tnathan

-

Posts

205 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by tnathan

-

Not the ideal ending outcome for shareholders - bought at book but if you've been buying more on dips its worked out ok

-

Yes - I was looking at banks that trade at fair or depressed multiples of book value that have a clear path to growing book value if rates come down. I own FFBB, unib, and hifs. I think all 3 have good management teams

-

Agreed but barring a forced breakup of the companies I think the risks are limited. Everyone hates healthcare but we don't actually have the political will to change how its working in substantial ways

-

I've decided to make a collection of the non Medicaid health insurers 15-20% of my portfolio. Major risk of (a) change in government policy, (b) utilization / loss rates being materially higher than estimates over more than a few years (c) some other major competitive change in the value chain I think are extremely low - with (a) being far lower now than maybe a few years ago with both parties showing no interest in changing the status quo. I think buying as a basket gets you a pretty easy 10%+ per year especially with a few of the MA players (CVS, Humana) now trading at value prices. If multiples ever go up from ~10-12 EV/EBITDA that's a kicker

-

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

tnathan replied to tnathan's topic in General Discussion

Does anyone have thoughts on TWFG? They IPO'ed in July here is the s-1 https://www.sec.gov/Archives/edgar/data/2007596/000162828024029560/twfginc-sx1.htm -

Per the Fed, terminal rates are not going to be as low as they were previously, but I still think HIFS grows book value ~10-15% per year and will trade up to 1.5x+ of TBV/share as rates fall so there's still plenty of room to run. When the mortgage business picks back up UNIB will truly be a monster their CEO is really sharp

-

Biggest 2 purchases for me were a couple banks - HIFS and UNIB. Both are extremely well positioned as rates are cut further

-

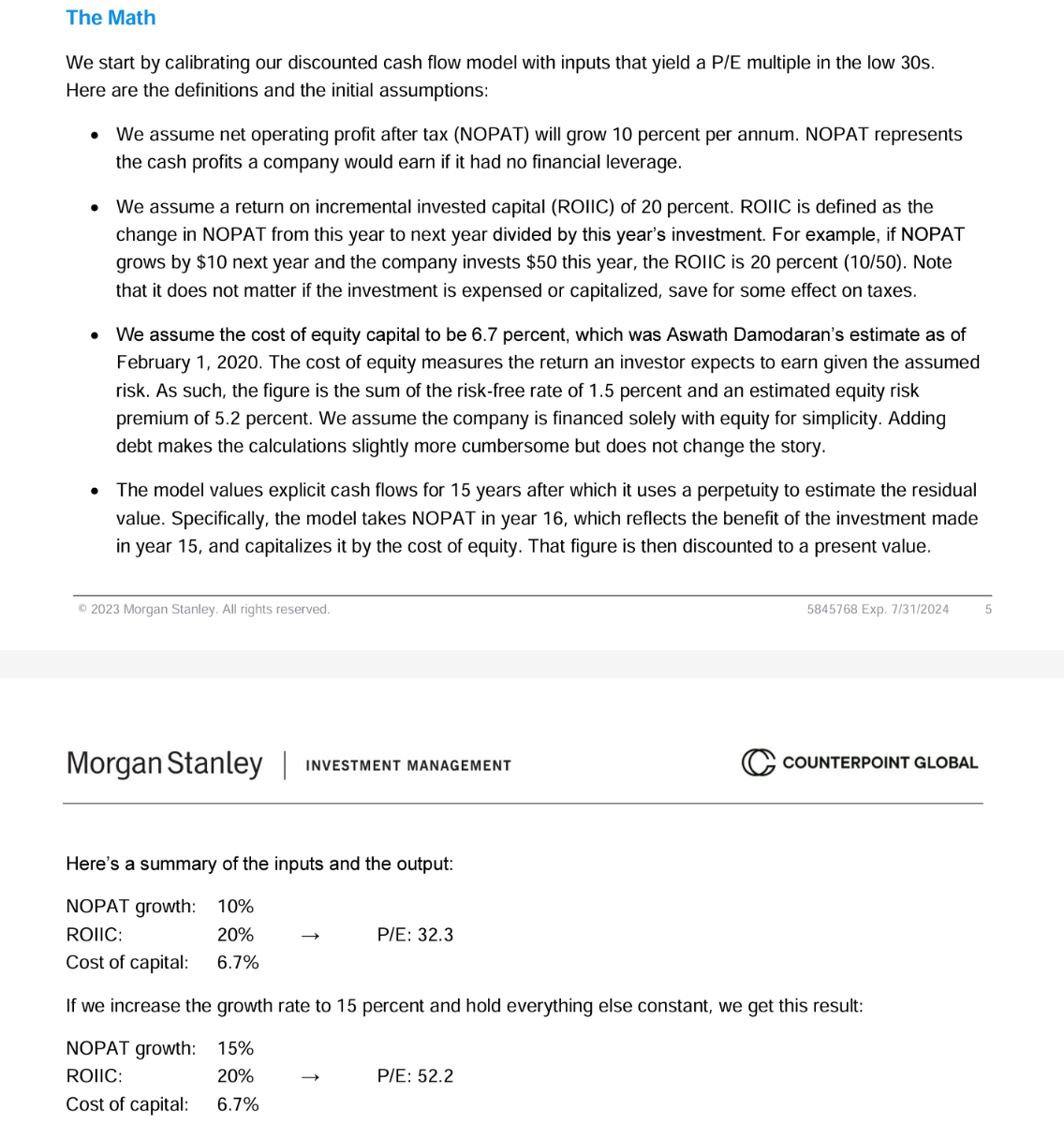

Thanks for the input everyone! I think I understand. Completely get that it is just a useful high level exercise to show how ROIC and growth interplay with each other but obviously these growth rates in perpetuity don't reflect the real world

-

It's definitely my ignorance, but I'm still having trouble translating this into the matrix. Essentially I understand the concept of ROIC and ROIIC and how it interplays with growth, but my trouble is converting that qualitative understanding into an actual solid understanding of what a fair price to pay is. I've seen multiple of these matrices, even ones that Mauboussin has but they never spell out the math behind the concept. Below is an additional Mauboussin excerpt. Can someone dumb the math down and show me simply???

-

Hi - was reading the piece "ROIC – The Underappreciated Variable in Valuation" from Kennedy Capital Management and am a little confused on the math behind deriving the chart I pasted below. Can someone show a simply DCF with the inputs listed and how that would convert into the investment multiples cited? https://www.kennedycapital.com/media/ROIC-–-The-Underappreciated-Variable-in-Valuation.pdf

-

HIFS - big position. Can't think of another bank who needs rates to go down more and the valuation is very fair for a bank that will grow TBVPS quickly as rates go down.

-

ADSK - the management team is a little clueless but its a great asset that is doing well being sold off for reasons not core to the business

-

SMART - this is going back to book when they start buying back all the shares

-

SN, FFBB, UBAB

-

ADM - I think the market cap reaction is too much for what is likely a small misstatement...stock will be under pressure until investigation is done. WABC - Bank with potentially the best deposit base in the country. 2x tbv is cheap for this -> typically trades at 3x+ tbv given how consistent this bank is. Mostly a levered bond shop and not a traditional lender so doesnt have as much risk as other banks (only duration risk, which has hurt, but doesnt matter as much for them given the low cost deposits)

-

Elon needs more Tesla stock to motivate him

tnathan replied to ValueArb's topic in General Discussion

People can hate on Elon for being a weirdo and really full of himself, but idk how you could call the initial 2018 share package a mistake. The stock was trading in the $20s back then and has since 10Xed. So yeah, he's got a huge ego and a lot of the success can't just be chalked up to him, but give credit where it's due. This is not about cow-towing to CEOs vs. withholding from normal employees. The guy is special at what he does and the results speak for themselves. He might be "distracted" but he still 10xed the shares so its a bad argument. I'm sure the next time he asks for shares he will again have to have proved that he has produced results, or he won't get special treatment -

Thanks all!

-

APPF - this is in the same bucket as my PCOR and ADSK that I've been building. Might not be the fastest grower, but the runway is so long within the SMB segment and APPF's ability to move upmarket and challenge inferior competitors in the enterprise segment will ensure this is eventually a $20B stock. Don't know when it'll happen but it will.

-

Does anyone know of any fundamental funds / investment managers in Chicago that they greatly respect? Funds that don't try to play quarterly earnings, that are truly trying to do quality research and understand the businesses they are buying. No need for it to be something super big.

-

Bought a lot of WABC, OFG, and PTLO

-

As an overall note, the earnings of regionals / community banks has been super variable and not surprising. Banks with variable rates loans and relatively strong deposit franchises have been able to keep or expand NIM, while banks that screwed themselves with long term fixed rate securities / loans are essentially screwed for the near term. Some have been biting the bullet and selling securities in order to get into more rate sensitive assets, but it's not totally clear if that is the right strategy at this point (especially if rates start to come down and then you get screwed again if you don't lock in longer term). If you do own banks, it is well worth owning specific stocks and not the KRE etf (or similar) given the difference in performance across the sector. The market has clearly rewarded strong performers, but has also rewarded weak performers, which suggests a lot of the moves in the recent weeks are etf driven. I am buying more OZK, which I've been buying for the past couple months - the results are really incredible and it's not being valued as it should. Great management team as well that is stepping into some of the market paralysis and using excess capital to take share. I think generalist investors are throwing every bank with construction loans out which is not fair to best in class orgs.

-

This is another great read laying out the broader India investment case. I also happen to be in India at the moment (here for a month traveling) and you can feel the energy in the people. As much as the government has problems, it’s clearly making positive investments and spending money in areas that will boost the economy, and people here want to succeed. In many ways I think the positive energy represents what the US has lost in recent decades. https://www.dispatchesfromindia.com

-

Sorry edited - meant to type NIB "non interest bearing"

-

I didn't dig overly deeply into the loan portfolio but it has a higher portion of non interest bearing deposits than some of the other large regional banks, it seems like their management has been more thoughtful about the move up in rates vs. other management (which to me makes me more confident in their ability to stay flexible in what will be turbulent times). Perhaps the commercial real estate exposure starts to bite them, but I still think their overall profile is more attractive (even more so when you take into account the lower valuation)

-

I strongly agree that the most important metric right now is understanding the deposit base of specific banks. When we think about book value, the deposit base composition is not included directly in the calculation, but we really should be thinking about it in the same way (just in the reverse) as we are thinking about the mtm losses on the security / loan portfolios on the asset side. Low cost / NIB deposits are worth a TON in this environment, and there are some banks (very few) which have an outsized advantage...check out SBCF and PFS for two good examples of smaller banks. I personally would be far less concerned with the lending portfolio right now, as I don't think that has as large an effect on the next few years as the deposit makeup. Banks with the strongest NIB deposits are going to be able to keep some (not all) of their margin profile which will help protect them when we start to seen higher loan losses...whereas I think you'll start to see huge margin compression on other banks that might screen "cheaper" at the moment over the next year and therefore might not be cheap at all