nwoodman

-

Posts

1,166 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Posts posted by nwoodman

-

-

25 minutes ago, SafetyinNumbers said:

Rebalancing occurs every quarter in March, June, September, December which makes Feb 29, the measurement date. The rebalance occurs on the third Friday of the month and they give two weeks notice via press release so that’s why I think we’re live tonight. I think the odds are under 25% though given the historical precedent of 20bps threshold in the 60 for kicking a constituent out.Ta, if that’s the case, then our AI overlord (unchecked) offers the following future dates if it doesn’t happen tonight:

“Based on the rebalancing schedule that occurs every quarter in March, June, September, and December on the third Friday of the month, with a two-week notice given via press release, here are the dates for 2024:

- **March Rebalance:**

- Rebalance Date: March 15, 2024

- Announcement Date: March 1, 2024- **June Rebalance:**

- Rebalance Date: June 21, 2024

- Announcement Date: June 7, 2024- **September Rebalance:**

- Rebalance Date: September 20, 2024

- Announcement Date: September 6, 2024- **December Rebalance:**

- Rebalance Date: December 20, 2024

- Announcement Date: December 6, 2024These dates align with the criteria of rebalancing on the third Friday of the specified months and providing a two-week notice before the actual rebalance occurs.”

-

Thanks @SafetyinNumbers. It all appears like the dark arts to me, especially the committee’s discretion. I understand that rebalancing is done quarterly, however could I trouble you to point me to where it specifically states that tomorrow is the decision making day?

Index inclusion is hardly central to the FFH thesis but I find the discretionary aspect a bit of an eye opener as far as indexing more generally

https://www.spglobal.com/spdji/en/documents/methodologies/methodology-sp-tsx-canadian-indices.pdf

S&P/TSX 60 Methodology

The S&P/TSX 60 is a subset of the S&P/TS Composite. It has 60 constituents and represents Canadian large cap securities with a view to reflecting the sector balance of the S&P/TSX Composite. In using trading data to determine any matter relating to the S&P/TS 60, including index composition and calculations, trading data on the TSX and U.S. exchanges is reviewed.

Additions to the S&P/TSX 60

- To be eligible for inclusion in the S&P/TSX 60 index, securities must be constituents of the S&P/TSX Composite.

- When adding securities to the S&P/TS 60 index, the Index Committee generally selects amongst the larger securities, in terms of float QMV, in the S&P/TS Composite. Size may, however, be overridden for purposes of sector balance as described in item 4 below.

- When adding securities to the S&P/TS 60 index, the Index Committee generally selects securities with float turnover of at least 0.35. This is a guideline only and may be changed at the discretion of the Index Committee. In addition, this range may be overridden for purposes of sector balance described in item 4 below.

- Security selection for the S&P/TSX 60 index is conducted with a view to achieving sector balance that is reflective of the GICS sector weights in the S&P/TSX Composite.

- Minimum index turnover is preferable. Changes are made to the S&P/TSX 60 index on an as needed basis. The most common cause of deletion is merger or acquisition of a company. Other common reasons for deletion include bankruptcy, restructuring or other corporate actions. If a company substantially fails to meet one or more of the aforementioned guidelines for inclusion or if a company fails to meet the rules for continued inclusion in the S&P/TS Composite, it is removed. The timing of removals is at the discretion of the Index Committee.

-

Not trying to labour this but genuinely interested as to when a company that has a top 30 market cap gets included in a diversified national index comprising 60 companies.

-

I have been using this for a while too. It’s very difficult to go back to normal search, that’s for sure. The potted questions are a bit hit and miss at times but the referencing is brilliant. For technical engineering searches it has proved invaluable and easily justifies its cost.

For investment research it is OK to good. It sometimes dives into filings but more often than not gives the usual lazy Chat GPT response eg.“one would typically look into annual reports, SEC filings, and other detailed investor communications that outline the company's strategic investment decisions over time. However, these details are not provided in the current search results”

-

58 minutes ago, petec said:

Yes - I've been thinking this for a while.

Don't they have equity in Altius as well as warrants?

Spot on!

“The Warrants and the Preferred Securities were originally issued on April 26, 2017. Prior to the Transaction,

Fairfax directly or indirectly owned or controlled an aggregate of no Common Shares, 6,670,000 Warrants

and $100 million Preferred Securities, which represented 13.94% of the issued and outstanding Common

Shares as of April 14, 2022, on a partially diluted basis. Following the completion of the Transaction, Fairfax

will directly or indirectly own or control 6,670,000 Common Shares, which represents 13.94% of the issued

and outstanding Common Shares as of April 14, 2022, on a non-diluted basis, and Altius will have no

outstanding Warrants, Preferred Securities or resulting interest distribution obligations.” -

Highly recommend “Boy Swallows Universe’ - Netflix Quirky, dark and uniquely Australian. The 80’s soundtrack was worth it alone. Brought back some great musical memories. Will be watching this one again

-

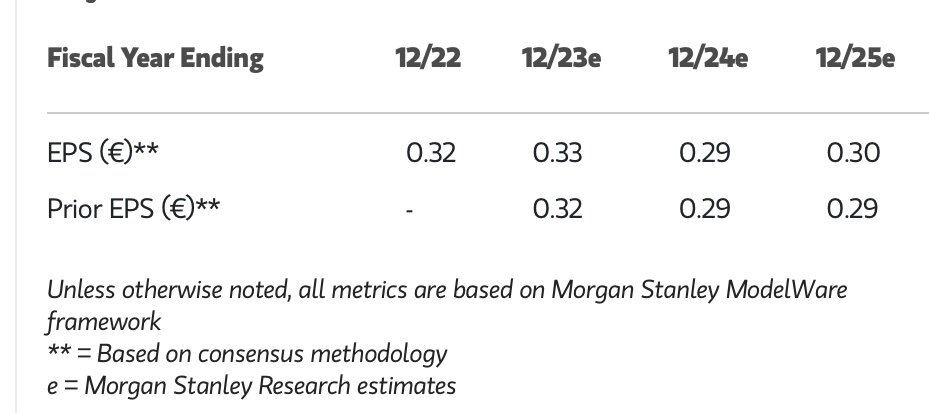

MS with a minor upgrade to Eurobank ahead of earnings. Revised PT €2.35 from €2.33

“We update our model ahead of 4Q23 results. We lower opex marginally to incorporate one offs related to floods in 3Q23 and restructuring cost. Our FY23-25 EPS is up by ~1.5% and our PT increases by ~1% to EUR2.35. We remain Overweight.

- A strong balance sheet means that Eurobank is one of the the most resilient Greek banks in our coverage. We expect performing loans to grow at a ~6% CAGR (pro-forma for Hellenic bank acquisition) in 2023-25.

- We forecast NIMs to decrease by 2bps in 2024 followed by a 13bps contraction in 2025 (pro-forma for Hellenic bank acquisition), as we expect the rate-cutting cycle to begin in 2Q24, thus driving asset yields lower.

- 3Q23 NPE ratio stood at 5.0%; we forecast it to reach 3.6% by 2025.

- We see the Hellenic Bank acquisition as accretive for the bank.”

So roughly a $2.5 bn equity position for Fairfax at an earnings yield of 15% for the foreseeable future. Every “little” bit helps.

-

https://www.fairfax.ca/press-releases/fairfax-announces-acquisition-of-additional-orla-shares-3/

“Orla and brings Fairfax’s total holdings, through its insurance subsidiaries, of such securities to 55,405,229 Common Shares (or approximately 17.58% of all Common Shares).”

$3.375 at the time of writing, makes this a $186m position. A bit more than a passing phase.

Between Orla and Foran it’s close to $400mn. Throw in the Altius warrants and it is close to $500 mn. Then take the Exco and Occidental positions that’s another $900m or so. Taken as a basket, you could almost argue that commodities is their third big equity idea after Eurobank and Poseidon/Atlas.

No idea about Exco, but the others seem to be long life assets and not just cigar butts.

-

For real? Results were good, but I thought the old boy did a good job of hosing future expectations. This market feels awefully bubbly.

-

46 minutes ago, ValueMaven said:

Where can I read about the history of FFH's ownership of Eurobank?

You could always try the EGFEY (ADR) thread. In a nutshell Prem tried to repeat the success with Bank of Ireland. It’s been a hard slog but is working nicely for shareholders now. Their perseverance with Eurobank has been brand accretive.

https://en.wikipedia.org/wiki/Eurobank_Ergasias

-

21 minutes ago, vinod1 said:

I think the more likely mistake we are likely to make is sell too soon. If it goes up to 1.5x tomorrow, selling out I think would likely be a mistake.

The slower it revalues upward the better off we might be.

This. I want any forced decision making deferred as long as possible. The current price +/- 10%, growing around 1% per month , for the next 10 years or so, is fine. If it turns out to be 0.25%/week even better.

-

@Luca Spectacular. Looking to head to Japan next season for some skiing

-

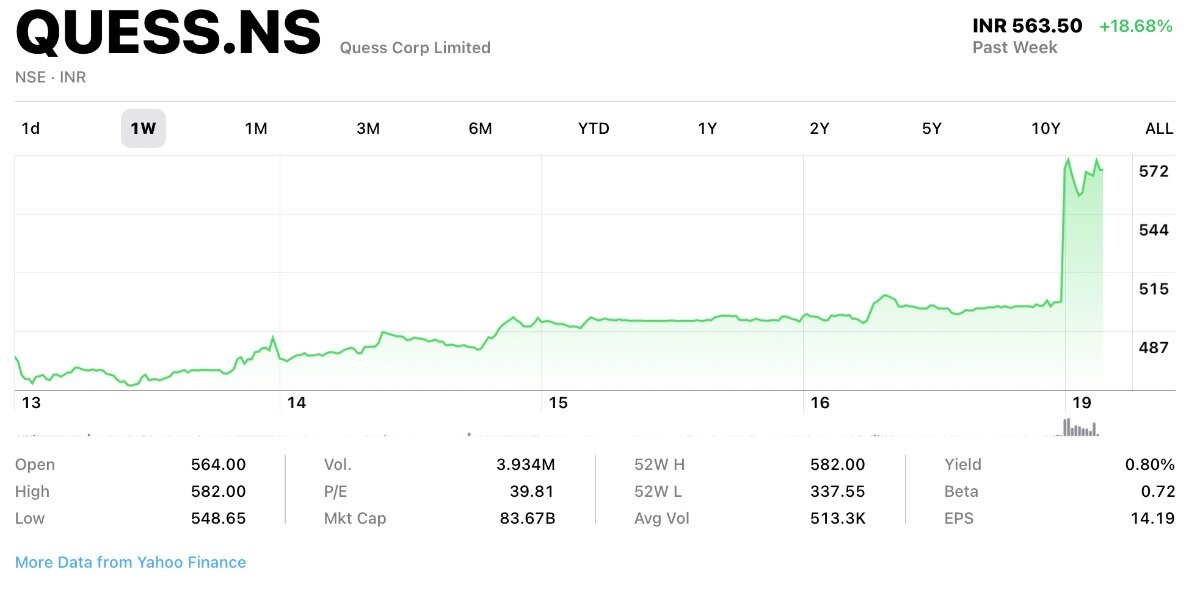

Market is enjoying the Quess demerger announcement

-

On 2/16/2024 at 3:53 AM, LC said:

That's kind of the only thing that attracts me to Sony as well.

I assume you think UMG is too expensive on a relative basis? UMG you get a pureplay and slightly better market positioning. I do like some of Sony's other businesses (gaming), but it's a huge conglomerate and my knowledge is cursory - I don't know what could be creeping under the surface.

Thanks, I need to do a side-by-side comparison with UMG. Sony's not cheap, but I consider it well-run. It's only a 2% position for me, but set-and-forget. I think they are executing well despite all the handwringing that goes on in the gaming division, a lot of which is misreporting.

Take Helldivers 2, for instance; that's a PC/PS5 release that's currently going absolutely ballistic and hopefully alleviating some of the cynicism about live service games. While not my bag, if people are going to game, I think it is better to do it with your mates and have a laugh. Helldivers 2 looks like a hoot

-

1 hour ago, valueventures said:

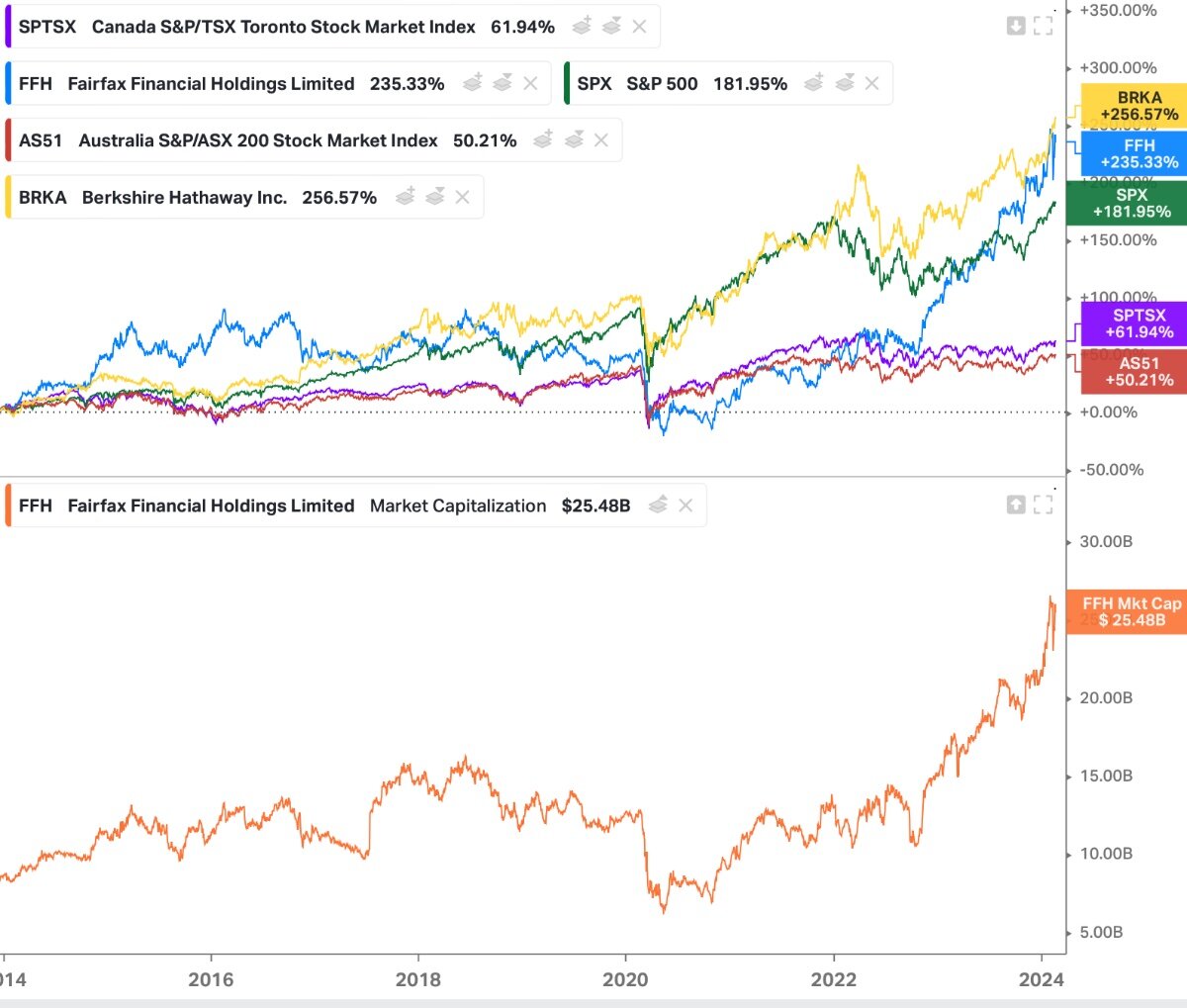

Apologies if this has already been discussed in detail, but does anyone have updated thoughts around FFH's possible inclusion in the S&P/TSX 60 this year? Seems like the most mechanical means of facilitating more institutional involvement in the stock and driving up P/B.

I believe FFH already qualifies for the index based on its size, so curious to hear what is holding it back. Thanks!

@SafetyinNumbers seems to be the resident expert here. However from what I can gather it is in the hands of the committee because as, as you rightly point out, they meet the following criteria:

1. Market Cap

2. Liquidity and Trading Volume

other things that will be considered by the committee are

3. Public Float

4. Financial Health

5. Sector and Industry Representation

6. Compliance and Governance

Not sure how the Muddy Water shenanigans affects the process, it shouldn’t but who knows. I will say one thing though the TSX60 has been a real laggard.

The demand from Index inclusion would make ideal conditions for unwinding the TRS position.

-

Discussion on BNN regarding results and the CC. I'm not sure who the grey-haired gentleman is and he is a bit waffly for my money. However, the upshot is a message of

1. They've been here before and survived.

2. Stellar results.

https://www.bnnbloomberg.ca/video/fairfax-operating-income-jumps~2868708

and another one

I think this coverage has been gold.

-

Just worked my way thru the Q4 23 conference call. Jen Allen did a good job of addressing the MW allegations. Lots of good information but my top four responses were as follows:

1. Forward Guidance

Prem Watsa“Now as I’ve said for the last number of quarters, the most important point I can make for you is to repeat what I’ve said in the past - for the second time in our 38-year history, I can say to you, we expect - there is of course no guarantees - sustainable operating income of $4 billion, operating income consisting of $2 billion-plus from interest and dividend income, $1.2 billion from underwriting profit with normalized catastrophe losses, and $750 million from associates and non-insurance companies. This works out to over $125 per share after interest expenses, overhead and taxes. Of course, fluctuations in stock and bond prices will be on top of that, and these fluctuations only really matter over the long term.’

2. Hard Market and Underwriting Discipline

Peter Clarke

“Sure, thanks Tom. I guess to address the Odyssey question first, in the fourth quarter Odyssey non-renewed a large residential property quota share, around $340 million of unearned premium they returned to the client, and that reduced their premium in the fourth quarter. But for us, it just shows the discipline Odyssey has and the focus on underwriting profit, and for us, that’s a great thing. They wrote that quota share for about two years. In their mind, the margins weren’t there going forward and they took the action necessary, so that was very good.

On the Brit side, we mentioned in prior quarters that they were reducing their catastrophe exposure, re-balancing it, and you continue to see that coming through the top line in the premium. A lot of the exposure they’re dropping is in the binder business, which takes a little longer to run off, and that’s why you’ve seen it come through a number of quarters.

On the pricing side, on the reinsurance side, we’re still seeing for most of our companies double-digit pricing, mainly on the property side, and then in insurance, mid-single digit price increases with the exception, as you highlighted, D&O and cyber, which had a lot of price increases over the last number of years, has been slowing down and actually reducing, so we haven’t been growing in those lines as much.”

3. Reserve Releases

Peter Clarke

“I think our companies are still being very prudent on the hard market years - 2020, 2021, 2022, holding back from a lot of the favorable development that they’re seeing in those lines and just waiting that through to see how it ultimately plays out. We’re very focused on the effects of inflation and claims inflation in particular, so--but generally speaking, we think our reserves are in a very good position and we’re hoping going forward will benefit us.’

4.Associate income in particular Atlas/Poseidon

Prem Watsa

“By the way, our associate income, Atlas has provided the disclosure because of the new build program before they were taken private. They gave you a forecast - $300 million going to $600 million by 2025, and as of today, we still think that forecast is appropriate. When you put all of that together, we look at that operating income of $4 billion as a pretty conservative number.”

10,000m viewWe are close to completing the share price regression to the mean phase. I think the baseline from here is at least 12% CAGR. We can argue what the upside can be but that will take care of itself.

-

4 hours ago, Parsad said:

Fortunately, Peter Cundill, Southeastern Management and Markel invested $300M right during the worst time of the crisis. With that money, plus by delisting from the NYSE where the FTD's were occurring, they were able to slowly right the ship, reduce losses, reduce the huge reinsurance recoverable balance from runoffs and improve the company's position. Then Brian Bradstreet killed it with the CDS during the GFC, and Fairfax was now in a totally different position financially. That was the end of any shorting!

Good account. NYSE delisting was 2009 around the same time that they stole ORH from some of us

-

1 minute ago, valuesource said:

Done. Sorry, everyone seemed to be chomping at the bit to see the numbers and sometimes it takes 15 mins for Fairfax to put it up.

Many thanks

. Great results and the increase in duration is just brilliant. When it comes to Bonds these guys really are Masters of the Universe. It is a treat to watch the balance sheet get stronger quarter by quarter.

-

@valuesource any chance you can delete your post. There are links to the release no need to cut and paste the whole thing and it makes the flow of this thread very distracting. Thanks in advance

-

10 minutes ago, Luca said:

Interesting, what do you see here? I found it quite expensive at first glance, high capex. What's your thesis?

A sucker for their music business.

-

6758.T SONY

-

39 minutes ago, SafetyinNumbers said:

I read that as IRDAI approval has been received and the two people were referring to SEBI approval.The Rupee has weakened since 2022 when they filed the initial IPO. At the time the suspected IPO valuation was $4.5-5b. On the same basis, the low end would be down to $4b. It’s grown a lot since then but perhaps there has been some multiple contraction. It looks like the plan is to sell 12.5% of the company with $150m being fresh issue and the rest from promoters. I don’t know if that includes Fairfax selling some.

If anyone has any colour, please share.

I believe MINT broke this news. It is unconfirmed IRDAI approval as far as I can tell. Sounds promising, hopefully Fairfax confirms tonight or on the CC as I couldn’t find anything on the IRDAI website….yet

-

18 minutes ago, Parsad said:

https://finance.yahoo.com/news/maersk-had-more-cash-knew-120000731.html

Not the way to spend a $41B windfall! Hopefully, Poseidon/Atlas has been more prudent with their income on their long-term contracts. Cheers!

That pretty much encapsulates the Atlas thesis - long term meat and potatoes vs short term sugar hit. A good reminder of how patient capital (strong hands) could make a difference to this industry

Perplexity AI

in General Discussion

Posted

OT but Claude 3 just dropped and so was playing with it today. I actually thought this wasn’t too bad in terms of output:

Sure, I'll provide a basic attempt at all 5 valuation methods for Fairfax Financial. Please note that these are simplified examples and should not be considered a comprehensive valuation or investment advice.

1. Sum-of-the-Parts (SOTP) Valuation:

- Insurance and reinsurance subsidiaries: $20 billion (based on book value and peer comparisons)

- Investment portfolio: $30 billion (based on market value)

- Other assets and liabilities: -$5 billion

- Total SOTP value: $45 billion

2. Comparative Valuation:

- Fairfax's P/B ratio: 1.2 (current stock price / book value per share)

- Peer average P/B ratio: 1.5

- Implied valuation based on peer average: $52.5 billion (1.5 * book value)

3. Discounted Cash Flow (DCF) Analysis:

- Estimated 5-year cash flows: $5 billion (based on historical growth and profitability)

- Terminal value after 5 years: $60 billion (based on a perpetual growth rate of 2%)

- Discount rate: 8% (based on the company's cost of capital)

- Present value of cash flows and terminal value: $48 billion

4. Dividend Discount Model (DDM):

- Current annual dividend per share: $10

- Expected dividend growth rate: 5% (based on historical growth and payout ratio)

- Cost of equity: 8% (based on the risk-free rate, market risk premium, and company-specific risk)

- Implied value per share: $333 ($10 / (0.08 - 0.05))

- Total implied valuation: $50 billion (based on the current number of shares outstanding)

5. Adjustments for Unique Factors:

- Add a 10% premium for strong management and investment track record

- Subtract a 5% discount for exposure to catastrophe losses and market volatility

- Net adjustment: +5%

Based on these simplified examples, the valuation range for Fairfax Financial could be:

- Low: $45 billion (SOTP valuation)

- High: $55.1 billion (Comparative valuation with peer average + 5% net adjustment)

- Average: $50 billion

Again, this is a basic attempt and should not be considered a comprehensive valuation. A thorough valuation would require more detailed analysis and assumptions.