changegonnacome

-

Posts

2,694 -

Joined

-

Last visited

-

Days Won

7

Content Type

Profiles

Forums

Events

Everything posted by changegonnacome

-

Exactly…..supply demand…..call me about the end of NYC when rents start slipping & it isn’t a top three surveyed destination for Ivy League student graduates. Until then I just can’t see it being toppled. Like if your in some other back/middle office city to a NYC HQ’d corporate …..ChatGPT & generative AI is coming for your cities employment activity first.

-

https://www.bloomberg.com/news/articles/2023-05-10/new-york-city-area-rents-surge-by-most-in-nearly-two-decades?srnd=premium&sref=7zqHEcxJ "Everybody complains about it but nobody seems to leave" - John Lennon c.1975 about NYC "Folks are leaving for sure - but there seems an endless supply of newbies moving to NYC just look at the rents surge as per Bloomberg article" - Changegonnacome c.2023

-

Leaked email from Microsoft CEO says salaried staff will not get raises this year due to macroeconomic conditions: https://finance.yahoo.com/news/leaked-email-microsoft-ceo-says-160307908.html?guccounter=1 This is what a soft landing result inside a rate hiking, inflation fighting cycle could/would look like.......a spontaneous break-out of wage restraint with de minimis uptick in unemployment.......its still possible IMO but history says its the outlier outcome....Microsoft & other 'thought leading' companies can really help set the tone as per the linked.......so many other companies ape FANGMA's every move......this in a way is a public service by Microsoft......ironically being done by a company with outrageously strong pricing power bordering on monopoly (so potentially self-serving).......which is choosing in some respects to show restraint on pricing & maintain margins holding down its OpEx.....very interesting move by them they are almost pretending like they couldn't get away with a $0.50 increase per Office365 seat sub!

-

Taking Advantage of the Fear Around a U.S. Debt Default

changegonnacome replied to Parsad's topic in General Discussion

Yep I'm rolling some cash laying around into bills which straddle the supposed date of "default".......MMF dont wanna hold them, cause why bother holding them if you dont have too type thing.....so they are stupidly high -

Russell 2000 & stuff like NFIB above is where you need to look for the health of the real US economy...........I'll admit the resiliency of large cap tech but really Google, Microsoft, Apple have surprised me somewhat.......but then when I think about it some more......why the hell am I surprised when monopolists display monopoly like business performance.....its the equivalent of being surprised that the atlantic ocean is cold.....Apple remains IMO the most vulnerable being as it is still a predominately hardware transacting business where the product purchase can be deferred for a year or two very easily bringing volatility to its earnings.....recession in H2 2023 & the iPhone 15 could seriously & surprisingly underperform the iPhone 12, 13 & 14.

-

iSavings bonds yielding 7.12% currently

changegonnacome replied to Spekulatius's topic in General Discussion

US T Bills expiring June 13th ~5.4% YTM....... because of default nonsense MMF's don't wanna hold em.....can't beat getting more than Fed funds right now for something that is effectively better than 40 day CD -

I'd say he needs to be very careful moving forward this version of the US economy post ZIRP has a balance sheet hitched to 3% fixed rates married to house prices that expanded in value to something of cyclical high.........the consumer & labor market has shown a resilience to 500bps rise in rates in a very short period which is surprising.....but not surprising in the context of 10+ years of ZIRP & everybody's fixed rate balance sheets..........if/when the economy deteriorates he needs IMO to remember just how rate insensitive spending was as he tried to wrestle the US economy to the floor.........cause it might be the exact same as he tries to stimulate it to grow again & get it up off the floor. There are no significant cash out refis happening in 2024. As regards what happens next......I remain in the hard landing camp........and we are where I've said we would be........sticky, disappointing, not budging MOM super core/made in America inflation that cant be blamed on Putin or supply chains.....unfortunately it can only be blamed on reckless politicians and dumb central bankers who continued to buy MBS's and enact fiscal giveaways.........this inflation were hitting now is domestic spending growth fueled with wage increases that exceed productivity gains by significant margin.......barring the labor market breaking to the down side.......I expect inflation now month after month to disappoint as the big headline CPI 'wins' roll off and headline rates converge with the super core inflation number......which just isn't living up to the inflation magically going away narrative that folks are telling themselves. The Fed sees what I see...500bps of rate rises and numerous bank failures later....and SuperCore inflation has barely flinched.......meaning headline CPI has zero chance of getting anywhere near 2%, anytime soon...........its clear now that you can only get to SuperCore via the labour market........I really do hope moderating wage increases is enough....but its not likely to be barring an early productivity miracle from ChatGPT implementations.

-

Yep quicker & steeper..........its a challenge for this Fed........this isn't Europe where Christine Lagarde raises & next month the average European mortgage holder has 100 euro less to spend in the real economy........Europe should be able to get inflation under control much much quicker & with less collateral damage........in the US the Fed raises......and the average mortgage holder couldn't care less........sure prospective mortgage holders do.....but its very hard to effect the monthly FCF of a US household...interest rates are such a blunt tool but interest rates in a post-ZIRP decade are really blunted. Higher for longer is the logical conclusion from the rate & term structure of debt in the USA.....and unfortunately the downside of the venerable 30yr fixed rate mortgage....is that in an inflationary period it almost guarantees that the monetary authorities HAVE to hit the US labour market in meaningful way to moderate spending. Its a challenge - but the cautionary piece of this that Powell should be paying attention too........is that as someone who is currently struggling desperately to temper spending via interest rates.......he must remember that once he accomplishes his mission of getting back to 2........the same problem awaits him on the backside of this........bringing the USA out of recession wont be so easy either for the exact same reasons........because coming out of the next recession we are unlikely to see rates go so low that Joe Sixpack is refinancing his existing 3% mortgage and improving his monthly FCF.......its also unlikely that Joe Sixpacks home value has appreciated relative to heady day of 2021 when he did his last cash out refi.....so no 'cash out' magic is waiting in the next cutting cycle......it will be a slow credit lead recovery (unless the fiscal authorities swoop in with helicopter stimulus).

-

Yep kind of the prototypical end of a market cycle behavior......as an institution you want to keep dancing while optimizing for career/client risk.....you pile into this stuff safe in the knowledge that all your colleagues & competitors are too. "Worldly wisdom teaches us that it is better for reputation to fail conventionally than to succeed unconventionally." - Keynes Wall St. the institutional kind can be pretty much summed up in that sentence.........and if Mark's et al are right about the 'sea change' and I very much agree with them.........this type of market with its lack of breath is exactly what one would expect before we transition into the new paradigm.

-

Interesting time period - wonder whats next for the venerable banking industry? The commercial real estate boogey man is well known.........and those loaded to gills with that stuff are getting worked over right now.....and bank investors have been forewarned on whats likely coming there. Suspect the next shoe to drop - are likely niche banks with some kind of idiosyncratic consumer risk on their balance sheets.....not bank collapsing stuff like we've seen but possibly share price collapsing stuff........credit quality deteriorating married to rising funding costs sure can impact short-medium profitability.

-

For sure it is........a consumerist capitalist society/economy/market...... is also a society of people who get up in the morning motivated Monday thru Friday.....to work their tails off making more & better stuff more efficiently...... to get the money they need to buy the things they don't 'need' . It's the best system human beings have created.........to solve for abject poverty, starvation & destitution......it's a goddamn marvel how good we all have it even the poorest......relative to the quantum of human beings that have ever existed on this planet. Fiddle with it at your peril i say.....especially these lunatics on the left.......the lunatics on the right are bad.......but IMO the lunatics on the left are the most dangerous cause they wanna mess with that market system....& on that pathway lies hell! Reminds me of one of my favourite Friedman clips about the humble pencil and what a god damn marvel it is:

-

Excellent point and well made- and at the end of the day @Gregmal will see his frugality suggestion to folks play out en masse.....the Fed to a certain extent, via interest rate rises, is a kind of frugality alchemist......that is attempting to initiate & create a frugality wave in the USA......first by influencing credit creation demand & supply.....which hits spending....which then hits unemployment......as anyone who lived through the GFC knows.....somebody in your inner social circle losing a job and demonstrably struggling to find another one.....unleashes interesting recession behaviour in the folks around them or as @John Hjorth quite rightly calls it "rationality & frugality" behaviour......which gets my vote for what a recession should actually be called....a spontaneous & widespread breakout of rationality & frugality. Chair Powell......should be renamed Chairman of the 'new' group called the F.E.D.......Frugality Expectation Department

-

Yep looked at Oxford too on the back of your reco.......bought a nibble and on my list to do more work. You can't beat the ticker either....it gave me a good laugh when I saw it first - OMG

-

The best hunting ground IMO right now for this type of this stuff are small cap value stocks listed on the LSE....the ones however that are international with little to no underlying exposure to the UK economy...............valuations are undemanding, frustratingly so for some issuers.....who are moving their listings to Euronext Amsterdam or over to NYSE/NASDAQ......CRH comes to mind..........anyway short version is you've got rule of law, the accounts can be believed as much as small cap value can be in the USA....I think they are less picked over and so better mispricings exist.......and most notably for a USD/CAD investor I think right now you've got in-built currency hedging & tailwinds against the GBP/EUR strengthening against both dollars.................applied to a well chosen basket of non-UK economy exposed but LSE listed companies I think one can do very well here. I'm up to my eyeballs in Hostelworld (HSW) ~150m mkt cap - which i've covered ad nauseam in this thread....so wont go into....but suffice to say that its grown to nearly 33% of NAV and I couldn't bring myself to trim it back even though that type of exposure is a little outrageous even for me. I also like Glenveagh Properties (GLV) on the LSE...500m mkt cap.....it tends to trade with the UK homebuilders and that's the opportunity.....it's actually an Irish homebuilder and should not trade with UK peers....cause you couldn't get two more divergent economies & macro backdrops right now.....Ireland has an exceptionally bad housing crisis demonstrably worse historical undersupply than the UK itself especially post-GFC......but its the divergence on the macro side that is the most interesting.... the Irish economy is booming with US big tech driven corporate tax windfall delivering surpluses to the treasury there.....the Irish government has so much cash it doesn't what to do with it and has started a mini sovereign wealth/rainy day fund. However housing is the No.1 political issue of the day.....and money is being spent like drunken sailers now to try and fix it. So interest rates might be rising & a recession might be coming.....which makes homebuilders traditionally bad bets given the interest rate sensitivity.....but in Ireland the system is throwing money at the developers to build with various schemes and loading up first time buyers wallets to buy.....doing in essence, whatever it takes, to make the math work to keep supply rising YoY......not that it's needed......rents have gone crazy in Ireland, the pricing mechanism by which the deep undersupply manifests itself......so the rent vs. buy maths even at 6% or 7% mortgage rates would still work in Ireland. Glenveagh in my view......is not a homebuilder......its a government contractor.......I think their planned 2024, 2025, 26 supply is effectively underwritten by the Irish sovereign at a 20% gross margin........and all this wouldn't matter without the valuation which is just x5 times 2024 earnings....and where the company is using all FCF to buy back shares.....a kind of European NVR.....last they took out 16% of s/o....this year easily 10%...more likely more. I might do up a thread at some stage I like the opportunity so much.

-

Right pricing power to pass thru rising costs.....but underneath & capped by the industry wide 4% net margin problem that bedevils a perfectly competitive industry like the grocery biz......the customer underneath then, as you say, can change his/her unit volume & the product mix hurting the grocer.....leaving them no better off and certainly possibly worse off, in real terms not nominal terms, than when the whole inflationary period began.

-

Right - a grocer has essentially no pricing power........and the opposite of grocer is a monopolist.....you want to hold a monopolist in an inflationary period....you get underlying nominal net income expansion driven by inflation....but the monopolist gets to also imbed real price rises alongside the nominal uplift......one reason why......in the big tech fallout from last year.....the Phoenix from the flames in 2023 in terms of share price performance for sure but underlying results too.....its a certain sub-set of tech.....the ones we all know that have monopoly or duopoly like positions.

-

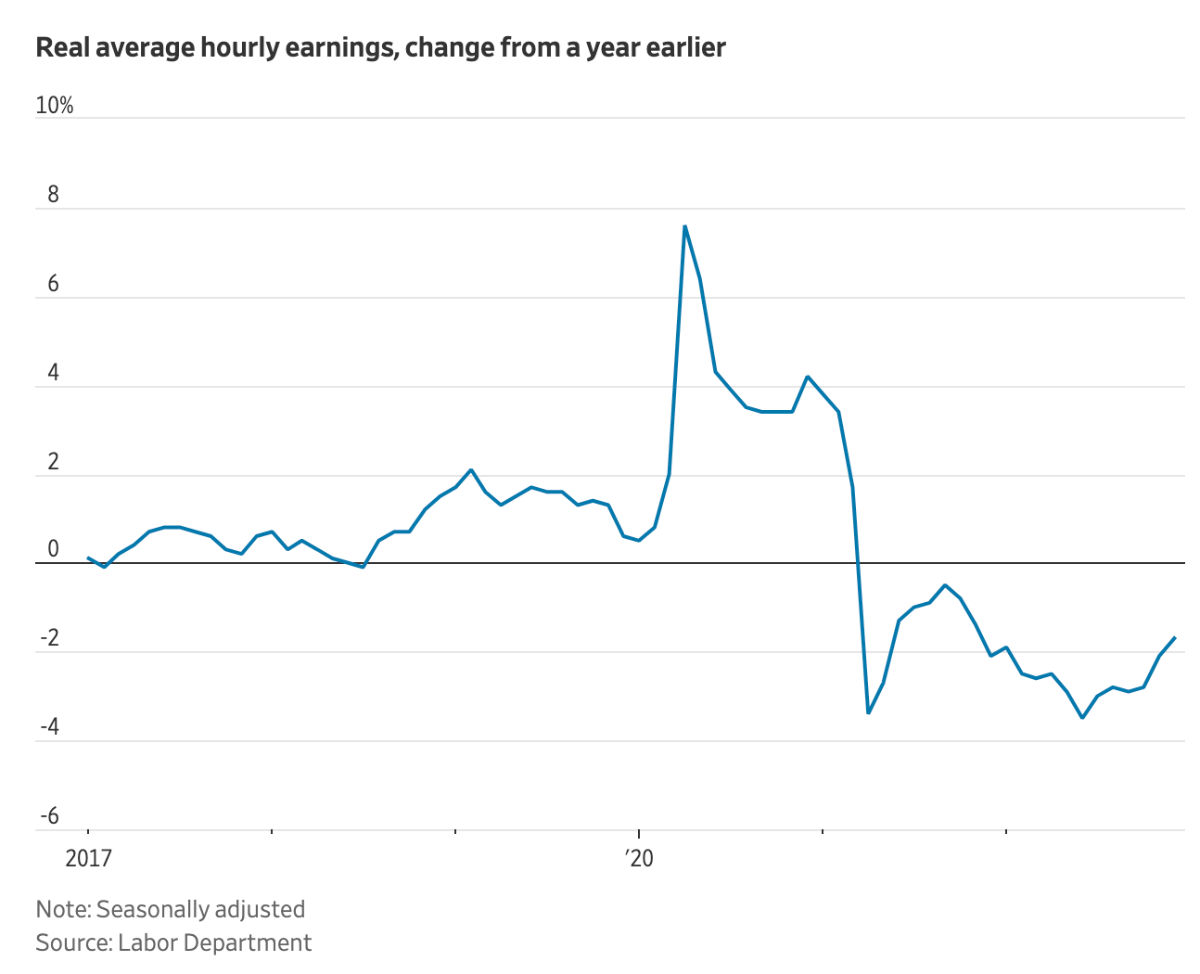

Thanks @SharperDingaan yep the 'math' is irrefutable........and why the answer to the question when is the right time to buy a house? The answer usually is always (1) when you need one & (2) right now......you really want that leveraged compounding short against the US dollar to start to play out ASAP. It's also math that shows why an inflationary & this emerging stagflationary version of the US economy is not a good one for 'the little guy' albeit with a headline 3.4% unemployment rate while positive tells a tiny part of the real underlying story.........real wages are falling....which is not a good outcome.....while the little guy is way more likely to be a renter, than an owner of hard assets....he/she therefore hasn't got an implicit short against the value of USD (a mortgage) benefiting from higher inflation...... and by extension doesn't own a hard asset appreciating against the devaluing currency....while providing fixed accommodation costs. Now who does have an explicit leveraged short against the US dollar?......the holder of lots of mortgages and the owners of lots of hard assets.....this aint Joe sixpack.......it's Joe Blackstone & friends......cheering on the debate out there that says "hey 4% inflation is nothing burger, lets shift up the 2% inflation target up to 4-ish".....of course it isn't, for them it's a boomtime if that happened.......their short against the US dollar had an expected 2% return unlevered....inflation running at 4% just doubled their unlevered expected CAGR by 100%.......which is amplified by how much they've levered it via a mortgage....something levered 10 times...where the underlying return just doubled is a beautiful outcome for the holder. However It's a lose-lose for poorest quartile of the population......and an inflationary period has always been a pretty good strategy if one were looking to introduce instability in your society.......& for obvious reasons.......that quartile might not know the math exactly....but they sure as hell sense when the 'system' is screwing them. Some here seem to think the 'war' on inflation is some elite conspiracy to screw the poor again & line the pockets of the rich.....it's quite the opposite....inflation if one wanted to 'go there'....could be more evidentially construed as a conspiracy by Blackstone/Brookfield investors, the landed class and the holders of multiple 3% mortgages + the government......to screw over the poor....given the beneficiaries of a persistent 4-5% inflationary period, as we've demonstrated above with math, are so clearly the top quartile.....that to think the bottom quartile is 'winning' right now ignores the reality, the facts and the math.

-

Your telling me the above is a great environment for workers.....some kind of golden age for the little guy......they are getting their pocket picked. They are worse off, not better. Fact. End of story. You can overlay COVID stimmy's but they are gone now....and workers above....can buy less than they could before COVID. Less, not more......and stimmys are gone. You must be confusing the diversity, availability and opportunity to CHANGE jobs......which was indeed AMAZING during 2021/22 period.......with what happened to the purchasing power i.e. REAL wages of workers.....which was just horrible......as bad as it is during a recessionary period.

-

Temporary Gov breaks vs salaries...........is mixing apple and oranges......your talking one time COVID assistance programs .......which as you know have gone away.....I didnt see any cheques come in recently for breathing.........however.....the price increase that XYZ company put on XYZ product in 2020/2021....and they ain't going down.....its a permanent impairment of purchasing power..

-

Your just fundamentally ignoring the maths here..............if inflation is 9% and you get an 8% pay rise......you got a pay cut..put simply you can buy less stuff......the average workers pay has been going down not up over this golden period you seem to have in your head..... Wage growth accompanied by low inflation is a 'win' for workers....that is not what has happened over the last 3yrs. https://www.wsj.com/articles/workers-lose-ground-to-inflation-despite-big-wage-gains-11673649460 This has been a terrible period for average workers wages....they've been robbed by inflation.

-

Yes they sure are - 2022-23 period saw inflation exceeding pay rises.......such that they weren't actually pay rises at all.....they are actually pay cuts in real terms when inflation adjust........right now based on current figures pay rises are barely covering inflation.....and so wages are STILL pretty much stagnant in real terms......the numbers on your payslip dont matter........its the basket of goods and service it can command.....and on that front (2020-23) this has not been a good period or some golden age for workers.....far from it......you can argue that for the marginal, unproductive, barely show up on time, barely do any work worker...who in a normal economy would spend more time unemployed than employed.........it's been unbelievable boom for them......let's call them the workers enticed off the couch as unemployment dipped below 4%.....the dregs of the labor market and the first to get sacked if you run a business and things start to slow down........this overheated economy has been a boom for those folks.... the basket of goods and services they can command while in W2 over welfare cheques is hugely increased. The median 'normal' worker can't say the same thing unfortunately.

-

Dude that just not the way it is..........4.5% inflation is not a nothing burger.........the difference is huge, cause of the magic of compounding......think of it this way......with 2% inflation the value of a dollar roughly halfs in 36 years......nobody notices, nobody cares inflation is not a 'thing' being routinely built into life.......... 'inflation phycology' is under control..........4.5% inflation however and the value of a $ drops in half in 16 yrs.......it becomes a thing, its noticeable at the grocery store......and expectations around it start to get imbedded......when inflation becomes a 'thing' in a economy.....inflation expectations can become unanchored & start getting built into unit prices in a way that feeds on itself.......wage-price spiral (which I know you think doesnt exist!) does indeed exist it doesnt have to spriral you can have what we have now which is wage-price trapped at a place that ensures 4.5% inflation persists.......but the problem is a 4.5% inflation economy is one that ends up an 8% one too easily.......its the way it works.....and why 2-ish is important.....its the level at which inflation becomes imperceptible to participants in the economy because its moving so slowly nobody year to year notices it. On the same point....and maybe backing up your Joe thesis - a colleague today framed something in a new way I implicitly know.....but in a more clear way than I'd be thinking......he mentioned how property is such a great bet most of the time as long as you don't pay bubble prices.............as its way by which people, unknowingly and with 10 or even 20 times leverage, get to short a depreciating asset that by dictate will fall at least 2% a year, guaranteed almost....cause what your shorting is the US dollar.....& going long politicians printing money...all collateralized by an asset that you get to live in to make that bet............and seen as you need to live somewhere anyway and the alternative is paying rent....you might as well live in asset that allows you to make that levered trade above..............interesting way to frame the act of buying a home......and perhaps buying JOE too........guaranteed currency devaluation against a hard asset (Florida Panhandle land) with extra demand/price push coming from migration trends + smart investment in the area that increases its desirability & price.

-

SPY/QQQ where they are & VIX @ 16............is an interesting chance to sell in May and go away via a bearish option spread on index......while holding on to your underlying......cheap-ish portfolio insurance if you ask me.......relative to some events up ahead (debt ceiling, FOMC May/June/July & looking likely recession afer etc.)

-

Thats already happened - 9% to 5%........that head fake is now pretty much over.....I expect headline to drift down 4.5% and get 'stuck' Core PCE ex-housing...or SuperCore as some call it....is what the Fed is watching to your point.........this number is stuck and showing little signs of moving.......their focus and efforts are to drive this number down now, they can OER just like you and I can....they aint worried about.......its SuperCore....& it has shown little momentum to downside.....and hence why higher for longer

-

https://www.nytimes.com/2023/04/28/business/wage-inflation-march.html 5.1% annualized wage growth.......in an economy growing productivity sub-1%........is not an economy on its way back to 2% inflation without the labour market breaking........the annualized PCE number stuck in the 4%+ range (which is what we got today too on that front) is now the floor IMO (absent a spike in unemployment/recession). I've been saying for a while the easy inflation wins (supply chains/Ukraine/energy) are rolling out of the data.......we are now in my estimation hitting the Made in America Inflation I've talked about......its a floor not a ceiling