Xerxes

-

Posts

5,689 -

Joined

-

Last visited

-

Days Won

9

Content Type

Profiles

Forums

Events

Everything posted by Xerxes

-

Math / mental gymnastic question: We know that mathematically (in a tax-free environment), a $1 of dividend, re-invested by shareholder for more shares will have an identical effect on EPS to a buyback by the company. Knowing that, a dividend will in fact give optionality to the shareholder to decide to increase exposure or not. Whereas a buyback doesn’t give that optionality. Now bringing this to FFH, on this hypothetical $1 billion of surplus at this point in time. Why should it not be disbursed as “special dividend” for the shareholder to chose to buy more shares or not. A buyback based on the company thesis of discount to intrinsic value forces a certain fixed outcome. A re-invested dividend, allows each shareholder executing on their specific view of intrinsic value and their desire for margin of safety to it. I think there is a certain mental view that a dividend is just money wasted whereas buyback below intrinsic value is not. That shouldn’t matter from a shareholder point of view (tax-free environment). In both cases, $1 billion leaves the company coffers never to be seen again.

-

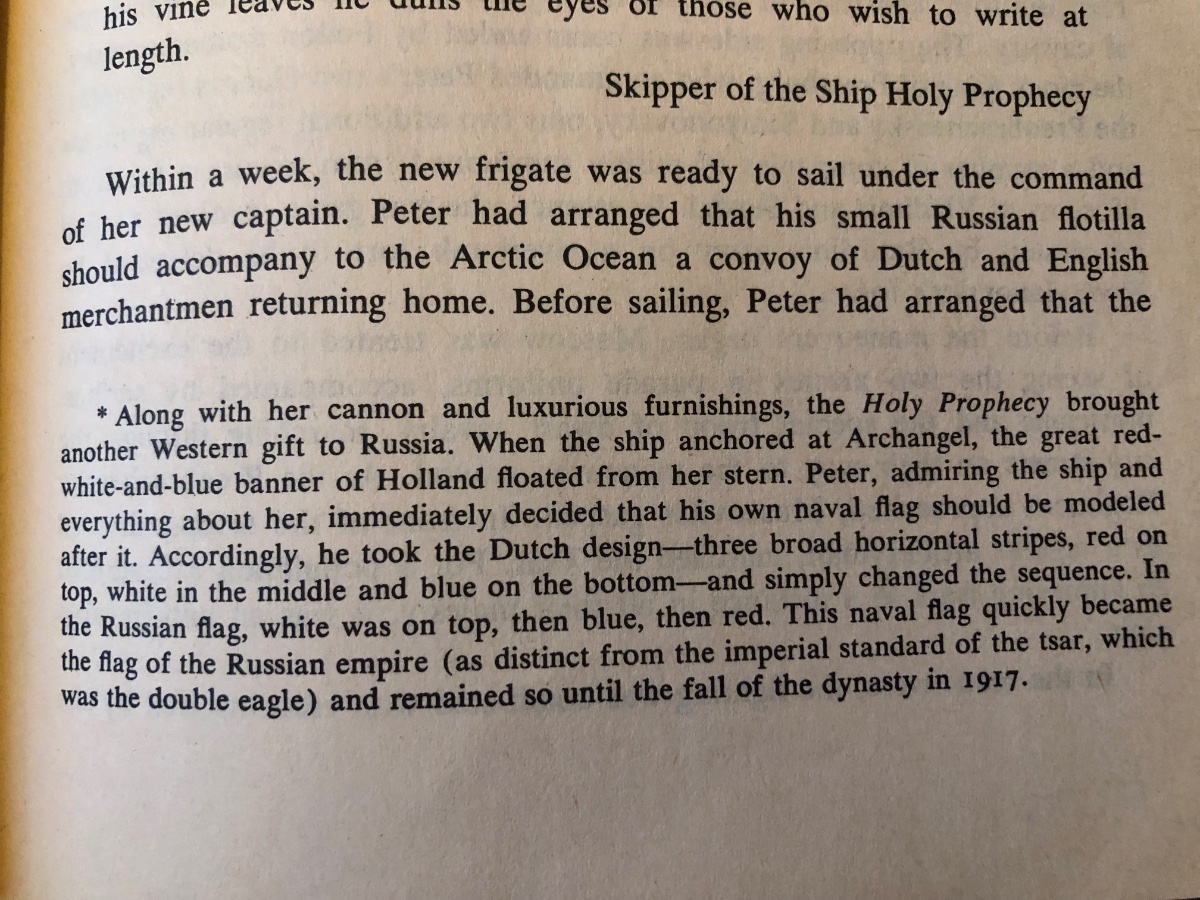

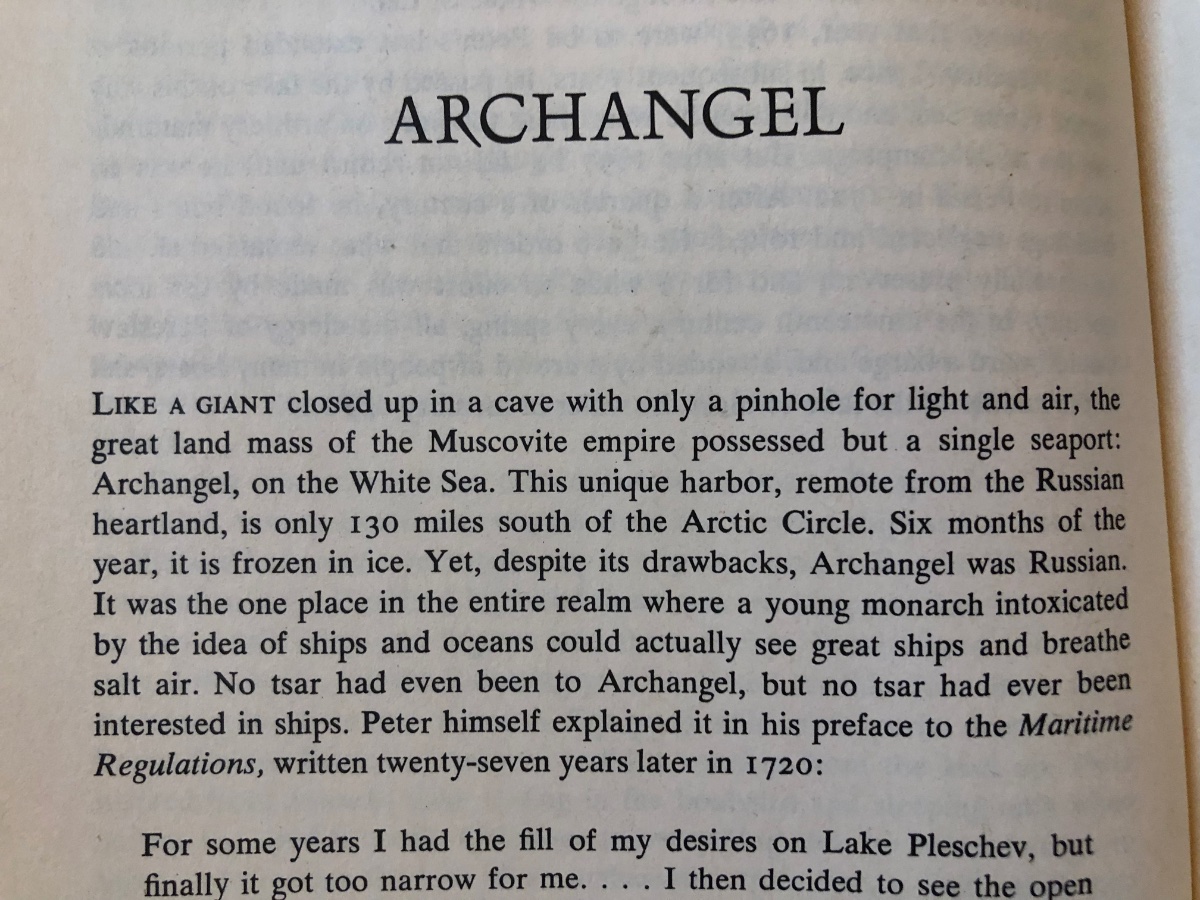

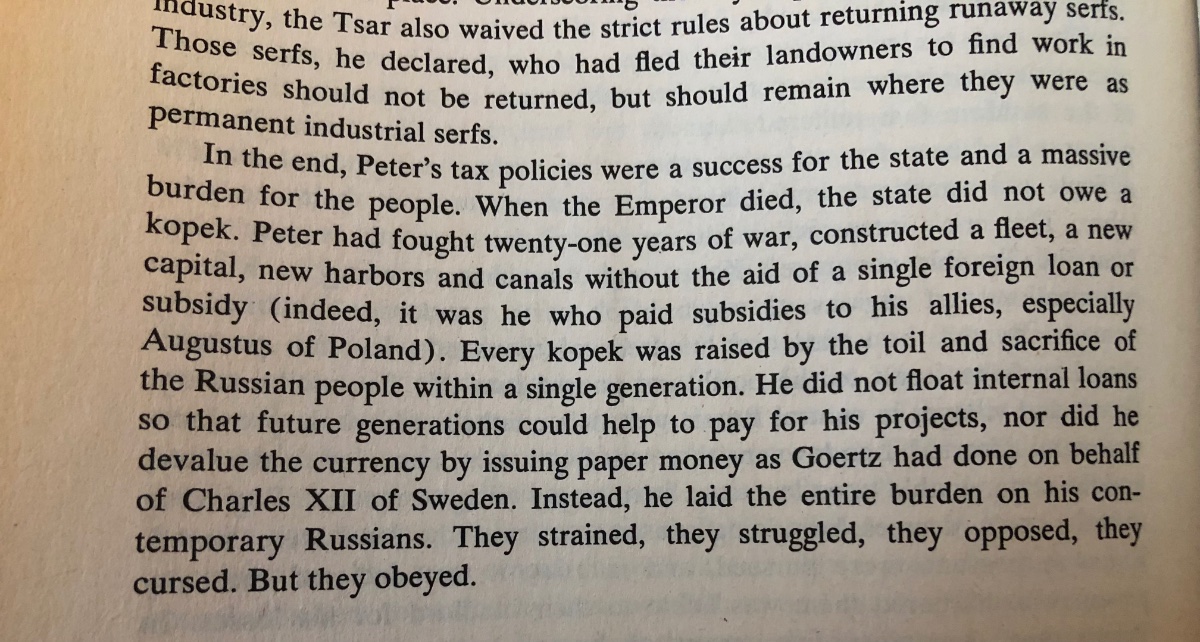

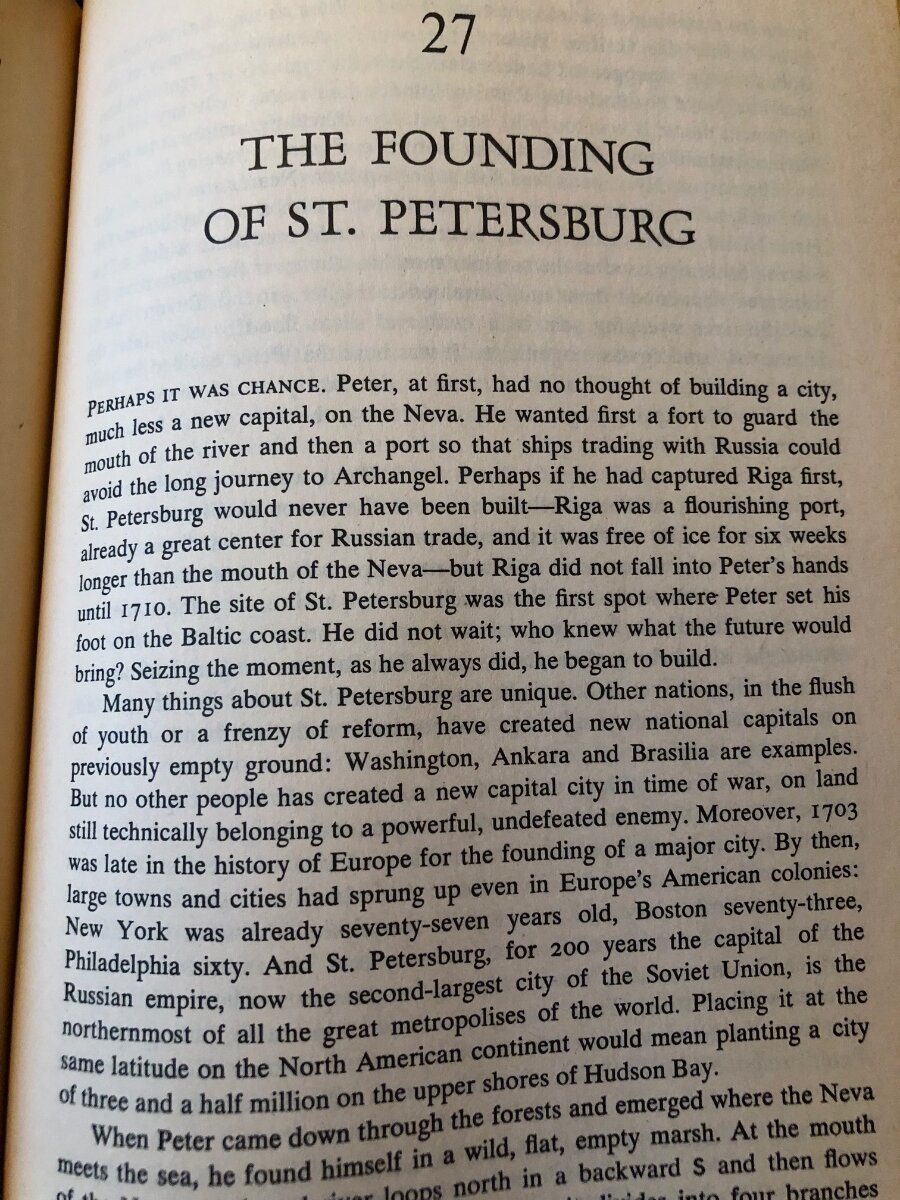

Robert Massie passed away few years ago. He wrote several books on the House of Romanov and two other books on the naval landscape pre- and post-1914 (i.e. Dreadnought era) Robert K. Massie, Narrator of Russian History, Is Dead at 90 - The New York Times (nytimes.com) I just finished reading his +900 page on "Peter the Great". What a fantastic read. The man was a clossus. A force of nature. Against interia itself he pulled the Russian people out of doldrums into the European stage and into a major power. The book is very well written and reads like a novel. The author does a really good job in explaining the European political situation. Where is the Ottomans, the Hapsburng, the Prince of Orange, Louis XIV, they all get a detailed explaination by the author. His four books on the Romanov are: Nicholas and Alexandra (written in the 1967; which actually became Book 3) Peter the Great (written in 1980, which became Book 1) Catherine the Great (written in 2011, which became Book 2) Final Chapter (2012?) I have bought the first three books and read only Peter the Great. Will read Catherine the Great in 2023. ----------------------------------------------------------------- Below I copied 4 excerpt from the book. Excerprt 1 talks about the origin of Russian flag. Excerpt 2 is about the Port of Archangel. It was truely the only sea-link that Russia had with the outside world pre-Peter era. It took a Peter to expand into the Baltic sea and it took a peter to challenge the Turkish dominion over the Black Sea, which was considered a Turkish lake till then. It would however be in the reign of Catherine, that the Russia would make most progress against the decaying power of Persia and the Ottomans. Excerpt 3 is about the tax policies and the enormous burden that the Russian people carried to fuel Peter' titanic ambitions. Excerpt 4 is about St-Petersburg, when and where it was created (how high it was on a frozen wasteland). And the force of personality that pushed for its construction and completion.

-

"Tell me the currency, I would tell you when was the supercycle bull market" that is what Jeff Curie would say. He said that comment few years ago pre-Covid, when he was explaining that while the peak and the pinch in oil price was $147 per barrel in North America in 2008-09, the emerging market (like Brazil) saw that pinch not in 2008-09 but rather in 2018-19 during unprecedent strenght in the U.S. Dollar. I may be fuzzy on the detail. Gold may not have worked for US or Canadian petro-dollar currencies, but probably worked wonderfully for emerging market holding gold in their currency.

-

Yeap, we really don't know much. We have few random datapoints from different sources. I want my books now ! And to your point only when a major milestone is achieved (a fall of a city) that goes toward tangible book value. Everything else is Goodwill till then

-

convicts/criminals in front, followed by freshly drafted conscripts, followed by regular season forces holding the rear and shooting deserters.

-

Just to clarify my comment. A possible move by the “system” against its patriarch is not meant to please the West or end of the war. But to save the whole complex from being toppled, if pressure goes up really high internally to the point of no return. The outcome will be whatever it will be but the complex will be preserved at all cost. Where we are in that “pressure gauge” we have no idea. @no_free_lunch On your comment about peace, I would argue that (1) Ukraine can re-arm and heal much much faster than Russia while it has the goodwill of the West and a flow of aid. But that goodwill will not last forever (war fatigue is a real thing) (2) Russia is at the point of not being able to try again anything for a very long time (3) the real political change/consequences and backlash in Moscow will happen AFTER the war ends and Russian troops are back in their base and homes. Not before. It will be a political shitstorm, which the system cannot deal with because there is a war. Once that ends the internal squabbling will really start. A peace may cost Ukraine some territories. Not the first time an aggressor takes another one’ territory nor will be the last time. Zelensky’ call to make, and happily not mine.

-

we are blessed with two large bodies of water protecting our western and eastern flanks. a southern neighbour that is culturally, economically, politically aligned with us and a northern frontier guarded by polar bears and one or two CF-188s.

-

Happy Thanksgiving to our friends and neighbours in the south.

-

Thanks. I am less familiar with that period. I referred to the word “system” in my earlier post. Going back to Yeltsin era, I would say that the “system” in the 90s was the oligarchs, who decreed by consensus. And they did save themselves (or so they thought) by backing Putin at the time. The “system” today is unlike that of the 1990s with the de-centralized gang of oligarchs. The “system” today is the Russian political and security establishment that presides over an immense amount of wealth and assets that have been accumulated over the past two decades. At the very top seats the patriarch. If the war continues to take a political and economic toll, in my opinion that rent-seeking establishment will move first and fast before such ‘revolutionary’ ideas take hold and topples the whole complex. There are no Vulcans in the Kremlin, but they do follow the ethos that “the need of the many outweighs the need of the one” Who and what comes after, we don’t know.

-

If I am not mistaken we are hitting all time highs !

-

The rent-seeking system will save itself before that happens. Too much at stake ! Putin’s vertical of power or not, such overt failure is not looked upon kindly and nor tolerated. If he cannot end the war satisfactorily, than the system (not people) would move against him.

-

“Lock her up! Lock her up!” That is all I got to say about Holmes. Mr Sokol, I don’t understand you.

-

I heard his name a lot when I was a kid. He was the “heir” before losing to an internal coup and being put in house arrest permanently. If Khamenei survived for +30 years it was only due to how cunning he was in eliminating rivals. It is really hard to say (answer yr question) but I would say there is everything wrong when power and religion are mixed into one voice. The little I know of Montazeri was that he could have been the passive “paramount leader” on the top.

-

Agreed. And a paranoid regime could be at its worse. Tightening the screws even more. The other alternative is that the people with the most to lose (elite* with commercial interests) would throw in the towel with the current masters (Clerics) and outcome of that would be nationalist regime but in the hands of military (elements of IRGC perhaps) and the likes bent to do major reform but also to keep its interest. *they have red lines too. But I don’t think you ll see a wholesale 1979 like situation. If it’s close to that, external forces wouldn’t be able to resist the temptation to interfere (if not already), and if done overtly as an attempt to break the nation, this may act as a dampener. Just like how Iraqi invasion in 1980 acted as a unifying forces and ultimately made the regime what it is today.

-

The Western and Israeli intelligence are not saint, if they could create a civil war at a cost of 100,000+ death they would. No ethics. It be would be as easy as drinking water. No second thoughts. All fun and game. And 15 years later they would get Michael Bay make a Hollywood movie about a few fancy Navy Seals doing “heroic” things. A broken country is far less likely to be a threat than a stronger one. But fair is fair, this specific situation is on Iran’ own government mismanagement of resources along other things (a very long list). And it has been compounding for a long time. Sadly Western sanctions made the bad actors stronger as they control the international trade routes, borders. The initial blame though lies squarely with one person only (“paramount leader” and his cronies), who on an unrelated note, interestingly enough is not even Persian but is an ethnic Azerbaijani lol. What is so unique about the death of that lady was that she was a nobody. Just came to visit the capital as tourist. She was not an activist. She was not journalist. She was not trying to make troubles with government. Just a normal person from the provinces going to visit Tehran. And that struck a chord with people, who saw her as themselves, or their own sister etc.

-

-

-

That was 4 days ago. Come now, Mr Zelensky, no one is going to think any less of you. Shit happens. Unfortunate but understandable. “own it” and move on. It is not worth it. As tempting as it is.

-

More or less a good speech. I browsed through it fast. Prefer video format when it comes to speeches to better gauge their body language (genuineness etc). That said, too bad that level of global leadership wasn’t there in 2003-05. “Aeroplane mode “ON””.

-

No relation. Just a coincidence. It was always bound to happen. People had it with the elite pillaging the country. The actual trigger could have been anything. These things cannot be predicted in terms of timing. Now that is not to say Israel/U.S./Saudi are not taking advantage and doing what whatever that they do best. (I.e creating more problems and making life miserable for the commoners) @Spekulatius Nope. U.S. is always enemy number one.

-

anything is possible and clearly I am not the one who is going to guess correctly. But I would caution against extrapolating the trend line. You can have multiple reversion to the mean, for various completely unrelated non-military and military reasons. when a war goes on for 4 years or 6 years, it was never foreseen to last that long in the first year. There could periods where both sides just lick their wounds for months on ! Before another phase of high intensity activities starts.

-

damn. Paywall. But I got the first paragraph and the jest of it. Well, the general is a student of military history and a no non-sense military man. But he is also subordinate to his civilian commander in chief. And therefore should probably keep in line of the chain of command. I ll look to find that speech that he supposedly gave to the economic forum.

-

my guess is that they (Russia) has far better intelligence about Ukrainian infrastructure since Ukraine inherited the old Soviet energy, power etc infrastructure. And those are fixed and highly knowable targets. whereas the intelligence from command and control, weapons depot location is not there. As they are far more mobile. And probably better “managed” by the Ukrainians since the start of war given that they are obvious targets.. lastly, I also think the Russian missile campaign against infrastructure has been months in the making. The media here has painted it as knee-jerk reaction to the bombing of Kerch bridge and Ukrainian rapid advance in Kharkiv. But I believe it was always bound to happen. But the timing was set by the Kremlin to be on the eve of the Winter for maximum impact. Perhaps pulled forward by a few weeks so that can also “package” it as well as a response to Kerch, while they are at it.

-

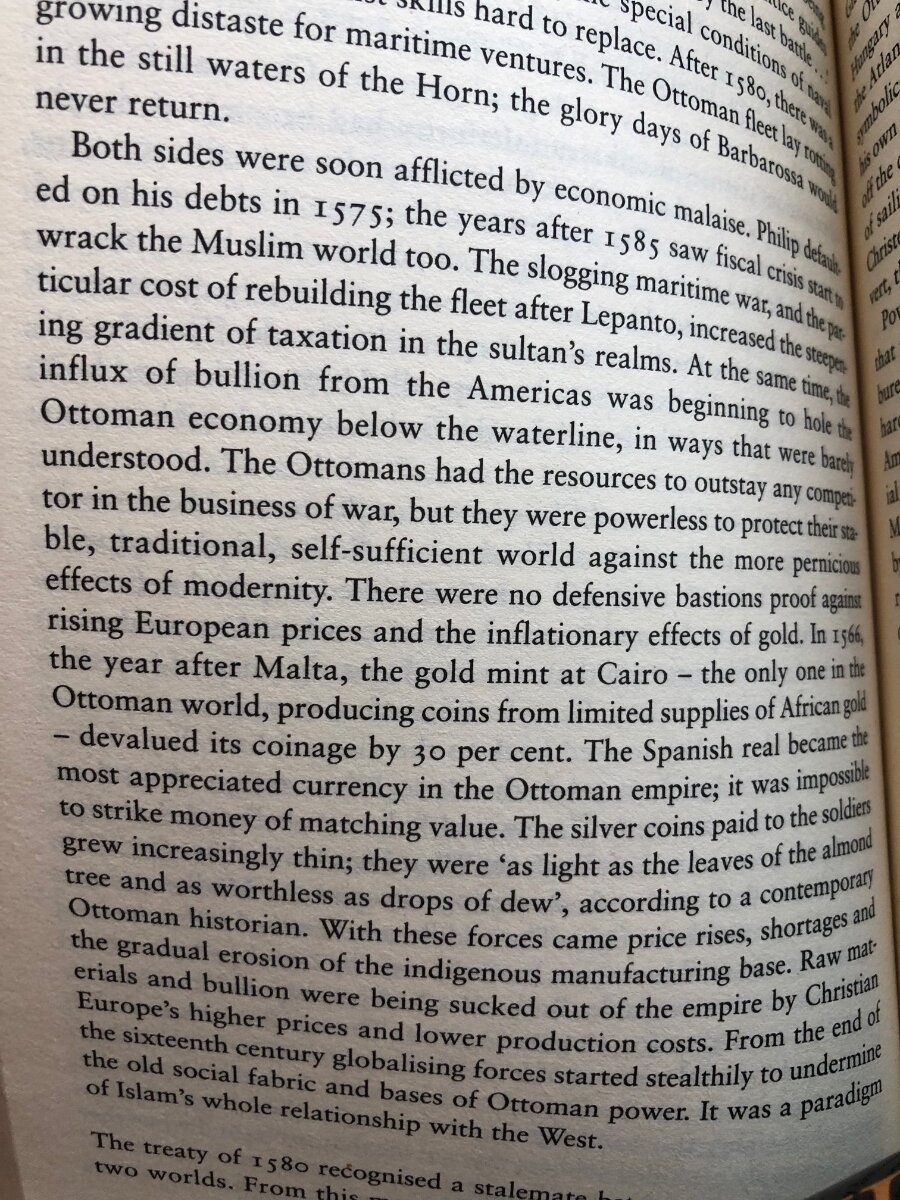

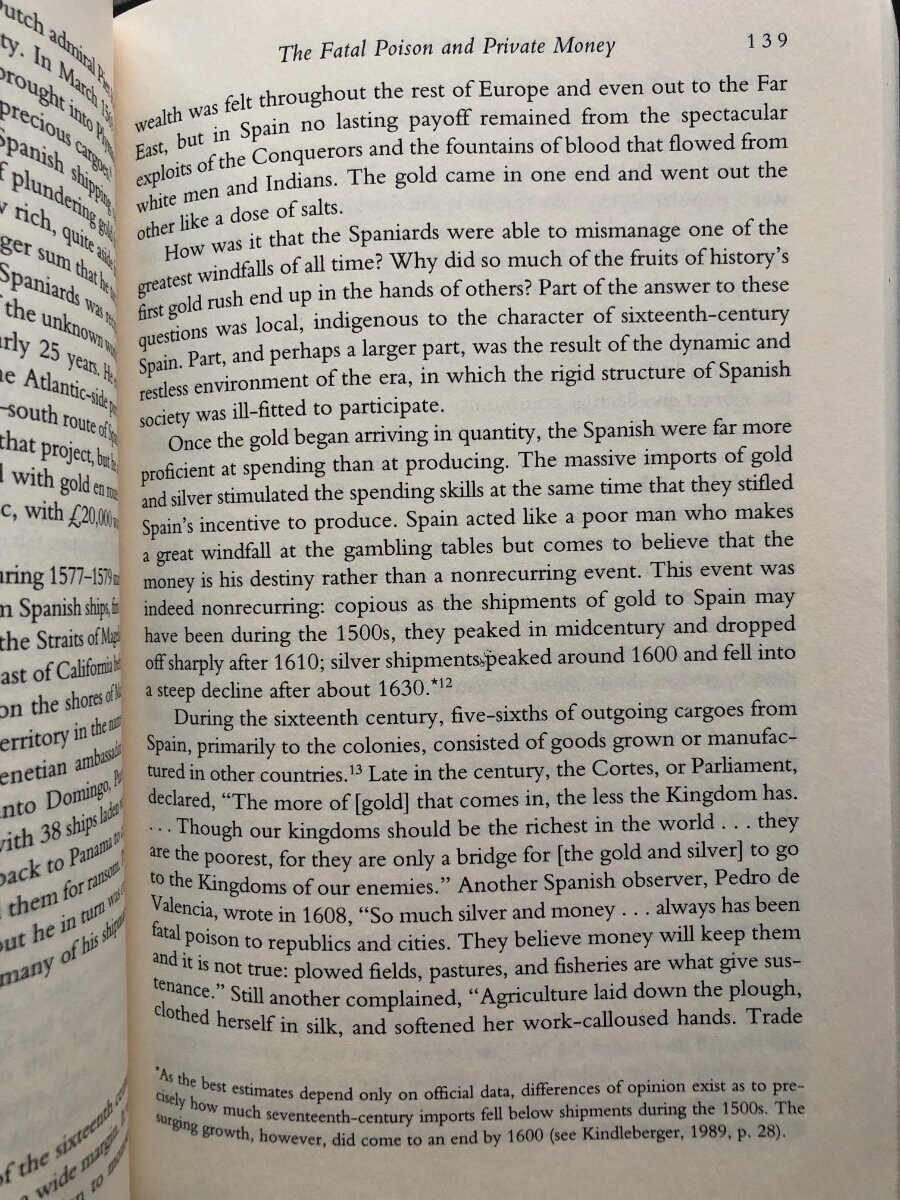

Thanks for posting. Looks like Spain had caught the Dutch disease before the Dutch, they just did not know it at the time. Speaking of the curse and blessing of the Spanish gold, I went down to Xerxes's Imperial Archives and pulled out these two ancient scrolls, concerning the Curse. Here are the passages: "... At the sametime, the influx of bullions from the Americas, was begening to hole the Ottoman economy below the waterline, in ways there were barely understood. The Ottoman had resources to outstay any competitors in the business of war, but they were powerless to protect their stable, traditional, self-sufficient world against the more perinicious effects of modernity. There were no defensive bastion against rising European prices and inflationary effect of gold. In 1566, the year after Malta, the gold mint in Cairo - the only one in the Ottoman world, producing coins from limited supplies of African gold - devalued its coinage by 30 percent. The Spanish real became the most appeciated currency in the Ottoman empire ... " Empires of the Sea: The Siege of Malta, the Battle of Lepanto, and the Contest for the Center of the World: Crowley, Roger, Lee, John: 9781400157228: Books - Amazon.ca Second passage: "Once the gold began to arrive in quantity, the Spanish were far more proficent at spending than at producing. The massive import of gold and silver stimulated the spending skills at the sametime that they stifled Spain's incentive to produce. Spain acted liked a poor man who makes a great windfall at gambeling tables but comes to believe that the money is his destiney rather than a nonrecurring event. ..... the more gold that came in, the less the Kingdom has, Though our Kingdom should be the richest of the world ..." The Power of Gold: The History of an Obsession: Bernstein, Peter L.: 9780471003786: Books - Amazon.ca

-

finally someone who knows what he is talking about. I mean within the circle of officials. Not commenting against anyone in this thread. I am equally ignorant.