Xerxes

-

Posts

5,689 -

Joined

-

Last visited

-

Days Won

9

Content Type

Profiles

Forums

Events

Everything posted by Xerxes

-

Thanks @Dinar Goes to show how much we don’t know on this side of the pond. And even perhaps in Europe as well. I don’t know about all other posters in this thread but I for one am unaware of these subtleties. If it doesn’t make it to BBC, CNN or The Simpson, it is not real. (sarcasm)

-

I recall you had a juicy trade on Overstock in 2020, one of your best ones. I don’t know if you can share this but were you also trading it prior to 2020. Also I think Fairfax was also an owner (they sold way too soon), would you know anything on top of your head, in terms why they were interested in the name. Was it a classic founder-turn around situation or more like pennies on the dollar value trade. thanks

-

@Spekulatius Spek, firstly I don’t think anyone is saying that. In fact I don’t even think anyone has said they should get zero support. Of course people having conversation in this thread to which degree there ought to be support (and consequences of). And those very same conversation are happening in the White House or other forums in the past six months. Doesn’t mean you can go around label people genocidle. secondly, you (and I don’t mean you personally, so pls take no offence) cannot choose when it is convenient for you to give damn about victims. And when put on your “airplane mode” on, and look the other way, because it is an inconvenience and you cannot be bothered. There is nothing cool about wars, genocides, that people should chose one set of circumstances over others. thirdly, unfortunately every genocide looks like a line or a paragraph in history books 100 years later. You are right in your comment about a genocide 150 years is no excuse to stand idly by. And those poor aboriginal people were probably saying/thinking the same thing even as they got hacked down (anyways) by the white colonizer. Everything is relative. We may have the a good excuse to help install Pinochet as a dictator in Chile, because Cold War, fighting communism etc, but surely the Chilean didn’t see it like that at the time, and said “WTF”. The Indians that got massacred by the Portuguese as the latter were building their commercial network in the Indian Ocean probably said: “WTF i thought we were pass this. This the fifteenth century for Christ sake !!!”. In 1991-92, after the Gulf War, Bush Senior got the Iraqis and the Kurds to rise up against Saddam, from north and south, only to let Saddam massacre them, so that the centre of power is preserved. What about that genocide and the enablers behind it ? Was there a forum thread on that ? Or there geopolitics trumped everything else. Everyone relative point of view of “oh we don’t do that anymore. We are in a civilized age”, is built on the skulls and bones of the last genocide. Once we are done with genocide, we declare the beginning of a new civilized age, built out historical monument and accuse another party that is trying to crash our party. Lastly, I think tribalism has now taken over this thread. I say this about the fall of Kherson. Happy that it happened on Nov 11.

-

@no_free_lunch you are sounding more and more like a Western teenager overexcited by war. Or should I say you are being “selective” in terms of what wars of aggression excites you to the point of hysteria and which ones doesn’t. Hint: It excites you if the victim are white people, and you couldn’t care less otherwise. Nope you don’t say it, but it is all subtle in between the words. And you are not the only one. I must be the only one on this board that actually lived in a country at war, where the aggressor was backed by all Western major powers, where cities were burned, people were raped, families were destroyed, infrastructure was destroyed, where WMD was used …. For 8 years ! So forgive me, if I am not as naive and stupid as you are. Given these last comments from you, me and you will have nothing else to discuss. I don’t have time for the likes of you. But just to close on this last point, understand however that political powwow and reality on the ground are not the same. George Bush declared mission accomplished in 2003, only to order a major Surge in 2008. Hence my comment of me not caring about Kremlin says. You want your enemy to remain stupid. An enemy that can make a decision to withdraw (as oppose to hold out) is one that acting more rationally and one that is less stupid. And yes independently of whatever Kremlin says about annexation and Kherson forever etc.

-

This is amazing https://ca.yahoo.com/news/mystery-flag-honour-dieppe-raids-015703175.html

-

@no_free_lunch yes, clear headed as oppose to turning that force into Chuikov 62nd Army and telling them to hold the ground. That is being clear headed. Don’t confuse Putin’s political powwow with realities on the ground. but I guess believe whatever you want @shhughes1116 yes, in contrast to the rout in Kharkiv (obviously). There is a difference between the speed at which that northern front unravelled and the slow grind in the south.

-

I would add that the retreat of the seasoned forces in proper order (as opposed to being routed) actually implies some proper strategic thinking by the Kremlin high command. They are being clear headed. Never a good thing, when the enemy is being clear headed. So it is good for the people of Kherson that they are (allegedly) gone, but bode less well for the war effort, messa think.

-

Understood, I just thought perhaps you meant different bridge. Thanks.

-

There is no relation between the explosion Kerch bridge and Russian withdrawal from Kherson. Perhaps you meant the bridges on the Dnipro river being taken out via HIMARS, cutting off supply lines. That said, I had found the news flow very confusing around the region of Kherson. Talks of mined dam upstream, potential Russian trap as it was reported by Kiev, definitely Ukrainian did not have the field day they day around the Kharkiv region back in August.

-

I was also intrigued by @Dazel statement. This is how I played it in my head: recession hits, yields crash, T-bill gain value At some point the yield curve moves from flat to an steepening one in the middle of recession, as it sees the economy recovery, with the back end yield shooting up, the 10-year treasury becomes a sought to asset.

-

Was that a bet on Fairfax that he made, or a beta bet on central bank intervention producing results and using FFH as a vehicle to capture that since he knows it best and controls it. To me that was a beta bet for him and those of us who added in 2020, but to bet in 2022-23 on Fairfax that would be a true alpha bet on Fairfax’s unique attributes.

-

See this new thread by Spek There is a bit about the “Grivalia story”. Perhaps Video becomes available at a certain point. https://greekvalueinvestingcentre.com/wp-content/uploads/2022/10/1.George-Chryssikos-The_Grivalia_Story-1.pdf Keynote Speaker Presenter: George Chryssikos, Vice Chairman, Non-Executive Director of the BoD, Eurobank Group, Athens, Greece Topic: “The Grivalia Story” View PowerPoint Presentation Video Not Available Yet

-

Pershing Square is trading at 30% or so discount to NAV, is it a “legacy trust” issue going back to the go-go days of Valeant now like 5-6 years ago.

-

We got Bloomstran covering Berkshire every quarter and we got Viking covering Fairfax every quarter !! Thanks to both of them

-

And the likely equity-accounting of Occidental (I think)

-

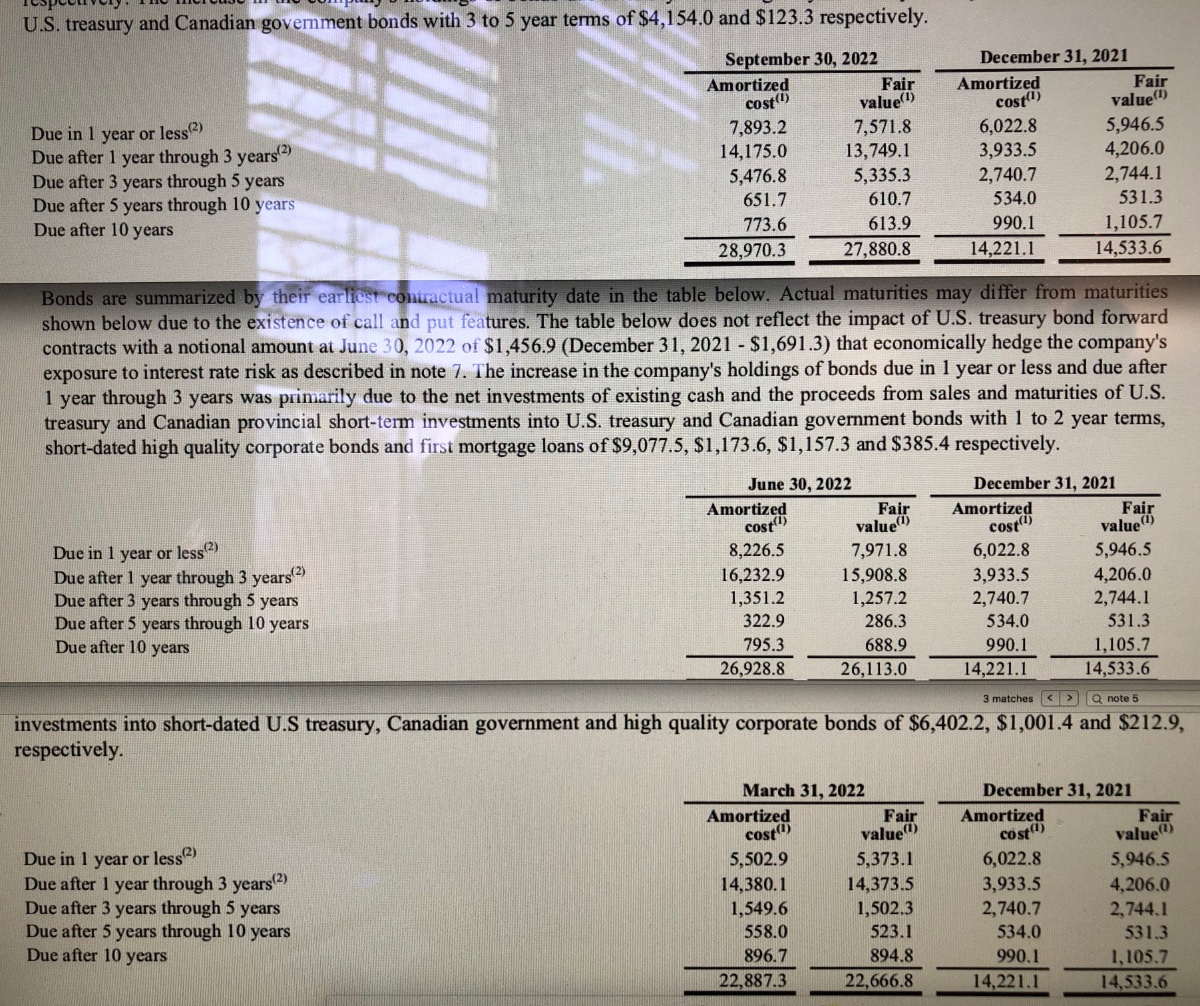

Just to capture the sequence of events since Dec 2021 till close of Q3, 2022. The big dollar increase in terms of investment in bonds/bills (funded from actual cash/cash equivalent) actually happened in Q1. In Q2 and Q3, I am thinking that the duration moved from 1.2 to 1.6, as treasury bonds/bills are getting recycled into longer dated ones. But the big thing was in Q1 in terms of fresh dry powder deployment.

-

I saw a note that says Apple is now valued more than Amazon, Facebook and Alphabet combined !! Wow. $1.1 trillion for Google $938 billion for Amazon $238 billion for Meta The last of the “Generals”, Apple, holding the line at $2.3 trillion. Today, would you rather pay $2.3 trillion to buy the whole of Apple or would you rather own the whole of the trio of Amazon, Google and Meta at these prices.

-

I am not used to see FFH doing a jump post earning. Uncharted territories for me. Using TwoCitiesCapital rule of thumb, it usually takes a few days post earning for FFH to react.

-

what you mean is “a nation state would launch a full scale assault on another state, POPULATED BY WHITE PEOPLE” Anybody (even folks who don’t follow this stuff) can do a quick Google search. The list does not include “proxy” and “hybrid like war”

-

^^^ Hopefully it is not going to do a U-turn once it gets above $1,000 (ala Paypal) because FFH management did not lock into longer duration, and when the next monetary easing cycle starts, all the 2-years T-bills will be rolled into lower yields, effectively making this a one-time boost Funny enough almost all the companies seem to have had their "Covid accelerent" in some fashion or another. Some earlier and faster, some later and slower, but always there ....

-

30% return in the past 12 months while market overall did not perform well. Not bad ! I was hoping for a little "deflating" of FFH prices heading into Q3 results, but looks like it is getting a bid instead

-

Great podcast on this new edition

-

Stocks for the Long Run: The Definitive Guide to Financial Market Returns & Long-Term Investment Strategies, Sixth Edition: Siegel, Jeremy: 9781264269808: Books - Amazon.ca The sixth edition of a classic, updated for most recent events. "The definitive guide to stock trading, Stocks for the Long Run has been providing the knowledge, insights, and tools that traders need to beat the market for nearly 30 years. This new edition brings you fully up to date on everything you need to know to draw steady profits for yourself or your clients. It’s been updated with new chapters and content on: • The role of value investing • The impact of ESG―Environmental/Social/Governance―issues on the future of investing • The current interest rate environment • Future returns investors should expect in the bond and stock markets • The role of international investing • The long-run risks on equity markets • The role of black swan events, such as a pandemic You’ll also get in-depth discussions on the big questions investors face: Are we seeing the eclipse of capitalism? What do global changes like climate change mean for markets worldwide? Stocks for the Long Run is essential reading for every investor and advisor who wants to fully understand the market, including its behavior, past trends, and future influences-in order to develop a prosperous long-term portfolio that’s both safe and secure."

-

The Titanium Economy: How Industrial Technology Can Create a Better, Faster, Stronger America: Padhi, Asutosh, Batra, Gaurav, Santhanam, Nick: 9781541701878: Books - Amazon.ca Just a placeholder if anyone has read this book. The author did the round in a few podcast "The future of the American economy is hiding in an unlikely place: the manufacturing sector While Silicon Valley titans dominate headlines, many of the fastest-growing, most profitable companies in the United States are firms you’ve likely never heard of, such as HEICO, Trex, and Casella. These booming companies belong to a burgeoning sector—industrial tech—that offers surprising hope to workers, consumers, and investors alike. Their role: to make a range of products—aerospace parts, for example, or recycled plastic lumber—that quietly form the backbone of America’s biggest industries. In an age of instability, industrial tech is a cornerstone of our economic future. In this book, McKinsey veterans Asutosh Padhi, Gaurav Batra, and Nick Santhanam reveal the “titanium economy,” a modern, reinvented industrial sector complete with high-paying, domestic jobs;, soaring stock prices;, and critical infrastructure. They dispel the myth that the best of American manufacturing is behind us and illuminate an opportunity for a brighter future—if we can seize it."

-

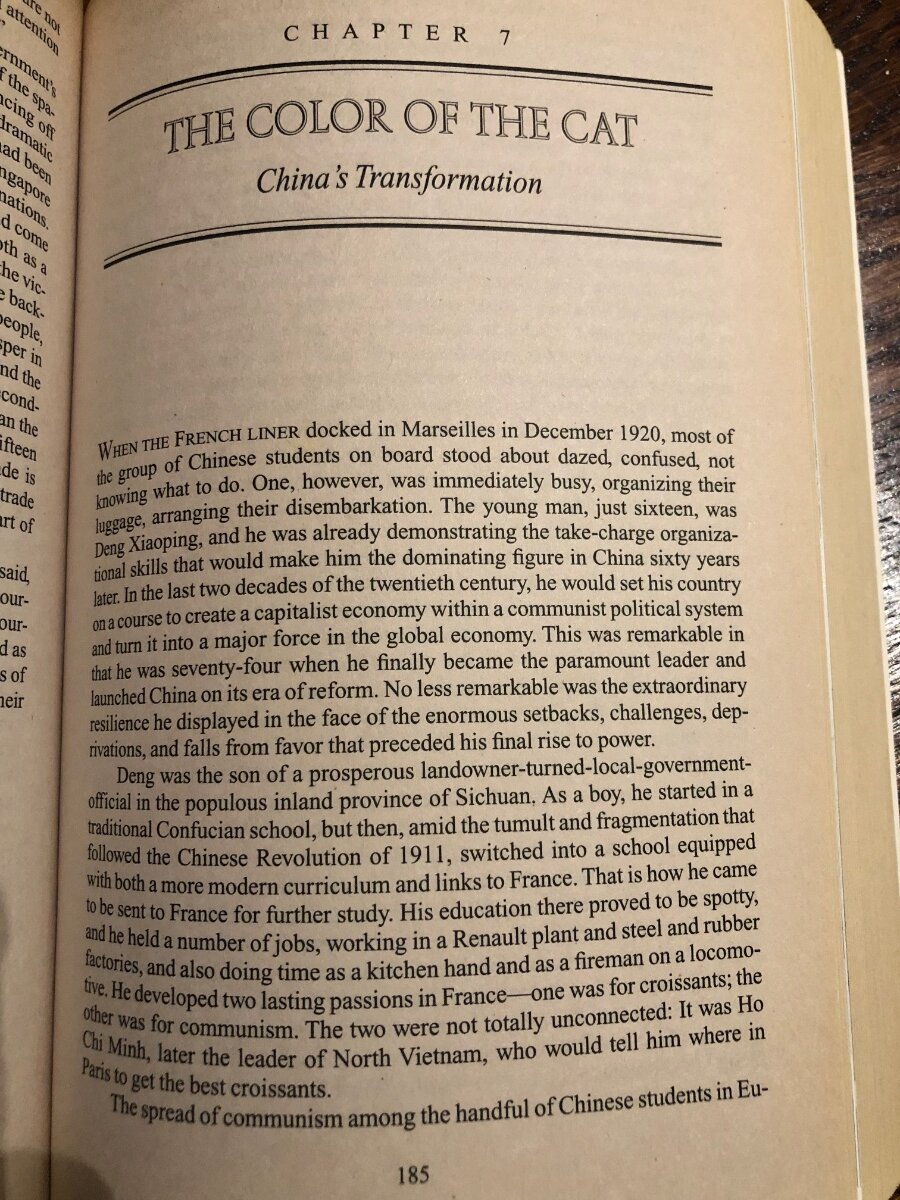

I think you mean pre-WW2. Notwithstanding the Wilsononian involvement in the First World War. On “China and Russia JUST deciding” I am not sure where you guys get this stuff. This is not 2022 news. China was once a great power, before the Opuim wars and before its humiliation by the Europeans. We may have short memory, but history remembers. That great power vision may collide with our more liberal vision of world. But it does not mean they JUST decided something. It is worth re-reading the first paragraph on one Daniel Yergin’ lesser known books: “The Commanding Heights”, shown below. This first paragraph speaks volume of Deng Xiaoping resiliency, him setting the stage and that of the current paramount leader that will now see that vision through. “Hide your strength and bide your time” Deng Xiaoping said at the time. Now comes the next step …