Parsad

-

Posts

16,250 -

Joined

-

Last visited

-

Days Won

64

Content Type

Profiles

Forums

Events

Everything posted by Parsad

-

Probabaly! The analysts have an average target price of $569 CDN. They'll talk to Prem on the call tomorrow and then raise their target prices early next week. I would imagine the current high target at $626 CDN will become the new average target price next week after the stock overshoots the current $569 CDN average target price. That's how it works sadly! Cheers!

-

Their average cost on the buyback in Q2 is $50 USD per share higher than where it is presently trading. I would expect them to be buying back shares tomorrow and next week if they are allowed (no blackout), and the stock doesn't jump $100 per share. Absolutely no reason why the stock shouldn't be trading at $640 CDN or better. Above the current highest analyst target of $626 CDN. Cheers!

-

Should surpass $600 USD a share by the end of the 3rd Q in book value. My average cost was $450 CDN, but it has risen to about $485 CDN after adding 33% more to my stake last week and this week. Cheers!

-

And all of this with certain businesses still struggling and recovering like BIAL, Recipe, retail businesses, etc. $19B in cash firepower ready to do some damage in bonds and equities when the opportunity arrives. Then finally you have the total return swaps on the FFH shares...what are the gains if they hit $850-900 CDN per share by 2025? Based on 3rd Q book, even if you mark their shares at 0.85 of book value as presently they are...you are talking about $630-640 CDN per share now. Trading at book now would be $735-740 CDN. Could be a homerun like the CDS investments in 2009 by 2024-2025! Cheers!

-

Just killing it! The two best turnarounds I've seen in the last year have been Handler at JEF and Prem at FFH. Nearly doubled Viking and my expectations! Nice job Fairfax! Cheers!

-

+1! Cheers!

-

Ok, my friend Andrew Wilkinson was an early investor in Shopify...so I've known about Shopify for a long time and followed it. But the valuation was always a huge problem for me. I wasn't making fun of it or anything, but I couldn't and still can't accept the probabilities that it can continue growing at the rate it does and that any investment will be worth that risk. This is the problem Prem has...and to a lesser extent Buffett has. Prem was happy to buy a mature GOOG, as did Buffett with AAPL. I had no problem buying AAPL shortly before Buffett did. So that's the first problem. Second, whether it's Shopify, AAPL or as I did with OSTK, if the P/E jumps over 40...I'm out! That's just my nature, and I find it distressing to hold onto positions that become fundamentally expensive. Meanwhile, my friend Andrew keeps increasing his net worth by the ten's of millions every quarter. He's built that way! I'm not. Incidentally, Andrew is a keen student of value investing, owns Fairfax and Berkshire...but he's built differently...maybe he's the next evolutionary step for the value manager of the future! Cheers!

-

If only we could...if only we could! Cheers!

-

Eric & Greg, do you guys own Shopify?

-

I fully agree with this. I wish Fairfax was capable of this...but they aren't. Doesn't mean it isn't a great investment from time to time. Nor does it warrant the denigrating comments by many about Prem. He's built a friggin' empire from nothing...copying Buffett's wheel to the best of his abilities...at 18% compounded since the beginning. If he can do it at 15% for another 25 years...it may not be Berkshire, but it would be closer than almost anyone else. That deserves a bit of respect in my opinion! Cheers!

-

ORI is more of a general insurer and does a lot of title insurance...as far as I know, they do very little, if any, reinsurance. Quite different than Fairfax...more comparable to First American or Fidelity National. They will do well most of the time and then get killed when housing corrects. It is more stable than FFH and most other reinsurers. It will get you a steady 8%-9% over time, but it will never do 14%-15% ROE simply because it isn't as leveraged...4-1 versus 6-1. Cheers!

-

All these transactions have to go through Ontario's securities exchange and the TSX legal department for approval before Fairfax can move ahead with the transaction. For example, even with us, when PDH does anything like loan capital to subsidiaries, transactions with parties that are not arms length, etc., our legal counsel needs to send a letter to the BCSC and TSX for approval. That means before Prem does any of the above transactions with related parties, it went through Paul Rivett (President), Peter Clarke (COO and compliance), the OSC and finally the TSX. So to blame Prem solely for any lawsuits seems to be a bit of a stretch. Yeah, he's the CEO, he was the star witness, so he gets the blame. I'm not saying they were in the right. If the judge says they were wrong, then they were wrong. But there are more voices and hands in these decisions than just one person. By the way, Buffett had his similar run-ins as well. The SEC investigated Berkshire and Buffett when they acquired Wesco and they paid a $115K fine. They also had a similar run-in when they acquired the Buffalo News and anti-trust charges were filed. Buffett also got dragged into the middle of the Solomon's failure and GenRe's dealings with AIG on finite insurance where they paid a $95M fine...neither of these were Buffett's fault, but he was CEO when the problems happened. Cheers!

-

-

Me neither. I don't think Prem knows either. But I'm often pretty comfortable with the ones I know are 90%...and I'm guessing Prem does too. You and I made two substantial bets at the same time...ORH Preferreds being bought back by ORH...that looked like a 90% winner to me, and I'm guessing you felt similarly. The other was our bet on BAC...which we both did extremely well on (you just killing it)...but I would say at the time, that was a 30-40% probability of success. Again, going back to an insurer...which bet would they make in a big way, and which would they maybe bet smaller on? Using that example, I do agree with you, Prem could make a number of smaller bets on some growth stocks like they did with GOOG, instead of the large single bets like on a BB. Maybe base hits is what investors want to see more of rather than the occasional homerun. Food for thought for Hamblin Watsa! Cheers!

-

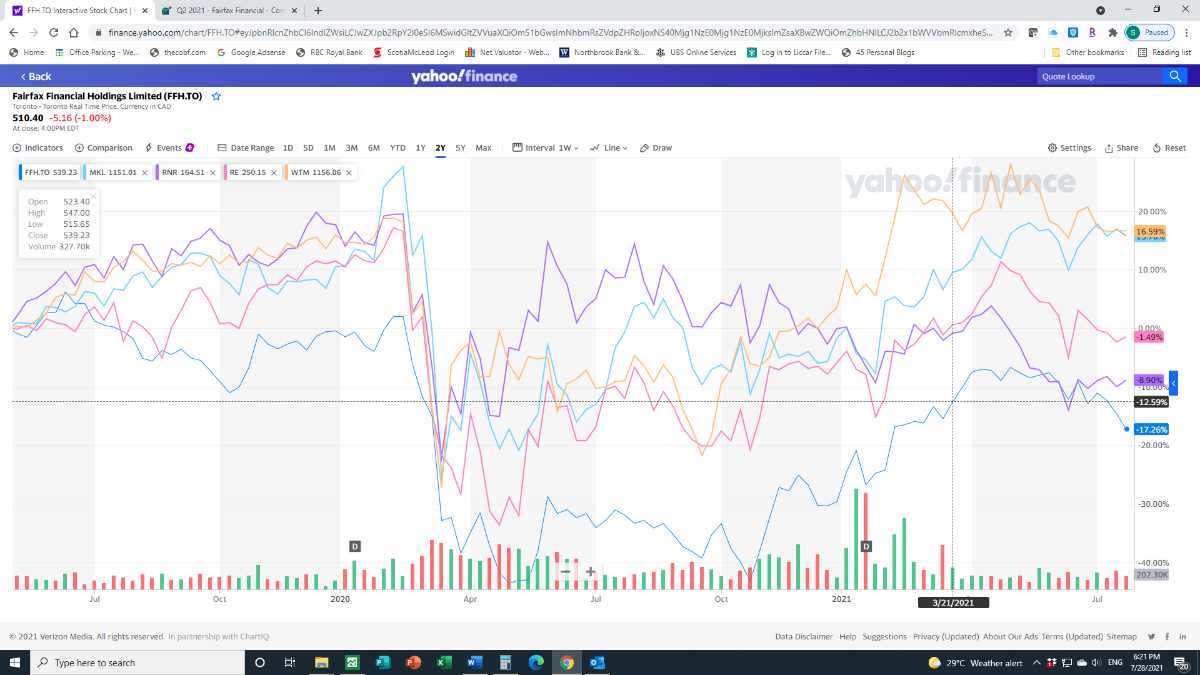

Looking at the chart below, we don't really need a catalyst. As we can see, the main competitors for FFH were priced similarly pre-March 2020. Then you had a substantial drop where Fairfax was hit the worst and then Everest Re. White Mountains, Renaissance Re and Markel got hit about the same. White Mountain and Markel have essentially recovered. Everest Re has recovered much of its loss. Renaissance Re and especially Fairfax have a much more substantial distance to go yet. Thus in an insurance industry where all insurers are doing good business and writing 20-25% ROE's I would imagine the market will automatically close the gap between them as institutions and funds reach for yield in a mature stock market. Cheers!

-

Would you rather own a 40x P/E company with the probability of growing at 25% a year for 10 years being 30%, or would you rather own a 10x P/E company with the probability of growing at 10% a year for 10 years being 90%? Essentially, this is what it comes down to if you are Prem. He wants certainty, a margin of safety and a high probability of success...not high returns with high risk. And with the leverage they utilize, they don't want to see a 40-50% drop in their equity portfolio (for those that argue about just owning SPY), which reduces their ability to write insurance business. We all know that with leverage and float, they only need to hit 4% on their investment portfolio to surpass a 15% ROE if the insurance subs are writing good business. Cheers!

-

+1! And yes, I did buy a ton when they were in the toilet...and not just FFH. But I continue to buy more FFH even now, because it is relatively cheaper than most other stocks. Cheers!

-

I thought I would start a new thread in preparation for tomorrow's release. I'm expecting about a 5% ROE based on everything I've been reading from other insurers and reinsurers...so book somewhere around $520-525 USD for Q2. That's on top of any gains from Digit that would be recorded in the 3rd Quarter...which should round book to about $600 USD assuming similar gross premiums written and a $60 gain on Digit. Ending Q2...stock should be about $650 CDN based on book. Ending Q3...stock should theoretically be valued at $750 CDN based on book and peer valuations. Cheers!

-

No one understood it then. To imagine that a money manager could have the foresight to invest in MSFT because of the development of Azure is like imagining a money manager to be able to pick the winning numbers in the lottery. Especially a value investing money manager who would sell the stock every time it got to a 35-40 times PE. Even Buffett, who is best friends with Gates, didn't have that insight. Also, it's not always we mock what we don't understand. Competitive behavior and market forces can help or kill any business. Look at Beta and VHS...the better idea went the way of the dodo because of the porn industry. AMZN would have lost if Barnes and Noble simply added porn as one of their offerings! Cheers!

-

I agree with you that I wish they had monetized their BB holding somehow. But I'll defer to Prem to see if there was anything legally holding them back. If not, it was a lost opportunity! That being said, if they see BB being worth far more than $20 a couple of years down the road, I'm ok with that. Although it would be nice to hear them say that. Cheers!

-

No one was buying MSFT when Ballmer was running it. MSFT went sideways from 2001 to 2014...it's only now with the changes Satya Nadella has implemented and restored growth that everyone wants to own it again. Cheers!

-

+1! Cheers!

-

It wasn't their investments like BB that lowered returns. It was their shorts and bets against the market that limited their investment gains. What about Atlas Corp...what about KW...and STLC. The cost of BB is now well below the market price. If it gets taken out by someone at $20+, it will be a pretty good investment...and it's likely it will get taken out as they continue to secure more contracts and deals. Africa didn't turn out well so far, but it's based on the same playbook that built Fairfax Asia and Fairfax India. The only insurer in recent history that has grown like First Capital (Fairfax Asia) is National Indemnity...that's pretty damn good company! Cheers!

-

Market Disconnect is One of the Craziest I've Seen in 23 Years!

Parsad replied to Parsad's topic in Fairfax Financial

Three important things here: - The insurance subsidiaries and operations between 2000 and 2010 were subpar to the likes of WTM, BRK, MKL, WRB, etc. Different story today. - Fairfax spent too much time on macro issues...made them money in 2009/2010, but cost them even more between 2012-2019. Different story today. - One of the most studied periods by Fairfax's team was Japan circa 1980-2000. They've seen what happens to insurers in low interest rate environments. I think they will do better in this environment than most of their peers. I'm not going to lie to you. Other than my taxable account, I've never held Fairfax from 2000-2020. I've never held Berkshire consistently during that period. I don't fall in love with stocks, no matter how much I admire the operations or manager...I put focus on the value of my portfolio...there is no forever hold stock for me. But the periods when I've held these stocks, I've done very well and I believe we're in for another period where Fairfax will eventually be priced 1.15-1.25 times book. Cheers! -

Market Disconnect is One of the Craziest I've Seen in 23 Years!

Parsad replied to Parsad's topic in Fairfax Financial

Just goes completely against the grain with me. I'm ok with easy money, if it is fundamentally easy money...buying in March of 2020...buying in late 2008/early 2009...buying value stocks in late 1999...buying Overstock at 0.1 of sales...buying WFC because everyone hates it at 0.6 times tangible book...buying JEF at 0.5 times tangible book...and buying FFH at 0.6 times book. But the other easy money today...other than buying a ton of puts on AMC at $67...or a certain Greek bank at 0.2 times book (no, not Eurobank)...not the type of stuff I can hold any conviction for. Cheers!