SafetyinNumbers

-

Posts

1,570 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

3-3.75b based on 1-1.25%. Fairfax might breakeven in a year like that.

-

The reason I’m so bullish is because the margin of safety is so high. Unfortunately, for my own net worth, I have historically sold as soon as a stock gets to a price where I wouldn’t buy it anymore. I’m trying to avoid that this time with Fairfax because I can see all of the ways the right tail can surprise to the upside. The focus of this discussion and the most of the analysts that cover the stock is the downside. There is almost no analysis of the returns of the non-fixed income portfolio. The two biggest pieces generate mid-high teens returns on their carrying value. That means the TRS and the rest of the non-fixed income portfolio don’t have to do much to boost returns. It’s possible FFH will get added to the S&P/TSX 60 next month as AQN continues to sit below 20bps in the benchmark (the committee might also defer to December or put TFII in instead). I assume a lot of our fellow shareholders will sell stock into price insensitive buying whenever it happens because they think the shares are fully valued at 1.2x book or wherever it ends up. Perhaps, that will end up being the right decision in the short term but it just seems so unlikely in the long term.

-

What’s the over/under on when FFH has a combined ratio of 100 or above for a full year?

-

That’s only part of the return although I do think insurance is a growth market because of climate change. I also think a lot of institutional investors that previously would have shown up to take advantage of the opportunity prefer less volatile returns so instead are in private equity and private credit. Do you think the recent large premium growth has added any permanent operating leverage for Fairfax or will it all be given back in price? What do you model for forward returns on the equity portfolio?

-

I think the assumption that returns should mean revert is a mistake because it doesn’t consider the actual balance sheet leverage, available returns on new investments and what’s already in the portfolio. I think it’s really hard to model ROE averaging less than 15% over the next 5 years based on the current outlook. Maybe you are correct, ROE will fall precipitously after that but my intention is not to sell unless forward ROE is expected to be < 10%. That seems far away for now.

-

I don’t think it makes sense to punish FFH for having a higher insurance float to book value ratio. Buffett says insurance float at a well run insurer is worth more than book value. I don’t think the relative size of it to equity should restrain that valuation as it could be solved simply by adding equity (which is what is happening as earnings flow in). The reference to past mistakes contributes to negative Social Value as opposed to any impact to Intrinsic Value. The numbers speak for themselves and the theoretical valuation exercise should remove bias.

-

It seems the relationship is actually exponential which also makes sense. 15% ROE businesses seem to trade > 2x book value and in IFC’s case 2.8x BV. Kinsale which has a 25%+ ROE trades at ~9x BV. I would caution FFH shareholders (including myself) from selling at 1.5x BV thinking that’s fair value when there is still significant growth and multiple expansion ahead.

-

There seems to be a relationship between P/B and ROE which makes intuitive sense. I interpreted Buffett’s view on book value to mean, don’t use it to estimate intrinsic value. That is if the stock is trading above book it doesn’t mean the stock is expensive and one should not buy the shares. It might indicate the business has high future expected ROE. It follows that a P/B multiple is appropriate to estimate IV because it’s based on future expected ROE. For BRK and FFH, their capital allocation decisions eventually show up in earnings. I haven’t studied BRK closely myself but it seems like investors have a return expectation of 8-10% but are willing to pay ~1.8x BV for that. IFC has forward return expectations of ~15% and it trades at 2.8x BV. Meanwhile, FFH has forward return expectations of ~15-20% and it trades at ~1.2x BV. My conclusion is that BRK shareholders have much lower return expectations as the margin of safety is extremely high. IFC has low variability in their earnings estimates which quants like which explains its premium multiple. Finally, FFH doesn’t screen well so it’s underowned by quants and most of the remaining actively managed money as they mimic quants.

-

Not throwing cold water on a potential MBO but technically they have to file an early warning report for every 2% they buy after the initial EWR when they cross 10%. The most recent purchase pushed them through the next 2% threshold which triggered the EWR and press release.

-

Waterous Energy Fund’s only holding is Strathcona Resources SCR.TO. I think FFH owns ~14.5m shares indirectly. They are supposed to report results tonight and announce an initial dividend. I own some stock as I think it’s too cheap to NAV and they are motivated to get the shares to NAV.

-

To be fair to the quants that set prices, that’s exactly what the humans are expecting to happen.

-

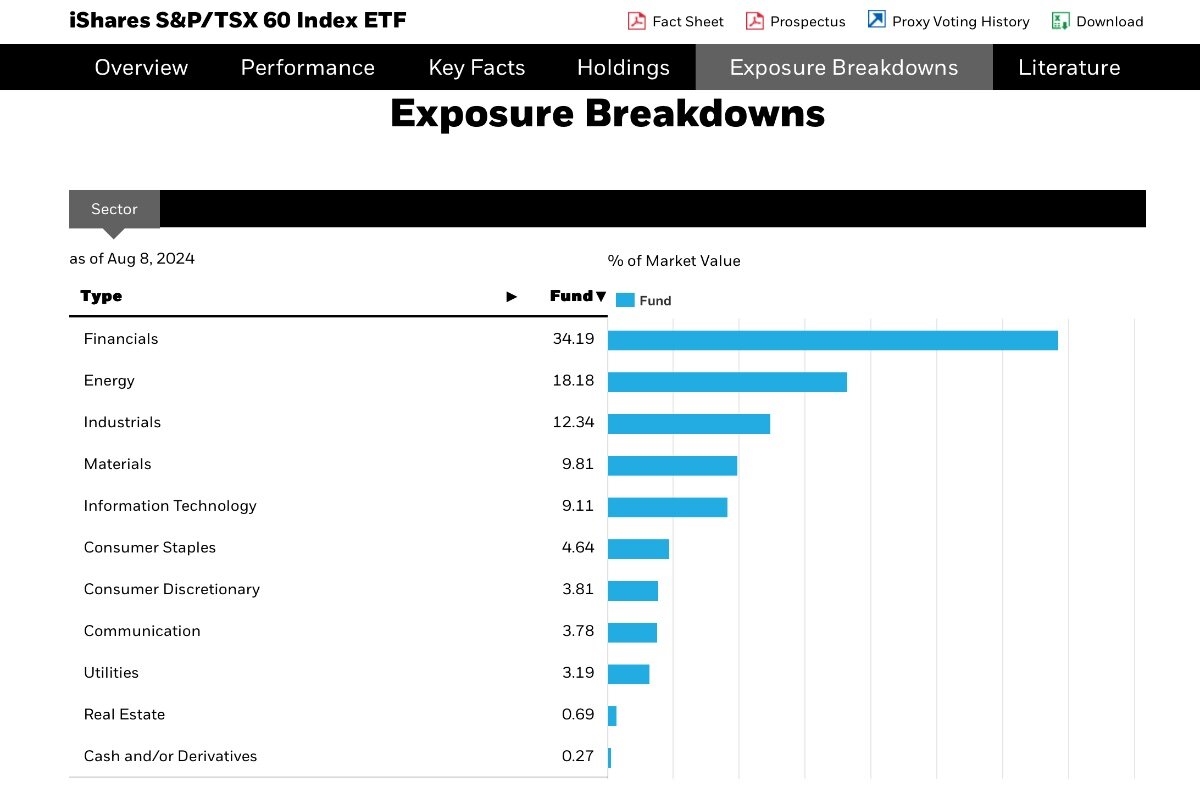

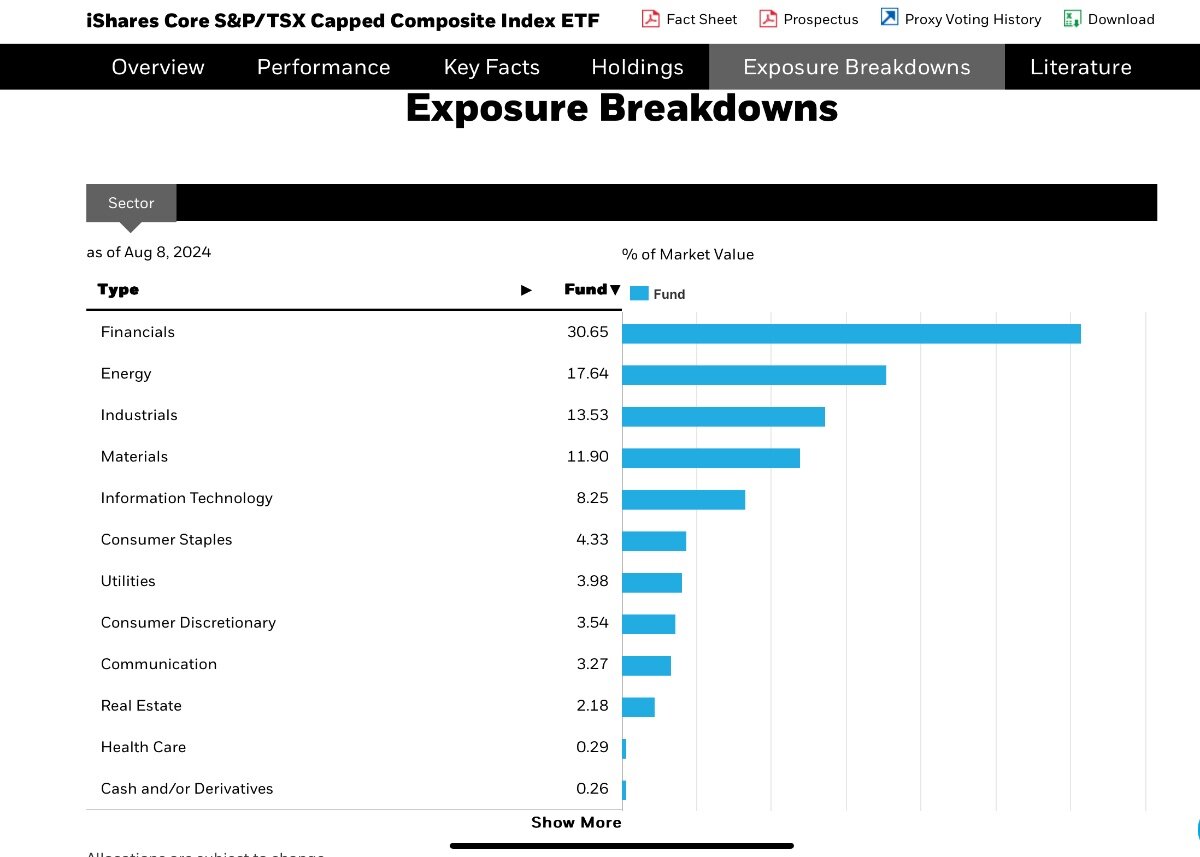

AQN is the 60th biggest component of the S&P/TSX 60 and after their bigger than expected dividend cut and more importantly lower than expected proceeds from an asset sale is now sitting right at 20bps in the index. Perhaps a bit below as of today. The index committee might have a decision on its hands if it drops below 20bps at the time of the quarterly rebalancing/measurement date which is August 31. The 20bps threshold is a rule of thumb based on previous deletions and the committee could choose not to make any changes. To be clear, even though FFH is the largest component of the S&P/TSX Composite that’s not in the 60, the committee also weighs the industry representation in the Composite vs the 60 in its decision and Financials are already overweight. For that reason, I don’t think most funds are positioned for it being added. Given, my expectation that FFH will execute well on BVPS growth for the next 5 years, I continue to think it’s only a matter of time before it goes in the index as at some point it’s too big to ignore. My bet is that a new ~4% shareholder that is buying stock every month (passive flows) will help with multiple expansion.

-

Also FFH fully monetized the position in 360 Wealth in May 2023.

-

Great podcast episode recommendation thread

SafetyinNumbers replied to Liberty's topic in General Discussion

Thanks for sharing. Did quants come up in the interview? I think they are the real price setters and passive just amplifies the move. There are lots of stocks in the index that don’t screen well for quality that seem cheap and stocks that do screen well that are not tech stocks that seem more than fully priced. -

It doesn’t make sense to do that comparison without consideration for the leverage the float provides. Fairfax has almost 3x the assets as equity. A 5% return is effectively a 15% ROE on that basis. Also, while the P/E on trailing basis might look like does not demonstrate the full economics of the transaction as FCF is significantly higher and a big chunk of that is being reinvested in the business to maintain the moat.

-

Between EUROB and Poseidon it looks like Assoicates income should be strong again in Q3 (FFH reports on a quarter lag).

-

Looks like a good sized beat on revenue, EBITDA and EPS for

-

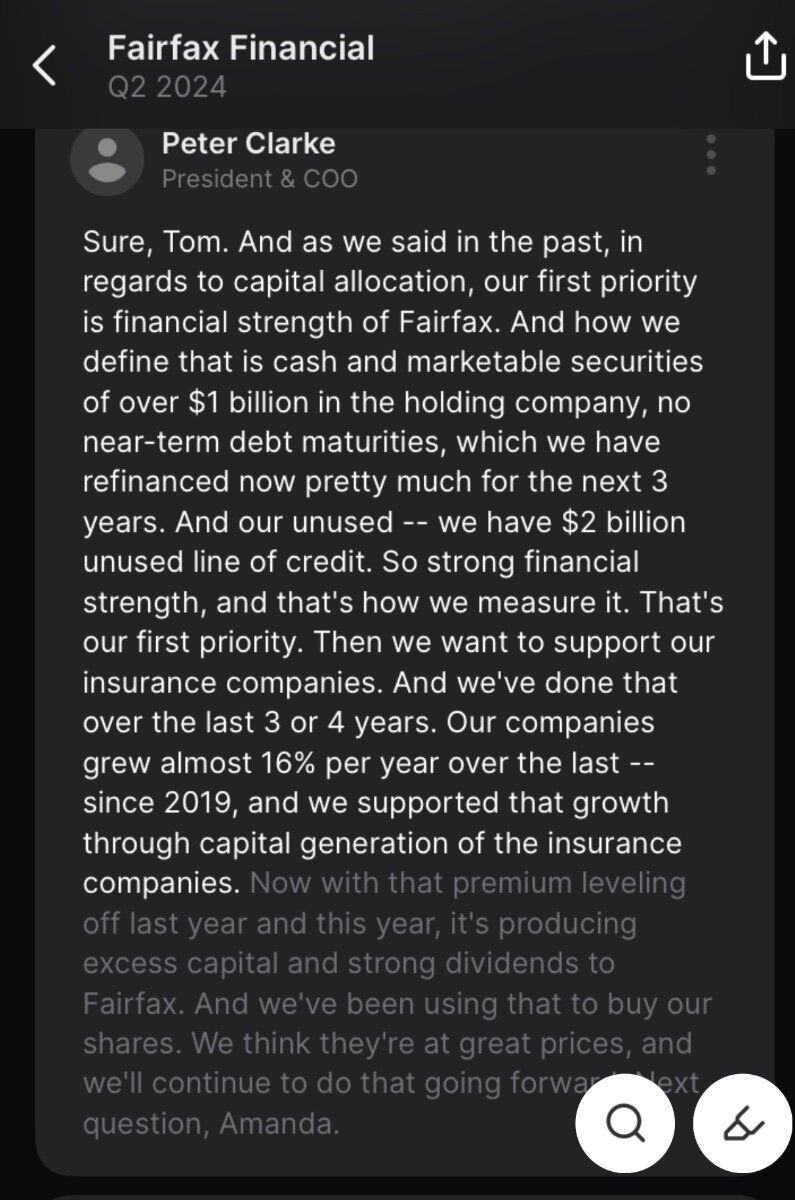

I thought Peter was pretty clear what they were doing with the excess capital not reinvested in premium growth (the non-highlighted part!).

-

I’ll add low premium growth. Had a few institutional PMs tell me it’s down because growth is down without appreciating that means excess capital is up and this is just FFH once again being tactical with capital allocation. Quants have trained the market to reward growth and so its participants are trained to chase it.

-

It shouldn’t but we have a lot of shareholders that would never buy an Indian Bank for heuristic reasons and that forces them to sell FFH.

-

Partners like FFH and other large asset managers like pensions and Blackrock types. Hopefully while earning a fee for the privilege.

-

It’s a $6b cheque. FFH will surely be contributing at least $1b.

-

The “bad” reasons why FFH is down in no particular order: -IDBI deal -ZZZ deal - decline in the interest rate curve Please add yours!

-

Looks like a 1550 top for the whole month. It doesn’t look like the stock trading under that price during the month except on those days FFH was active.

-

I think there are a few marginal traders that owned it for higher for longer and now they think that’s over so they are selling. They aren’t projecting where book value will be in five years or how understated estimates might be given low expectations for the equity portfolio or how well FFH is positioned to be opportunistic in market volatility.