Saluki

-

Posts

1,514 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Posts posted by Saluki

-

-

Some interesting videos from the Capital Link conference (Russian Oil Price Caps, LNG, VLCCs, Product Tankers). Some of these videos have double digit or low triple digit views, which makes me think that the energy sector is still not on most people's minds and has more room to run.

-

12 hours ago, Spekulatius said:

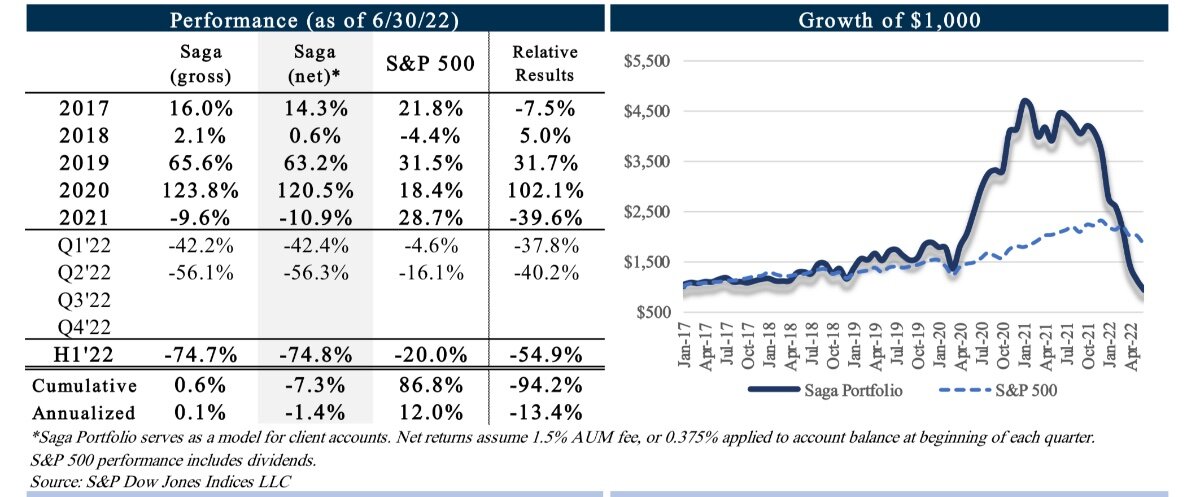

Saga partner is a concentrated growth fund that had phenomenal performance in 2020 and subsequently lost it all:

https://www.sagapartners.com/_files/ugd/3b0d6d_ce16f046c4524c08893864f3ce87152c.pdf

just one example where one bad year wiped out many years of market beating performance. They stopped making their letter public as well.

Wow, that was a painful read. Roku, Trupanion, Carvana, GoodRx. That portfolio looks like it was all offense and no defense. A lot newer managers have never lived through a bear market.

-

added a little Coupang.

Not any particular news, but I've been thinking about diversifying globally as well as across industries. Ideally with compounders instead of cyclicals.

Coupang (CPNG) (probably 1/2 the position size I want, but I'm already fully deployed)

Fairfax India (FFXDF): India (could add some more)

Televisa (TV): Mexico (full position)

Alibaba (BABA): China (full position)

I've been thinking about a good one for South America, but although Petrobras looks cheap, It's a cyclical. I really admire what Mercado Libre has done and how it's managed, but it's too rich for my blood. Tigo Millicom I've looked at but can't pull the trigger. Anyone have any suggestions for cheap latin american companies with compounder potential?

-

I think Peter Lynch was right when he said the most important organ in investing isn't the head, it's the stomach. If you had held the nifty fifty stocks in the 70s, you would be down 80% at some point, and if you kept holding it for another 30 years, they would've come back, but how realistic is it that someone would have the emotional ability to hold on that long. A lot of legendary investors do things that are mathematically sub optimal but work for them.

Peter Cundill would sell half of his position when a stock doubled so that he would feel like the pressure was off because he couldn't lose the original amount he invested. Peter Lynch would call that cutting the flowers and watering the weeds. As your number of positions increases, it becomes increasingly harder to beat the index, but Lynch had hundreds of positions.

The recently deceased Rakesh Jhunjhunwala, was worth a few billion when he died. A huge chunk of that was from one stock that he bought and never sold, but he did also buy and sell other positions rapidly and even founded an airline right before he died (which is the worst business in the world, besides the dairy business). Maybe the other active, hectic stuff kept him distracted so that he was able to not sell the golden goose position for decades?

I heard of another investor who only puts in buy/sell orders after hours so that he's not looking at blinking red and green numbers and letting his emotions take over. Buffett says that he reads the 10k and then decides to try to figure out what a company is worth without looking at the stock quote. He acknowledges that even he is prone to anchoring bias.

In this vein, maybe the best course is figuring out what your personality is and coming up with strategies to compensate for your blindspots or your emotions and then devise a strategy based on that. I started a second trading account at another broker when my main account got too far over the SIPC amount (I know, but I'm a worrier). I do much less trading on that account, because it's only on my phone, not on my desktop computer, so it's not in front of me all day. I have to seek it out to do something. I think when I'm fully deployed, maybe I should find a way to keep myself from looking at my main account. If I have no extra cash and I wasn't planning on selling something, why am I looking at it and thinking about moving things around?

Buy and hold works great because (at least among professional managers) the amount of trading activity is inversely corellated with performance. The only exception is quant funds that trade in nano seconds. But to be able to hold for decades, you have to find a way to not be tempted to sell.

-

Bought some VTS and OXY with the last of my proceeds from the ATCO squeezeout.

-

My Fairfax India limit order was filled

I have almost a full position now but no more cash without selling something else, but if it comes down more or I sell something, I may add more.

I have almost a full position now but no more cash without selling something else, but if it comes down more or I sell something, I may add more.

Air India last month announced that it is buying 470 new aircraft from Airbus and Boeing and wants to be a global aviation leader. One of the airports that they fly out of is Bangalore, which was recently enlarged and may be publicly traded soon. And FF India is still selling below the self-tender price.

-

Added a little TV, OXY and SWBI today. Put in a limit order for FF India, but it didn't get filled

-

Sold some GOOGL. It's still my second biggest position. I tapped into my HELOC and added another 10% when it dipped to the low high 80s/low90s a couple of months ago. No particular reason for the sale other than it was too big a position in my portfolio already and 10% or so in a couple of months in this environment is nice work if you can get it.

-

26 minutes ago, Gregmal said:

See Jay fell for the rhetoric and those within his sphere who were pushing it. Why couldn’t he use some common sense? The ultimate tell of a dishonest take on the inflation is the “it’s their mandate” and “so what keep zirp forever” responses. It’s not all or nothing, especially at such as high level. Saying 5% inside 6 months or whatever is insane isn’t saying they should have stayed at 0%. Or saying 3-4% is fine isn’t violating this “mandate” as well. We keep hearing about these comparisons to the 70s…well guess what? If we applied some common sense and say, capped these hikes to 250-300 bps on a TTM basis, you know….so we could actually be data dependent and see the lagging effects…we d still be at a 10% FF within a few years and back at peak Volker levels many years sooner than it took back then. It’s just that the chumps like Summers, who I am certain is also getting paid by hedge funds for “advisory” work, told him he needed to go bananas to be credible and defeat inflation…yup, it’s as dumb as it sounds and was all along.

Some guy who tracks private planes is reporting that 20 private planes have flown to Omaha recently from different regional banking centers and DC. It could be too that uncle Warren is working on some kind of deal with multiple banks to give his imprimatur to boost confidence in them in exchange for some preferred shares as he did with BAC and Goldman.

-

Sunday Markel Brunch in Omaha:

I'll post other things as I find them to keep track of them all in one place.

-

Sold the last of my ATCO shares (got the dividend, and less than 1 percent difference between todays price and the buyout price) and sprinkled it around to some of my favorites: TV, VTS, OXY, BRK, FFH, and FF India.

(I also added some BABA, but plan on selling the same amount of much higher cost basis shares in 30 days to try to offset some capital gains).

-

Right before the close I added some OXY (still below the Oracle of Omaha's price), and some FFH.

I was on the fence about adding more FFH, but if I was right to be upset about getting squeezed out of ATCO, then when they have 20+ new ships in a couple of years, purchased at 30% cheaper prices than their competitors, it should help Prem and me out

-

It seems that the order book for VLCCs and Product tankers is very low. The shipyards are booked up with orders for containerships (covid reopening and supply chain disruptions?) and LNG ships (ESG fad?). According to this, 2026 is the soonest you could get more.

https://www.freightwaves.com/news/crude-shipping-revs-up-supertanker-rates-top-100000-a-day

I try to keep on eye on the macro stuff because although replacement orders in tankers and product tankers is low, in the back of my mind I'm always concerned that a recession could hurt demand and bring pain to this industry even if the fleet doesn't grow. But with the wars and sanctions and shutdowns, trade routes are shifting and these assets seem to be a way to go long chaos in the world.

And when governments take aim at oil companies with windfall profits taxes, they don't seem to mention ships or refineries, so maybe there is less political risk involved.

I have a medium size position in STNG for the past few years, but I haven't really looked at VLCCs. Are there any names you like in that space?

-

12 minutes ago, lnofeisone said:

I have a core VTS position and been trading around it. The volatility is insane.

Yes, sometimes the bid/ask spread is a couple of cents and balanced b/w buyers and sellers, and on days like yesterday (on no company specific news) it was wide enough to drive a truck through with 5x more asks than bids.

Even OXY was trading yesterday for 5% less than the greatest living investor was buying it for last week. Fear is a helluva drug!

-

Bought some VTS and Fairfax India

VTS (both VTS and OXY dropped yesterday to attractive levels, but the drop was much bigger in VTS)

Fairfax India (it's still trading below the self-tender offer and it's still improving. I was tempted with FFH at these prices, but I have a lot of FFH already and this seems like a better bargain, FFIndia 70% of what they believe is NAV vs FFH 1.1x book )

-

History doesn't repeat, but it rhymes. This is a great book I read years ago about the Penn Central Bank Collapse. Penn Central was a small Oklahoma bank that was making loans in the Oil industry during the boom times. Big banks like Continental Illinois (which was the 2nd largest bank collapse in US history up until last week), was buying up a lot of these loans. When things went south, Continental was hit bad by these loans and then when the 1987 crash happened they were wiped out (A broker that they had purchased was badly run and the losses were the final blow).

The collateral on a lot of these loans were near worthless. Casings and pipes for drilling rigs can be sold for scrap, but a drill bit for an oil rig is kind of expensive and there are no uses for it besides oil.

A bank that specializes in one industry (even an extremely profitable one like the tech industry) is a risky proposition on the best days. When you match that with paying depositers short term and investing long term, like during the Savings and Loan crisis, you are doubling down on risk.

Most people never heard of Penn Central but the collateral damage it did took out a giant bank. I hope the SIVB damage is contained with the Government involvement and bailout, but it very easily could have damaged many companies who were customers and would be unable to make payroll because the bank took stupid risks to get a few extra basis points of profit.

-

Even during the great financial crisis, when firms were going under, I don't recall their customers stock positions being affected. SIPC only goes $500k (vs $250k for FDIC). But I've heard Buffett say that he's not concerned about their stock positions if their broker goes under (is this because they are not held in street name, or because it's not really a risk?).

I see that SIVB depositors are getting bailed out, and I was surprised to see that Roku had half a billion dollars in cash there. But why wouldn't the treasurer or CFO of a public company keep most of the money in short term treasuries instead of a bank account? Aside from what you need to make payroll, keeping more money in your bank account than you need to pay bills seems like a unnecessary risk to take. If Roku had an account with, say, Charles Schwab and kept that money in 3 month treasuries, instead of a bank account would this be an issue for them if the Bank/Broker wasn't bailed out by the Government?

-

TV, VTS and OXY on the dip (when you can add to a position at a few hundred basis points lower than Buffett was buying last week, it's a good day. Some FFXDF and I have a resting bid on JOE with an 7 handle that hasn't been hit but it got close today.

-

I have a work conflict that prevents me from owning most banks, which is sad since everything is on sale. Added some TV, OXY and VTS on the dip. If JOE drops another dollar today, I'll buy some.

-

Added a little OXY, TV and SWBI. Just listened to the SWBI conference call after the close, it probably won't be this cheap tomorrow

-

Craig McCaw is involved now with a company called Clearwire.

The founders of Nextel are now involved with a company called Anterix which owns 900mhz broadband and licenses it to utility companies for private LTE networks.

My client, took control of Citizens Utilities (water, gas, electric) and sold off all the utilities and bought rural ILECs and renamed it Citizens Telecommunications. Because of the Universal Service Fee that you are (still) paying on your cellular service, it's almost impossible to lose money on rural fixed line phone service. He made a bunch of money on that and bought a gas/pipeline company (Southern Union) when the energy industry was in the dumpster. He later sold that for a bunch of money when energy was on an upswing. I think the last thing that he bought while I was still at the law firm, which he still owned at his death was a lot of Spanish Language radio stations in the US (Mega Radio). Which is part of the reason why I like Grupo Televisa so much (they own half of Univision, which includes a lot of Spanish language TV and Radio stations in the US).

-

Added a little VTS and OXY. When I think of worst case scenario 1970s stagflation, I think owning real assets, including oil is the best of the worst scenarios. Taxing windfall profits from energy producers isn't incentivizing anyone to look for new capacity so the existing capacity should be worth more.

-

If you hadn't heard of ChatGPT (or seriously considered that Google, Meta, Baba etc have all been developing AI for years and just haven't shown their hand yet), it looks like a no brainers. About 10% cash and selling at a multiple that is slightly above the historical SP500 multiple, with incredible growth and margins. If you step back and squint your eyes, it looks great. If you read the DOJ's antitrust complaint (yes, I'm a nerd) it doesn't look like a legal document. It looks like a pitch deck from a sell side analyst about why you should own GOOG.

It's my second biggest position (I've owned it since 2016) and I wouldn't buy more because LiLu owns it, but it's comforting to know that smart people think it's a good buy at these prices.

-

added a little SWBI. It dropped 6% yesterday, I assume it was on a false rumor that was trending on twitter that that they endorsed the Proud Boys (They showed a photo with a tacticool shirt from Perception Brands ("PB") which the outrage mob assumed Proud Boys merch).

added a little VSTO (still a small position but the ammo part that I'm interested in will be the remainco, and the whole thing doesn't look too bad now that they fired the acquisition happy CEO).

What are you buying today?

in General Discussion

Posted

Sold a small position that I didn't want to hold anymore and bought some TV, Fairfax India, and Eneti.