 hours ago, Haryana said:

Morningstar newswire on Fairfax response is missing the word "never" in second paragraph,

making it sound wrong while any other financial website you go to have the correct wording.

well picked up - I highlighted in yellow from original press release from Fairfax below

-

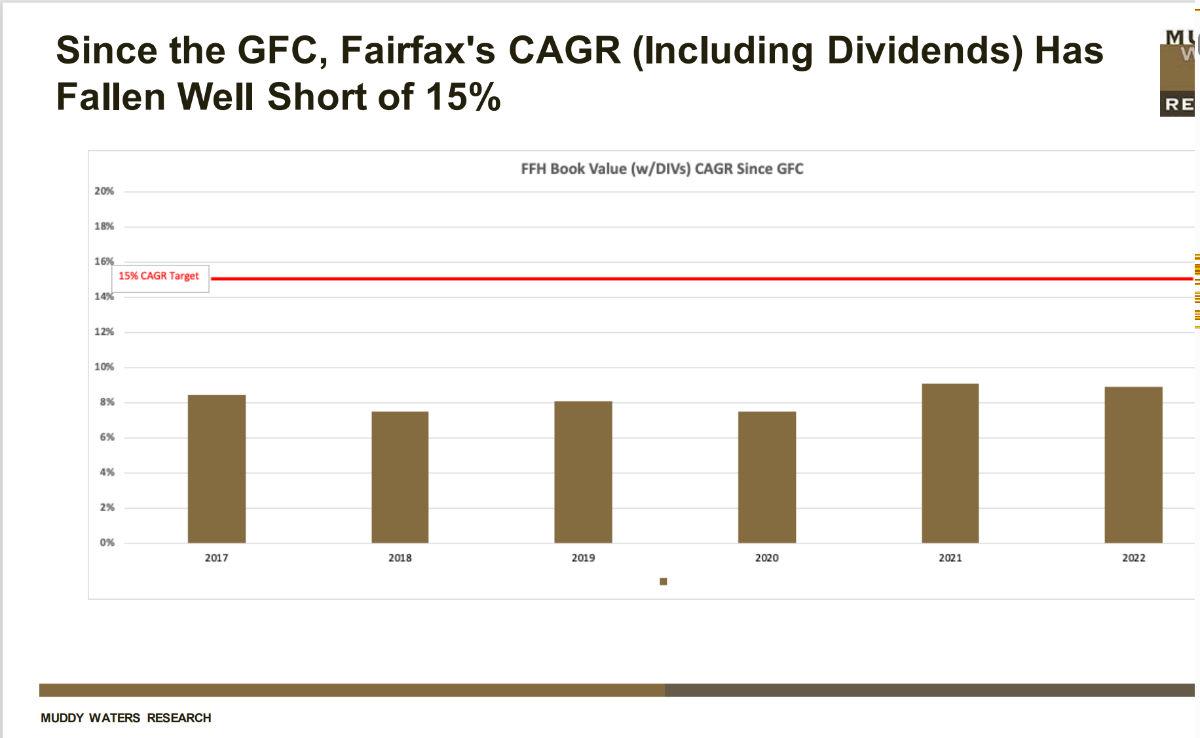

31 minutes ago, gfp said:

The Muddy Waters graph of book values appear to be each year's CAGR in Book value since some arbitrary day they are calling "the GFC." So it isn't the book value growth for those years, but those end-dates.

The actual BV growth for those years (which is probably what most casual observers understood it as) was this:

2017: +24.7%

2018: -1.5%

2019: +14.8%

2020: +0.6%

2021: +34.2%

2022: +6%

(and 2023 comes out this week and should look pretty good)

* one thing about posting Fairfax's actual annual results as above is that the bumpiness goes against the narrative that this is a GE-style smoothed manipulator.

yep the narrative - I looked at the chart & thought it looked odd

-

34 minutes ago, nwoodman said:

https://www.fairfax.ca/press-releases/fairfax-responds-further-to-short-seller-report/

To the best of our knowledge, Muddy Waters has never attended our conference calls and neverasked a question, called us or written to us, but instead went to CNBC during our quiet period with these one-sided, ill-informed allegations and insinuations in a transparent attempt to profit by short selling our stock. They may have successfully done this with other companies, but they have woefully misjudged the strength of Fairfax’s financials and prospects and we are confident the marketplace will reflect our strong fundamentals.

Prem Watsa, Chairman and CEO of Fairfax, commented: “We are neither Berkshire Hathaway, nor GE, as Muddy Waters suggests. We are Fairfax, a strong and enduring company built over 38 years, committed to integrity, customer service, employee welfare and the communities we operate in. We have a unique Fair and Friendly culture throughout our organization. We strive to provide excellent returns to shareholders, and are committed to providing full disclosure in our annual report, highlighting both our pluses and minuses.

great response- liked '“We are neither Berkshire Hathaway, nor GE, as Muddy Waters suggests. We are Fairfax..."

-

Looking at MW chart table below for years 2017-22 - how does that reconcile with Fairfax's number from their 2022 Annual report for 2017-22 period? Or am I missing something?

-

1 hour ago, Viking said:

Murad Al-Katib, President and Chief Executive Officer - AGT Food and Ingredients.

On September 19, 2023, Murad gave a 75 minute talk to his Alma Mater, Edwards School of Business in Saskatoon, Saskatchewan. Great history and overview of the company. Pretty amazing what he has been able to accomplish.

Click the link to watch the YouTube video:

https://youtu.be/DzE9ypecdI8?si=cxvsU3EeXoXGzELc

AGT 'reported sales' in 2022 = C$2.8 billion (the slide below is from the video)

In Fairfax’s 2022AR, Prem said AGT had EBITDA of C$150 million

Do board members have any thoughts on how this company should be valued? Fairfax owns around 60%. It seems to be in a perennial growth phase where everything is getting reinvested in the business.

cheers Viking - looks like Fairfax were carrying the equity portion of 58% AGT stake at $57M in 2020 & then in 2022 it is potentially included in 'other consolidated' category but we can't confirm as this is not broken out

2020 AR

2022 AR

-

Looks like Chou Associates Mgmt retained Kroll LLC to provide an independent valuation of their Exco shares at 31 Dec-22 & mean price was US$21.08 per share.

This is above Fairfax's carrying value of Exco of US$12.59 per share at 31 Dec-22.

See below comment on OTC market pricing of Exco shares

-

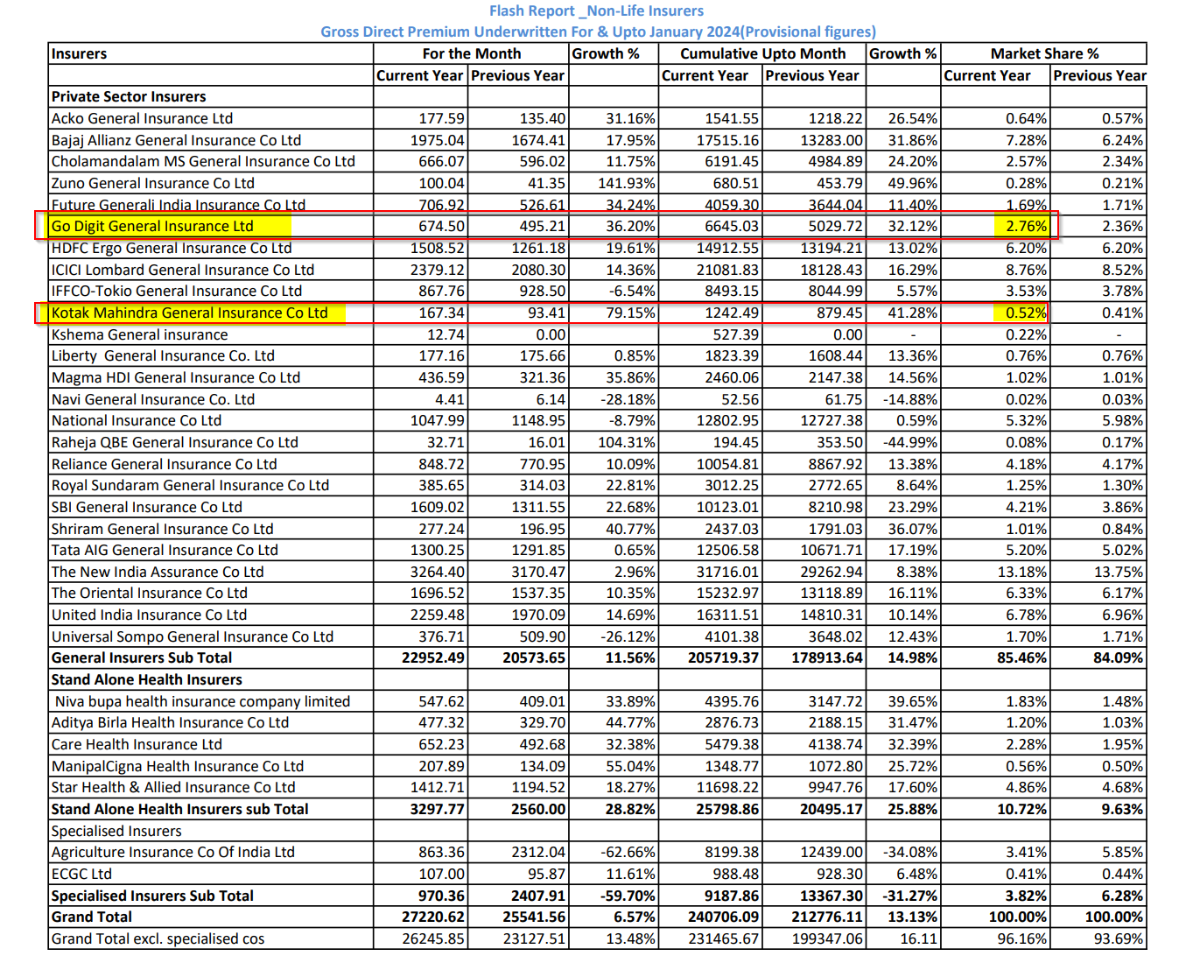

From a valuation perspective, here is an interesting recent M&A/transaction comp for Digit.

In Nov-23 Zurich agreed to acquire 51% of Kotak General Insurance for US$487M for an implied valuation for 100% of Kotak General Insurance of ~US$955M

https://asiainsurancepost.com/archives/48809

https://yourstory.com/2023/11/zurich-insurance-to-buy-51-pc-of-kotak-general-insurance

Digit is writing about 5x more GPW than Kotak YTD & 4x more GPW for current month.

Digit has ~2.76% market share vs Kotak's ~0.52% mkt share according to recent flash figures below (below) - Digit's YTD growth rate is 32% vs Kotak's 41%, but Kotak is also coming off a smaller premium base.

-

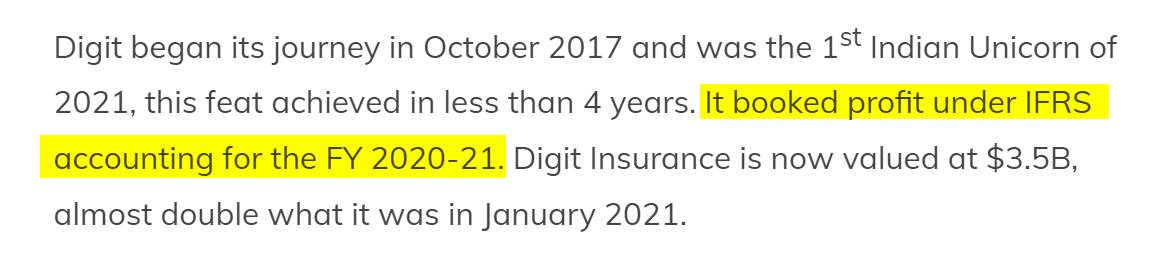

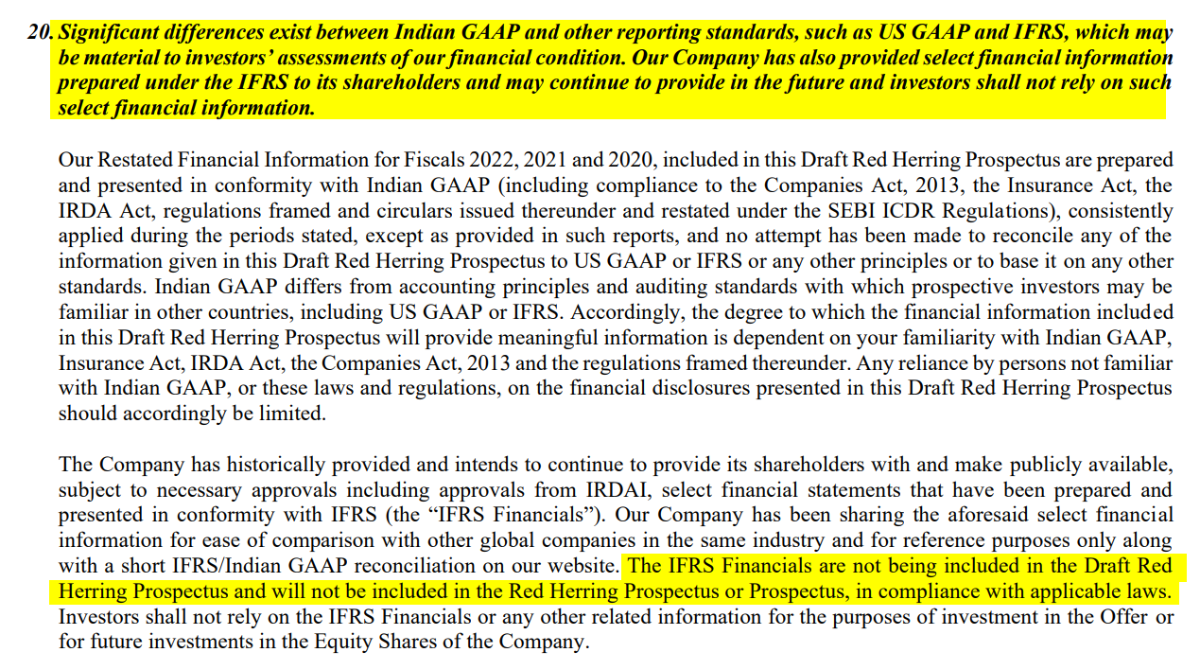

https://www.godigit.com/digest/stories/digit-funding-press-release

The key word is IFRS - Fairfax reports Digit results under IFRS but Digit reports under Indian GAAP. As per below, there are 'significant differences'.

Below Digit indicate that they cannot by law include IFRS Financials in their IPO Prospectus (excerpt below), but they plan to make IFRS financial data available after IPO for ease of comparison with other global companies in the same industry.

-

6 hours ago, SafetyinNumbers said:

Thanks for sharing Glider! Was a good listen.

Overall, the commentary on culture was very interesting and encouraging. I think the most disappointing parts to me were that they think markets are efficient and they manage money the same way they did at Schroders. I think FFH best chance for significant absolute returns is not acting like everyone else and taking advantage where others have constraints that FFH doesn’t.

Fairfax India new issue

in Fairfax Financial

Posted

reported last year, but Air India are ramping up their fleet too

https://www.reuters.com/business/aerospace-defense/air-india-firms-up-order-with-airbus-boeing-470-planes-2023-06-20/