Saluki

-

Posts

1,876 -

Joined

-

Last visited

-

Days Won

3

Content Type

Profiles

Forums

Events

Everything posted by Saluki

-

https://techcrunch.com/2023/08/24/better-coms-stock-tanks-after-spac-combination-brings-it-to-the-public-markets/ Since this is the CEO who fired 900 people on a Zoom call, it couldn't have happened to a nicer guy.

-

Almost finished with the book and giving it a bump. There are just enough examples of investments and the outcome throughout the book to make it interesting. A good balance between just theory and just war stories. The Year by year summary of his investments in the back half of the book are also very good because you know what will happen with the world and he doesn't. I didn't get any hidden arcane techniques of what to do in a high interest environment, but it seems his approach was mostly classic Ben Graham (maybe that's what works best in a high interest environment?). He writes in a very folksy, readable style. I was surprised to find out that although he is not mentioned in the Super Investors of Graham and Doddsville list, he could be considered one of them. Although he didn't study under Ben Graham, he took an investing class as a student in Ohio and his professor was a student in Ben Graham's class at Columbia. A great book on investing that is not often mentioned, I would recommend it.

-

I'm not a hunter or a gun guy, but I looked into it quite a bit before investing. My understanding is that when people go to the shooting range to practice, they generally buy what is cheapest. If the ammo is low quality and occasionally misfires it's not a big deal, it's only range practice. When they buy the "self defense" rounds (i.e. hollow point), or when it's purchased by police, or the hunting rounds, they pay up. And for those, they tend to have brands they prefer. The ammo is fairly easy to make (which is why several low-end, or specialty brands exist). You need the gunpowder, the brass casing and the primer. The first two are easy to get and with some machinery you can set up a factory and start making bullets. The primer is difficult to make, and currently only four companies in the US make it (3 are owned by Vista Outdoor and one is owned by Olin). Recently, due to a primer shortage and unhappiness about the price spikes, a low-end brand (Expansion) tried to open their own primer facility. It failed miserably. So their is a kind of toll bridge that independent (US) ammo makers have to pay to get the primers. A foreign company, Fiocchi, which makes primers in Europe, is building a US primer facility for lead free primer (more expensive), but I don't think that will alleviate the toll bridge problem for the little guys.

-

Yes, even though guns can last 100 years, people like to buy them and just keep buying more. That's what took me a long time to come around to for gun stocks. If someone already has a gun, why do they need another one? They don't NEED it, but they think they do. "This is my home defense gun, this is my everyday carry, this is my small gun that I use for jogging, this is the backup gun, this one is my bugout gun, this is my hunting rifle for small game, this one is for big game, this is for target shooting etc." But I'm very interested in the ammo as a kind of model where someone is selling the razors and you sell the razor blades. Maybe someone will prefer the Beretta over the Smith and Wesson, but no matter which he chooses, he still needs to buy ammo for it, and he needs to keep buying it. And with Olin and Vista owning all 4 domestic primer manufacturers, even if the customer buys a cheap brand for use at the range, the no-name brand is probably still paying Olin and Vista. I'm not sure to what extent they are able to use foreign primers (the small ammo makers are private and don't share details), but it's something that I'm looking into. And yes, with Coke people drink it over and over again. Since the ban on tobacco advertising, despite the decline in smoking, it seems like it is calcifying the existing moats. People keep smoking and if they don't see ads for other brands, there is no social pressure to switch. And ditto for R&D in tobacco. They bought into companies that make vaping products because tobacco is not very innovative. The last piece of "tech" introduced by a tobacco company was the flip top lid in a cigarette pack. So if the moat wasn't so powerful, the lack of R&D could have invited an innovative competitor to disrupt them. Eventually vaping happened, but for decades they just chugged along and made money without having to develop new products because no one was foolish enough to try start a new tobacco company. I heard performance psychologist Gio Valiante say that "beliefs blind your observation." Railroads were terrible for a hundred years, but then when they weren't most people didn't notice because they had a belief about them that prevented them from looking at it with fresh eyes. Ditto about the consolidation in the aircraft and chip industries. I have some energy, shipping, and other things that hopefully have a better near future than recent past, but maybe the reason I was able to get in cheap is because of people's beliefs about the industry. The other possibility is that they are still cheap because I'm wrong, which would not be a good alternative theory. John Neff's "measured participation" method seems to be a good way to split the difference.

-

Sold the few shares of VTS that I have in my IRA (still holding all my shares in my taxable account for at least a full year). Up 50% in 8 months. Nice work if you can get it It had a nice little pop today , people probably noticed that a director bought more shares http://openinsider.com/search?q=vts and it's not a big company, so it doesn't take much to move the price. The dividend is great and it may still have more upside, but my IRA is tax free, so why not take some chips off the table. A lot of their production is hedged so they weren't hurt too much when oil prices dropped, and probably won't knock the cover off the ball if oil prices go up.

-

I was thinking recently about Buffett (and some others like Tom Russo) who have a penchant for brands. Sees Candy doesn't take much capex (it doesn't grow) and just kicks off cash every year. Ditto for KO, which owns the Coke brand, the costs are borne by the bottlers. Both have great moats. Car companies and fashion brands are recognizable, but they aren't really moaty. Each car company must design new cars and spend capex to improve cars every year. And a fashion brand that stops advertising quickly loses it's appeal. The ability to raise prices in an inflationary environment is evidence of a moat. But what about the ability to operate for years without spending a lot of capex, isn't that evidence of a moat? What does KO have to do to stay in business besides cashing their checks every year? I was thinking about this recently when looking at an ammo company. Gun companies, like Smith and Wesson, have to come up with new models every year, like car companies, but bullets are just bullets. So it would seem like gun companies are like car companies. Wouldn't a respected ammunition brand be a moaty business because it doesn't require capex and can command more $$$ than no name range ammunition? I looked at SWBI and RGR to see how much they spend per year in R&D capex. RGR spends about $20mm total capex and R&D is about $8mm. SWBI capex is bloated now b/c of the new factory costs, but the R&D capex is also about $7-8mm per year. I realized that it's not a huge amount for two of the biggest brands. Smaller brands, who (are private and we don't have the numbers) have to spread that cost over fewer sales, so the % cost is likely a lot higher. So is this evidence for the strength of their brand moat? I.e. that they can spend so little on R&D and still run circles around the competition for the mid/high end sales. Somethings are not brands, but obviously have moats that don't require a lot of capex (patented drugs, FCC licenses, lowest cost commodity producers etc.) I wonder if there are other ones out there that I'm not seeing. Just thinking out loud here.

-

I'm embarrassed to say that in my young and foolish 20s I dabbled a bit in this and couldn't get it to work. I studied various things including books on technical analysis methods like japanese candlesticks and other TA stuff. I subscribed to Investor's Business Daily and studied the CANSLIM method. One problem with technical analysis is that it's subjective. It looks like a head and shoulders pattern, but it doesn't work. So afterwards, some wizard will point out why it LOOKS like a head and shoulders, but actually it isn't. This is "no true Scottsman" fallacy. If there was something objective about it you could program some computer to do it for you. Another problem is that if you are looking for a pattern, whether you are using a daily, weekly, or monthly price chart will give you different answers. So which one are you supposed to use? what if they give different answers? The biggest problem is that people who subscribe to this are usually not lone alchemists sitting in front of their screens trying to create their own magic. They either share with other members of the true religion or pay for trading signals where a master tells the Jedi trainee what to buy and sell. And if you have a lot of people buying / selling at the same time, it looks like it's working, but it's just a bunch of pikers getting bad fills and slippage and thinking the magic beads work. The arguably good counterpoint is that IF you have already done the fundamental work and your technical analysis makes you more confident in your work, that might be a benefit. "It looks cheap, but I was not sure whether to buy today. However, the magic squiggles give me confidence." In Thai kickboxing, the fighters wear magic headbands and armbands and do a ritual dance before a bout. I can assure you it does nothing to protect you (especially since the other guy has the same thing), but if it gives you the courage to see the ring and a scary guy waiting to kick you in the face, and not turn around and head back to the locker room, then it's done it's job.

-

One of my small positions is a company called Anterix, which has FCC approval to use part of their bandwidth for private 4G LTE for utilities to do Internet of things. One of the use cases is that it can detect when a line breaks then remotely turn of the power to the downed line before it even reaches the ground. Maybe this will speed up adoption of the technology?

-

This company is down for $40 to $12 yesterday, and is up about 15% today on this news: https://finance.yahoo.com/news/hawaiian-electric-takes-expert-help-112122259.html Hawaiian Electric said in the filing that unlike in California, there was no precedent in Hawaii of applying an "inverse condemnation" to a private party like an investor-owned utility. An "inverse condemnation" exposes California utilities to liabilities from wildfires regardless of their negligence, as long as their equipment is involved. I don't think this means what they think it means. They didn't say "Hawaii courts don't recognize [i.e. have rejected] the inverse condemnation legal doctrine." It said that there is no precedent for it in Hawaii. If the plaintiff's win, there will be a precedent. Maybe the state will provide aid to those affected in exchange for not suing the utility, but this is a stretch. And even IF the court's say that the utility is not liable regardless of negligence, as long as it was caused by your equipment, they still might have been negligent. After they heard about the California wildfires, they had years to harden their infrastructure to prevent the same thing from happening. I've never worked with anyone from Hawaiian Electric, but I did have a client who is an electric utility on one of the other islands. And lets just say that I wasn't bowled over by their ability to dot every "I" and cross every "T".

-

picked up a few more shares of NTDOY

-

Picked up some NTDOY

-

The lines are much worse at the US/Mexican border crossing. If by "freely", you mean going across some section of unguarded border, you a free to try to swim Lake Michigan or drive from Calgary towards the border and attempt a mountain crossing on foot. I should warn you, the amount of people who die trying to cross the desert into the US to avoid the manned borders is not small. Maybe swimming Lake Michigan would have a higher survival rate, who knows?

-

Revson, the founder of Revlon used to say "we don't sell lipstick, we sell dreams" and "our stores don't sell perfume. Our factories make perfume, our stores sell hope." These crazy SPACs and IPOs are just selling people what they buy when they buy lottery tickets. A way to snap your fingers and get rich.

-

I haven't seen this posted about even though it was a couple of months ago: Concerned Shareholder Urges BlackBerry Board to Guard Against Unfair Buyout Bids and Oppose Watsa as Director as Board Considers Strategic Alternatives https://finance.yahoo.com/news/concerned-shareholder-urges-blackberry-board-140300075.html As a Fairfax shareholder, I hope it works out because that money has been parked in BB for a long time in something that was fairly speculative. I don't blame the guy for thinking he's going to get low balled in a take under. It literally happened to a lot us with ATCO last year.

-

Added a little NTDOY and FRFHF

-

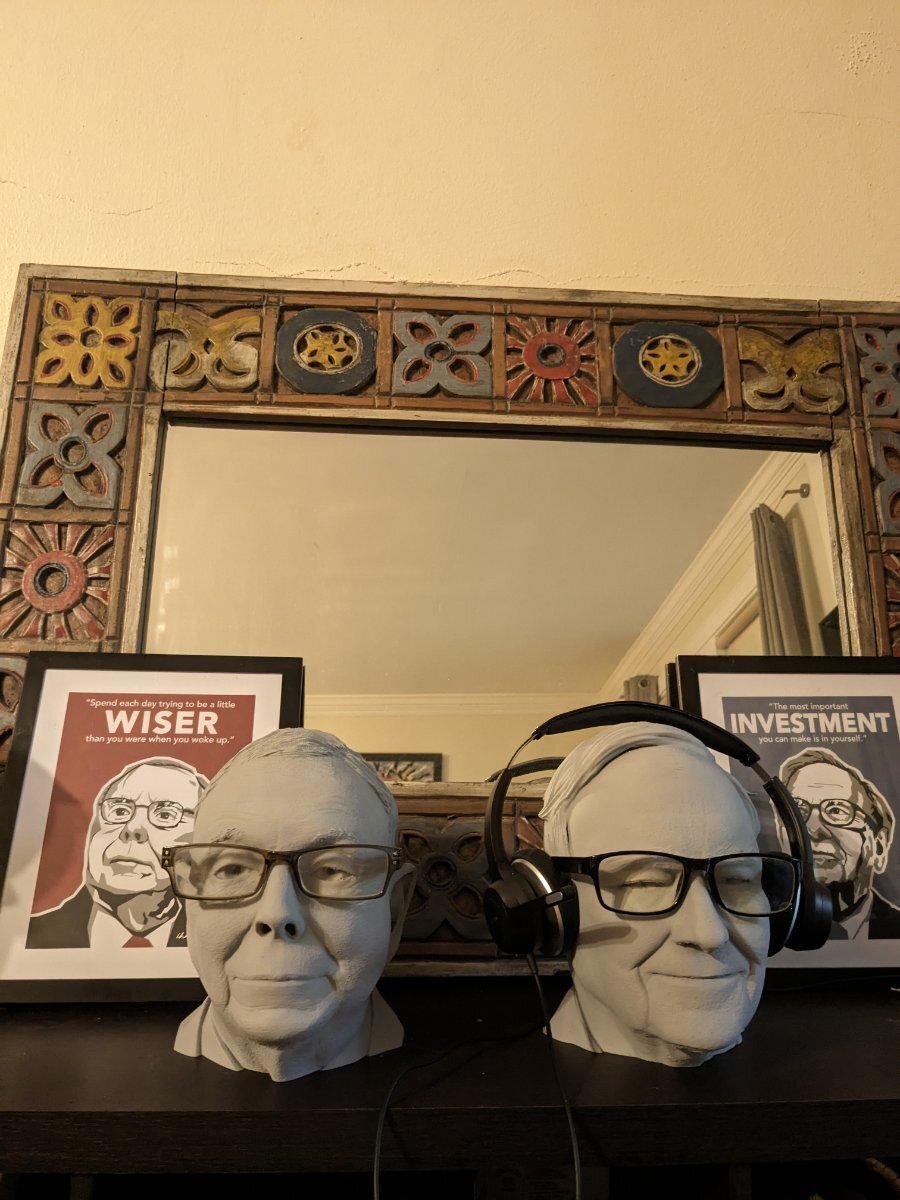

It's no secret that for many investors, including myself, their Achilles heel is their stomach, not their head. So anything I can do to help with that like having trading rules (don't sell this position for 3 years; don't check what the market is doing during trading hours unless you have cash to trade etc) is helpful. When I was looking for a headphone stand so I don't leave my equipment on the couch like a hobo, I almost bought a Mexican day of the dead colorful skull to hold my headphones, but the skull doesn't have a nose so it won't work to hold my glasses too. But when I saw these I knew that the universe had sent me a sign. The only drawbacks are that I should have ordered white, but gray was on sale and I'm a value guy. And I should absolutely have warned my better half that these were coming. Because when I heard "Ahhh , what the fcuk!! " from the living room, I realized that seeing two of these through a layer of bubble wrap looked like someone mailed me two severed human heads. Live and learn! Whether it not these will help my performance remains to be seen.

-

Picked up some shares of NTDOY.

-

Beginning of the End of Car Ownership as We Know It

Saluki replied to Parsad's topic in General Discussion

I haven't looked at the numbers in a while, but I would bet that based on miles driven a self-driving car is safer than most passenger driven cars. For highway driving, or roads without a lot of cars (rural, but not dirt) it's a much easier lift than trying to get it to work in San Franscisco (pedestrians, hills, obstacles, buses, more cars). It's interesting how different companies approached the problem. Waymo started in Phoenix (sunny all the time, few pedestrians, flat terrain, long distances), and another intentionally chose Pittsburgh because the amount of iron bridges made it harder to communicate with the vehicle. And snow, potholes and people added to the difficulty. The theory was that if we can get it to work here, it will work anywhere. Self-driving cars could reduce the cost of ownership. If your car is in the driveway, why not let it pick up fares and pay for itself? I don't see why paying for a driverless car, which surely would cost less than a car with a driver, for the occasional trip wouldn't work for rural people. Especially if the car comes to your door. Most construction companies don't have their own cranes or other specialty equipment because it's cheaper to rent it you don't use it a lot. It's not going to happen overnight because no one is working on retrofitting existing cars to be driverless. For a time riderless cars will share the roads with drunk drivers, distracted teens and Maryland drivers, just like cars shared the road with horses for a while. Eventually the lower cost of maintaining a car vs a horse made it hard to justify the joy of riding in the saddle. I'm sure your grandkids will chuckle one day when you tell them about how you had to learn to work a clutch. -

@CGJB Actually, I think you might be right. I found this https://acquirersmultiple.com/2017/06/walter-schloss-cagr/ which mentions some of his railroad bonds. Maybe he didn't want any more investors in his fund, so went by "Herbert"?

-

That was my first thought too. But it appears Schloss took the Graham course through the NYSE, and he was know for holding dozens of cheap stocks, not distressed bonds that would take years to pay off. And Schloss started his own firm in the 1950s, so why wouldn't he use his real name if he was still trading for outside investors?

-

I mentioned in another post about someone mentioned in Supermoney. Does any know who this person's last name? Warren introduced me to another Graham disciple. “He has no connections or access to useful information,” Warren wrote. “Practically no one in Wall Street knows him and he is not fed any ideas. He looks up the numbers in the manuals and sends for the annual reports,and that’s about it. He is a very family-oriented fellow: he probably spends more time thinking about children than about stocks.” There followed a list of stocks, about half of which I had scarcely heard of. The Rutland Railroad? The New York Trap Rock Company? The Union Street Railway of New Bedford? Jeddo Highland Coal? Clearly the fellow had never been to lunch at Scarsdale Fats, and was probably not around after the close at Oscar’s. The record was not spectacular; it plodded away, beating the Dow Jones average by a few percentage points, not as wide a margin as the Buffett Partners, but up 17 percent compounded over fifteen years. I made a lunch date with Herbert. We stopped at the checkroom with his raincoat and briefcase. He waited until the briefcase was stashed away. You couldn’t, he said, be too careful. “I didn’t get to go to college,” Herbert said. “I went to work in the Depression because my folks didn’t have any money, and I worked as a runner on Wall Street and then in the cage, tallying stocks.” Herbert took a Graham course at night at the Institute of Finance. “Ben really loved to teach,” he said. “He could have made a lot more money if he hadn’t been so interested in teaching.” Herbert operated just as Warren said he had. He never looked at rising stocks. He looked at the list of new lows in the paper every day. “Look at the steels,” he said. “No one wants them. Will they go bankrupt? How can an industrial country not have a steel industry? Look at American Can under thirty. Can they keep that dividend?” “I’m not very bright,” Herbert said. “I can’t compete with all the bright people, and especially the ones who have college educations, who have been to business school, who have lots of corporate contacts. I don’t know anybody. I have to buy what I’m comfortable with. These fellows that buy, even Procter and Gamble and General Electric, why, those stocks go up and down all the time. I just wouldn’t be able to sleep at night if I owned stocks like that.” What was Herbert buying? “Well, there’s one issue of Penn Central bonds,” Herbert said. That was a bit breathtaking. The Penn Central is very busted. “The Pennsylvania Railroad is bankrupt,” I said. “The value of the stock is negligible. The value of the bonds is questionable. It will take twenty years to straighten out. What you should buy is Shearman and Sterling, the lawyers, who will get all the money for the next twenty years.” “I know,” Herbert said. “But there is one issue of Penn Central bonds that is collateralized by the Pittsburgh and Lake Erie Railroad. I wrote Irving Trust and asked them, did they have the collateral behind the bonds, and they said yes. They don’t pay interest on the bonds, but when they settle the case, I think they will, and meanwhile the interest is in a special account at Girard Trust, twelve, thirteen, fourteen percent. It may take a long time, but I can sleep at night. I’m not in a hurry. Things always take longer than you want them to.” Had he really owned the Union Street Railway of New Bedford? “Oh, yes. They had a lot of cash. It took quite a while to liquidate, but it worked out very, very well.” A couple of things about this passage are very interesting. In the Snowball, if I recall, he mentioned an investor that he would trust to invest on his behalf (the investor had died years before). In this passage, he directs Adam Smith to someone who is only managing his own money and doesn't want to give a last name. Does he not like competitors for the spotlight? Or does he not like anointing people, besides Munger, who works with him? Herbert had a really long time horizon, but he wasn't betting on things like vacant land. He was sticking to railroad bonds backed by good collateral. Ted Weschler also made a killing on distressed assets (W.R. Grace) which took over a decade to sort out. Even back in the 1970s, there didn't seem to be a lot of patience for ideas that would take a long time to play out, no matter how big the payoff. In the 1940s, the average holding period for a stock was 7 years. In 2020 it was 5.5 months. It seems like the short term end of the investing curve is getting more crowded, what happens to the long-term end of the curve? I'm sure the decline of full service brokers and the outrageous fees helped to speed up trading by reducing the transaction costs, but it's still interesting to look at your portfolio and think about which ones will have a big payoff, but not for a very long time. I won't mention my favorite real estate stock, because I want it to go down, not up, but if you take a look at something like Howard Hughes, maybe the payoff down the road is so big that the mismanagement is not going to matter? Or maybe, like Trinity Place Holdings or Seritage, someone may eventually get rich on it, but it probably won't be you? Just a thought. But if anyone knows Herbert's last name and how he turned out, I'd be very curious to hear.

-

Lead in underground cables and other nothing burgers

Saluki replied to Saluki's topic in General Discussion

@ValueArb yes I agree, you shouldn't be reckless, you should be informed. Ackman made a big pile in Wachovia during the great financial crisis when it was announced that Citi was buying the banking subsidiaries. He realized that the holding corp parent had a lot of valuable stuff and it was worth 10 or 11, and it was trading for $1. I was recently re-reading Supermoney and the author spoke to a friend of Buffett named Herbert (no last name given) who was a Graham disciple who had never been to college, but took the course at the NYIF when it was offered. He had invested a bunch of money in the bonds of the bankrupt Penn Central Railroad. He explained that MOST of the bonds were garbage, but that the bonds he bought were guaranteed by another railroad, which had been depositing funds into an account to be paid when the court ordered it. Because the bankruptcy case was so complicated, he didn't think he would get paid for several years, but knew that in the meantime that account was racking up interest at 12-14% per year. The people who bought energy companies when oil went negative (not me) did the work, had a variant perception and nerves of steel, and they deserve whatever riches came their way. I'm just trying to keep learning and getting better every day. -

I tend to agree with Peter Lynch that the most important organ for an investor is the stomach, not the brain. Here's an interesting interview I came across from a Psychologist about Behavioral Finance. Most people know the things to look out for, but don't do them. Because it's not a lack of knowledge. If it were, there would be no smokers.

-

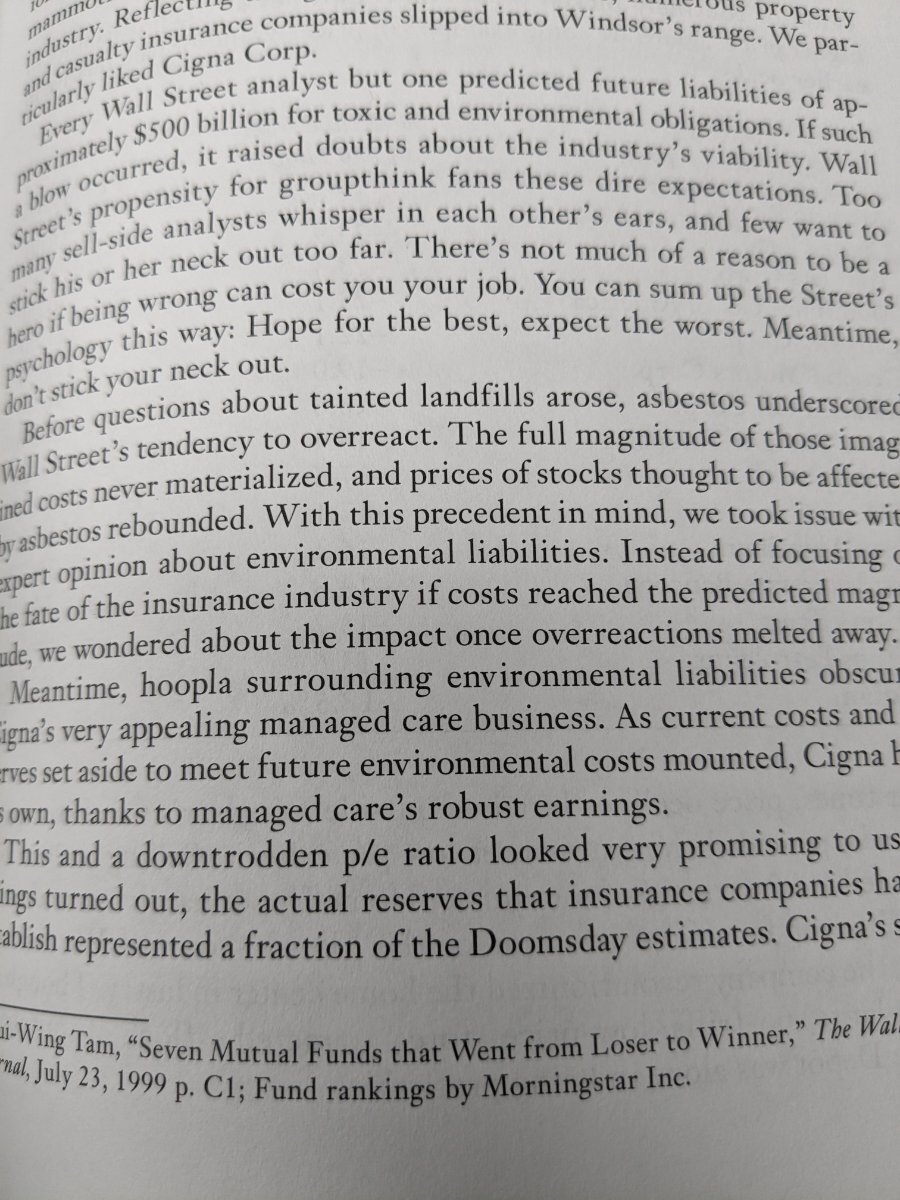

I'm reading a classic, John Neff on investing. If we return to 1970s stagflation or 1980s double digit interest rates, it would be interesting to follow the play book of someone who crushed it then. This passage caught my eye and reminded me of the tanking stock prices of several cable companies. Several billion dollars in market cap wiped out overnight based on a wall street journal article that had a lot of scary words, but not a lot of facts. If you're wondering how it worked out, the SP500 went up 29% while his Cigna pick went up 54% in the same period. Reminds me of an investor who said "if you smell smoke, run towards it, that's where the money is." Just as there is hype in things like crypto and AI there is fear in things like China (they can just steal your BABA VIE shares) or North Korea (CPNG is in Seoul, which is within artillery range of North Korea), or ESG (oil companies are shrinking ice cubes, EVs will replace cars and no one will need auto mechanics so dealers will go bust). I'm working on figuring out better guard rails for myself as an investor. A behavioral psychologist I was watching on YouTube said "if you're excited about a stock, don't buy it" and "and if you're worried about it, don't sell it". It's not bad advice. Decisions should be made rationally.

-

I remember that right before it went bankrupt there was a day where it went something like 120%, then it opened the next morning down about 30%. Stay away from the mosh pit. It's not for people who have a mortgage and a day job.