Thrifty3000

-

Posts

637 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by Thrifty3000

-

Growth doesn’t just come from new housing starts. With 39 million people comes about 39 million mattresses, of which, about 3 million of them have to be replaced every year. Sleep Country currently sells about one out of every three mattresses purchased in Canada. That means they have opportunity to triple their domestic market share before even having to worry about selling mattresses to the world’s 8 billion other sleepers. Over the last 10 years they have not only grown store count, but they have also grown via acquisition - acquiring competitors as well as companies with complimentary product lines, like fancy pillows and fancy weighted blankets. Being the largest scale provider in Canada that’s also owned by a large financial backer will provide important competitive advantages. They will now be able to ramp up new stores, acquisitions and marketing at whatever pace they can justify to Fairfax (and these factors were well scrutinized by FFH during negotiations and diligence.) I suspect the base case expectation is to grow the value by 15% annually over at least the next decade, or the investment committee would have black-balled it. Notice some of the main reasons Sleep Country’s profit declined year over year: - acquisition/integration related expenses (hopefully to offer better value proposition) - increased marketing/advertising spend (hopefully to increase sales) - increased compensation (hopefully to attract/retain better talent) ^ those will either positively impact future results, or be reversed if results fail to materialized. I don’t have a problem with them sacrificing some current yield to more aggressively invest in growth. Some other nice things to consider: - in recent years the medical community has been emphasizing more and more the importance of sleep. Sleep is now one of the core pillars of health alongside diet, exercise and stress. If you look at Sleep Country’s mission statement it appears they are positioning the company as an expert sleep solutions service rather than just a mattress retailer. I think it’s a brilliant move that will become a key differentiator if they continue to stick to that promise. (I think sleep solutions providers will enjoy a multi-year tailwind of increasing wallet share as more people recognize the importance of high quality sleep. Who knows, maybe there will be a line of Sleep Country CPAP machines soon. Haha) - I assume several hundred million mattresses are sold annually worldwide. If Sleep Country currently sells a million or so a year, then they have PLENTY of room to run with the right long term financial partner. What if they captured 30% of global market share? Now we’re talkin! Needless to say, I’m happy with the prospects of this one and look forward to seeing what they can do with it long term. I expect it will outperform treasuries, I’m hopeful it will compound by double digits for the foreseeable future, and I’ll be delighted if it does any better than that.

-

I just scanned ZZZ’s financials on Morningstar: - book value has compounded by roughly 15% annually since 2014 - net earnings were basically negative ten years ago and have steadily grown to an average $120 million for the last 3 years - cash from operations has been steadily around $160 million for the last 4 years At first glance it seems like FFH has offered a fair price for a solidly performing asset. Seems like a perfectly good way to further diversify.

-

I read it. It’s consistent with all the other chatter about hurricane risk being elevated this year. However, I’m not so sure insurers - especially Fairfax - are as unprepared as he suggests. It sounds like we can expect increased losses from storm damage this year, however, my understanding has been: - cat prices had already increased by at least the levels he suggested were necessary to absorb a record year of losses. - insurers have pulled way back, or completely exited, high storm risk areas like Florida, which means the insurers have already opted out of the areas - like Miami - that he is most concerned about. - insurers have been able to write policies with much more favorable terms/limits/riders, which will further reduce risk. - in the case of Fairfax, they opted to pump the reinsurance brakes pretty hard during the second half of last year. They backed away from a sizable chunk of business, while they also decided to hold their overall reinsurance volume relatively steady yoy. I assume if Fairfax doesn’t make an insurance profit this year that plenty of its competitors will be in a far worse world of hurt, which would actually be a huge opportunity for FFH to pounce on - while its dividend checks keep flooding in.

-

I noticed Mark Dwelle commented on the article about Fairfax / Muddy Waters.

-

Now I’m feeling better about FFH’s decision to pump the brakes on premium growth in recent quarters.

-

RULE OF LAW + freedom of press/speech + democratic elections + term limits + mostly free trade + excellent geographic advantages + entrepreneurship + upward mobility + good military/patriotism + decent infrastructure + decent education + decent healthcare + decent demographics + decent people = I ain’t complainin’ (much) #’merica

-

50+ year bonds!

-

Fairfax Financial - Volume 2 - 80 of the Best Posts All in One Document

Thrifty3000 replied to Viking's topic in Books

Thanks @Viking! Truly amazing work. -

Simply buying back their own shares yields a double digit return, so if they’re investing in something other than buybacks it has to be a pretty high conviction bet with a high probability of outperforming buybacks. That’s a great problem to have. In other words, what would be the rationale for buying short term bonds yielding 4 to 5% when they know with an unprecedented level of certainty that their own shares will be churning out >10% returns for 3 years and beyond? I think it’s perfectly reasonable to set a 10% placeholder for returns on reinvested capital as long as the stock trades at current levels relative to book value.

-

Sounds like it might conservatively add another $4 or $5 ish per share of earnings annually to what @Viking is projecting.

-

“Freedom has many difficulties and democracy is not perfect, but we have never had to put a wall up to keep our people in, to prevent them from leaving us.” - John F. Kennedy ’Merica!

-

I believe North Korea has the strictest ban on emigration. Other countries, like Iran, make it VERY difficult to leave. Some charge exorbitant rates to purchase an exit visa or passport, making it all but unaffordable for the average citizen.

-

At first governments build walls to keep people out, then eventually they build walls to keep people in.

-

What if Berkshire Charged 2 and 20?

Thrifty3000 replied to weighingmachine's topic in Berkshire Hathaway

@weighingmachine Wow, Buffett would theoretically be worth $300 billion today if he had charged 2 and 20 (all else equal). -

Thanks to this great forum and our worldly friends at FFH, I now know where Cyprus is (here I was thinking it was in Texas). Investing is the gift that keeps on giving.

-

I just back-of-the enveloped the potential per-FFH-share impact of Eurobank’s projections between now and 2026. Am I missing something? These numbers almost seem too good to be true. Looks to me like FFH currently owns $2.8 billion worth of Eurobank. If the stock price simply follows Eurobank’s projected TBV per share then FFH’s ownership will be worth $3.7 billion in 2026. If the stock price grows to 12x projected 2026 earnings then FFH’s ownership will be worth $5.7 billion. Following the above logic FFH’s per share pre-tax gains from Eurobank will be somewhere between $45 and $136 per share between now and 2026. (That’s pretty material since FFH doesn’t include investment gains in projected earnings estimates.) *On top of the capital gains, in 2026 Eurobank anticipates paying dividends of $.19 per share. For FFH’s 1,266,000,000 shares, the dividends will equate to approx $240 million! Or, approx $11 per FFH share!

-

The board gripe is just ignorant. Buffett has gone on record to say most boards are useless, but he says the board structure that seems to be most effective is the one where a family with controlling ownership governs a professional management team (meaning the managers aren't family, and the board isn't dominated by a single person). With that structure there is genuine interest in the best long term performance of the company for its owners.

-

Additionally, hundreds of private deals go across their desks each year, which they analyze. Todd says most of them are deals he wishes he could short. I'm sure the opportunities that do look promising end up getting outbid by private equity.

-

They meet every weekend and discuss any S&P 500 companies selling for less than 15x earnings that have long term growth prospects. It's not rocket science. My guess is there aren't many companies selling for 15x or less, and that there are even fewer for which long term growth can be predicted with any confidence (aka: too hard pile).

-

I think they're grooming Todd to succeed Greg Abel. Todd's a brilliant investment analyst, especially of financial companies. He sits on the board of JP Morgan and meets weekly with Warren Buffett, so he's learning from the best of the best. And, he's running Geico to get legit operating experience (which I'm sure was like drinking from a firehose for him at first). All of that activity hints pretty strongly that Berky is taking his leadership development VERY seriously.

-

Wow. He sounds retarded. At best he has a 100 IQ. I love that his advice for serious MBA students wanting to become short sellers is "don't". What a putz.

-

Back of the envelope: In the annual report it looks to me like FFH is valuing/carrying their Digit holdings at around $2.2 to $2.3 billion. If FFH owns 58% of Digit after the IPO and if Digit’s market cap is around $4.5 billion then the IPO will increase FFH’s BV per share by around $15 pre-tax.

-

If Digit IPOs at $4 bil what will the impact be to FFH’s BV?

-

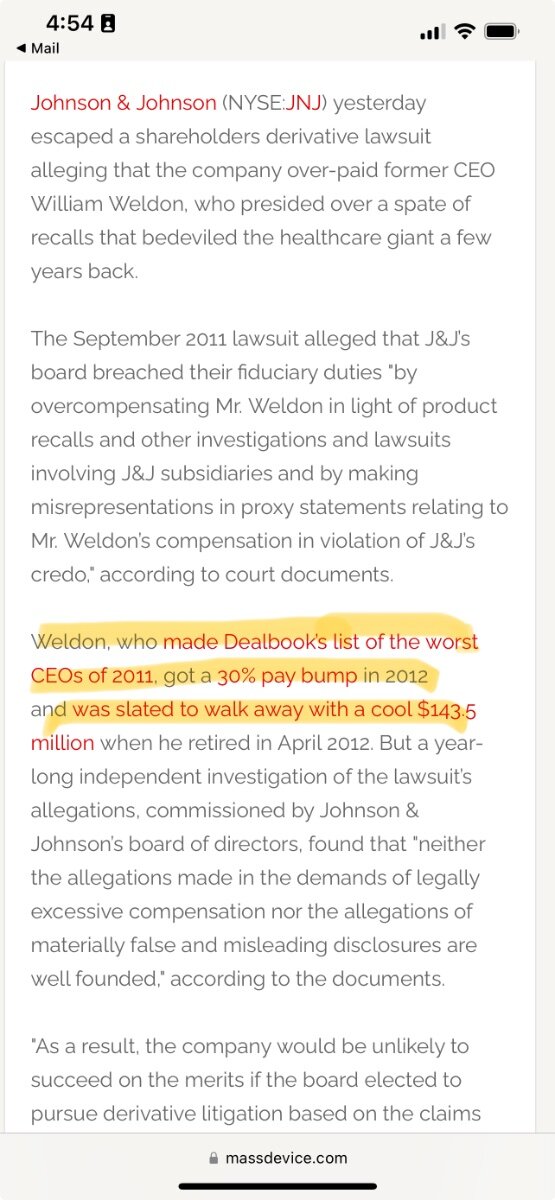

I did some digging on Weldon. Looks like he was at the center of plenty of controversy when he was at JNJ.

-

PS. I bought a few more shares today to bring my position to a nice round number. First, to make it easier/possible to do the math in my head. Haha. Second, because watching this annual meeting further cemented we're sitting on one of the most obvious lollapaloozas we'll see in our lifetimes: EXPERIENCE + INTEGRITY + CULTURE + NETWORK + SCALE + DECENTRALIZATION + GLOBAL PRESENCE + STRONG CASH FLOW + RISK PROFILE + AGILE OPPORTUNISM + CONTROLLING SHAREHOLDER + BENCH STRENGTH + FV DISCOUNT... = LOLLAPALOOZA!