mattee2264

-

Posts

703 -

Joined

-

Last visited

-

Days Won

7

Content Type

Profiles

Forums

Events

Everything posted by mattee2264

-

What does seem to be the case is that if things do get bad then markets are likely to overreact on the downside with the Fed probably less inclined to step in and rescue markets the way they did in previous panic sell-offs. Fed is increasingly backward looking with its data-dependent approach and insistence they won't overreact to a single month's data (they failed to pre-empt inflation so it would be apt if they failed to pre-empt recession as well!) and with inflation above target still will need to see a meaningful deterioration in the labour market before cutting aggressively. Problem is that by then the economy is already in recession and in a vicious cycle (job cuts, reduce consumption, which reduces profits, which results in more job cuts etc) and while an interest rate cut might boost market confidence it won't reverse deteriorating fundamentals overnight. And when the market is used to disproportionately aggressive cutting cycles even a few 25-50 bps cuts won't be enough to satisfy it. As for AI it is almost 2 years since Chat-GPT got released and there's been a huge amount of capex spend and that is expected to lead to an acceleration of growth rates which is an incredibly difficult hurdle to overcome especially in a deteriorating economy. And any deceleration in capex spend is going to hit semis hard and they've become a huge part of the market. And with Mag7 approximately 1/3 of the S&P 500's market cap any selling pressure is going to hurt the rest of the market and the chances of a healthy rotation into small caps and other industry sectors is far less likely in a deteriorating economy where fear is on the rise and a flight to quality will mean defensives, bonds, gold etc which will have a net negative impact on the S&P 500 market price.

-

I think it is simply a case of momentum starting to run its course which puts us into more of a sideways market with a lot more volatility. CNBC do a Mag7 index and at the July peak it was up 3x from the October 22 lows. That is pretty incredible so a correction was inevitable. But cloud revenues continue to increase at a rapid clip, there is still an expectation that the AI capex spend will sustain or even increase revenue and earnings growth. No real signs of diminishing enthusiasm for AI capex spend which supports semiconductor valuations especially NVIDIA. And Big Tech seem relatively insulated from the economy. Companies will start cutting staff long before they consider cutting IT spending and if you are struggling to grow revenues then you are going to be very tempted to want to try AI products in the hope it can cut your costs. Not to mention the worry that if you don't do so then a competitor will and be able to undercut you. So there is a defensive aspect to the investments. As for the rest of the economy we are seeing a lot of weakness in consumer stocks and that isn't surprising really. Financials are probably the next domino to fall. Lower interest rates aren't bullish at all for banks especially to the extent they reflect a worsening economic picture. And the commercial real estate issues are closer and closer on the horizon. And commodities also won't do well if economy weakens. But the market is not the economy. It is 1/3 Big Tech and as I mention above they are secular growers. Aside from a few years of peak stimulus the US economy has been anaemic but it hasn't prevented Big Tech companies from growing at 20% a year. Financials, commodities, consumer stocks are probably only about 1/4 of the index and there will be an offset because in a flight to quality defensive stocks such as utilities, healthcare will do well. And it is only a matter of time before the next big stimulus whether it comes from US government or the Fed.

-

If the AI bubble like the Internet, in what year are we now?

mattee2264 replied to james22's topic in General Discussion

https://www.theatlantic.com/technology/archive/2024/07/thrive-ai-health-huffington-altman-faith/678984/?gift=bQgJMMVzeo8RHHcE1_KM0dnShzV9_FNXfV9x6vixORQ&utm_source=copy-link&utm_medium=social&utm_campaign=share This article is a bit waffly but its basic premise is fascinating: "Faith is not a bad thing. We need faith as a powerful motivating force for progress and a way to expand our vision of what is possible. But faith, in the wrong context, is dangerous, especially when it is blind. An industry powered by blind faith seems particularly troubling. Blind faith gives those who stand to profit an enormous amount of leverage; it opens up space for delusion and for grifters looking to make a quick buck. The greatest trick of a faith-based industry is that it effortlessly and constantly moves the goal posts, resisting evaluation and sidestepping criticism. The promise of something glorious, just out of reach, continues to string unwitting people along. All while half-baked visions promise salvation that may never come." Reminds me of the concept of religion stocks. And when you think about it there are so many reinforcing factors. -The dizzying ascent of technology stocks and especially NVIDIA seemingly confirming the promise of AI -The huge investments by "smart money" aka the tech giants in AI technology -The proliferation of Chat GPT which has enchanted consumers and business people alike -Sam Altman's masterful balancing act of downplaying the current capabilities while making seemingly profound pronouncements about future possibilities -The chorus of companies mentioning AI at every single opportunity in earnings calls and presentations and company literature -The appeal to greed as companies dream about the possibility of laying off half their workforces and increasing profits -The appeal to fear as workers worry about losing their jobs so figure they may as well invest in the technology that will eventually displace them And I am sure there are lots of others I have missed out. -

The interesting difference with the 90s tech bubble is that back then it was much more of a free for all. Anyone and everyone set up dot com companies. All you needed was a website and some pie in the sky business idea. The technology this time around is more widely available than people think. There are lots of LLMs being developed and a few interesting start ups for sure. Chip availability is a bottleneck but it is easing. But you have these huge tech gorillas who are doing everything they can to restrict the availability of AI chips and are funding a lot of start ups themselves. And I am sure they will try and buy up any promising competitors. But there is only so much they can do to delay the inevitable. And this is exactly how it is supposed to work. Before AI Big Tech were sitting pretty. Amazon dominated online retail. Meta dominated social media. Alphabet dominated search. Apple dominated smartphones. Microsoft dominated enterprise software. Cloud came along but with little capex required it greatly enhanced revenues and they shared the pie. The assumption is that they will dominate AI. But while AI bells and whistles may give them some incremental revenue it is likely that the transformative applications of AI (which are yet to be discovered) will come from nascent businesses and they will take investment dollars and consumer dollars away from the incumbents.

-

The problem at the moment is that AI can do some tasks that workers can do but at multiples of the cost! AI also needs a lot of handholding because there is still a good degree of hallucination. So the value proposition is somewhat questionable. And adoption has been quite disappointing by businesses. And for workers there is a catch 22. If their productivity increases because of AI then they put their job at risk. So they try to hide their use of AI. Luke's point I think is the ultimate beneficiaries will be the users of the technology. But even then it won't be overnight because adoption takes time and it takes time to learn to use a new technology. NVIDIA has a technological lead but so did Tesla and there is now a proliferation of EVs. And if NVIDIA loses market share or its margins fall its stock price will get destroyed! The other Mag 7 companies are all scrambling to release AI products to recoup their massive capex spend on AI and there are also start-ups releasing LLMs. It is difficult to charge much upfront because they need to encourage adoption and capture market share. As Zuckerberg has already said it is a long game and investors may not be patient enough to wait until then just as they weren't prepared to wait for the internet to bear full fruit.

-

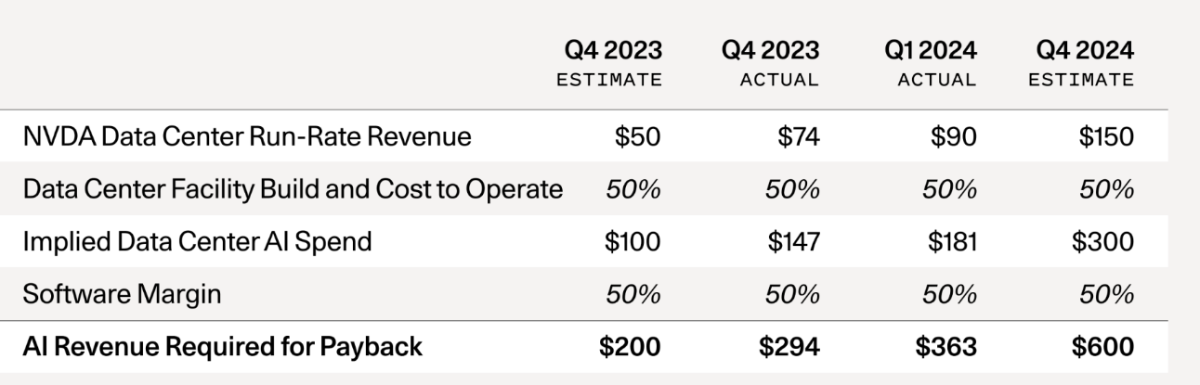

https://www.sequoiacap.com/article/ais-600b-question/ This is a good read as well which should also encourage caution for those investing in a top heavy S&P 500. For those too busy to read the article the table below sums up the argument: we are seeing huge amounts of AI spending but it has yet to translate into any meaningful incremental revenue.

-

It is a stupid situation really. Interest rates could be a lot lower if the US government showed even a modicum of fiscal restraint. And that would in turn make US government debt a lot easier to service. And then you would have a chance of growing nominal GDP faster than national debt so that US government debt as a percentage of GDP would decline over the next decades instead of spiralling out of control. Of course for markets it doesn't matter.....until it does.

-

If the AI bubble like the Internet, in what year are we now?

mattee2264 replied to james22's topic in General Discussion

Something that Big Tech should be very worried about at the advent of a new technology is you cannot control people. Fat salaries are not enough. Bright young things are always going to want to take the first class training they've had places like Meta, Google, OpenAI and start their own companies. Being a "founder" is considered very cool by the kids. -

If the AI bubble like the Internet, in what year are we now?

mattee2264 replied to james22's topic in General Discussion

I don't think anyone can really claim that AI is within their circle of competence. But at the same time no-one wants to miss out. Most people just buy NVIDIA. They are the only ones making any money from AI and the gold rush analogy is intuitively appealing. So long as everyone believes there is gold to be found they will keep panning for gold and NVIDIA has a monopoly in picks and shovels. Big Tech have been cornering the market in AI chips and also funding start-ups and partnering with OpenAI. And with their massive user-base it seems logical that if AI-enhancements make their products more valuable then they will make money (although question is whether they will make enough money to justify their huge capex spend). The problem is that incumbents rarely come up with anything revolutionary. Doing so would mean cannibalizing their existing technologies and products and also as companies mature they become less dynamic and more focused on efficiency and monetization than innovation. And a lot of their investment is defensive in nature. Good for them. But bad for everyone else because it is blocking progress. -

If the AI bubble like the Internet, in what year are we now?

mattee2264 replied to james22's topic in General Discussion

So far it is a virtuous cycle. Big Tech pump up NVIDIA stock price. NVIDIA going vertical boosts confidence in AI and supports the narrative that Ai will change the world. Big Tech's huge investments in AI make investors believe that incredible growth and profits lie ahead even though these companies already have multi-trillion market caps. And AI is the easiest thing in the world to market. Corporates are rubbing their hands with glee imagining the potential to lay off half their workers. Consumers have been enchanted by Chat GPT already and can't wait to try the latest iterations. But there is a lot of extrapolation going on. Existing use cases are cheating on college papers, drafting emails, taking meeting notes and providing a somewhat superior upgrade to chat bots and personal assistants (Alexa etc). Useful maybe. But is it really going to move the needle and justify continued spending of tens of billions a year? Also a lot of the spending is defensive. In the same way that Big Tech maintained their dominance by acquiring every potential competitor they are stockpiling chips and investing in AI start-ups. They'd rather lose money investing in something that ultimately turns out to have low returns than risk missing out on the next big thing and getting disrupted. But as people said early days. People will have a bit of patience because the technology is new and there is still the belief that if enough computational power is thrown at AI it will bear fruit and mature into AGI. But eventually AI will have to deliver in a meaningful way to the ultimate users. -

"Magnificent 7" Top of the Market?

mattee2264 replied to Thelilyinvestor's topic in General Discussion

Approaching $10TR market cap for Apple + Microsoft + Nvidia. https://www.morningstar.com/news/marketwatch/20240614265/the-sp-500-would-be-nearly-20-lower-without-ai-mania-says-bespoke Article above reckons S&P 500 would be about 20% lower without the AI mania which sounds about right. What you are also seeing is ridiculous volumes of call option activity on these three stocks. So even allowing for the quality of these stocks with their monopolies, competitive advantages etc. there is a lot of speculative demand for their stocks and if this evaporates when momentum reverses then there could be a long way down. -

Stocks that did well 2000-12 (when S&P500 was flat)

mattee2264 replied to thowed's topic in General Discussion

The resources super-cycle thesis is now greening and the economy and AI. That could turn out even better than the China super cycle. Although there will probably be a better long term buying opportunity as the global economy slows down over the coming year. Emerging markets seem worth a look. And you can even do it ex-China. Malkiel and Ellis did a good analysis of the lost decade for the S&P 500. They found a diversified portfolio which included EAFE, EM, small cap did just fine. I suspect the same might be true given the S&P 500's incredible outperformance over the last decade. Ex-USA most valuations are pretty much in line with historical averages and even if AI lives up to all the hype then the resulting productivity improvements will mean faster growth and higher margins for ex-USA companies. But in the USA margins are already way above the historical average so any AI related benefits to margins could well be offset by higher taxes, more regulation, higher interest rates etc. And if AI flops then high flying USA tech companies have the furthest to fall. -

Thought this would be worth an update. Eurostoxx has gone up about 20% since the October 2023 lows after Powell fuelled rate cutting hopes. But really it has gone nowhere over the last decade with a return of around 70-80% with dividends reinvested. Meanwhile USA stock market has gone up almost 200%. It has its fair share of cyclicals (banks, industrials, oil and gas, autos, chemicals) but majority of the index is represented by growth/quality/defensives such as technology (ASML, SAP), health (Sanofi, Novo Nordisk, Roche), consumer goods (LMVH, L'Oreal) etc. And over the last week or so it has started to sell off after the French political turmoil is spooking European stock markets. If sell off continues might make an interesting buying opportunity for those looking to diversify outside the USA.

-

TIPS at a 2% real yield do look pretty attractive. And might not be around for much longer. I don't think nominal long bonds at 4% are that attractive from an income POV. To get 2% real returns holding to maturity you need to assume over the next decade inflation averages 2%. The Fed may well achieve its target during slowdowns and recessions but with all the debt in the system I do not think it is willing to be aggressive enough to do so over the cycle and some of the disinflationary trends are reversing with a move towards protectionism, more geopolitical tensions and conflicts, increased demand for finite resources for green energy and AI etc. And you are already pricing in further disinflation and rate cuts to the extent that the yield curve is inverted. If a more normal term premium of 100bps or so is re-established that could offset any benefit from further rate cuts. And if inflation remains above target then absent a recession the Fed probably doesn't have that much room to cut. But there is still a chance of a hard landing or something breaking in a serious way. And that is a good reason to have some long nominal bonds because if the Fed does aggressively cut rates (and it has over 500 bps of runway to do so) you can get some very good capital gains. Also it is pretty clear that those worried about a return to 70s stagflation were wrong. You don't have the conditions for a wage-price spiral. Illegal immigration and the threat of AI will make workers wary of asking for wage increases and we aren't as unionized as we were in the 70s and with remote working you can outsource and draw from a wider labour pool.

-

CPI/interest rate focus is ridiculous. Europe and Japan had outright deflation and ZIRP for long stretches of time and massive amounts of QE and their stock markets went absolutely nowhere. As Powell said himself when you look 5 or 10 years out it is impossible to detect any impact from a 25 bps interest rate change. Earnings are what matter. S&P 500 was 2000 a decade ago. Now it is over 5000. And over that same time period S&P 500 EPS has increased from $100 to around $250. So pretty much all of the increase in stock prices can be attributed to earnings. And you cannot evaluate the impact of interest rate changes in isolation. If interest rates are rising because the economy is growing strongly then the earnings benefit offsets any negative impact from interest rates and stock prices will go up. And if the Fed is cutting interest rates because earnings are falling off a cliff then as we've seen in prior cutting cycles stock markets will go down. And inflation is also intimately connected with the strength of the economy. The transitory supply side influences have mostly gone. So any further declines in inflation are likely to be cyclical and reflect a slowing economy. And if inflation increases it will probably because the economy is growing strongly. But there seems to be a lot of confidence that corporate earnings (especially for favoured Big Tech companies) will grow strongly and therefore investors are praying for bad economic data and rate cuts in the hope that rate cuts add fuel to the fire and result in even higher multiples that get multiplied by higher earnings and continued rapid stock price appreciation. In a way I understand their point. Big Tech did benefit from a period of economic stagnation that resulted in low interest rates and Fed policies to flood markets with liquidity that coincided with a long period of secular growth powered by monetisation of the internet, adoption of e-commerce and digital advertising, shift to the cloud and now AI. But at the size they are now their fortunes are probably a lot more closely aligned with GDP growth because they now dominate their markets and adjacent markets and while AI represents virgin territory everyone is competing for their slice and the only one making serious money from AI is Nvidia.

-

Inflation adjusted oil price is way below the $100 reached in the middle of last decade. Shale productivity is declining and ESG concerns are making it difficult to fund exploration and development spending. Oil demand shows no signs of declining and it is becoming increasingly clear that fossil fuels will play an important role in bridging the energy transition. There has been a lot of consolidation in the space and bigger players are more focused on paying dividends/buying back shares and producing FCF rather than growth at all costs. Near term there could be some weakness if we go into recession and China continues to struggle economically. But low prices will discourage production and investment and provide a setup for a big rebound in the future. And you are being paid to wait because dividends are very generous in the sector and buybacks at lower prices are more accretive to value.

-

Institute of International Finance recently stated that global debt (governments, consumers, businesses) is $315TR. That compares to global GDP of $109.5TR. Maybe it is nothing. But there probably is a link between massive accumulation of debt since 2010 and the incredible global stock market performance. And if interest rates stay high or there is a rise in unemployment or a fall in corporate profitability or bond vigilantes start disciplining governments running unfunded deficits then it probably will start to matter in a big way.

-

CNBC's newsfeed was amusing. GME reported a 29% decline in sales and $32m loss in the first quarter. But pre-market trading its up 30% because Roaring Kitty is doing a livestream. This isn't a market where fundamentals matter.

-

Is the signal as accurate in this day and age when the Fed manipulates bond prices not only through the base rate but also by QE/QT operations? Or when speculators have been buying long bonds betting on a pivot and continued disinflation due to the Fed's forward guidance? Regardless the actions of central banks such as ECB and Canada show that central banks aren't going to let the inconvenience of inflation being above target prevent them from cutting aggressively and blowing up their balance sheet via QE if we go into recession or there are any kind of issues in the financial system. So the moral hazard is alive and well.

-

Gold miners versus physical gold value gap

mattee2264 replied to mattee2264's topic in General Discussion

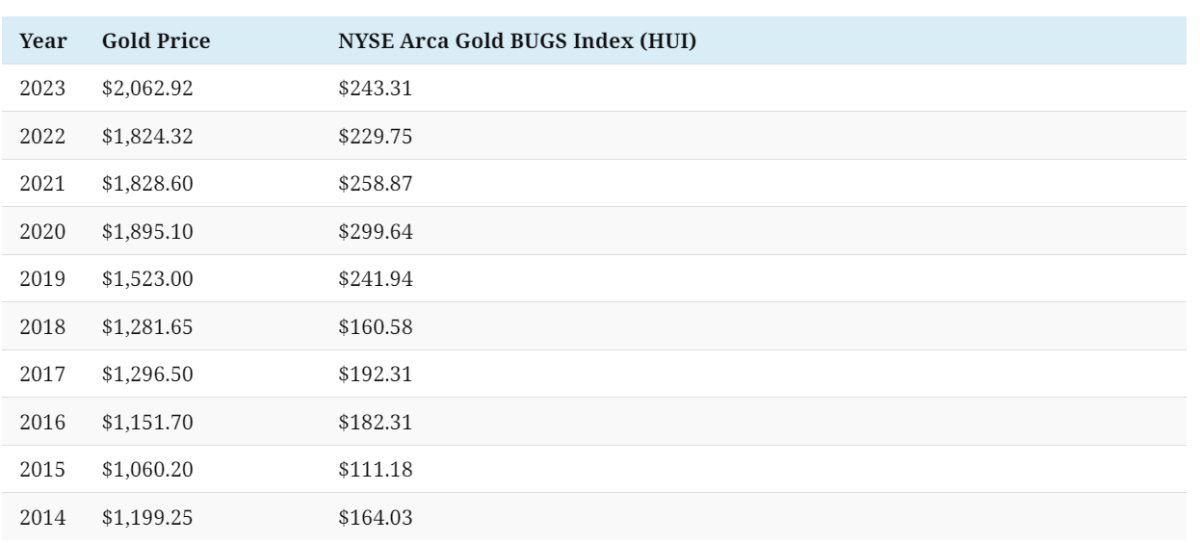

Central banks are also loading up on physical gold. I was going to go with Barrick and Newmont and Agnico Eagle Mines as they have diversified portfolios mostly in stable regions and not make it a large position. I was a little surprised by the shale analogy. My impression is at least at the top end the industry is consolidating and reserves have been declining over the years as new investment is not forthcoming. And this trend will probably continue as ESG discourages mining. And the CEOs of the top miners with Barrick a good example are talking free cash flow and capital discipline etc. -

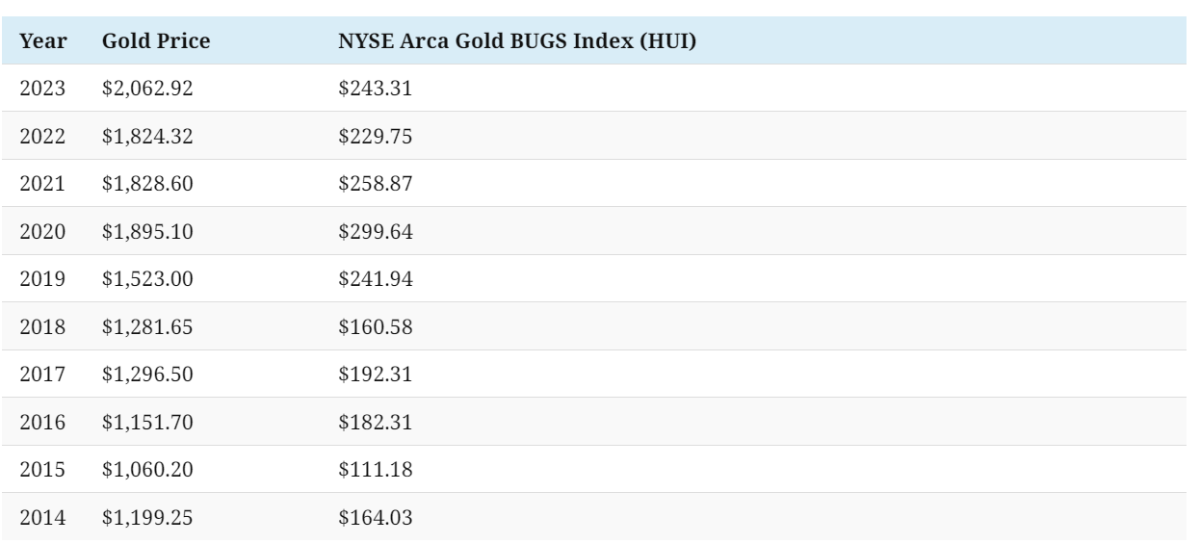

Gold has been on a tear lately. But little evidence of that in the price of gold mining stocks. Disconnect is especially apparent since the pandemic not surprisingly as operational costs have risen, interest rates have risen and ESG considerations have tainted the mining industry. But the weighted average all in sustaining costs are around $1,345 per ounce (Source: S&P global March 24) so there is a healthy spread. Difficult to imagine much expansion of supply and the industry is consolidating. And unlike physical gold you get dividends while you wait for the gap to close. I do not have a strong opinion on gold but when central banks are increasing the money supply at a rapid rate its nice to have something that is fairly limited in supply and isn't something like crypto that is overhyped. Anyone else have any thoughts on gold miners as an investment?

-

I can see markets melting up this summer when it becomes clear that central banks across the world are quite happy to start cutting rates even while inflation is still above their respective targets. But if falling interest rates are accompanied by falling earnings later in the year then it might be a case of "be careful what you wish for".

-

Who needs births when you have a never-ending labour pool of illegal immigrants to drawn on?

-

Not much more than a hundred billion or two of market cap away from overtaking Microsoft as the most valuable company in the world. There are other technology companies in the trillion dollar market cap club. But their moats have been time-tested and they've shown the ability to defend them and expand them over time and the use-case is obvious: any modern business needs Microsoft products to operate and there are over 1B I-Phones in circulation and most people can't live without their phones and therefore want the top of the range and Apple has been ruthless in charging companies who want access to their customers. Meta has over 3BN monthly active users who spend a good amount of their waking hours on social media. Google has YouTube and still dominates search. And Meta and Alphabet have a duopoly in digital advertising which accounts for around 2/3 of total advertising worldwide and is used by every company trying to reach consumers. Amazon dominates e-commerce and cloud. And built up both businesses over many years from nothing. It is easy to understand why NVIDIA is minting money in the here and now. They are selling shovels in an AI gold rush and such is the confidence that there will be gold that everyone wants the shiniest shovels. And they aren't selling to penniless miners but to the richest companies in the world who make so much money they can afford to stockpile AI chips rather than risk missing out on the next big thing. But there seems to be an assumption that this dynamic will go on for decades. And it seems implausible that these companies will continue to spend most of their capex budget on AI chips from a single supplier for the next decade or two, let alone the next year or two. And the underlying premise seems to be that computational power is the only limiting factor and all you need to do is throw more and more computational power at AI development and it will achieve all the wonderful things people are predicting of it. And there is a lot of extrapolation. Right now you can use AI to write an email, make meeting notes, do some basic coding, do a term paper, and generate some cool images and write a bit of poetry. Useful and fun. But if that was all there was to it you wouldn't see Nvidia with a $3TR market cap and AI has probably accounted for a significant amount of the trillions of market cap that other Big Tech companies have added over the last year and a half. So implicitly there is this notion that AI will be able to replace millions of workers and therefore a significant proportion of the money companies used to spend on wages will end up lining the pockets of the companies selling AI technologies. And it will happen fast enough to satisfy investors who are notoriously impatient. After all, all the things people were expecting of the internet such as the mass adoption of e-commerce and digital advertising eventually happened but not fast enough to support the market caps reached at the peak of the bubble.

-

Problem though is that even a safe 6-7% is very boring and unattractive to most investors who always look in the rear window mirror when it comes to projecting future returns and over the last 5 years you'd have made over 25% a year investing in the Nasdaq and almost 15% a year investing in the S&P 500. And investors aren't worried about losing money because they figure the Fed will rescue markets at the first sign of trouble. Bull markets do not end because investors decide bonds offer a better risk-reward. They end because sentiment shifts and investors are more worried about losing money than anything else. That is probably why stagflation is the greatest worry because it could conceivably prevent the Fed from rescuing markets and might even require them to increase rates as well as being a serious headwind to earnings.