johnpane

-

Posts

74 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by johnpane

-

If transaction costs are the same, a reason not to use ADRs is where the sponsor charges a substantial fee. For example, for GLNCY Citi charges 20% of the gross dividend, max 5c/share.

-

iSavings bonds yielding 7.12% currently

johnpane replied to Spekulatius's topic in General Discussion

Remember, only newly purchased i-bonds get that fixed rate. Bonds previously purchased get the same fixed component they originally received: 0.4% for purchases in the most recent 6-month window, and 0% for several windows prior to that. -

iSavings bonds yielding 7.12% currently

johnpane replied to Spekulatius's topic in General Discussion

Fixed rate on new purchases will be 0.9% . Combined with a 3.4% inflation component, the full rate for May-Oct 2023 will be 4.3%. -

iSavings bonds yielding 7.12% currently

johnpane replied to Spekulatius's topic in General Discussion

It could, but would only apply to new purchases. Bonds purchased in 2021 through Oct 2022 have a fixed component rate of 0% for the life of the bond. Hence the term "fixed". -

iSavings bonds yielding 7.12% currently

johnpane replied to Spekulatius's topic in General Discussion

New bonds are predicted to be ~3.8% if the fixed component remains around 0.4%. If you bought when this thread started there was a 0% fixed component, in which case the new rate will be more like 3.38%. I am also inclined to get out after holding 3 months at 3.38% which will be forfeited. I think annualized rate over 21 months (since Nov '21 or subsequent 5 months) will work out to something like 6.6%. -

Marty Whitman? Howard Marks? Distressed credit.

-

Look at TUA, and how it is described on pages 5-6 here.

-

IRS Pub 550: A wash sale occurs when you sell or trade stock or securities at a loss and within 30 days before or after the sale you: Buy substantially identical stock or securities, Acquire substantially identical stock or securities in a fully taxable trade, Acquire a contract or option to buy substantially identical stock or securities, or Acquire substantially identical stock for your individual retirement arrangement (IRA) or Roth IRA.

-

iSavings bonds yielding 7.12% currently

johnpane replied to Spekulatius's topic in General Discussion

You may want to look into using the gift box feature, if you haven't already done so. -

How do money market funds like SPAXX calculate interest distributions?

johnpane replied to aws's topic in General Discussion

In order to maintain the $1.00 value, interest does not accrue to NAV but is held separately and distributed proportionately to the how long the shares were held. If a person redeems mid-month they still get the accrued interest. This is in contrast to, for example, a very short-term bond fund, where NAV does reflect accumulated interest and there is no partial-month interest payment upon redemption. -

What did investors in the Japan stock market think in 1990?

-

Your puts were exercised Friday, giving you a sale of ARKK at $100 and leaving you short 500 shares. Your broker must have covered that short Monday -- maybe you can't borrow ARKK.

-

Felix Zulauf mentions the TGA in today's Barron's: Yet, he predicts lower long-term rates:

-

You bought stock in step 3, within 30 days before this sale. It is as simple as that.

-

An article, written 6 years ago and not attributed to any author, claims that an unnamed "partner at Deloitte" "suggested" a 3 step process. (Note the three steps do not include selling the call, so essentially amount to doubling down. It is apparently the author -- not the claimed Deloitte partner --who mentions selling the call to harvest the loss and does not say when). This could be completely made up, or the person might have retracted the suggestion. You can't believe everything you read on the internet.

-

Selling a call you hold is not "writing a call", thus not "writing a covered call", thus not "writing a qualified covered call". Your whole argument rests on a section of Pub 550 that does not apply to the situation.

-

"A qualified covered call option is any option you grant to purchase stock you hold." (Source: 2020 Publication 550, page 60) The publication equates writing and granting, e.g., "Writer of option. If you write (grant) an option, ..." (p. 57). Step (4) in your scenario is selling a call you have purchased, not writing one. If you deem yourself to have written an option, the one you acquired in step (2) is not closed and you cannot take the loss.

-

This is the flaw in your thinking. The "tie" between the security sold at a loss and the purchased security is instantaneous, not lasting. The cost basis of the purchased security is increased and the "tie" is no longer present. Now the purchased security (calls in your case) with stepped up cost basis is completely "fresh" with respect to the wash sale rule. How it got its cost basis is not relevant.

-

The market price was up 3% Friday but the NAV barely moved. So don't count on that day's action as an indicator of leverage. Also, keep in mind that the swaption prices are also affected by volatility. https://www.simplify.us/etfs/pfix-simplify-interest-rate-hedge-etf NAV Change +$0.07/0.17% Price Change +$1.26/3.14%

-

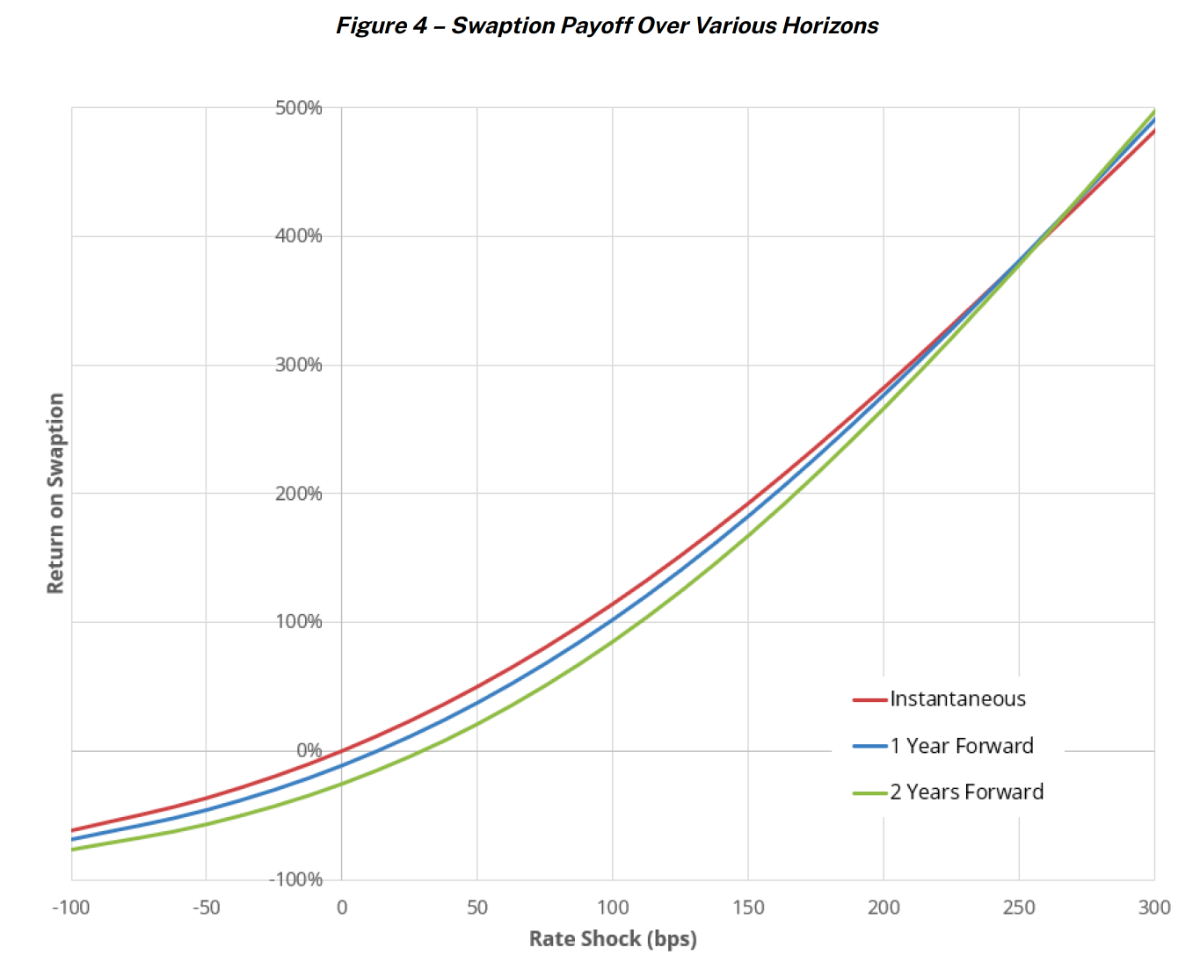

What do you guys think of this new interest rate hedge ETF as a way to position for interest rate rises (and increased interest rate volatility) with limited downside and timing risk? The fund uses swaptions on 20-year treasuries dated 7 years out. The chart shows theoretical performance of the swaptions, with a positive convex response to interest rates, and carry cost of about 10% per year if rates and volatility are unchanged. I think an increase in interest rate volatility would push the entire curve upward. These swaptions represent about half of the ETF holding with the rest in 5-year treasuries. This post has more details on the ETF's strategy, and is the source of the curve shown here.

-

Are you sure $120b by July is correct? I see you cited a Bloomberg article early in this thread that quotes that number, but others are saying the target may be higher and the deadline later, e.g. $500b, $750b.

-

No, that's not the worst case.

-

In my retirement account I'm using New York Life Guaranteed Interest Account (2.0%); otherwise MINT (1.8%), Amex Personal Savings (1.7%).

-

Interesting you should mention this. I have noticed an increasing trend of my neighbors reporting they have lost their cats (and dogs), but it has not seemed to be related bad or good weather.

-

GNW Current price of $3.18 is one-sixth of its $20.30 NBV (2015-09-30, excluding AOCI). I am not aware of any significant negative developments since Booth-Laird's worst-case-destruction-of-value NBV of $8.85. http://www.boothlaird.com/wp-content/uploads/2015/08/Booth-Laird-Investment-Partnership-Genworth-Analysis.pdf