SafetyinNumbers

-

Posts

2,811 -

Joined

-

Last visited

-

Days Won

37

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

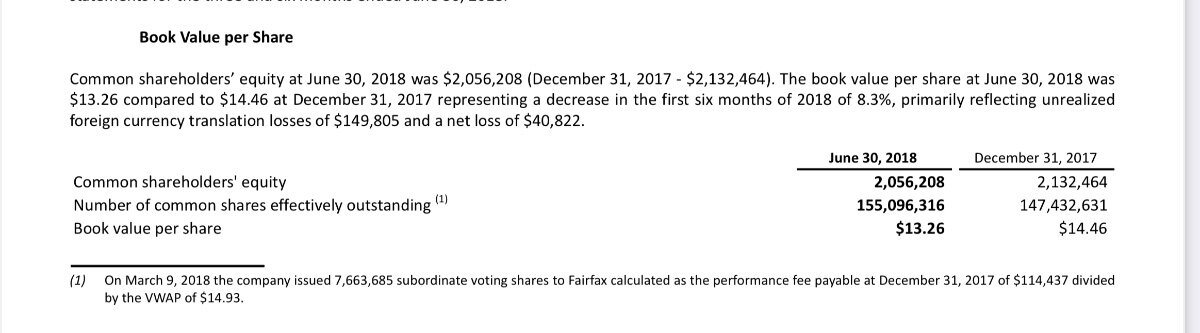

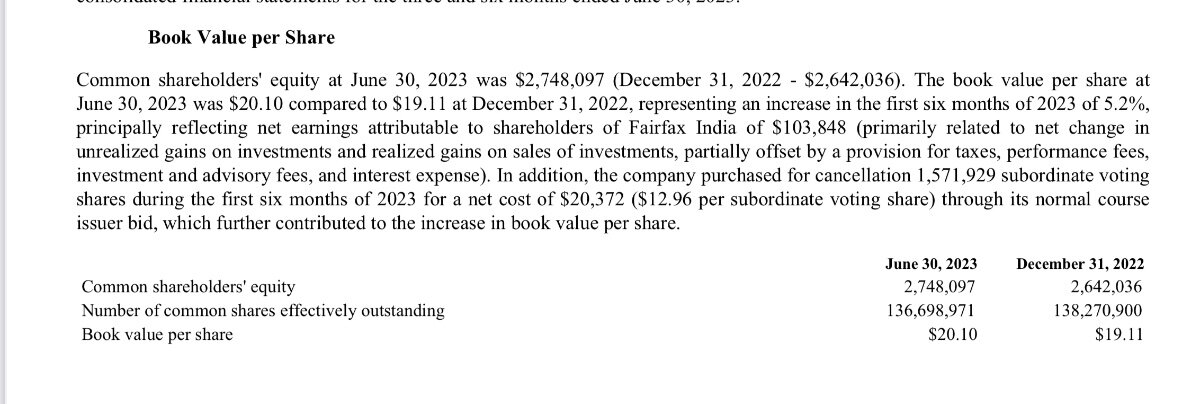

They are playing a different game but comparing prices for a fund that trades at NAV to one that doesn’t and using that to analyze management performance doesn’t make a lot of sense to me. BIAL is a big chunk of returns but actually has performed below the return on public investments. FIH is playing the public markets game better than Matthews. At June 30, 2018, BVPS was ~$13.26 and with it likely still over $20 now, the returns aren’t that different over the past 5 years. You seem to own it because you think BIAL is marked too low and I think it’s likely that’s true for the rest of private book too. On that basis FIH returns have destroyed Matthews returns and they are doing it with almost 100x more capital.

-

INDA (MSCI India ETF) just hit a new 52-week high today while FIH.U sells off. It’s a great example of nervous active investors which represent the entire shareholder base of FIH (no quants, no passive, not much institutional) trimming while asset allocators keep buying passive exposure to India.

-

That’s great analysis! Thanks for highlighting. Given Fairfax’s 32.2% is marked at US$1.77b, that contributes to ROE at 20%+. It really helps pull ROE higher. The street is for the most part ignoring earnings from the investment portfolio and they will likely keep getting surprised since it’s already too cheap based on the insurance operations alone, there is no need for reasonable expectations on the investment portfolio.

-

And they partially financed it with stock issued around 2.5x book. Trisura also recently issued equity at similar multiples. Smart moves by the management teams. It’s the easiest way to grow book value!

-

For FIH.U, the stock going sideways while intrinsic value grows used to be what investors looked for as an opportunity but now mostly everyone thinks the market is efficient. I don’t think Fairfax let investors down here. They did their job in terms of buybacks and additional purchases by Fairfax as soon as the shares started trading at big discount to BV. With the third performance fee period ending on Dec 31, I think the odds are decent (50-50 at least) we see another SIB before year end which would effectively pre-fund the performance fee and shrink the float. The group that let us down are the original institutional shareholders who negotiated the fee structure on our behalf. OMERS, Fidelity and Markel (I think) were presumably supposed to close the discount every three years so that shareholders wouldn’t risk dilution on paying the performance fee and so far they haven’t shown up (and I don’t expect them to).

-

It’s the same security whether held in Canada or the US so there are no ADR fees and no economic difference. I know for Canadians, we can get margin on the CAD ticker but not the pink sheet.

-

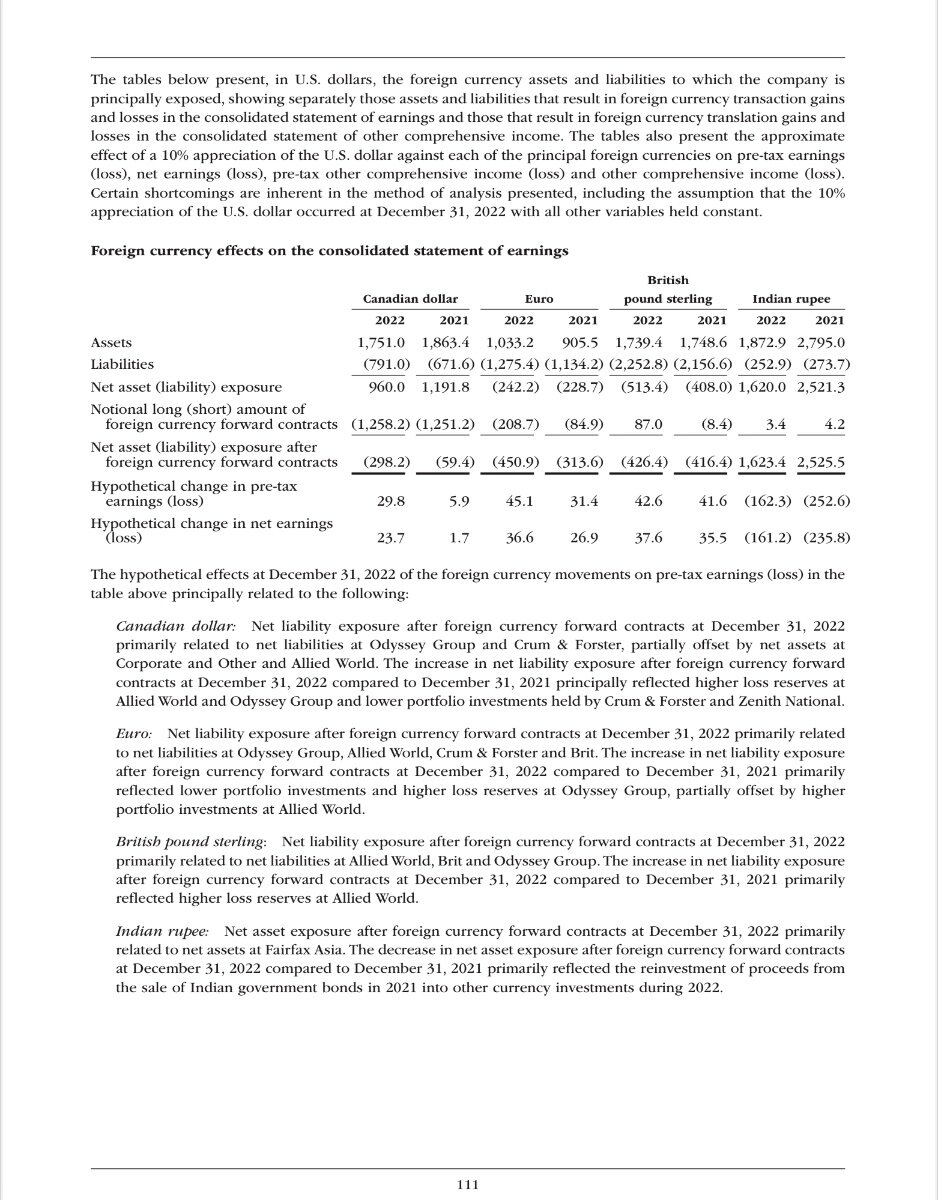

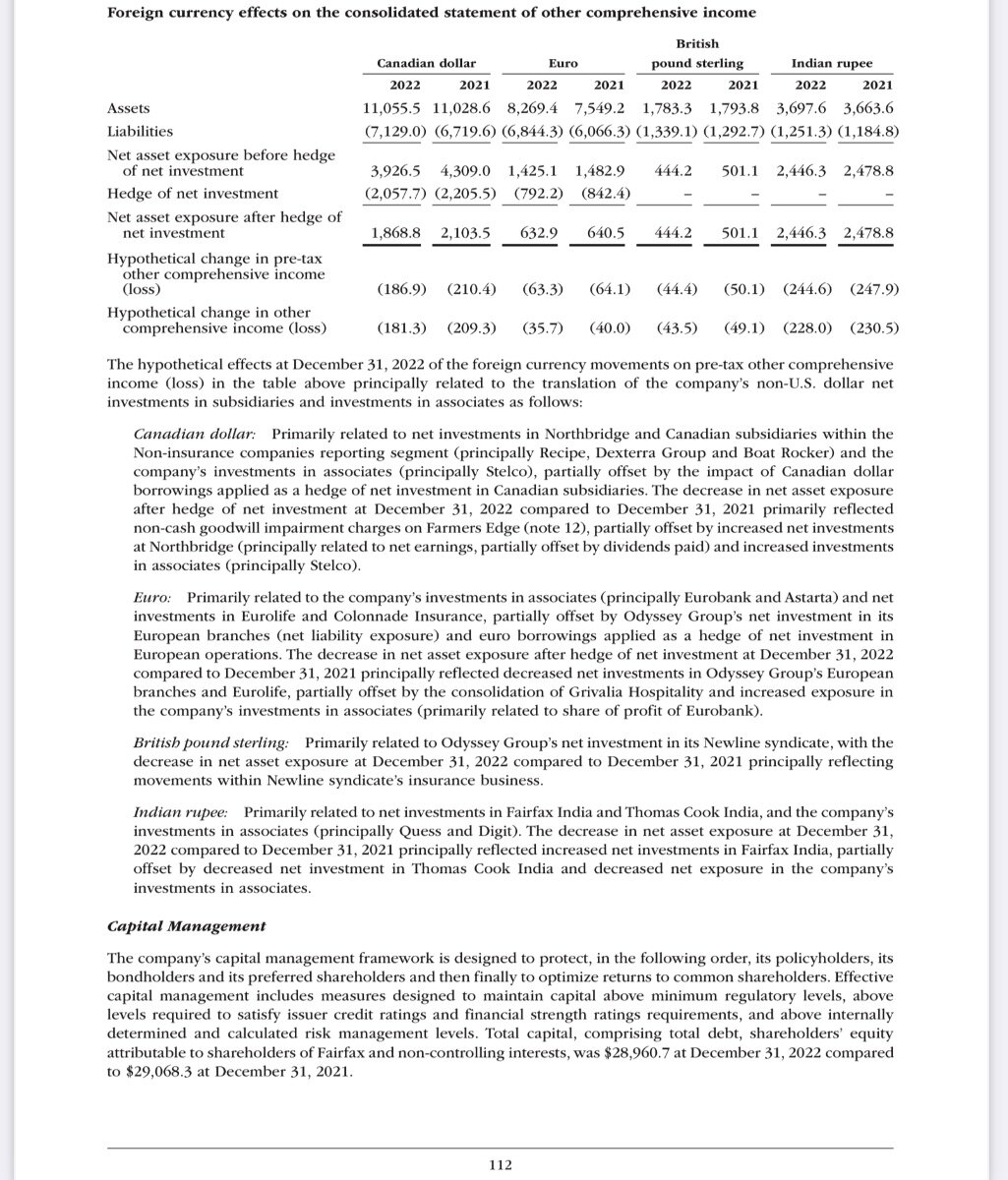

I doubt they explicitly currency hedge but there are a lot of natural hedges. This is the sensitivity analysis they provided in the 2022 AR. It must be a constantly moving target. Is currency exposure something that concerns you?

-

I think it’s an interesting example of how quants can’t analyze certain stocks because they don’t fit historical models. Perhaps lumpy 15s are more likely undervalued than ever as a result.

-

I was in equity research at UBS for a few years and continue to chat to friends who are analysts regularly. Everyone I worked with was smart and wanted to be right more than anything else. They are compensated by being right on stock performance, accuracy of estimates and most importantly client votes. The more commission a client pays, the more their votes matter. Clients also care about access to management, industry knowledge and other qualitative matters. They become industry experts because they talk to everyone in the ecosystem even though they may have never worked in the industry. That’s what gives them value to intrinsic value based investors. The advance of quants, passive and social value makes the analysts job a lot harder. Stocks can trade a lot further below and above intrinsic value for long periods of time because of passive, quant and social value flows which means anyone who sticks to valuing on intrinsic value alone can be wrong for long periods of time. That by definition makes the research less valuable for anyone approaching investing based on intrinsic value. Fortunately for them, hardly anyone approaches investing that way now. Most investors think the market is efficient and are narrative surfing. I wish I could do that. It looks like fun but I would lose all of my money without intrinsic value as a guide post. I still might. Morningstar has a totally different business model. Their analysts as far as I can tell don’t talk to management or investors. How can they be experts on anything? They don’t even do the valuation themselves. A Morningstar quant model kicks it out based on the analyst estimates which he probably manipulates to kick out an acceptable result. It’s clear from his financial estimates that they have no relationship to a reasonable forecast for Fairfax earnings. A good analyst compares his estimates to consensus and explains the differences. I doubt Mr. Horn has even thought to compare his numbers to the 6 people who are supposed to be the experts let alone to Viking (an actual expert). Probably because it doesn’t matter as the only people reading his research are discount broker clients and there is no feedback mechanism. They are still getting paid. No one who uses the product gets a vote.

-

My explanation of why Morningstar can’t understand Fairfax:

-

My ETF substitute is E-L Financial. Basically a global quality equity portfolio plus some $VOO for greater than a 50% discount to liquidation (which would take about a week).

-

The options were buying at or greater than book value or internally reinvesting. Issuing at 3x BV was what becomes available if the stock is made as accessible as possible to the largest group of investors since supply is limited. I know you will have sold by then but it’s still probably leads to better long term returns for the remaining shareholders. I certainly won’t be buying over 1.5x book but it technically could have a relatively high probability of getting to 3x given the set up. It’s all just speculation until it happens or doesn’t happen.

-

It’s not gambling, it’s just being open to the possibility given how underowned it is by Canadian funds. At the beginning of 1995, I probably would have sold at 1.5x BV and missed the 6x in 4 years as the multiple expanded to 3x while the ROE was “only” 20%/year. History may not repeat but it could rhyme. I prefer them make more equity investments vs buybacks above 1x book as it would make the company more durable which provides another reason for investors to be comfortable with a higher multiple.

-

The one advantage of trading on the NYSE is that it would increase liquidity which means we might get options listed. All of these things require inventory which means more demand for the shares at the same time index huggers are trying to buy the stock. I know people prefer buybacks but I rather issue shares at 3x book value vs buy them back at 1x any day. It’s way more accretive to BVPS.

-

Excellent post Thrifty3000. I’m trying to get people to appreciate how big the right tail could be if one of the biggest unconstrained investors in the world gets to keep reinvesting $3b+ in profits every year in one of the most inefficient markets ever. It could get even bigger if valuation gets aggressive as momentum and index huggers try to keep up allowing the company to raise equity at silly multiples. ROE’s could be 20%+ for a period of time. The narratives will of course be different but the book value growth will be real. I think the odds are decent given the high float to market cap, the expectation of lower interest rates, the high float to book value ratio and the cheap equity portfolio.

-

I object to 1x BV being froth!

-

Lots of discussion of what might happen to the downside without a lot of odds or timing included. A lot of positive things could also happen with the equity portfolio which seemingly almost no one is counting on for a contribution to ROE. I’m also curious what kind of valuation multiple the momentum and index hugging buying can take us. I’m guessing we find out post hurricane season as both buyers and sellers will be less afraid of a near term drawdown.

-

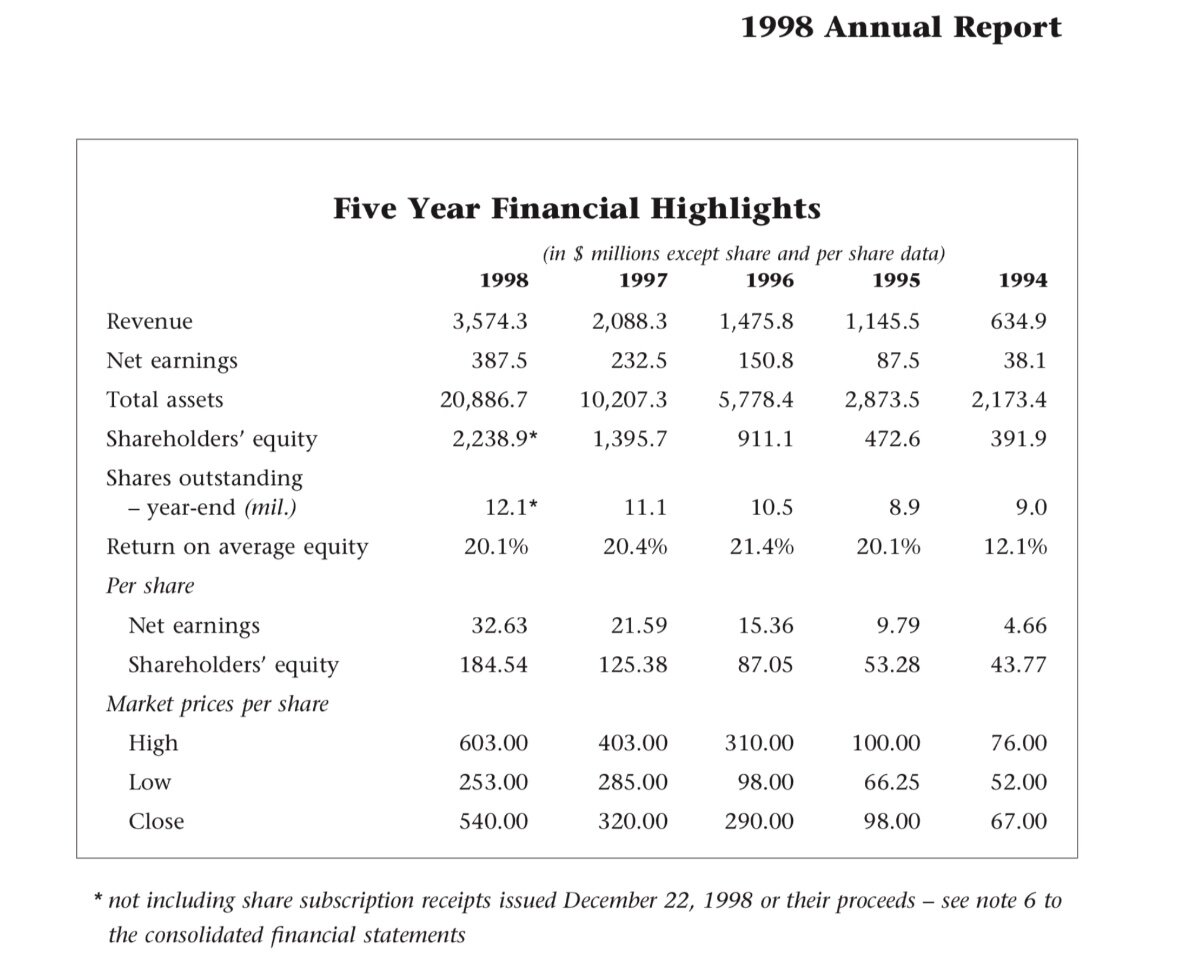

I chat with quite a few Fairfax holders and my impression is that many of them are looking for reasons to sell. I think it’s mostly to avoid drawdowns which might lead them to feel or worse look stupid. Especially to their bosses/clients if they are portfolio managers. Meanwhile, the index huggers just buy stock on VWAP so are price insensitive. Personally, I think it makes little sense to consider selling until Fairfax trades at least 1.5x book value because that seems likely over the next 5 years given how underowned Fairfax is by Canadian PMs benchmarked to the S&P/TSX and how active shareholders like ourselves see very strong book value growth over the same period. In the past three years, Fairfax has gone from 47bps in the index to 89bps. The shares outperformed the index by 170% but that was offset by growth in capitalization of the index and Fairfax’s share buybacks. It’s already very hard for active PMs not to own Fairfax given how it’s crushed the index recently but given the built in growth that I think we all agree is highly probable, if the stock just stays at 1x BV, it’s weighting will go well above 100bps and the urgency to own it will increase. It’s easy to think up narratives PM’s will use to justify paying up to 1.5x BV. They can point to comps like BRK, MKL that trade there. They can point to long term and recent ROE north of 15%. They can point to exposure to Greece and India in the equity portfolio and how cheap it is although that might be to justify paying 2x BV! I really want to avoid selling too early because I think we could be in the first year of Fairfax’s 95-98 experience where ROE hit 20% four years in a row and the multiple went from 1.5x BV to > 3x BV. Fairfax also increased shares outstanding (Singleton like) by 33% which contributed to the growth in book value from $39 to $112. These analogs are all pretty useless except they do show us what’s possible if not probable. It’s easy to hold or buy at 1x book value, it will be much harder north of 1.5x but I don’t have to worry about steeling myself until we get there. In 1995, the starting point was 1.5x BV. I don’t know if I would have been interested back then even if I had my knowledge now. That set of shareholders didn’t make it easy for the index huggers as the market cap grew from ~$800m to north of $7b. Maybe this set of shareholders is jaded enough given the last decade to hand over their shares easily but I’m trying to hold on to mine. Of course, everyone should do whatever makes them comfortable. This is not investment advice. It’s just my thought process for which I welcome criticism.

-

How many years in that table depicting growth in BV was the float 2x the BV?

-

What if the equity portfolio returns 5-10% per year on average for an indefinite period of time? Wouldn’t an ROE of 15-20% be achievable then even if combined ratios inevitably go higher?

-

I think this take on Brit and Allied ignores that Fairfax issued stock at 1.3x book plus and issued preferred at tight spreads to partially fund these acquisitions. Singleton is a legend not only for the buybacks below book but for issuing stock early on well above book to grow the earnings power of the business. Call it towering ego if you like, I call it accretive capital allocation.

-

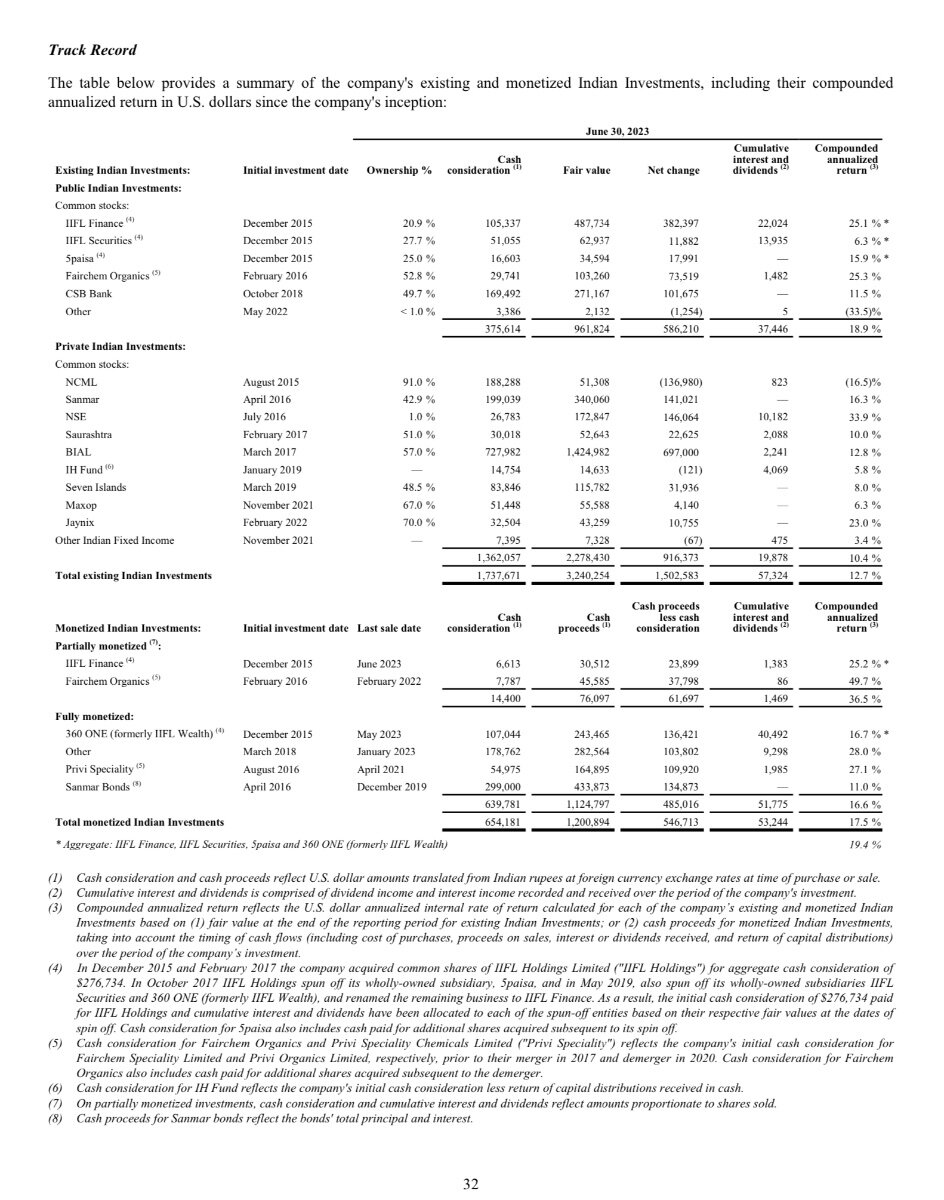

James East pointing out over on Twitter that FFH seems to have sold a big portion of its direct stake in IIFL Securities while FIH.U continues to hold. I think FIH.U likely announces an SIB by year end as they have the cash, have taken a break on the NCIB for two months already and need to pay the performance fee at year end. In 2021, they announced it on June 15. If it ends up being a reasonable analog then maybe Sept 15 is when we should expect an announcement. https://x.com/acipartnerhship/status/1692192406903365930?s=61&t=o1MAr_q6CYLyhGegyE3GdA https://t.co/wnlzyCWQcn https://www.fairfaxindia.ca/press-releases/fairfax-india-announces-us105-million-substantial-issuer-bid-2021-06-15/

-

Float to market cap and float to BV would also be an interesting comparison over time and currently vs peers.

-

The best part about is that they could do it without putting any new cash in using Stelco’s cash on hand and some term debt.

-

I can tell you exactly how something like Morningstar happens. They are paid directly by discount brokers who by settlement post the dot com bubble have to provide research. Morningstar having a good brand name adds a new business line selling equity research. Because they are quants, they use their models to come up with target prices and earnings estimates. The analyst then just has to write a narrative to support the “AI” valuation. With ChatGPT, maybe AI is writing that too. Every analyst covers a lot of companies and probably gets paid very little. He covers a lot of companies. He can’t be an expert. At the crux of it, quants can’t value a lumpy 15% very well. They don’t understand the business model and the structurally high ROE. All they do is look at history and weigh the recent history extra because that’s what works for the rest of the stocks in their universe whose businesses are more predictable. It doesn’t matter by the way that it’s bad at valuing Fairfax in particular. I think regulators should look at banning this type of research because individuals read it and think that it’s Fairfax specific research when in fact it’s a snippet of a big data project that is being shared with an individual in a more personalized way via the analyst narrative. A fund managed based on that quant strategy might still beat the market! It’s a big reason why an obviously cheap liquid company like Fairfax can stay so obviously undervalued when everybody has the same information. The number of active managers has diminished significantly in the past 20 years and the ones left for the most part are good at hugging the index and/or using quant screens to pick stocks. They might as well be following Morningstar research because their quant screen knocked Fairfax out of consideration. None of this should be surprising. If passive and quant based funds are taking all of your assets it makes business sense to mimic your peers. It’s a very hard job. I know I would find it very difficult to make money with those constraints. That’s a big reason why I don’t do it but if I found myself needing a job I might give it a shot! I would try to find an unconstrained seat first of course! Frankly, I don’t think there has been a better time for unconstrained investors in decades. It’s one of the reasons I’m so bullish on Fairfax. They are an unconstrained investor with the potential to make 10%+ returns on the equity portfolio while the fixed income portfolio is making 5%. That all translates to 20%+ ROE potential. Viking’s brilliant well written post above spells out how easily that can happen. Buying insurance subsidiaries at < 10x earnings is also a 10%+ return on investment. I think selling 10% of Odyssey at a premium valuation to fund the SIB was a Singleton move. When I talk to investors about Fairfax, the focus is still on the downside and I fear that’s why there is selling at these prices on a daily basis. People are worried about a near term drawdown which could absolutely happen and likely will but that has nothing to do with intrinsic value. I know a lot of people are hoping for more buybacks but I hope Fairfax keeps making buying what they know (Stelco could be next) and making the company more durable. That will make it easier for shareholders to hang on and worry less about drawdowns. That will gives Fairfax a much better chance of a premium valuation as the index huggers and momentum quants keep buying which I’m sure Prem will use to issue equity (Singleton!) and increase book value that much more When I was in UBS Equity Sales as a desk analyst, one of my bosses clients gave me the nickname “The Dream”. My boss actually said he gave me the nickname but as a 27 year old kid at the time I remember thinking it was awesome that a hedge fund manager running billions of dollars knew who I was. He didn’t know my name though which is why he called me The Dream. My ego took it like I was at a Hakeem Olajuwon level but in reality he was just referring to my propensity to figuring out the narrative where everything goes right. At the time we were trading a lot of risk arbitrage and event driven trades so some creativity was helpful and paid off big time as there was a lot of money to be made in 2004. To that end, I’m clearly focusing on what could right for Fairfax. I think that’s an important part of the expected returns and focusing on the downside might make me let shares go too early which I will almost certainly will regret doing.