treasurehunt

-

Posts

387 -

Joined

-

Last visited

-

Days Won

1

1 Follower

.thumb.png.e9643dd797bb6bfa93083ce1311ba74d.png)

treasurehunt's Achievements

")

-

Very interesting interview; thanks for posting. So according to Li Daokui, policymakers' goals are clear even if specific policies might be issued only over a period of a year or two - swap out local government debt for central government debt and increase domestic consumption mostly by incentivizing local governments properly. Good to keep this in mind.

-

I really like this idea. There will probably still be gray areas and room for different interpretations, but at least this is an attempt at an objective analysis. There seems to be this view that government bureaucracy is so bad that doing something - anything - can only be an improvement, regardless of what this something is. I disagree. Having lived in another country for a good part of my life, I can assure you that government bureaucracy could be much worse. So it is important to examine the actions that are being taken to make government more efficient and the consequences of these actions.

-

I bought my first B shares in February and March of 2000 for right around $1,500 per share. Still have those, although I have sold some that I bought later.

-

Sold some BYDDY. BYD is executing very well, but a P/E of 25 for a company that faces intense competition in all its verticals seems rich.

-

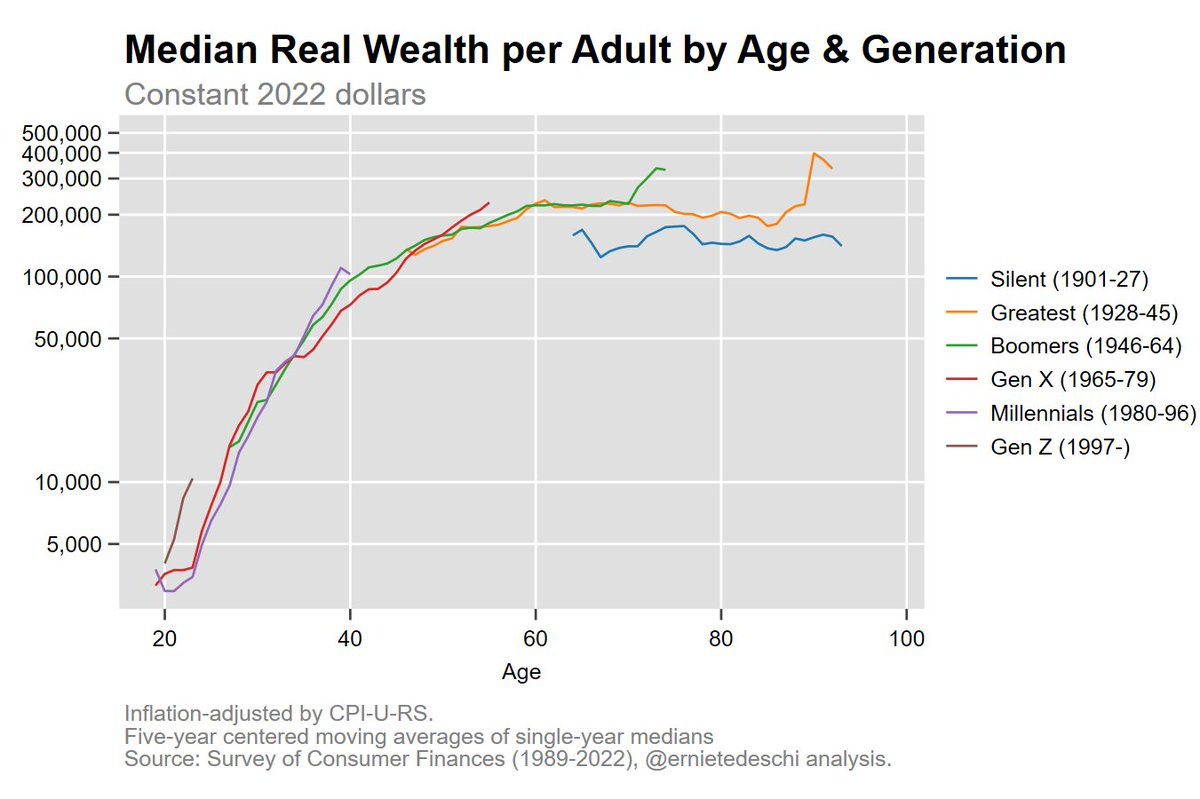

I have cut and pasted the chart below. It was posted on X by Ernie Tedeschi, former head of the White House Council of Economic Advisors. Anyway, this chart maps inflation-adjusted median net wealth (assets - liabilities) versus age for Gen Z, Millennials, Boomers etc. And by this metric, Gen Z and Millennials are doing better than Boomers. Your data uses different metrics - percentage of total wealth owned by people under a certain age, wealth as a percentage of disposable income etc. Arguably these metrics are better at gauging how a generation is doing financially. I think it is accurate to say that Gen Z own less of the total pie than Boomers did at the same age, but today's pie is much bigger in real terms.

-

Is it?

-

I don't think BAC is particularly cheap now and for me over time it had become too small a position to bother with. So I sold. There was no company-specific reason for my sale.

-

Sold the last of my BAC. It was a very nice run from 2011 till now. Thank you, Brian Moynihan!

-

Added to my Prosus and Tencent positions. Only a nibble though.

-

Amazon's Kuiper might be a viable competitor although they are way behind schedule at the moment. Apparently, half the Kuiper constellation has to be in place by July 2026. https://spacenews.com/beta-project-kuiper-broadband-services-pushed-to-early-2025/

-

Well, big banks such as BAC and JPM are quite constrained when it comes to growth, I think. EWBC has a chance at growing faster than these behemoths. But the main reason I kept EWBC while lightening up on BAC and JPM is that it is not as overvalued as these two in my estimation. Defining IV as the price where I can expect a 10% annual return going forward, I have BAC valued at $36, JPM at $200 and EWBC at $105. Of course it is entirely possible that my estimate of IV is off by quite a bit. Also, take a look at past growth in book value per share for these banks (I use growth in BV per share as a proxy for growth in IV per share). Annual Book Value Per Share Growth BAC JPM EWBC Since 2013 5.11% 7.44% 11.48% Since 2018 6.12% 8.95% 10.89%

-

Interesting. I too bought EWBC last year after SIVB went belly up, but haven't sold any yet. I have lightened up considerably on other US banks - C, JPM, BAC, GS etc - since I have about 20% of my portfolio in this sector.

-

Milton now up to Category 5! I hope it weakens before landfall and spares the more populated areas in Florida.

-

My biggest buy in the last three months is PROSY (2% of portfolio). Second biggest is HQI (1% of portfolio).

-

The Economist has jumped on the solar bandwagon with both feet. They are predicting a future (some decades out) of very cheap electricity, quite the opposite of an electricity crisis. I think the articles are behind a paywall, unfortunately. https://www.economist.com/leaders/2024/06/20/the-exponential-growth-of-solar-power-will-change-the-world https://www.economist.com/interactive/essay/2024/06/20/solar-power-is-going-to-be-huge The Economist doesn't really address seasonal fluctuations or problems with long duration storage. On the other hand, solar electricity production is only 6% of total global electricity production, so there is some time to solve these issues.