Parsad

-

Posts

16,250 -

Joined

-

Last visited

-

Days Won

64

Content Type

Profiles

Forums

Events

Everything posted by Parsad

-

Best options for buying Indian or Pakistani mangos

Parsad replied to rogermunibond's topic in General Discussion

In my 50 years of eating mangoes, this has never happened to me once...perhaps, because I live in frigid Canada! Is this a naturopathic anecdote/symptom? Or is it like that episode of Seinfeld where George eats a mango, and his testosterone jumps ending his short-term impotence! Cheers! -

The question is, were the hedges removed at a time when they would have been most valuable? with a ton of cash and short-term bonds, I think they are ok. But I'm not entirely sure removing shorting altogether was the best idea. Cheers!

-

Isn't this the refrain of every bubble? It's a new era, generational change, game-changing, the future! I'm a huge proponent of blockchain technology...have been following it longer than 99% of crypto investors...so I'm certainly not blind to the technological change. But the functionality, utility and volatility of the current crop of crypto leave me bewildered regarding how confident people are that these are investable. Combine that with the fact that there is nothing backing the current batch of crypto...no tax revenues, no assets, no cash flow generation, absolutely nothing. If ever there was a fiat currency, I would imagine crypto is it! Even tulips could be planted and new bulbs sold for pennies. What the hell will people do with wallets full of crypto when the bubble explodes? And it's this explosion that concerns me. How much capital will be destroyed (I would imagine at least $2.7T - 99%). Are certain companies, institutions and national balance sheets holding some of this potential risk that could create a systemic issue? The internet bubble destroyed about $6T in capital...the housing bubble of 2008 destroyed roughly the same. Maybe we have some ways to go before we see the crypto craze collapse based on the damage done during those bubbles! Cheers!

-

With more and more people jumping on the crypto bandwagon, and some institutions/countries partaking in some form of participation in cryptocurrencies, is there a possible underlying systemic risk from potential losses that regulators aren't noticing? It's starting to feel like deja vu...we've seen new tools, instruments rise and create systemic risks as participants clamor for the new thing. Junk bonds, CDS, ARM mortgages, etc...is crypto the new financial nuclear bomb?! Cheers!

-

I spoke to Francis today, and he said the specialty lines aren't increasing much, but reinsurance is very strong. So I would imagine that Fairfax's reinsurance businesses are going to continue to do well into 2023, but their more generalized specialty lines will not benefit nearly as much. Fortunately, they do a ton of reinsurance! Cheers!

-

Movies and TV shows (general recommendation thread)

Parsad replied to Liberty's topic in General Discussion

Yes, you can see the definite connections to David Lean's work in Dune. But all artists steal bits and pieces from other artists or are influenced by them. Cheers! -

Movies and TV shows (general recommendation thread)

Parsad replied to Liberty's topic in General Discussion

I think GOT was so good, because the producers and writers were able to take their time and tell the story...granted, I'm still pissed off about the ending, and I'm waiting to see how Martin ties up things in the final books. LOTR under Jackson and Dune under Villeneuve...two very different styles...and I agree with you it's because of the source material. That being said, I think both were amazing. Jackson's movies, like the original Star Wars trilogy would appeal to a wider base than Villeneuve's Dune. Cheers! -

Movies and TV shows (general recommendation thread)

Parsad replied to Liberty's topic in General Discussion

The book was one of my favorites, but it isn't easily digestible for most...especially if you've seen the Lynch version of the movie...which I actually thought was pretty good, but probably not most people's cup of tea. Villeneuve takes the political/Shakespearean atmosphere of Lynch's version and Herbert's book, but makes it more relatable to current or even past world events...not dissimilar to what Benioff and Weiss did for Game of Thrones...just on a much more massive scale. Combine that with stunning visuals and cinematography, fantastic character development and actors, and you have an epic powerhouse that could become like the Star Wars movies. If it wasn't for the pandemic and theater restrictions, this thing would be on it's way to making over a billion dollars. Just blown away by how good it was! Cheers! -

Movies and TV shows (general recommendation thread)

Parsad replied to Liberty's topic in General Discussion

Just saw Dune! Absolutely magnificent! So good, it might be the first sci-film to win an Oscar...which should have gone to Kubrick and 2001 or Close Encounters of the Third Kind in my opinion. Villeneuve has crafted a masterpiece that I think most viewers will want to see over and over. I'm not sure how I'm going to wait 2 years to see the 2nd half. By the way, it's almost certain that Dune 2 was greenlit from the beginning, and Villeneuve was going to get to shoot both 1 & 2 based on how this ends. Man, where was Villeneuve for the last three Star Wars, and too bad Timothee Chalamet wasn't the same age as Hayden Christensen. He would have made a perfect Anakin. Just couldn't get enough of Dune! Cheers! -

Movies and TV shows (general recommendation thread)

Parsad replied to Liberty's topic in General Discussion

I would imagine that they've already planned to announce the project, but are waiting to see what the box office numbers look like. They aren't going to give Villeneuve another $165M unless Dune is on target to make $500M+ globally. They should break $200M globally after this weekend. If it bombs, they may want to pull the plug, which would not happen if they made the official announcement already. Dune is not Star Wars or Star Trek...not even LOTR. It's a much more acquired taste. That being said, I think Villeneuve is probably the guy to make it a much larger franchise on par with those other sci-fi/fantasy stories. The global numbers look good so far...it's all up to the domestic audience to guarantee its future. Cheers! -

My point was that at least Prem's kids have a business background, asset management skills and have studied finance. In either case, as both CEO's have long stated, their children are to act as surrogate stewards for them, maintaining the culture and legacy...not necessarily day to day operations. I'm inclined to think that's a good thing if the offspring are anything like the parents. I know Ben and Christine much better than I know Howard and Susan...that being said, my interactions with all of them have always been very cordial and while they may not be the leaders their parents are, they are certainly their parent's children in ideals, virtues and beliefs. Cheers!

-

For those critical of FFH's board composition with two of Prem's children, how do they feel about Berkshire's board now retaining two of Buffett's children? https://www.barrons.com/articles/berkshire-hathaway-names-warren-buffetts-daughter-and-money-manager-chris-davis-to-its-board-51634767965?siteid=yhoof2 Cheers!

-

...which is now closed. Cheers! https://finance.yahoo.com/news/big-short-investor-burry-says-215758318.html

-

I don't know, is it? In case it's hard to tell by the chart, the return from October 2006 to May 2010 was 243%, while the S&P500 was essentially zero. Yes, results were juiced by CDS, but you don't need juiced results to get to 100% in two years from today. Especially since the stock was trading above book value at the end of 2006 and slightly below book value mid-2010. We're starting at 0.7 times book now...that's nearly 50% of upside without any additional growth in book. Like I said, barring any massive catastrophe or market meltdown, things look good for Prem and FFH. Cheers!

-

No, you need to make clear what you are saying. You insinuated that the sale of the UK runoff was due to capital requirements and banker's debt requirements. In the December 2019 press release where they announced the 40% sale of the UK runoff to OMERS, Fairfax clearly states that: Upon completion of the transaction, Fairfax will deconsolidate the UK run-off group and apply the equity method of accounting for its remaining interest. Fairfax may further monetize its remaining interest in UK run-off in the future although the company also retains the flexibility to repurchase its interest over time. Nothing to do with Covid, statutory capital, or bankers. They've always looked for flexible financing, especially when it is advantageous to them or they are getting a premium price. So can the BS and stick to the actual facts! Cheers!

-

The stock will do over 50% regardless...just reversion to book will do that! So you're not really adding anything! 15% compounded on $595 USD book over two years gives $786 USD...was trading at $393 USD on Monday. I say 100% return or better by October 2023 at the latest...barring a massive catastrophe or market crash. Cheers!

-

+1! Cheers!

-

Yes, because you saw the pandemic coming, correct? Suddenly, some of their insurers had to book losses from the pandemic and their equity portfolios took a hit...something probably unaccounted for like 9/11 was for insurers. Fairfax had $1.7B in cash at September 30, 2019, which dropped to about $1.1B at December 31, 2019 because they paid $600M in insurance debt. That's why they had to reborrow and issue more debt in 2020 to inject capital into the subs after $400M in Covid losses and $1B in equity losses. As well as keep over $2B in cash because liquidity was drying up across the world. The UK runoff business sale was announced well before the pandemic...nothing to do with bankers or statutory capital. Get your facts straight! Cheers!

-

Haha! With all of Prem's faults, he's somehow managed to put together a $15B company from scratch and lead about 50K people, but you go ahead and tell him what a failure he's been or how he can do much better. Cheers!

-

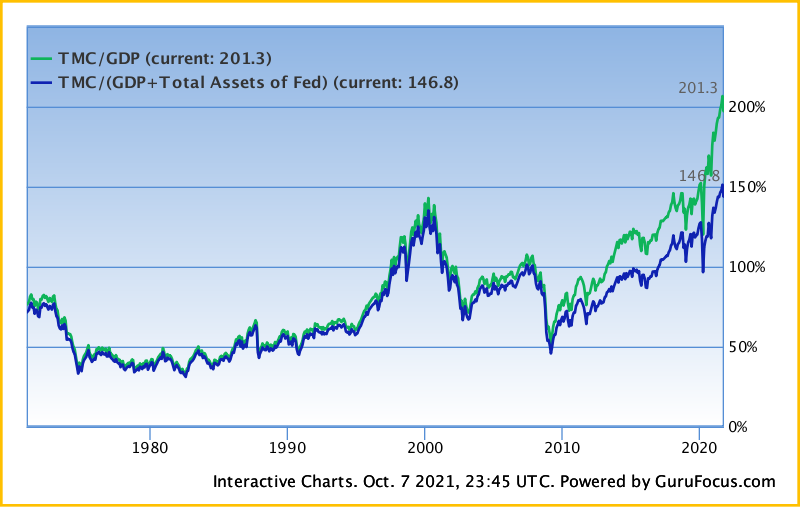

Hi Greg, you do understand the chart below, correct? You don't find it interesting that the period in which distressed value investors underperformed looks like that? And that you have massive distortions from the Fed's balance sheet. I'm not saying that Prem couldn't make money from 2009-2014 and certainly again in 2020, but you can see that the next decade cannot repeat itself. And that outcomes for equity markets are almost certainly to be well negative between now and 2031. Fairfax will have their time...which doesn't negate your argument presently. Nor does your argument presently negate the fact that Fairfax is cheap and will return to a more historical mean value over the next couple of years. Cheers!

-

Actually it wasn't Prem's problem. Balsillie and Lazaridis were on the board when Prem joined. The board pushed for Heins and his vision...so Balsillie resigned. Then the board pushed out Lazaridis, and Prem was left the lone voice in the wilderness pushing for John Chen and directing the company to focus on software. It BECAME a Fairfax problem, since they had a substantial investment in the company. Either Fairfax got involved, or BB would have disappeared a long-time ago. You can then argue...should they have cut bait and let it fail...or get involved, get Chen on board and perhaps save the company, its employees, its shareholders, the community built around BB and FFH's investment. In hindsight, which is where we all sit, including you...I'd be happy if they sold. But arbitrarily throwing around your opinions without any experience or being there...armchair quarterback at best! Cheers!

-

They had to step into managing BB because the board was killing the company under Thorsten Heins. Whatever you want to say, BB under Chen has been a relative turnaround with much work left to do. Getting out of the hardware business and focusing on the QNX software business was the right move. Should they sell BB...I agree, they should. But suggesting that Prem's ego is the only reason he's there is just plain silly! The whole reason he put Paul in as President was to remove himself from alot of these things. Cheers!

-

They've essentially bought back roughly 10% since 2017: From the fourth quarter of 2017 up to June 30, 2021, the company has purchased 1,322,303 subordinate voting shares for treasury and 1,102,998 for cancellation at an aggregate cost of $1,022.9 million. And the latest normal course issuer bid indicates they can buy up to 2.456M shares...or another 10%...and I suspect they will buy most of those fairly early as long as the price remains cooperative. In a low-interest rate environment, with little opportunity as asset prices have risen in most sectors, the natural area to allocate capital is in undervalued buybacks of his own company. This alone will be accretive to shareholders if bought under book...very accretive if bought under tangible book...eventually Mr. Market will come to his senses, and the bears on here will have to come up with excuses on how lucky Prem was or why they took the other side of this simple argument. I remember most of the same people telling me how Handler should have been removed from Jefferies two years ago, yet they couldn't see the improvements and how Handler was simplifying the business to be more like Jefferies and less like Leucadia. Same argument was made by people on why everyone should avoid Biglari Holdings during the pandemic...they thought it would go bankrupt and didn't want to invest with Sardar. You buy something because it is cheap...not because you don't like the management. You also need to have enough common sense to get out when the stock reaches your estimate of intrinsic value...again whether you like management or not. Cheers!

-

d) 25% in 1990. Cheers!

-

100%! No one is telling anyone to hold Fairfax shares forever. I don't hold any stock forever. I think the bulls are simply saying that the stock was dirt cheap last year, and remain cheap this year. And once it is revalued back closer to intrinsic value, we will sell and wait for other opportunities. The bears think that we are all Prem lemmings and that we will hold the stock for the long-term. There is a difference between admiring Prem and how we invest...yet they are convinced we are imbedded in our ways because of that admiration. Cheers!

.png.b132bc9f7727b3d70020a4f20a54d707.png)