omagh

-

Posts

433 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by omagh

-

https://www.investopedia.com/terms/q/quietperiod.asp "...For publicly-traded stocks, the four weeks before the close of a business quarter is also known as a quiet period. Here again, corporate insiders are forbidden to speak to the public about their business to avoid tipping certain analysts, journalists, investors, and portfolio managers to an unfair advantage – often to avoid the appearance of insider information, whether real or perceived. ..." I believe that BRK doesn't repurchase shares during the quiet period preceding the quarter end as an integrity measure for their executives.

-

Warren strikes me as a paper guy -- he needs a hard copy of things to get into his comfort zone. So somebody has to print stuff off for him or get his hard copies from the office. His process is probably a bit slower. I doubt that he gives out his cell number much either. So instead of someone setting up the conference call for him, he's all thumbs. My Dad would be the same... :) But really, he's probably head down working (reading, thinking, calling his brokers) as businesses are on sale, so why waste time with public interviews and statements?

-

On the asset side, cash decreases by $10B On the OE side, a combination of "Common Stock", "Capital in excess of par value", and "Retained Earnings" decreases by $10B. Starbucks is an example where so much common stock has been repurchased that their Retained Earnings has gone negative: https://s22.q4cdn.com/869488222/files/doc_financials/2019/2019-Annual-Report.pdf

-

Dalio with his thoughts. To be clear, he is talking his book, so a grain of salt is required. https://www.linkedin.com/pulse/implications-hitting-hard-0-interest-rate-floor-ray-dalio/?published=t Long-term interest rates hitting the hard 0% floor means that virtually all asset classes go down because the positive effects of interest rates falling won’t exist (at least not much). Hitting this 0% floor also means that virtually all the reserve country central banks’ interest rate stimulation tools (including cutting rates and yield curve guidance) won’t work. The printing of money and buying of debt assets that central banks are now allowed to buy almost certainly won’t work much (because bonds can’t be pushed much higher and they are also less likely to be sold to buy other assets of entities that are in financial trouble). Further, with this hard 0% interest rate floor, real interest rates will likely rise because there will be disinflation or deflation resulting from lower oil and other commodity prices, economic weakness, and more credit problems. If that plays out in the typical way, rising credit spreads will raise debt service payments to weaker credits at the same time as credit lending shrinks, which will intensify the credit tightening, deflationary pressures, and negative growth forces. God help those countries that have these things and a rising currency, too.

-

Catalyst for BRK from Book Value to New Metric

omagh replied to longterminvestor's topic in Berkshire Hathaway

Buffett's usually strategy is to demand good terms for convertible debt. With an injection of convertible debt at above market rates along with the opportunity to convert debt to equity shares, again at favourable terms, Buffett has been able to pick off some pretty great targets in the past by allowing the balance sheet of the company in crisis to be mended. So, essentially it's a risk-free transaction for Berkshire. Get high coupon income for a period with the opportunity to remove the capital if things don't work out. But if the company performs coming out of the crisis, he further reduces the company's debt/equity ratio by converting to equity and then takes all the equity upside. At the sizes that he puts these deals in place, he often comes out with a 10%+ equity stake. Berkshire can be a bank proxy and take on transactions within a day or two that other banking institutions and private equity lenders would struggle to finish in the time that Berkshire makes the commitment. -

Inflation has been ticking along, so it would take a big deflation thump to move the indices. source: https://inflationdata.com/Inflation/Consumer_Price_Index/HistoricalCPI.aspx?reloaded=true YEAR JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC AVE. 2020 257.971 2019 251.712 252.776 254.202 255.548 256.092 256.143 256.571 256.558 256.759 257.346 257.208 256.974 255.657 2018 247.867 248.991 249.554 250.546 251.588 251.989 252.006 252.146 252.439 252.885 252.038 251.233 251.107 2017 242.839 243.603 243.801 244.524 244.733 244.955 244.786 245.519 246.819 246.663 246.669 246.524 245.120 2016 236.916 237.111 238.132 239.261 240.229 241.018 240.628 240.849 241.428 241.729 241.353 241.432 240.008 2015 233.707 234.722 236.119 236.599 237.805 238.638 238.654 238.316 237.945 237.838 237.336 236.525 237.017 2014 233.916 234.781 236.293 237.072 237.900 238.343 238.250 237.852 238.031 237.433 236.151 234.812 236.736 2013 230.280 232.166 232.773 232.531 232.945 233.504 233.596 233.877 234.149 233.546 233.069 233.049 232.957 2012 226.665 227.663 229.392 230.085 229.815 229.478 229.104 230.379 231.407 231.317 230.221 229.601 229.594 2011 220.223 221.309 223.467 224.906 225.964 225.722 225.922 226.545 226.889 226.421 226.230 225.672 224.939 2010 216.687 216.741 217.631 218.009 218.178 217.965 218.011 218.312 218.439 218.711 218.803 219.179 218.056 2009 211.143 212.193 212.709 213.240 213.856 215.693 215.351 215.834 215.969 216.177 216.330 215.949 214.537 2008 211.080 211.693 213.528 214.823 216.632 218.815 219.964 219.086 218.783 216.573 212.425 210.228 215.303 2007 202.416 203.499 205.352 206.686 207.949 208.352 208.299 207.917 208.490 208.936 210.177 210.036 207.342 2006 198.300 198.700 199.800 201.500 202.500 202.900 203.500 203.900 202.900 201.800 201.500 201.800 201.600 2005 190.700 191.800 193.300 194.600 194.400 194.500 195.400 196.400 198.800 199.200 197.600 196.800 195.300

-

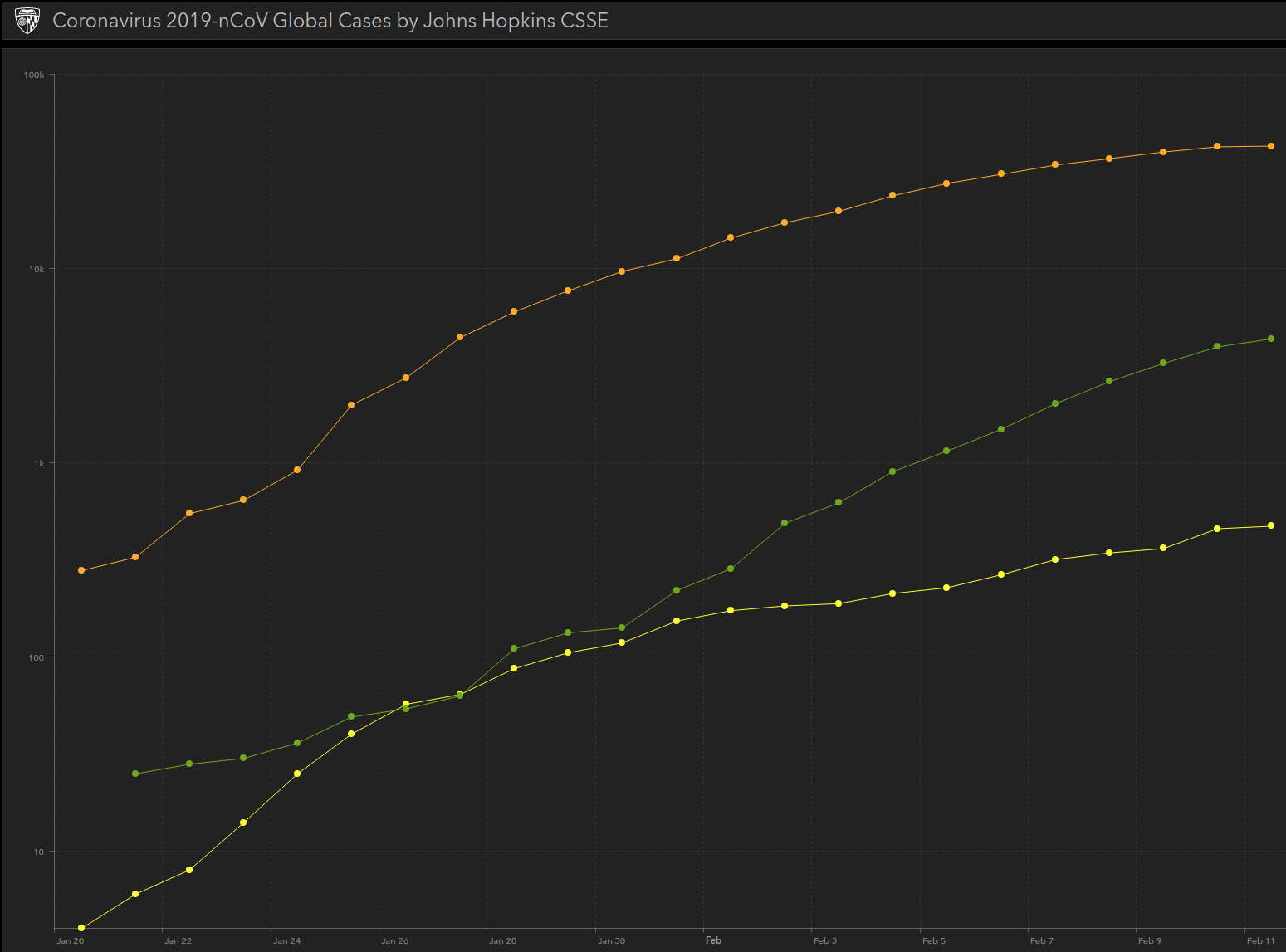

If we knew, we'd be rich. © Warren Buffett. Jurgis, I think Buffett’s answer (do not try and time the market) is overly simplistic and not actionable for most investors. When we are in the midst of a bear market emotions get the best of most investors. I am simply trying to assess what the probabilities are that this out break starts to spread in the US to the point that it impacts the economy in a meaningful way. Two weeks ago my read was that the virus was not going to impact the US economy very much. Over the past 4 days my view has started to shift and it now appears the question is when the virus breaks out in the US (not if) and how bad it gets. Hopefully this thing just blows over. The next could of weeks are going to be very very interesting :-) Here in Canada we are being told to make preparations: stock up on prescriptions and perishable food. Canadians being told to prepare for a possible novel coronavirus pandemic - https://vancouversun.com/diseases-and-conditions/coronavirus/canadians-being-told-to-prepare-for-a-possible-novel-coronavirus-pandemic/wcm/f93197f0-8c56-4050-a50c-4de1f031c659 “Etches said people can take steps now, at home and at work, to prepare. Some of those steps include stocking up on needed prescriptions ahead of time so there is no need to do so during a possible pandemic. She also recommended people stock up on non-perishable food.” So, looking at the data and the big picture, the pace of increase of new infections has declined. It's a novel flu, but the profile of people that are dying from the flu is traditional. It's a headline driven phenomenon with journalists amping and hyping the story. National health authorities put out warnings several times a year on various infectious diseases, but the public largely ignores these. This virus just has captured the public's imagination and it's become a plaything of salacious interests. As an investor, that's useful information. How are long-term business models being impacted? A quarter of earnings misses could very well happen, but I am looking for discounts on valuable businesses.

-

Coronavirus is looking increasingly contained. Logarithmic scale shows the rate of increase is tailing off. https://gisanddata.maps.arcgis.com/apps/opsdashboard/index.html#/bda7594740fd40299423467b48e9ecf6 At most, coronavirus could impact the 1st quarter of 2020 for just about any global business as a fraction of sales. Will it really harm any business models? Of course not.

-

I've always thought that middleman Express Scripts was a Berkshire acquisition in waiting as well as Fastenal. Cigna bought them last year for $52B.

-

Berkshire holds a lot of cash. The composition of assets is malleable and used to meet regulatory requirements (see table below) as well as investing for long term wealth generation. This article does a reasonable job of extracting the right ideas to think about how the float is managed and employed from an investment perspective. Berkshire's approach is different from other insurance companies, as you could expect -- they have better and rational thinkers with decision-making power. https://brooklyninvestor.blogspot.com/2011/12/so-what-is-berkshire-hathaway-really.html

-

Of course. The hard market starts to appear when insurers, that have under-priced their contracts, consume capital in payouts for catastrophe losses. These insurers tend to write less business as they need to preserve capital. So, the insurers that have a counter-cyclical approach (i.e., write less business when pricing is soft and more when pricing is firm) have lots of available capital just as pricing increases (post-catastrophe pricing usually increases) and the overall capital is shrinking. Hard markets can last a few months or a couple of years, often in niche categories, so putting capital to work at high rates for long periods is the aim of the game. Not every insurer is geared to do this, so lots get caught up in increasing top-line revenues year by year. Multi-cat years will shake out the weak capital. - O

-

Adjusting for inflation (the early years were horrible), were the real returns much larger? Gaudy headline numbers may dazzle but inflation took up a large number as well.

-

Agree on the competitors. They have an immediate windfall from cap gains on their bond portfolios, but will be hard-pressed to fund their future insurance liabilities. I'm in the process of selling down a long-held stake in WR Berkley as it has become inflated at $13.2B market cap on $6B book value. It has limited upside from here, mostly relying on continued BV multiple expansion. As my general rule, 2xBV is an expensive proposition for an insurance company. At this point, I'd rather pay the cap gain taxes and hold cash than hold the shares through a downturn and watch the multiple collapse back to 1xBV. It will be easier to put money to work at high rates in the future. At this point, I'm only holding BRK in the insurance space. Buffett has done a tremendous job of building a float machine. Chris Bloomstran at Semper Augustus has a wonderful write-up on how the energy business and the railroad business are able to generate further ways to use insurance float through accelerated depreciation accounting rules. Even if the railroad business isn't throwing off cash due to cyclicality of the overall economy, Buffett will still be able to run insurance operating profits and cap gains through the railroad business' accelerated depreciation shield. - O

-

https://www.morningstar.com/articles/942242/5-reasons-to-consider-buying-berkshire-hathaway?dtr

-

Insurance companies are usually modelled using a sum of the parts (SOTP) and book value (BV) multiple. So, something like WRB is at the top range of valuation (approaching 2x BV) while Fairfax (sub 1x BV; use US$ as financials are US$) is at the bottom range of valuation. Your view on BV growth and a range of BV multiples is probably more meaningful than DCFs which are a trickier model to get 'right'. Fairfax is saddled with a 1xBV valuation because their portfolio management has been atrocious for years. They play the Templeton-style deep value game, in the small percentage of their portfolio dedicated to equities, which hasn't worked for ages. The bulk of their portfolio is in cash and bonds which was great during the bond bull market but tremendously limits their upside going forward. At best, Fairfax will grow their book value by xx% and possibly get a 1.2 or 1.3xBV bump when one of their deep value plays finally pays off. There are easier ways to make money. DCFs are more appropriate for predictable cash-gushing businesses than insurance companies which have catastrophe years where cash is needed for payouts. Even still, favorable assumptions in DCFs lead to a large tail value which is quite probably wrong. Caveat emptor.

-

Best Ideas To Profit From Big Increase In Downside Volatility

omagh replied to wescobrk's topic in General Discussion

1. Ignore the macro. 2. Increase exposure to cash. [Cash is a call option on volatility] 3. Identify high ROIC / high NOPAT companies with long reinvestment runways. 4. Wait and watch for your price targets. 5. Read and learn. 6. Enjoy life and see Rule #1. -

Buffett buybacks: Could Berkshire tender stock?

omagh replied to alwaysinvert's topic in Berkshire Hathaway

I wouldn't recommend extrapolating a few weeks behaviour indefinitely. Buffett disclosed on CNBC that there was an elephant-sized acquisition in the works during the last few months which ultimately failed to close. During an elephant acquisition, cash put to work at high rates of return, is MUCH more valuable than buying back whatever mildly-discounted BRK shares are fully available for repurchase. - O "If you speak up and put it [investment idea] on record, you end up getting too wedded to your thesis and that's dangerous because everything you're invested in is a function of the facts and circumstances on a given day, it changes" -- Ted Weschler -

Ben. Although we've rarely interacted, I appreciate your board input and share your opinion. I have removed this board from my RSS reader and only visit on rare occasions. The quality of the CB&F board has degraded so significantly that I'm now focused on a high quality private board with some other folks that don't post as often here. The ongoing analysis of FFH here is 2nd to none, but quality drops off rapidly on everything else. -O

-

http://fairfax.ca/Theme/Fairfax/files/2011%20AGM.pdf

-

Lots of good posts as usual. +1 It's helpful if people are rigourous about confining discussions to particular threads so that it's easy to skim over the areas that are not of interest. In that context, I am a little surprised about the comments about LVLT from some users. Whether you believe that the LVLT discussion is fabulous or inane, it is nicely confined to a particular area which makes it either easy to find or easy to avoid. SJ, You've nicely pointed out how different the experience is using the web interface and the RSS reader interface. In the web interface, the LVLT discussion is there for those who are interested in a single thread. In the RSS reader interface, the LVLT discussion is there in its fabulously inane glory. I would really like to find a way to mute that thread in RSS. In RSS, you get to see everything on all the boards and threads, but it's becoming very noisy as the community grows. I may just start using the web interface and looking for specific users. Your dialogue with Harry Long was epic for sure. "Ignore user" feature is a personalization to tune down the board noise -- no one is being deliberately censored to everyone else as some folks seem to think -- i.e. no one is being banned. I just want to mute one or two users that I don't care to read. If there are enough interesting comments pointing to a post by the muted user, that user can be turned back on momentarily and then re-muted. Sanj has done a great job for many years on top of his day job.

-

The board is getting bigger which is a good thing since we draw from a wider range of opinions. Some members of the community have a low signal-to-noise ratio. The ignore user button. http://custom.simplemachines.org/mods/index.php?mod=2299

-

I see that the earlier comments were edited from this morning. I was going to reply and thought better of it. What was missing from the debate is a discussion of "fair use" (US term) and "fair dealing" (Canadian term). There is an element surrounding fair use of copyrighted materials that are "out of print". An example of fair use rules are the following: www.macewanbookstore.com/Copyright-Guidelines-2010-Dec-2.pdf (good treatise of fair dealing on page 2) http://www.ehow.com/list_6934290_copyright-laws-out-print-books.html http://www.umuc.edu/library/copy.shtml#whatis Copyright and Electronic Publishing The same copyright protections exist for the author of a work regardless of whether the work is in a database, CD-ROM, bulletin board, or on the Internet. If you make a copy from an electronic source, such as the Internet or WWW, for your personal use, it is likely to be seen as fair use. However, if you make a copy and put it on your personal WWW site, it less likely to be considered fair use. The Internet IS NOT the public domain. There are both uncopyrighted and copyrighted materials available. Assume a work is copyrighted. Some universities and libraries will make a copy of out-of-print books for about $10 if you meet the fair dealings guidelines in Canada. Since there is no local university with a copy, I took a copy of the Klarman book to a local printer and had a bound copy made for personal use. I would gladly pay Klarman if there was a reasonable means to do so. -O

-

It's a real measure of respect for the senior leaders to make the effort to be at the dinner. Obviously your own contributions, Sanjeev, have been the galvanizing effort in this 2-way relationship with the message boards and the FFH team. Well done! It has been about 12 or 13 years now since we started the journey down this path as FFH shareholders and it has been tremendously profitable. -O

-

The new site has lost some valuable content -- the shareholder meeting presentation slides. Hopefully when the slides for 2011 are posted, some of the older slides can be reposted. They're meaningful from year to year since they provide context and information not found in the AR. -O

-

Sanjeev...congrats on the fundraising and to all the contributors. Did you have any advance notice of the guests? -O