Viking

-

Posts

4,936 -

Joined

-

Last visited

-

Days Won

44

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

Does anyone have thoughts on the RiverStone UK sale? Fairfax mentioned when they announced the sale that there will be a $10 gain in BV. My guess is that is still coming in Q1 when the deal is announced (i.e. it did not hit in Q4 financials). Correct? Prem on the conference call said the benefit of selling 40% and getting OMERS involved is it will provide access to $ to grow the business. It will be interesting to see how fast Riverstone UK grows post acquisition. Sounds like there are lots of opportunities. That deal closes soon (sometime in the next 6 weeks). Fairfax will be able to put the $600 million to work. They will likely use it to buy 10% of Brit and Eurolife minority interests. And grow the business at the insurance subs. Prem mentioned they may IPO Riverstone UK down the road. Perhaps that is the plan for how they will take out their minority partners in Allied. Trade runoff (Riverstone UK) for minority positions in Allied and Brit looks like a good trade to me. Makes Fairfax more of a pure play insurance operation and removes the overhang of having to find a big chunk of cash to buy out minority partners (especially in a hard market when your stock is trading below BV). It really is amazing how much stuff is going on under the hood at this company. My guess is 2020 will see lots more developments just like 2019 :-)

-

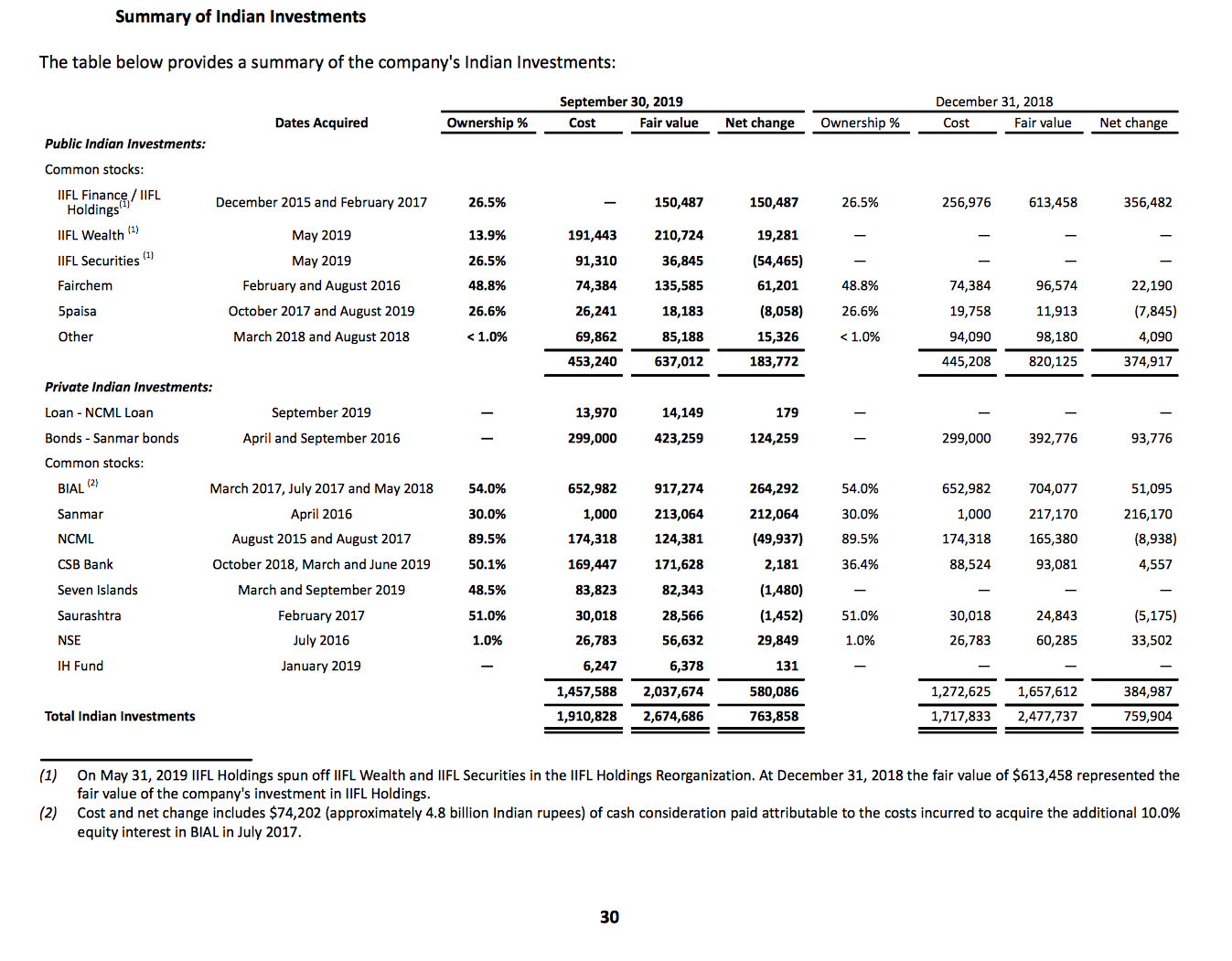

Xerxes, nice to hear that you are finding the spreadsheets useful :-) The Fairfax information is much more 'hairy' and I plan on updating it when the Annual report comes out. The share count (for all companies) is shares owned by Fairfax India. If you are interested the Fairfax India quarterly reports do a great job of clearly laying out all investments they hold (with lots of different perspectives). I wish Fairfax would do the same. I have attached a screen shot of page 30 of the Q3 report as an example (hopefully it opens in a format you can see).

-

Here is a summary of Q4 results from one of the big Canadian banks: “Our view: The insurance part of the business is shifting into a higher gear with strong growth, improving margins and still solid reserves. Quarterly results were negatively impacted by some non-insurance items that are largely one-time in nature. We think valuation is among the most attractive in the P&C space at a discount to book value with rising earnings momentum.”

-

Fairfax India reported yesterday. As expected, the increase in 'fair value' of BIAL increased BV to $16.89/share (from $13.86 at Sept 30). Key development: "The net change in unrealized gains on BIAL of $751.5 million are supported by positive operational developments and the finalization of BIAL's real estate development plan." The other piece of good news with Fairfax India is what is going on with its triplet investments in IIFL (Wealth, Finance and Securities) to start the new year. These three companies had been in a bear market for about 24 months (falling in value by more than 50%). However, they all look to have bottomed in price last Oct and have been moving higher since then. And so far in 2020 (6 weeks) they are up +45% or about $180 million. Fairfax India has 153 million shares outstanding so this increase (more than $1.00 per Fairfax India share) is significant. This will be worth monitoring moving forward. Shares are up a little today to $12.94 Attached is an Excel spreadsheet that can be used to track all of Fairfax India's publicly traded holdings (tab 2 of the spreadsheet is a tracker for FFH holdings). Let me know if you see any errors :-) Fairfax_Equity_Holdings.xlsx

-

A couple of notes from the conference call: - Annual report and Q4 info will be available March 6 - net written premiums grew at accelerating rate each quarter; sees trend continuing in 2020 - supporting growth of insurance subs top priority; this is because hard markets occur infrequently and only last a short period of time (a couple of years) - share repurchases will be done with cash not needed to grow insurance subs - in the non-insurance segment, TCook/Quess demerger resulted in $191 million impairment - US runoff had $216 million loss due to asbestos strengthening; example of social inflation - $600 million will be coming to FFH in Q1 when the Riverstone UK deal closes; after sale closes Riverstone UK will have opportunity (with OMERS) to grow business. Fairfax may take Riverstone public at some point. - minority insurance partners buyout: 10% of Brit soon at $100 million (seems low?); Eurolife will be small amount; Allied agreement opens up mid year and Fairfax has 3-4 years to buy out minority partner - Go Digit: the company recently raised 10% at $800 million valuation. The $300 million gain recognized by Fairfax was Go Digit convertible shares (owned via Quess) not the common stock owned by Fairfax (hope i got this right) - BIAL sale was to third party investor; purchaser was not named

-

SJ, regarding market valuations my guess is Fairfax is expecting the US and global economy to continue to chug along which should be good for stock markets. When you look at their specific holdings (Dec 31, 2019 valuations) there is nothing that i would call grossly overvalued and not much that i would call overvalued. The large position in Indian equities (Quess, Thomas Cook and the twin IIFL positions) have been in an 18 month bear market that looks to have finally turned in the last 6 weeks (for Quess and IIFL anyways). Similar for their position in Recipe - casual dining restaurant stocks in Canada have been getting crushed all 2019. Hard to see Recipe getting much cheaper and when they get back to same store sales growth (and improve profitability) there will be lots of upside (2H 2020?). Seaspan had a wonderful run in 2019 but i dont know if i would call it super expensive (perhaps a little expensive). Eurobank also had a great run in 2019 (it was crazy cheap at the end of 2018) and is probably fairly valued now with decent prospects. Blackberry is not expensive and if the Cylance acquisition works out it could increase 50% or more. Bottom line, valuations of the stocks they hold look pretty reasonable in aggregate. 2020 should be another decent year for investment gains.

-

Here is what one investment house had to say in their preliminary report :-) "Net/Net: Core insurance underwriting results were strong and growth was good across most units although this was significantly overshadowed by weak results from non-insurance operations, affiliates, and the run-off unit. While we think that Fairfax is well positioned for current favorable market conditions, quarters like this are why valuation has continued to lag peers. A conference call will be held at 8:30 a.m. ET (dial-in 800-369-2013; passcode Fairfax) on Friday, February 14."

-

That’s worrying. Petec, given he is going to continue to be involved with FFH in a small way i am not worried. Yes, it is unfortunate to lose a good person. My guess is Fairfax has a deep bench to pick a replacement from.

-

All in all, very good results. Chug, chug, chug. Most importantly a few nice upside surprises. 1.) solid top line growth of 11% for year 2.) solid CR of 96.9, slightly improved from last year - big jump in underwriting profit of $394 versus $318 last year 3.) reserve releases - solid $295 million in Q4 across all subs 4.) BV = $486 versus $432 Dec 31 2018, +14.8% (including $10 dividend) 5.) As expected, lots of changes to equities, most positive. Will need more disclosure to fully understand individual impacts. Quess revised down. Digit revised up. 6.) no update on buying out minority partners (unless i missed it) 7.) shareholders - no meaningful share repurchases; expect this to be discussed on the conference call tomorrow 8.) has Fairfax learned the lessons? - very good quarter. Lots of good news and positive trends to continue to build on. Stock closed today at US $460 or Price to BV of 0.95 (BV is now $484). Top line is growing due to hard market. Underwriting is improving. Interest and dividend income is growing. Investment results were very good and look well positioned moving forward.

-

Fairfax India. Book value at Sept 30 was $13.53/share. The Anchorage/BIAL transaction will result in BV gain of $3.30/share. This takes book value to about $16.80. Fairfax India owns large stakes in IIFL Finance, IIFL Securities and IIFL Wealth. These are publicly traded companies. So far in 2019 (6 weeks) the stock prices of these 3 companies have increased about 45%. At Dec 31 their combined value to Fairfax India was about $400 million. Today they are worth about $590 million = $190 million gain. With 153 million shares outstanding for Fairfax India the increase in the IICL companies is about $1.20/share. Bottom line, book value of Fairfax India as of today is likely approaching $18.00/share. Shares are trading today at $12.45. Looks like a decent margin of safety to me :-) From Fairfax India Dec 16 press release: “As a result of the transaction, Fairfax India will record investment gains of approximately $506 million (approximately INR 35.6 billion at current exchange rates) implying an increase in book value per share of approximately $3.30 per share. The investment gains are supported by positive operational developments at BIAL. For the 12-month period ending October 2019, total traffic at BIAL was approximately 33.7 million passengers. The second runway commenced operations in December 2019, making BIAL the first airport in India to operate independent parallel runways that enable aircraft to land or take-off simultaneously on both runways. In addition, the expansion project for a second terminal at BIAL is expected to be completed in 2021.”

-

They're pretty secretive and they're probably the most under the radar PE firm out there. And the model is fairly unique - they basically source deals from their own network of high net worth individuals who own businesses and promise to hold them for a long time. Not forever, but also not flipping it three years down the road. Very Buffettesque way of doing business (e.g., proprietary sourcing, stable capital, etc.) and it seems to be working. Whether the deals are good or not I have no clue as they don't seem to be targeting institutional money (at least any that I could find), so no disclosure on performance at places like Calpers, etc. Thanks for the info. BDT Capital looks like a quality operation which is nice to see especially given its large size in Fairfax’s equity portfolio. The position increased nicely in size from $355 at Dec 31, 2017 to $443 million at Dec 31,2018. No idea if they added capital to the position or if the increase was all gains. Hopefully they once again do the same disclosure (top equity positions) at the AGM this year.

-

My experience is the simpler i can keep things the better (both mentally and return wise). I would bite the bullet and merge the two into one. Investing decisions get more simple. Allows for maximum flexibility at withdrawal time. My guess is your improved returns over time will more than offset the financial hit in the short run. Give the long time horizon why not wait 6 months or longer for a nice fat pitch. They usually happen about every 2-3 months. Because your portfolio will be fairly concentrated it makes sense to have a high bar in terms of what/when to buy. I have posted this before... i have three kids and started a group RESP when the 3rd was born putting in $2,000 each ($6,000 total). The government added 20% so i started with $7,200. We never put any more money in. When my oldest started university (Sept 2018) the RESP was $104,000. My guess is the RESP will pay for 1/2 of each kids post secondary schooling. The keys to compounding were: 1.) low fee structure (self directed RESP so low cost to execute trades) 2.) one account for all three kids: made investment decisions very easy, especially in the early days when the $ amounts were lower 3.) of all my investment accounts, over the years only my very best ideas went into my RESP (and TFSA’s). I was very patient when making buys. 4.) i was not afraid to concentrate when great opportunities appeared 5.) i was not buy and hold for 14 years; buy low and sell high Today all three of my kids understand they have an RESP and its total value. There are no sibling issues in terms of how big ‘their’ account is. Just a bucket of money to help them get a post secondary education and hopefully graduate debt free :-) Good luck :-)

-

I certainly agree. Just "switch to quality" is not that easy either. Exactly. Fairfax is an insurer/investor that focuses on value* and invests globally, including in some risky places. If you want an insurer/investor that focuses on long term ownership of quality stocks in a jurisdiction with low political risk, I’m sure you can think of one ;) *Edit: value and quality aren’t mutually exclusive, obviously. CIB, Quess, Bangalore and others prove Fairfax aren’t averse to quality when they can find it cheap. My point earlier was more intended more for the company to live its guiding principal: “We always look at opportunities but emphasize downside protection and look for ways to minimize loss of capital.” There are too many examples where the company invested in a distressed company/industry. Things (predictably) got worse and they doubled down. Things got (predictably) worse and they doubled down again. Resolute is the best current example. Blackberry is another good example although the story is still being written there. Where was the downside protection to minimize the loss of capital? When Prem talks about Fairfax and its investing style he sounds like Graham: value investing with a focus on safety of principal. Walk the talk is all i am saying. If you want to continue to swing for the fences with very large purchases of shitty companies/shitty industries then change your Guiding Principle. Clear communication with investors is all i am saying. Fairfax has brought in some new people to their investment team. I am optimistic we will see a subtle shift in the equity portfolio over time to more quality positions :-)

-

If Fairfax is serious about hitting a 15% BV growth average over time they will need to write at a sub 95% CR. Bonds represent the majority of the investment portfolio and yields are very low and look likely to stay low. The whole insurance industry is facing the same issue. On conference calls other insurance companies are communicating that they are getting price increases a couple of % in excess of expected loss trends. They expect this will result in a lower CR over time. These companies need a lower CR to deliver return targets required by shareholders. And their stock prices are moving higher as a result. I am pretty sure Fairfax feels its shares are very undervalued. The reason they are so undervalued is the company has not been able to grow book value per share (much) over the past 5 years. And investors have little confidence they will be able to grow BV moving forward (let alone hit the 15% target). They should deliver a +15% growth in BV this year. Will they deliver in 2020? Writing at a 97.5CR they will need their equities to do exceptionally well every year and this is simply too much for an investor to reasonably expect. There is another solution. Get more aggressive with lowering your CR. (And if you don’t grow top line as fast put your excess capital into share buybacks.) Fairfax has much improved its underwriting from when i first started following the company way back in The early 2000’s. Its CR over the past decade is pretty decent and some subs are very good. I think they understand and will find a way to lower their CR to below 95% in the coming years. As i mentioned in my previous post, placing parts of Advent in run off and minimal growth at Brit (worst op co from CR perspective) are good signs. The op co’s with the best historical CR’s appear to be growing the fastest in the current hard market which is another positive sign. Fairfax is so big now it is like a big oil tanker. I do believe they have been making incremental changes the past couple of years that are slowly turning the ship in a better direction for shareholders. I think we are going to see the insurance op co’s continue to improve (with some bumps along the way). And i think investment results will also improve. And the management team has demonstrated in the past that it can be very creative in surfacing value (with the sale of 40% of Riverstone being the most recent example). In 2012-2017 Fairfax dug itself a very big hole. I think they are just now crawling out. The head winds are now being replaced with tail winds. 2019 was a very good year. 2020 could be just as good. So i am optimistic :-)

-

A large chunk of Fairfax’s equity holdings are being negatively impacted by the Coronavirus risk off environment: Eurobank, Seaspan, Emerging Markets equities (Fairfax India, Fairfax Africa, Thomas Cook India).

-

Fairfax releases Q4 results after markets close on Thursday. Here are a few of the things i will be watching: 1.) what is top line growth? - Looks like we are in the early innings of hard market (ex workers comp) so growth should be solid 2.) what is company wide CR? - with 10 year US government bonds trading at 1.5% a CR of 95% is the new 100% - Fairfax said its presidents are incented at a 95% CR. Fairfax needs to now start to shoot for sub 95% CR (after catastrophes). - Placing parts of Advent into runoff at the end of 2018 and minimal growth at Brit (worst CR performers) perhaps lowers company wide CR moving forward. 3.) what is trend in reserve releases? - the trend (industry and Fairfax) has been lower over time. 4.) increase in book value per share - should be a very good quarter for book value growth - all three engines should contribute: underwriting, interest and dividend income and investment results 5.) update on recent transactions and their impact on financial statements. Not sure what gets booked in 2019 or 2020. - Sale of ARP to Seaspan: Atlas will acquire APR, the world's largest lessor of mobile gas turbines, in an all-stock transaction valued at $750 million including the assumption of debt, for an expected equity value at closing of approximately $425 million. Atlas shares will be issued to the sellers in the Proposed Acquisition at $11.10 per share. - Sale of 40% of Riverstone UK to OMERS: The cash purchase price of at least US$560 million... will result in Fairfax recording a gain of approximately US$280 million before tax (an increase in book value per basic share of Fairfax of approximately US$10 before tax...). - Demerger of Quess shares from Thomas Cook (TC owned 71 million shares of Quess and FFH owns 67% of TC): September 30, 2019 the company's investment in Quess Corp Limited had a carrying value of $1,038.7 which exceeded its fair value of $477.2 as determined by the market price of Quess shares. - For Fairfax India, sale of 5% stake in Bangalore Airport for $134 million. Will record investment gain of $506 million or $3.30 per FIH share. - For Fairfax India, transaction with Sanmar: Sanmar purchased $300 million principal amount of Sanmar bonds held by Fairfax India, plus accrued interest at an effective annual interest rate of 13.0%, for net cash consideration of approximately $425 million. Fairfax India re-invested $200 million of the cash consideration received from the bond sale in the purchase of Sanmar common shares. Fairfax India’s equity interest in Sanmar increased to approximately 43%. Fairfax India will retain approximately $225 million of the cash consideration for future Indian investments. 6.) update on buying out minority partners - Brit and Eurolife appear the two at the top of the list. This really sucks as Fairfax has such better uses for cash right now. Brit is the worst performing op co (from a CR perspective). But it sounds like they are contractually obligated to do these deals in the near term. 7.) shareholders - when do we see meaningful share buy backs? - Most of Fairfax’s insurance peers have seen their stocks appreciate 30-40% over the past year. Fairfax stock is down 4%. - Fairfax stock is actually trading 10% below where it was trading 5 years ago. 8.) has Fairfax learned the lessons? - The decisions Fairfax made over the past 7 years have shattered investor confidence in the company. - Fairfax has said they have learned the lesson when it comes to shorting the market. That is a good start but more needs to be done to restore investor confidence. - Are they done with empire building (low ROE insurance acquisitions)? - Will investment results improve? Walk the talk on this Guiding Principle: “We always look at opportunities but emphasize downside protection and look for ways to minimize loss of capital.” Stop saying the problem is value investing is ‘out of favour’. Investments in declining companies like Blackberry or declining/shitty industries like Resolute or Stelco are simply bad decisions. Or regions with unmeasurable political and/or currency risk like Africa. There is no safety of principal; and it is not investing it is gambling - Own it, learn from it and stop doing it! :-) If Fairfax wants to attract more long term investors as the equity portfolio turns over they need to move up the quality ladder with the companies they hold. Hopefully this is what we see moving forward.

-

Wondering, i was trying to list only the largest holdings (over $200 million). Yes, these are a bunch more (values at Dec 31): - Resolute $128 - Stelco $102 - IIFL Finance $55 (the three IIFL co’s are also held in Fairfax India) - IIFL Securities $16 - IIFL Wealth $70 .... and more smaller holdings

-

What happened to European stocks starting April 2015?

Viking replied to RuleNumberOne's topic in General Discussion

To me at least, the question is, who cares? The only one with a material benefit from RNOs returns are RNO. If we dive in, as has been done, its probable to conclude that the returns are of course "possible" but very "unlikely". But again, whether they are or arent doesnt really impact anyone but the author. If we wanted to be scrupulous jerks, we could literally attack just about every single person on the board who ever posts an investment idea, analysis, or makes a statement. We are all(hopefully) at least in the category of moderately sophisticated investors; we can all come to our own conclusions without being pompous jerks and risk alienating other(and future) posters, especially ones who actually take the time to engage. I've actually been quite surprised by how many people read, but dont post. Ive been contacted via PM a bunch of them over the years and the reason is always the same... Further, sometimes, there are people who go far out of their way to do the above, when their own "analysis" could just as easily be picked apart and disparaged unnecessarily, probably to an even greater degree. All I'm saying is that I dont think engaging in that sort of stuff is productive. For all the whining about politics from people, at least those of us that engage there know what we are getting into and its largely contained to its own section. Someone taking the time to post their thoughts or share their "strategy", and being called a "liar", or having posts from the past dug up and ridiculed...I dont really see what purpose any of that serves. (especially again with the nitpick bs like "oh you said easily 25-30% here, and now say 50%! OMG. well, 50% is "easily" better than 25-30%..." Who fucking cares? We all do our own thing. We're all going to be wrong if we invest enough. We're all going to make mistakes. If there are folks who claim they dont lose money or make mistakes, well, I think most of us are capable of drawing our own conclusions..... I'd point to Cigarbutt as probably a good example of doing it the right way... Gregmal, well said. :-) -

Here is my guess for Fairfax’s largest equity holdings (US$) at Dec 31, 2019. Fairfax has a total of $10 to $11 billion in equity investments. Please point out any errors you see :-) or values that look incorrect. 1.) Eurobank $1,255 - MTM 2.) Seaspan $1,096 - MTM (not included: APR = $381; warrants = $355) 3.) BDT Capital Partners $500 - Guess (Dec 31, 2018 = $443) 4.) Recipe $404 - MTM 5.) Commerce International Bank $395 - MTM 6.) Quess $324 - MTM 7.) Blackberry $300 - MTM (not include: convertible bonds which doubles share count) 8.) Kennedy Wilson $297 - MTM 9.) Toys R Us $234 - Guess (purchase price = US$234) 10.) Thomas Cook India $222 - MTM Seaspan and Quess are not captured mark-to-market in Fairfax’s financials. Quess MTM value is considerably less than where it is carried on FFH financial statements (carried at $1 billion which i think is pre-demerger from 67% owned Thomas Cook and their 71 million shares) and Seaspan is the opposite. In Q3 fair value of Investment in Associates was $600 million below carried value; this should shrink considerably when the Q4 report comes out. Not included: Fairfax India $660 - MTM (largest investment Bangalore Airport) Fairfax Africa $208 - MTM Others to research/watch (a few of these would likely make it in to the top 10 if we knew their current value). Digit: Fairfax’s stake may be worth $400 million AGT: Fairfax owns 59.6% Peak Achievement (Bauer/Easton) Dexterra (formerly Carillion) Farmers Edge: Fairfax has invested $159 million KWF Real Estate LP’s KWF Ireland Exco Resources $221 fair value (42.8% equity ownership); June 8 ‘19 emerged from bankruptcy protection

-

Question. At Dec 31, 2018 what was Fairfax's 2nd largest equity holding? My guess is most board members would get this question wrong (even if given multiple guesses). Answer: BDT Capital Partners (Oak Fund) = $443 million Source: Fairfax 2018 Annual Meeting presentation Currently, after Seaspan and Eurobank, BDT Capital Partners is likely Fairfax's third largest equity holding. A year earlier (Dec 31, 2017) its value was $355 million (#5 in equity holding that year) Given Fairfax has about $10-$11 billion in equity holdings this one represents about a 4% position. I tried to find information on the fund in Fairfax quarterly and annual reports but am striking out. So I am assuming they still hold their position :-). Interesting holding. Not domiciled in India. Not in a declining industry... Looks like a quality holding with well regarded management. Byron Trott (founder and CEO) used to work at Goldman Sacks where he was Warren Buffett's private banker. Anyone have any information on the company and/or the Oak Fund (what it owns)? Who are they? "BDT Capital Partners, LLC is a private equity arm of BDT & Company, LLC, specializing in investments in family-owned and entrepreneurial businesses. It also co-invests. BDT Capital Partners, LLC was founded in 2009 and is based in Chicago, Illinois." Here is an article: https://heavy.com/news/2019/06/bdt-capital-partners/

-

Here is what the CEO of Chubb had to say: "On pricing, I think, it endures. The fundamentals speak to it. And so the environment we see is the environment I imagine and will continue for some time, it's rational. And there are many reasons for it. And there is nothing that I see that tells me the momentum will slow. If anything, it's picked up, and it is spreading more broadly. Industry needs rate and needs it in quite a number of classes and across the globe. And then you're in a low interest rate environment and you can hardly rely on investment income to bail you out. And the industry needs rate because rate has just not kept pace with loss cost trends for quite a number of years. The math is so simple. People seem to over intellectualize this. And then on the other side of the coin, in the numerator, there are a few discrete classes where the loss environment is more hostile, and that is out there. That is understood. That is known and you either recognized it and reflected it in your reserves and in your loss picks and pricing in the past come, or it's something that you're doing with currently and is in front of you. But I think that just varies by organization."

-

No, i not have any insight there (and am not an insurance expert :-) So i listen to a few of the conference calls to get better insight into what is going on. The WR Berkely CEO said the hard market was being driven by three factors: low interest rates, increased frequency of cat activity and social inflation. I have also read that Lloyds has made some changes that has shrunk capacity. Perhaps these factors in aggregate are larger in size to excess capital coming in. RBC is now calling for pricing to remain hard for all of 2020 and likely into 2021 as well. I am looking forward to seeing what kind of growth Fairfax is getting and to hear from their CEO, who is a pretty straight shooter.

-

Well enough insurance companies have reported that it is pretty clear that insurance pricing is ‘hardening’, even though most do not want to call it a ‘hard market’ yet. What is encouraging is: 1.) price increases in Q4 are accelerating. 2.) increases are spreading to more lines. 3.) no end in sight. Here is what Chubb had to say in their earnings release tonight: “P&C net premiums written in the quarter grew 9.8% in constant dollars, supported by a pricing and underwriting environment that continues to improve, with rates increasing at an accelerated pace quarter on quarter while spreading to more classes of business, risk types and countries. From what we have seen so far in ’20, this trend is continuing.

-

Have you tried FFXDF (OTC)? It is very thinly traded. My issues is i would like to buy on the Canadian side (FIH.U) in a Can$ account but it is traded on the TSX as a US$ stock. So to avoid currency charges i have to buy in my US$ account which it picks up as FFXDF. Not sure why the company listed the stock on the TSX as a US$ stock.

-

if you compare BIAL with other publiclty traded airports around the world , it still seems quite a bit undervalued even more so with a second terminal coming up soon. Absolutely agree. That is, in part, why I was a buyer at $13, and $12, and $11. All I'm saying is this transaction is just an accounting entry - it's the same BIAL it was 2-days ago, but the shares are 10% higher and Fairfax can now charge fees again as this pushes NAV substantially higher. I get why Fairfax did it. I just don't understand why this would pop the stock or why the people buying it today weren't aware of the value of BIAL two days ago. For me, a better question is why investors sold the stock so low. At September 30, 2019 common shareholders' equity was $2,064.7 million, or book value per share of $13.53 (us). Add to that the $3.30 (us) for the current revaluation and we have book value $16.83 (us). So, if it's the same BIAL as it's always been, then the low was ~ 65% of book. With clarity on the financials coming, I think a retracement towards book value is in the cards. I'm not scratching my head as the stock recovers back up, I was scratching my head on the way down. The stock is on sale again :-) trading today at under $12.50. With the second terminal at BIAL scheduled to open next year there is more near term upside for that asset to continue to grow much more in value. Given the disconnect in where the stock is trading ($12.50) and likely reported Q4 book value ($16.50 to $17.00) it will be interesting to see how Fairfax India (and Fairfax) responds. I see in the past Fairfax India has bought back stock; perhaps they get more aggressive and use some of the proceeds from recent transactions to buy back a big chunk of stock. Or perhaps Fairfax increases its stake?