MMM20

-

Posts

3,354 -

Joined

-

Last visited

-

Days Won

14

Content Type

Profiles

Forums

Events

Everything posted by MMM20

-

@Viking my only comment would be to hide gridlines - ALT WVG (yes I still have investment banking PTSD)

-

I agree! The family control + massive skin in the game —> management for long term wealth creation, not income statement optics really is a massive and durable competitive advantage. Permanent owner style value investing + float = structural durable high returns through cycles. Sort like an individual investor with a 3% 30 year mortgage and no asset/liability mismatch (no quarterly or annual client liquidity to worry about)… but on steroids! They’ve proven that over almost 4 decades and we saw it play out in a big way over the past ~5 years. It seems to me that from this point on through cycles they should durably and structurally earn a ~400-600 bps spread on their mostly cash/ short term fixed income plus some longer duration investments, vs roughly zero or slightly negative borrowing cost. So therefore the recent float growth has added ~$1B of structural earning power that did not exist ~5 years ago, driven by savvy insurance acquisitions/turnarounds —> growth into the hard market. (BTW that incremental earning power would be roughly zero if they’d had to issue ~6-8% debt to finance all that incremental growth after the acquisitions!) Looking forward, that growth alone is worth an incremental $500+/share which is not reflected properly in accounting BV. IMHO that is the core of the opportunity! That’s my best Prem impression!

-

@SafetyinNumbers@Parsad I respectfully disagree! All that matters in the intrinsic value calculation is the net present value of distributable cash flows to a permanent owner. So all I care about is the core cash flowing power and how it will be retained and reinvested. That will of course drive growth in book value, but that’s a lagging output. Aren’t low cost commodity producers classically great businesses? That’s about as volatile an earnings stream as you can get! And if one ever trades at a low multiple of mid cycle earnings, isn’t that an opportunity for value investors? Look at what Buffett is buying nowadays! Let’s say a new company raises $100M and succeeds wildly. They are doing $1B in annual EPS right away with a long runway and wide moat. Do we still value the stock at ~1.5x the ~$100M BVPS because “that’s where peers are trading” - or something else? I would argue Fairfax recently did something like that with its mid 2010s insurance acquisitions. Would Fairfax’s intrinsic value be higher if they replaced their now massive quantum of float with fixed rate debt? Earnings would be lower but more predicable year to year. Would the company therefore be *worth* more? Fairfax should trade at a higher multiple if it has more insurance float - truly an asset and not a liability - due to the impact on cumulative future cash flows - even though they will certainly be *more* volatile! I understand that Fairfax may *trade* at a lower valuation than a company of similar quality with a lower but smoother stream of cash flows, because Mr Market tends to prefer smooth… but isn't that exact disconnect a classic opportunity for value investors? A stock is also not worth less just because GAAP accounting doesn’t slap us in the face with the underlying value. Float is a textbook example - it is an accounting liability but an economic asset. If we are comparing to BRK, Buffett has told us exactly that repeatedly over the years. And if BRK’s float was ~1.5x its equity book value today, you gotta think Buffett would still be writing a whole lot about valuing float. Float is a truly massive economic asset for Fairfax now. NAV is US$1500-2000 per share, and float is a big chunk of the delta to accounting BV. It may appear like theyre be overearning right now, but if you do the work to adjust accounting BV to economic reality, ~$150 ‘23E EPS makes a lot of sense as a normalized number! I think the crux of the opportunity in FFH right now can be best summarized as exactly that: accounting book value significantly understates intrinsic value and mostly because of the massive float growth of the past few years - both how it has changed the core earnings power and what it says about Fairfax management! A business with a durable competitive advantage that earns elevated returns over long periods of time and has ample room for growth should be considered great whether or not (1) those returns are volatile or (2) it shows up properly in GAAP EPS or BVPS. Accounting often misleads the value investor and we have to do the work to get at economic reality. That is true here in an extreme way. Sorry for the long and rambling post. I am right and you are smart so you will see it my way eventually. Is that the munger quote? Lol.

-

Still can't believe that Fairfax seems to trade primarily on book value. IMHO this more than closet indexing, technicals, volume, skepticism about Prem or anything else is why the stock is still so ridiculously cheap despite Fairfax's transformation into a top 20 insurer and cash flow machine...

-

Maybe this should be a DM, but check out https://www.credible.com/home-insurance - no spam calls, first heard about it from Mr Money Mustache https://www.mrmoneymustache.com/mmm-recommends/credible/ - they handled the shopping around part and quite literally saved me ~15% by switching to GEICO (—> Liberty Mutual). No affiliation but delete if too tangential / off topic...

-

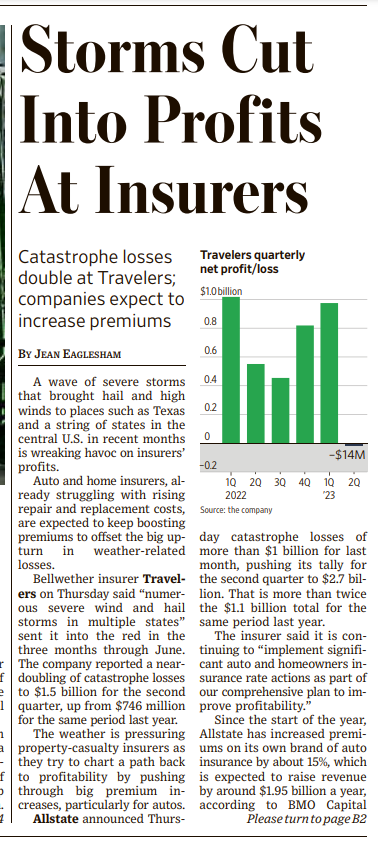

What if the hard market reaccelerates and @Viking's '24/'25 numbers are way too low? https://www.wsj.com/articles/facing-big-storm-losses-insurers-aim-to-boost-rates-f70211d6?st=mu1hv017qtasvf1&reflink=desktopwebshare_permalink

-

Whenever you see a comparison over some specific and arbitrary time horizon rather than something like rolling 3-/5-/10-year periods, you should squint your eyes a little and wonder why they picked that specific period. I think that's a useful thing for every investor to understand and apply across the board.

-

What I’m trying to do is think through this off of normalized earnings looking forward… maybe helpful, maybe not, fair enough. There will of course be extreme volatility around that core structural earnings power and risk of various 100 year floods. But there is also some chance that the outcome is much better

-

If earnings roughly match free cash flow and are at least stable for the next 3 years (as @Viking and others here have argued is a reasonable assumption) then they’ll retain earnings of about 60% of the current market cap depending on the dividend and incremental ROIC (and assuming no buybacks). If they agree the stock is too cheap and keep buying it back, that’s theoretically ~US$10B of buybacks using free cash flow alone over the next few years. If at an average cost of ~US$1000/share that’s ~10M shares. Then even if earnings are flattish vs current as we exit year 3, ok, that’s ~$3.5B / ~12M shares = ~$300 EPS. Even at still just a ~5-6x multiple, that’s a ~$1500+ stock or a ~2x+ from here even with flat earnings. That gets at the power of FFH's now structurally higher earnings yield and good capital allocation.

-

With a high earnings yield, a stable/growing stream of earnings, and reasonable capital allocation, you get a compounder… a real compounder, not just a stock that went from 15x to 50x P/E as interest rates went to 0...

-

Value of BRK Float By the way, a while back, my big thing was that Buffett and others kept saying their float is more like equity, and some even proposed to add float into the valuation of BRK stock. Like, literally, take book value of BRK, and then add to it the amount of float as if it were equity etc. I thought this was interesting, but sort of nuts. My argument then was that this “float” was actually never even invested in stocks or even their operating businesses as, up until that time, the amount of cash and fixed income on BRK’s balance sheet was always around what their float was, and never below it. This was true, by the way, only post Gen Re. And with interest rates so low, I argued that the float is not worth all that much to BRK in that case. It adds some incremental income for sure, but nothing big enough to value all of float as equity. But now, with rates rising, the value of float is increasing. Float at BRK as of the end of 1Q 2023 was around $164 billion, and cash / fixed income was around $150 billion, so it is still very close to the amount of float. But what has changed since my last post about all of this stuff is that interest rates are now in the 4-5% range. OK, so on the short end, let’s say it’s 5%. Assuming all of the cash / fixed income can earn 5%, that’s $8.2 billion in additional pretax income for BRK, or $6.5 billion after tax (assuming 21%). With $500 billion in shareholders equity, that adds 1.3% of incremental return on equity to BRK. If you value BRK at 20x P/E, this float earning 5% will add $130 billion to the value of BRK ($6.5 billion x 20). Well, this is kind of circular; assuming something earns 4% after tax, revaluing it back at 20x P/E etc… Anyway, $130 billion comes to 26% of BRK’s book value. That’s a nice bump compared to when interest rates were 0-1%. https://brklyninvestor.com/2023/07/04/value-of-brk-float-buffett-market-view-etc/ Sorry about another float post…but the market is still way behind the curve on this for Fairfax. The impact of this alone is ~3-4x higher for FFH than for BRK — by my math something like +75-100% to fair value on book value. ~+$1-1.5B of net income = ~+$50 of EPS * low-to-mid teens fair multiple = +$600-800/share vs. prior fair value at 0% short term rates = ~US$2000 IVPS. Maybe normalized short term rates are only 2-3%… but that’s still a few hundred dollars per share incremental to FFH fair value, and then they’re still getting zero credit for the many other recent positive developments.

-

Exactly. And could be higher with the sorts of cash flows they've lined up and the auction buyback playbook.

-

Past is prologue. FFH should still have plenty of good opportunities to deploy capital at higher rates / longer duration at good risk reward. They’ve set themselves up to generate so much cash over the next few years that they probably just need to get the reinvestment roughly right for us to do just fine from ~5x earnings… wake me up at US$2000…

-

ok, good… FIH still near the top of my wishlist

-

Oof, I hope you're wrong about that @brk64311 b/c that's where I own Exor (and would own FIH). I thought the IRS instructions were clear that individual retirement plans are not taxed as shareholders of PFICs, but I am not a tax guy or lawyer... https://www.irs.gov/instructions/i8621 However, a U.S. person that owns stock of a PFIC through a tax-exempt organization or account described in the list below is not treated as a shareholder of the PFIC. An organization or an account that is exempt from tax under section 501(a) because it is described in section 501(c), 501(d), or 401(a). A state college or university described in section 511(a)(2)(B). A plan described in section 403(b) or 457(b). An individual retirement plan or annuity as defined in section 7701(a)(37). A qualified tuition program described in section 529 or 530. A qualified ABLE program described in section 529A. https://www.bogleheads.org/wiki/Passive_foreign_investment_company "First, the Final Regulations modify the definition of shareholder as announced by the US Treasury and the IRS in Notice 2014-28, whereby a United States (US) person shall not be treated as a shareholder of a PFIC to the extent such person owns PFIC stock through a tax-exempt organization or account. This effectively extends the exemption that was already afforded to the tax exempt organization under the temporary and proposed regulations to the US shareholder(s) of such organization, and expands the exemption to encompass tax exempt accounts as well. As a result, for instance, a US person owning stock of a PFIC through an individual retirement account (IRA) described in Section 408(a) will not be treated as the shareholder of the PFIC stock, and in turn, is not subject to the PFIC rules. Because Notice 2014-28 originally provided for the aforementioned exemption, it will be effective for the taxable years of US persons who own stock of a PFIC through a tax-exempt organization or account ending on or after December 31, 2013."

-

can’t you just own in an IRA to avoid all that?

-

Time to sell

-

I think it’s similar to an investment fund with ~250-300% gross exposure and ~100% net exposure. The key difference is that (most of) the leverage is (structurally far superior) insurance float instead of margin loans. So I think it’s most informative to compare each individual investment to the 100% net NAV when I am thinking about the underlying exposures. Digit can really move the needle relative vs FFH market cap — like +20% to FFH if Digit executes and its valuation doubles. The same is not really true right now for the FIH investments within FFH, so I get the argument for owning both…especially if you think the airport is a crown jewel asset about to pop on IPO…

-

Fairfax’s best investment in India so far seems to be Digit. It was made by Fairfax itself and not Fairfax India because Digit is an insurance company. Fairfax’s clearest circle of competence is insurance. Fairfax itself is trading at ~5-6x earnings. That said, until recently to @gfppoint I was one of those who thought FIH was ~15% of the value in FFH b/c I misunderstood the minority interest…it’s really ~3%, while Digit is ~15-20% at this point, incredibly. So I think it’s still a fair point that you get a lot of India exposure within Fairfax itself and FFH shareholders with big positions might not want more. Anyway…I get the case for owning both but I think the unfolding Digit case (and clearer alignment with Prem) is the gist of why many stick with FFH.

-

I’ve been wondering “whats the catch” with the KW deal and saw the following in the JPM transcript. Could the mark to market LTV across the pool be closer to 70-80%? If so, still very attractive for that duration, but the ~10% expected return makes more sense… maybe the transcription is wrong and they’re just talking office… ”So we did a bit of work to understand the dynamics in the real estate market in the last several months. And so the real estate market’s totality in this country is around $13 trillion, $14 trillion, commercial real estate. The average inception loan-to-value was in the low-50s. If you were to do a mark-to-market of that portfolio now at the new cap rates and new occupancy rates and all that so that probably, the loan to value at the moment is between 70% to 80%. So definitively, it has been a deterioration. So an asset class that an insertion was $2.2 trillion, giving or taking, probably now is sometime between $1.5 trillion to $1.7 trillion. The amount of lending against that is $1.2 trillion. That is roughly half by — provided by banks and have provided by the markets, CMBS, some insurance companies, other participants" - JPM call

-

What is the intrinsic value of Fairfax's stock as of today?

MMM20 replied to Viking's topic in Fairfax Financial

I guess I’m still way off in the right tail b/c I think something like ~US$2,000 right now would pencil out to a fair ~10-12% per share expected return. My base case = flattish float growth + 98-99% normalized combined ratio + mid/high single digits return on the investment portfolio + good enough capital allocation => sustainable 15%+ per share EPS growth from a ~15-20% EPS yield starting point. That’s a setup for lollapalooza returns like a leveraged buyout in the early 2000s when the Yale endowment was loading up on LBOs of private companies at low/mid single digit EBITDA multiples that went on to expand and make them a fortune (and then of course the copycats piled in at 3x+ higher entry valuations)… except that Fairfax has better quality and much cheaper (probably free or negative cost) leverage. I still don’t think many people fully appreciate this point. I do understand why people prefer BVPS, but I think in this case and at this time it’s misleading and anchoring investors to much lower than fair numbers in terms of first principles IVPS following Buffett. Even in an inevitable soft market, the float is not going to get cut in half. That’s one way to look at what’s priced in at US$730. The market remains extremely unfairly negatively biased and slow to incorporate new information. I think the stock is still priced for capital destruction and a zero interest rate world. So FFH is priced to a ~30-40% CAGR over the next ~3-5 years, assuming a gradual rerating to a fair and historically normal low-to-mid teens multiple of normalized earnings. If I’m right, I’ll end up with a ~10x over 5-10 years from Jan ‘21 b/c the earnings base has ~3-5x’d over the last ~5 years, things have fundamentally transformed, and yet the stock price still reflects skepticism / disdain. That should slowly melt away with good execution… …and probably a shift, already in motion for the past few years, to a new generation of shareholders who don’t unduly overweight the early/mid 2010s results. It doesn’t bother me that FFH doesn’t have a BRK-like fortress balance sheet. I think that’ll come at some point down the road, and my risk tolerance is high. I am happy for the stock to trade at a heavy discount to IV for years as they flip to highly cash generative and take out stock. Disclosure: talking my book! My biggest position since Jan ‘21 and I recently added ~20% in the low $690s. Probably wrong. Not investment advice. -

This feels like a Saturday morning post so here goes. https://www.rottentomatoes.com/m/blackberry This movie is a must watch for Fairfax / Blackberry shareholders. So good... 98% on Rotten Tomatoes. Helps if you’re a fan like I am of Glenn Howerton and Jay Baruchel.

-

Yes! If you read his reports going back, it's pretty much been the exact same report for like 5 years now. The analysts will turn bullish when the stock hits $1,500 in a couple years.

-

Rate the overall quality of the management team at Fairfax

MMM20 replied to Viking's topic in Fairfax Financial

A few thoughts off the top. They run the company like a true family business / family office. For better and worse. Excellent in turnaround / management of insurance acquisitions. Contrarian and opportunistic. Not afraid to look dumb, e.g. going to extremely short duration when rates were at all time lows (and kept dropping for a while). Family / kids on the Board. Shareholder communication could still improve (fewer words, better explanation of the key drivers, like peers) -

Let's say they underwrite to 105% combined over the next decade with more catastrophe losses but in more historically normal interest rate environment. That's equivalent to borrowing at 5% when literal cash is yielding 5% right now. That’s an oversimplification, but borrowing at even 5% wouldn’t be too bad if a global 60/40 portfolio is priced to return something like 8-10% again. FFH produced some decent returns early in their history underwriting at nearly 110% combined, eh? And still not up against law of large numbers like BRK, where even a $5B profit in Japanese trading companies doesn't move the needle as Buffett and Munger discussed at the AGM. The expected returns math is instructive, but we gotta remember that FFH doesn’t just own the whole market (for better or worse ) and if something like Digit cuts a certain way, FFH could produce silly returns. The reverse is of course true too but still way overstated nowadays IMHO b/c of the lingering stench of the 2010-18 ish performance.