Saluki

-

Posts

1,514 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Posts posted by Saluki

-

-

2 hours ago, ICUMD said:

IDBI

Looks like Fairfax India is in a strong running position for IDBI bank, results anticipated for June.

Adding a bank of this size to the Fairfax India portfolio would be an incredible deal. Well positioning the company in an important growth niche in coming years.

Thoughts?

How often has the government waived the restriction on owning more than one bank? It looks like they made an exception in 2020 (when it looked like the world was going to end), but do you know how likely it would be now? Given the turmoil in the US and Germany from some big bank failures, maybe they would be open to a well-run firm with a good balance sheet taking them over, which may prevent a problem before it happens. But other than the incidence cited in the article, is this common or only done rarely?

I'm still bullish on FFXDF either way. Other than the illiquidity (my broker makes me use two factor authentication and limit orders only for Fairfax India), I don't see how others don't see that this is undervalued. It's trading for ~2/3 book and you are buying it below the tender offer price last year, even though things are going better with the world reopening, which should make their biggest asset, BIAL, more valuable.

-

-

I'd be curious to know if the teen deaths in Europe are similar to the US, since there is a huge difference in gun ownership in places like UK vs the US. I also think that the incidents of violence are worse than the numbers portray. There is a very controversial former Army Lt Colonel, Dave Grossman, who researched and wrote several books on things like school shootings. People get upset when they find out the police department spent money to hire a guy who wrote a book called "On Killing" to work with their officers. I haven't read the book but his YouTube videos make a lot of counter-intuitive points. He's got some shocking statistics to back up his theories. If we had vietnam era medical treatment for gunshot wounds, the murder rate from guns would be 4x higher than it is today. So just as we adjust housing prices for inflation, we should take trauma medicine into account when saying things like NYC violent crime is less than it was in the 1970s. It's higher. In the 70s, a place like Peoria Illinois probably never had a gunshot victim in the emergency room. Now they probably have see shooting victims weekly, but have better skill at treating them and having them live than NY doctors in the 70s.

Curiously, he puts much of the blame on violent TV and video games. During WWI and WWII less than 1/4 of troops on the firing line would fire their weapons. The army switched the bootcamp training from firing at round bullseye's to human silhouettes and got it to 55% by the Korean War. They got it up to 95% in Vietnam with silhouettes that pop-up, you shoot them, and they go down: Skinner's operant conditioning. They also drilled into you things to desensitize you to violence, like the scene in Full Metal Jacket where they sleep with their rifles, or the chants during marches "what makes the grass grow? blood blood blood. What do marines do? Kill kill kill." The first person shooter games, specifically are desensitizing them to killing and the violent TV makes them less affected by human suffering, which is what the military did to get the kill rates up in War, but it's being done to teenagers who have little impulse control and access to guns. Scary stuff.

-

1 hour ago, nwoodman said:

No good reason, other than time of holdings. The retirement fund initially had three holdings BRK FRFHF L. Two out of the three went to zero, in terms of holdings. Fairfax made it back in the last couple of years. Added a number of times in the personal portfolio to BRK but it was setup later than the retirement fund due to running money for others and private business interests etc.

I've had BRK since 2010, but I don't mind occasionally selling some in my retirement account and repurchasing the same amount in my taxable account, so that I can still have the same percentage ownership of BRK, but put a (hopefully) faster grower in the retirement account to compound tax free. I also sold almost all the Fairfax in my retirement account and purchased Fairfax India there for the same reason.

I think people don't think enough about after-tax money when they buy or sell. If I have something that pays a big dividend like VTS (10%), if it's in my ROTH IRA account, the tax on the dividend is zero. If it's in my taxable account, it's the qualified dividend rate, which is lower than my ordinary income rate but more than zero, but if it's in my Traditional IRA, it's tax only tax deferred. When I take it out eventually, it will be taxed at the highest rate as ordinary income. So that makes a difference when deciding where to hold it, as well as where I have idle cash.

-

I've read several good books about the great financial crisis. Too Big to Fail is becoming the default official story, but it's interesting to see someone else's take on it. Tim Geitner's book was good, but there was something about his version that didn't sit right with me, and I couldn't put my finger on it. The Bullies of Wall Street is a short, very readable book by Sheila Bair.

I won't go so far as to say that she comes out swinging, as some in the press have suggested, but she definitely wanted to get her side out given the unflattering portrayal in the most popular accounts of the matter, mentioned above. Yes, Ken Lewis is referred to as a "country bumpkin", but if you read Too Big to Fail, you probably thought that in your head, even if you never said it aloud.

In other tellings, she is the one who put the turd in the punch bowl by not going along with things that Geitner and Paulson had worked out because she didn't want to put the FDIC's money on the line. In her telling, she didn't have the authority to use the FDIC's funds for some of those schemes, and would be breaking the law if she did it. Since Congress quickly changed the Fed's authority to allow them to buy up assets that were not permitted under their original mandate, she wanted Congress to amend the FDIC laws to allow her to do what they were asking, because without that cover she would be breaking the law (committing a crime?).

Geitner and Pandit come off looking particularly bad in her side of the story. Geitner had some kind of fan boy crush on Pandit and was favoring Citi's bid for a bank, which would require a lot of government money because Citi wasn't in great shape to begin with. She viewed Pandit as a failed hedge fund manager who fell up and up until he was given the big chair at Citi.

Speed was of the essence in these deals (as we saw recently with SVB, and First Republic), so when Citi stalled and tried to get more concessions, she accepted an offer from Wells for more money (better for the target Banks' shareholders/creditors) with no government assistance, she jumped on it. Geitner was furious and felt like she had made him look bad in front of Pandit (so what?).

There are three sides to every story, his side , her side, and the truth. This is obviously not from an unbiased source. She doesn't like some of the players and takes joy in retelling about a meeting in the White House when Geitner got a dressing down from Obama for trying to undermine her on something. Still, it's worth seeing things from multiple angles and coming to your own conclusions. This wasn't a long book because it only involved her and FDIC's role in the saga, which are only a few chapters in Too Big to Fail. But it's definitely worth a read.

-

I hadn't heard of Orla before, and I hate junior miners, but it's a big position, and I remember a few years back Prem bought a rights offering for a $100mm potash company and that went from $1 -$4 in a year, so it's worth digging into the annual report to see if you can figure out what he sees in it. Even if you pass on it, and just participate indirectly through FFH, it's a good learning exercise.

Since ATCO is private now, I assume there will be some discussion of how it's valued going forward when the new ships are delivered and whether that nice fat dividend will still keep coming to FFH like it was to shareholders.

-

18 hours ago, LC said:

Saluki, did you grow up in the Bronx? Just curious, as I am no stranger to gun hill road.

On rent control - I agree. The model for a while now has been rent stabilization and 80/20 buildings.

Generally most people agree you need market rate units to carry the rest. True rent control is probably gone - but rent stabilization which gets escalated when a unit turns over, that is OK with me.

Not a lot of broke NYC landlords.

@LC I grew up in Brooklyn, but my dad was a contractor and he had an office for a while in the Bronx because he had a lot of work up there. When they remodeled Skyview on the Hudson in the 90s, we did a lot of the drywall and tile work in those buildings as a subcontractor. I left NYC after college to go to law school. I don't miss it. There are things I like about NY, but the things I dislike are much more irritating when you've been away for a while.

-

Yes, I agree, it make life easier for senior lawyers and miserable for new lawyers.

I played around with it and asked it to draft a sample forum selection clause, and a sample material adverse change clause. Because those two are so common, I think it did pretty good job. Without any false modesty, I know that I could've done a better one when I was a junior attorney, but it wouldn't have been twice as good. If a lawyer (or client) has a choice of free and good enough or slightly better for a lot of money, I think they will go with the off-the-rack option vs the bespoke suit. Maybe senior lawyers will use this for a first cut? Or the type of client who uses RocketLawyer or LegalZoom will use this and take it to a lawyer for editing? Or maybe, like computer programmers, junior lawyers will use it and will just be pumping out much more product for the same salary?

I asked a couple of specific legal questions about my current practice area and my prior one (both of which are not very common), and it gave an incorrect answer for both, but sounded very authoritative. Which is scary if a small landlord or mom and pop business owner will rely on it to prepare for a court case where they can't afford a lawyer.

Without the foresight of a crystal ball, all I can say is that I'm glad I'm not graduating now, since the practice seems to get worse every year. I saw that in the 1960s, even the white shoe firms on Wall Street had a billable requirement of 1500 billable hours. Nowadays that would be considered part time, even at a smaller firm.

So do you use the sample template the same way you would use a sample brief or prior contract and just follow the pattern to make sure that it includes everything it's supposed to, but edit everything so that it fits the specific facts? Since they charge for shepardizing cases, I would assume that Chat would have to have an agreement with Westlaw before that becomes an option.

-

On 11/30/2022 at 10:13 AM, Gregmal said:

I like VAL warrants. Its the classic post BK forgotten about turd with a muddied name from prior life cycles. Well positioned, ripping tits, and you have more than half a decade to watch it for pennies.

A friend of mine has a bunch of those. Not because of your thesis, but because he had a bunch of the common that got wiped out in the bankruptcy and those out-of-the-money warrants were all that was left after the restructuring. I looked at the common when he had them and after the bankruptcy reorg and decided to pass since those floaters are the last things to turn in an oil price boom and the first to collapse. I hadn't thought about the warrants, though. I'll take a look. Thanks for the tip.

-

I don't think so, for the same reason that AI can't tell jokes, it doesn't understand nuance and can't make analogies.

It has for years been getting better and better in some things like filtering through emails for discovery in litigation and flagging the ones that might be relevant, then having an actual attorney look at them. 20 years ago, when some of my friends graduated and still hadn't found a job, "document review" was like Uber/Lyft/TaskRabbit for lawyers. They would pay you a decent amount (no benefits) to cull through thousands of emails and documents in response to a discovery request, and you would be a room with 20 other underemployed recent grads, and after you made the first cut of the docs, the big lawyer would review them. That first step is gone now. The software is not only cheaper, but more accurate than most lawyers, and it doesn't get tired, it doesn't take days off, and it doesn't sue for things like a real employee.

If you ask an AI program to explain Brown vs Board of Ed, it will find enough articles written on it to explain it. But giving it a set of facts and asking if it's legal or not, is probably way beyond it's abilities for now.

-

On 5/10/2023 at 9:38 AM, Spooky said:

Charlie keeps mentioning he would prefer if American oil companies stopped pumping oil entirely since hydrocarbons have other important uses and there is a limited supply. He mentioned this again at the AGM. I can't help but feel like this is part of the thesis that people are overlooking since it appears that there is still significant oil reserves under the Permian that are currently not easily accessible with current drilling technologies.

I used to own shares of a land based oil rig driller called Patterson UTI, and the former CEO/founder was a thousand years old and very sharp. Reminded me of Munger. He said that the problem with the oil industry (the E&P guys) is that they like to drill holes more than they like making money, and that if you give them a dollar, they will drill you a hole, you give them another dollar and they drill you another hole, and that you run out dollars before they every tell you that it's a bad idea to drill another hole.

-

Well, I like to give credit where credit is due, but I can't remember who told me this pithy analysis. He said if you want to destroy a city, the only thing more effective than rent control is carpet bombing.

In the poor areas of the city, where it's meant to help, it does the most harm. I grew up in NYC and the South Bronx had many blocks with buildings that looked like something from The Last of Us. When you aren't allowed to raise rents, you don't have money for repairs, and many landlords just borrowed as much as a bank was foolish enough to lend them, then collected the rent for as long as possible, and eventually just stopped paying the mortgage and the taxes and eventually just walked away from the property and let it be the bank or the city's problem. The problem is made worse by laws that make it incredibly expensive and time consuming to evict a "professional tenant" who knows how to work the system and probably has a free lawyer. In NYC if you own a property through an LLC or Corporation you have to hire an attorney to appear for you. How many mom and pop landlords can afford to do that for a year without rent coming in? Why don't they own it in their own name? Because they don't want someone to slip on a banana peel in front of the house and sue them into oblivion.

I think the risk is less in high end buildings. New construction isn't subject to rent control in NYC if I'm not mistaken, and even in the older buildings, if you are charging market rent and verifying income, it's unlikely that someone put his nose to the grindstone to graduate at the top of his class, get a job at a top law firm or bank and then use that lifetime of work as part of some grift to rent a place and not pay. But at a lower income level, 9 months or a year of free rent might look like a great risk reward situation. You stop paying rent, after a year when they finally evict you, you rent a new place under your wife's name, then a year later under your elderly mother's name, then your kids, and eventually yourself again when enough time passes.

-

Just watched this. Great find, thanks for sharing.

-

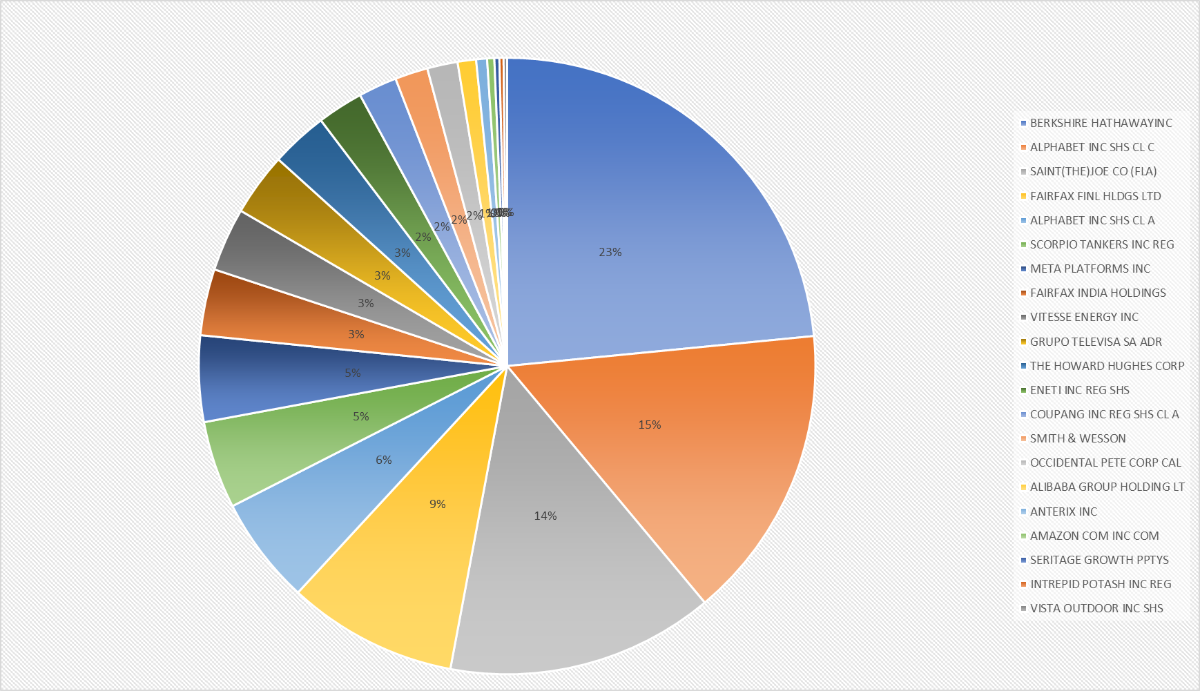

On 5/3/2023 at 1:21 PM, gfp said:

You look at that pie chart and worry about the concentrated positions and I look at that pie chart and wonder what the point is of having so many of those tiny positions at all? If you don't like which positions became the big ones, by all means trim them if you are uncomfortable. But having a lot of money in your very best ideas is not a bad position to be in.

After the Berkshire AGM (where Uncle Warren explained how AAPL is not a 35% position, b/c their investments include their operating businesses) I decided not to trim the big ones anymore, because as a percentage of my total assets, which include my work provided 401k and future pension, and my home in my city and condo in Florida, it's really not that big a position at all. And yes, some of the big ones that slowed down in the past (like Fairfax) and I didn't sell eventually came back strong and if I sold, knowing I still liked the future prospects, just to keep a certain allocation like 5% each for 20 companies, then the returns would be less lumpy, but they would be less overall too.

As to the small positions, I do see your point and I didn't have a good answer. But in reading the Joel Tillinghast book, who outperformed the market for two decades and had 800+ positions in his fund, he explained it better than I could. Something can look really cheap, or have huge potential for growth, but it's not a sure thing, so putting a huge part of your net worth is not optimal. But a smaller position is a way to start to participate and you can add to it as the picture becomes clearer or your faith in management improves.

Maybe researching the smaller positions keeps me busy and therefore I don't do something foolish like trim the big positions? Maybe the big positions aren't attractive except for brief periods every few years and I feel uncomfortable sitting on cash or buying my biggest conviction ideas at prices that are unattractive currently but will still do okay over time?

Thinking of those small positions as a percentage of my total net worth/assets makes the allocation even more questionable in some ways though. Viewed through that lens, they are so small that they are basically just going to Vegas and playing the nickel slots. Just thinking out loud, but I appreciate the feedback.

-

I trade in and out of the SRG cumulative preferreds, currently have a tiny position. They pay 7.5% at par ($25) and periodically dip below $22. It's not a bad place to park your money since the CEO is trying to sell the company and if the common holders get anything at all, the preferreds will be called at $25 and you get the dividend while you wait. It won't make you rich, but it's not scary either. No telling when the company will sell though, since the real estate environment has gotten tougher with the rise in interest rates.

I have the SEC filing for another preferred in my reading pile that pays a little more, but it's trading at close to par and the business has been having some problems, so I'll probably won't stick my neck out for a few more basis points.

-

17 minutes ago, gfp said:

what tool are you using to produce those pie charts?

it was a pain, but I did it with excel. I copy/pasted the positions from my brokerage account, which needed reformatting (ugh), then I added a column that figures out percentages. Then click on the "Insert" tab, and on the top of the tool bar there will be a bunch of options for bar or pie charts.

-

I think looking at this in pie format is helpful because it keeps me from stressing about the smaller positions, which won't really hurt me even if they go to zero.

The concentration on some of the bigger ones though, is concerning me lately. I'm not Bill Miller who can hold 90% of his personal portfolio in Amazon and just let it ride for 20 years. BRK is a great company that I've owned for more than a decade, and so is Google, but I've been thinking of trimming them if they get past 25% of my portfolio. 30% would definitely be too much for my tastes. Maybe trimming BRK and adding to FFH, or trimming GOOG and adding to something else techy?

-

Sold a bit of junk and bought some Seritage preferred (SRG-PA), STNG, VTS, OXY

-

Added some NETI and CPNG.

-

I'm almost finished with this book now and I'd highly recommend it for anyone to add to their collection. Just enough anecdotes and charts and post mortems on investments to get the point across, but no fluff whatsoever. No one is as pithy as Peter Lynch, but this guy has a very readable style. Whereas One Up on Wall Street got many people interested in investing that otherwise had no clue, this is a definitely not a beginner's book because it assumes you already know terms like enterprise value and EBITDA, so I think this forum is the target audience.

I had several bookshelves full of investment books and have made a deal with my better half that I only buy a new one if I get rid of five old ones. I usually put them in the little free library near my house. There are some that I can't imagine ever getting rid of because I re-read them occasionally (Greenblatt, Peter Lynch, Charlie Munger, Ben Graham's Security Analysis), I think this one will make the permanent collection.

-

I was an M&A lawyer in the beginning of my career, and the best advice I would give is don't skimp on the due diligence and make sure the lawyers/advisors that you use are experienced in the type of business that you are buying. My firm did a lot a cable transactions and once we had a white shoe manhattan firm on the other side, who did a lot of M&A stuff, but not in our industry, and they probably cost their client 2-3x as much because everything took them longer since they didn't know it and had to "get up to speed" on things while billing for the learning curve. I'm sure it would be prohibitively expensive if someone hired us to do a software or pharmaceutical deal, for the same reasons.

It's okay to have different people for different things. Our clients had a boutique tax law firm that represented a lot of cable companies, and they had a different firm for litigation. Just because you use a firm for, say, the real estate portion of the deal, doesn't mean that the tax or IP people in the firm are just as good.

-

I'll echo what others have said that having read both this and 100 baggers, both are worth a read and this is the better of the two books. Along this line of buying compounders and holding for a very long time, a couple of books with similar strategy that are good reads are The Davis Dynasty (the patriarch was a bureaucrat at the state insurance commission and later got rich investing in insurance companies and holding for decades), and the Phil Fisher books (I believe that he held Motorola for decades and it was a huge part of his portfolio).

-

Added a little JOE and CPNG. I think there are cheaper things in my portfolio, but none that I'm willing to increase position size right now.

-

46 minutes ago, John Hjorth said:

This has been on my mind for while. To me, personally, it has become gradually worse over time. I can't really pinpoint towards time, but to me : It's happening : *BS* and nonsense posted there about every day.

So called "writers" running out of steam, now providing i.e. "Berkshire bits" - of the week - about what Mr. Buffett might have said some 20 years ago at an AGM, or what do I know.

Lately, I've become really tired of all that stuff hitting me, making me choose to disconnect to several Substack accounts.

How about you? - What do you do? - And what are your thoughts about it?

-Thank you in advance for sharing your perceptions, opinions and insigths in this topic.

Have a nice weekend.

I don't go on Substack, I avoid Twitter like the plague, and I try to avoid articles that give their take on what Buffett said. Like everything in life, it's usually better to go to the primary source. I've got Buffett's chairman's letters in the hardbound book and it's a great learning tool. It seems all media is moving towards shorter, click baity content. Twitter is the worst for the written word, and Tik Tok for video. Maybe you should make a conscious effort to move in the other direction towards long-form content.

There are legendary investors who have written books (Peter Lynch, Ben Graham, Phil Fisher, Phil Caret, Joel Greenblatt, Einhorn, Tillinghast, Howard Marks) and I think those are great sources. I read a lot of biographies. Currently I'm reading one on Marvin Bower (responsible for taking McKinsey from two offices to an international powerhouse). In the past I've read books on a particular industry (shipping) and I have one in my queue about graphene now. I don't know if I'll ever use the knowledge, but it's easier to just keep accumulating knowledge and then having it ready if something comes up then to pass up an opportunity because by the time you get up to speed on something the opportunity passed.

-

1

1

-

What are you buying today?

in General Discussion

Posted

Added a little bit of FFXDF and NETI.