Crip1

-

Posts

749 -

Joined

-

Last visited

-

Days Won

7

Content Type

Profiles

Forums

Events

Everything posted by Crip1

-

So, if 10% of BIAL is worth $225M, then the whole enchilada is worth $2.5B with FFHI's now 64% ownership valued at $1.6B. IF that is the case, then everything else is valued at $173M. What am I missing? -Crip

-

I think MKL gets the premium to BV based on consistency. True may not have done much outstanding over the past decade but they’ve not done much stupid either…that’s a big reason that they’re priced at higher metric than FFH. The MKL investor is concerned more than the average investor with return OF my capital rather than return ON my capital. The thing I can’t get my head around on MKL is Markel Ventures, specifically, what it is worth. Berkshire morphed from primarily an insurance company to an operating company. Markel is still mainly insurance, but operations are starting to be a bigger piece of the pie and, generally, operating companies are going to be valued at higher multiples to BV than Insurance Companies. -Crip

-

Two separate and disparate thoughts on this: • As a long-time shareholder who has seen BB negatively impact my net worth, I don’t have any psychological need to get rid of it. The losses on this are in the past, and nothing can change it. • BB has always been in my “too hard” pile so I have no idea if the true value of this company is the current share price or somewhere north or south of current share price. So, bottom line, if this can “unlock” some of the value, so be it. If it can be sold with the capital being redeployed into buying back shares, buying out minority interests or better investments, so be it. I’d rather not sell just because it’s adversely impacted the company. -Crip P. S. That said, like most all of us, I really wanted them to sell when it was a meme stock back in 2021.

-

Same for the upper midwest as the snowpack is higher than average. Can't recall the year but a few decades ago we had a similar situation. Once spring arrived, heavy rains were exacerbated by snow-melt runoff which caused a boatload of river flooding. That said, I've no idea the level of FFH's exposure to this. -Crip

-

I'm not sure I see why this is the case...anyone? -Crip

-

Analysts starting to get it...the final paragraph looks like all they did was read Viking's posts. -Crip

-

Likewise. The one surprise that popped out at me is the average duration of the bond portfolio being unchanged from the end of Q3 as I would have guessed something closer to 2%. It compels me to think that they (Bradstreet) still sees inflationary pressures and, accordingly, did not see the benefit of locking in longer-term yields in Q4 of 2022. That did not look to be the right move in January but so far in February the story has changed. -Crip

-

Prem's statements about relationships were quite interesting as they really apply in multiple areas, business-related and otherwise. The one point that he missed that is vital, however, is that of trust. Maintaining relationships is all fine and dandy, but if the people with whom we look to establish, maintain and build relationships do not have a level of trust in us, those relationships will be borderline meaningless. For Prem, my guess is the trust/integrity factor in dealing with people is almost like breathing so he does not mention it here as it's second nature to him. (Now, I do wish he spoke with more candor in his letters to shareholders as opposed to being the eternal optimist but that's an entirely separate discussion). -Crip

-

From the Q4 Markel press release: Development on prior years loss reserves within our general liability and professional liability product lines in 2022 was impacted by broader market conditions, including the effects of economic and social inflation, and was most pronounced on the 2016 to 2019 accident years, which was before we began achieving significant rate increases for these product lines. There's a yin and yang to this. First, one has to think that as time goes on this (economic inflation) is going to be seen throughout the industry. This has to have a negative impact on loss ratios for everyone which will negatively impact earnings for the foreseeable future. At the same time, this will either delay the end of the current hard market or mitigate the "softness" of the market. It is going to impact the whole industry and, like other macro trends, some companies will navigate it better than others. -Crip

-

That's damn right.

-

So, yeah, we had to figure this was coming. And while I agree with upgrading FFH as it is my largest holding, this is really another example of Wall Street advisors using the rear view mirror approach. The main difference between FFH now and FFH 3 months ago is the 30% increase in share price. It's the same damned company that was rated neutral at US$490 but is now rated outperform at US$638. It's back-asswards, -Crip

-

Was thinking the exact same thing... -Crip

-

Is anyone seeing a reason for this? Volume does not look to be extraordinarily high. -Crip

-

Just finished this book yesterday. I would highly recommend this to most folks. The abject narcissists out there would not benefit from it, however. The author did not speak much to what compels individuals to not use a checklist, but I feel that's a pretty important part of the equation. In my opinion, it's really an ego thing, and all of us suffer from that to one extent or another. We all have a tendency to overestimate our intellect, our memory or our aptitude. Accordingly, we don't feel the need for checklists. In reality, even the most brilliant and disciplined among us would benefit from using checklists for multitude of applications. The reason we don't is because we feel we don't need it. Bottom line, we all need it. This applies completely to investing, and I'm really looking to develop a checklist (though I'm not against leveraging off of a previously developed one). -Crip

-

@MMM20The oil company comparison is not a perfect one, granted, but the concept of selling the product in the future for less than it is selling for now is similar between the industries. It is not a question of if the hard market in P&C Insurance is going to end, but when and how severely it will end. As the economics are presently, the industry is sure to attract new capital and any new entrants into the space have one big way to differentiate themselves and that’s with price. The market will soften, so profits are going to decline. And, in the past, the market softening has resulted in the industry as a whole eating capital which is going to drive down earnings (even taking into account the investment portfolio throwing off significantly more cash than we’ve ever seen at FFH) resulting in the P/E moving higher, even assuming the same share price. History does not repeat itself, but it rhymes. @Viking Before responding, I do want to echo the sentiments of many others regarding the insights you’ve shown on this message board. You’ve done a great job making a complex analysis easier for many of us to understand and, for that, you have my sincerest appreciation. Your point about the BV now being notably different (higher quality) than the BV from 10-15 years ago is not in dispute and does, admittedly, show the limitations of using it as a valuation tool. P/E valuation has its limitations as well due to the lumpiness of FFH’s earnings and the inevitable Cat losses as well as the inevitable softening of the market. -Crip

-

Two separate thoughts: Seeing a declining P/E in a hard insurance market is similar to when oil companies see the same when oil prices are rising. Insurance companies SHOULD see outsized growth in earnings when the market is the tide rising all boats. This decline will bottom out and, eventually, move higher. The question is whether it will be due to increasing market value or decreasing earnings, or both. Though others disagree with this, I still see the price/BV metric being the best way to value FFH. Buffet said years ago that intrinsic value of BRK roughly follows book value over time and it seems to fit with FFH as well. The good news is that intrinsic value has been growing in a few areas which are not reflected in Book Value, the pet insurance business and Digit being prime examples. The P/E graph suggests that FFH would be worth 2-3x what it is currently selling for assuming a reversion to a P/E of 20, and I don’t think that’s accurate. I do think that it’s worth a 25% premium to BV, which is about 20% higher than it is right now, more or less. Furthermore, as has been pointed out multiple times on this board, there are several catalysts for further improvement in BV so, yeah, I’m holding it. -Crip

-

What are you listening to ? (Music thread)

Crip1 replied to Spekulatius's topic in General Discussion

40 years ago I was 19. If someone would have told me back then that 40 years from now I'd be digging on Mongolian heavy metal, I'd never have believed it. But, oddly enough, here we are. Saw this band live with my son and a buddy of his and had an absolute blast. Does not matter that it's not English... -Crip -

What are you listening to ? (Music thread)

Crip1 replied to Spekulatius's topic in General Discussion

It really is a magnificent song. -Crip -

Based on FFI's share price today. I'd personally appreciate a heads up on your next move. -Crip

-

I am considering subscribing to Seeking Alpha and would appreciate the thoughts from other board members on the relative merits of the service (or various subscription levels). There seems to be no limit to "stuff" on the site to be sure, but I can't gauge the usefulness of said "stuff". Thanks much. -Crip

-

I own all three, and each of them are in my top-5 holdings. FFH is selling at a much deeper discount to BV than the other two which makes it a more compelling buy, all things being equal. In reality, though, is that all things are not equal with the following being among the inequalities. • FFH has historically more big-bets compared to MKL/BRK such as MBS shorts in the aughts and equity hedges a decade later. Markets prefer consistency. • The communication from FFH, IMHO, is not on par with MKL/FFH. Prem tends to be a cheerleader for his company as opposed to Buffett who willingly acknowledges his mistakes and downplays his accomplishments. Markets like candor and generally don’t like cheerleading. • FFH’s longevity of disciplined and profitable underwriting is not on par with the other two. Markets like demonstratable performance. It comes down to this…if you believe that FFH’s future business performance (underwriting and capital allocation) is going to be close to the last 5 years as opposed to the preceding 15 or so (excluding the MBS bet) then FFH is the better investment, especially considering that BRK has gotten so enormous that market outperformance is very difficult. FWIW, I currently have a larger position in FFH than the other two. -Crip

-

1) This is a great time to reduce share count, but I'm not positive this is the best way to do it. 2) My understanding is the subs have sufficient capital to write their business and then some, so I don't think this is even necessary right now. 3) I like this as well, the return on this in terms of eliminating the interest payments is solid, additional earnings are then gravy. 4) Better now than 8 months ago, but I like other options more. 5) The general mood of the market, the past week notwithstanding, is still negative. They should be able to snap up some shares below UD$500. -Crip

-

Many others, myself included, have been saying this for a while. It was overdone when it fell from US14 and change down to $11-$12, and it's not stopped. I don't disagree with anything you've said but there are times when I do start to wonder if the market sees something that I don't. As far as what to do with the proceeds from selling IIFL Wealth, unless there is a screaming bargain out there, I'd love to see another Dutch Auction. -Crip

-

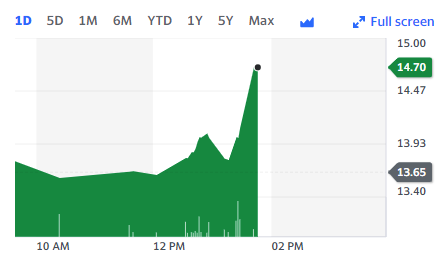

Ummm...up 10% today on seemingly normal volume with no news that I can see. What did I miss? -Crip

-

I'd be happy with cash put to work with 2-year treasuries...don't see the benefit of pushing durations out appreciably longer at this point. -Crip