oscarazocar

-

Posts

241 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by oscarazocar

-

Brett, I enjoyed the book, you did a great job covering the important information in a concise manner. I recall seeing somewhere (maybe Twitter) a few years back that small cap stocks did extremely well in the 1950's/1960's, the period covering much of the Buffett Partnership years. I don't know how that was measured or if any small-cap indexes existed at the time. Did you come across anything like this while researching the book? Thanks.

-

Which service do you subscribe to? https://investors.valueline.com/equities/digital-equities-services

-

What about the digital booklets do you like? Is it like the paper copies but in a clean online form? Thanks.

-

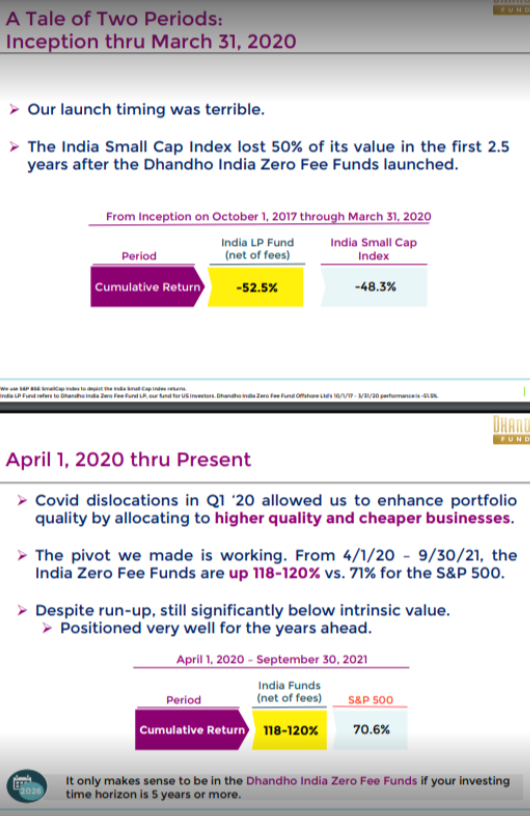

The slides below are from a Dhando Zero Fee Fund presentation from 2021 Q3. They show comparisons between three funds (Dhandho Zero Fee Fund, India Small Cap Index, and S&P 500) over two periods, 10/1/17 to 3/31/20 and 4/1/20 to 9/31/21. The slides show the Dhandho fund slightly underperforming the India Small Cap Index from 10/1/17 to 3/31/20 and then hugely outperforming the S&P 500 from 4/1/20 to 9/31/21. After looking at the slides, what was the total perfomance of the funds over the combined periods? Combined performance: Dhandho India Fund: 10/1/17-3/31/20: -52.5% 4/1/20-9/31/21: 119% Total: 3% (not shown in slide) India Small Cap: 10/1/17-3/31/20: -48.3% 4/1/20-9/31/21: 195% (not shown in slides) Total: 52% (not shown in slides) S&P 500: 10/1/17-3/31/20: 6% (not shown in slides) 4/1/20-9/31/21: 70.6% Total: 81% (not shown in slides) Do you think that the slides as shown are a reasonable way to compare the perfomances of the three funds?

-

There is no federal inheritance tax in the U.S. 6 states have inheritance taxes: Iowa, Kentucky, Maryland, Nebraska, New Jersey, Pennsylvania, that range from from 1% to 16% with various thresholds. https://www.cnbc.com/select/what-is-inheritance-tax/ Say you have a wealth parent and their child living 20 minutes away from each other right across state lines in the NYC suburbs . If the parent lived in NY and the child lived in NJ, they would be hit by both NY estate tax and NJ inheritance tax. If the locations were switched and the parent lived in NJ and the child lived in NY, there would be neither. The vagaries of the tax system - this impacted a friend recently.

-

Minimum Viable Market Cap For A Listed Company?

oscarazocar replied to Voodooking's topic in General Discussion

ITEX is a good example of a tiny company like this that has worked reasonably well. It trades on OTC, it's a weird little business that's basically a platform for barter exchange. Market cap is around $8 million, it has over $4.5 million net cash, has earned around $1 million EBIT per year going back on $6 million revenue, slowly shrinking, paying $1/share dividend per year now, has paid $3/share in dividends since 2019, stock was available around $4/share at various points over past 5 years. Chairman owns a big chunk (Sardar Biglari owns a piece too as a minority holder). For most of the period from 2019-2023, it has traded around 1x EBIT. Dividend bumped from $0.20/yr to $1.00/yr last year. I don't see why you shouldn't invest in a company like this if you are comfortable with the business. -

I donate to Rails-To-Trails Conservancy and think they do outstanding work that has a huge positive impact on communities around the country. They are the main lobbying group that works with federal/state/city agencies to promote the building of public bike/walking trails, often through conversion of dormant rail lines. They have a terrific website and magazine (I think quarterly) that highlights their work. https://www.railstotrails.org/about/ https://www.charitynavigator.org/ein/521437006

-

Buffett has spoken very highly of 3G: https://www.reuters.com/article/business/buffett-says-willing-to-partner-with-3g-again-on-very-large-deals-idUSBREA42096/ "I think 3G does a magnificent job of running businesses," Buffett said at Berkshire's annual meeting. "We're very likely to partner with them, perhaps on some things that are very large." https://www.nytimes.com/2017/04/10/business/dealbook/warren-buffett-jorge-paulo-lemann-brazil-conference.html Then, Mr. Lemann’s 3G Capital and Mr. Buffett’s Berkshire Hathaway teamed up to acquire H.J. Heinz for $23 billion. Two years later, 3G Capital, again together with Mr. Buffett, merged Heinz with Kraft Foods. “I consider it one of the largest mistakes in my life that we didn’t really team up as partners until considerably later,” Mr. Buffett acknowledged Saturday night, but that since doing deals together, “he and I are on the same wavelength.”

-

I have had this issue for a week and it makes the site pretty much unusable as I can only see the very recent commentary.

-

This is a quote from a 2007 student visit to Omaha: Question 2: GEICO is one of Berkshire’s crown jewels. You know the auto insurance industry cold, and you have been extolling the virtues of the GEICO and Progressive business models for decades. Why haven’t you ever taken a stake in Progressive? Essentially, "thumb-sucking". That is what his partner Charlie Munger calls it when they identify opportunities in their circle of competence and fail to pull the trigger. Buying one didn’t preclude buying the other. He immensely admires Peter Lewis, the longtime CEO of Progressive. He asks the question of CEO’s – if you had a silver bullet and could kill one of your competitors, who would it be? For GEICO, Buffett would his silver bullet, and all the rest of his ammo, shooting Progressive. Years ago [presumably in the early 1980’s], they were briefly looking at putting the two companies together. He joked that each CEO, Jack Byrne of GEICO and Peter Lewis, would each come to him and report that negotiations were moving along, only that each was under the impression that he was gong to be the CEO of the combined company. Buffett told the story of his initial involvement with GEICO as a Columbia student. It was obvious to him in 1951 that GEICO would do very well for a very long time. Everyone hates buying car insurance, but they are forced to, and a good chunk of them will go with the low-cost provider. Buffett mentioned that GEICO now has a slightly better position than Progressive [due to a lower cost structure, I believe], but that the two of them will be duking it out and both will gain share for a long time. When the internet hit, Progressive actually had an edge for awhile. Because they had no direct distribution up to that point, they were quicker to seize on the internet as their direct distribution channel. GEICO had been so successful with its direct mail and phone strategy that those institutional forces vested in the old systems prevented it from shifting to the internet nearly as quickly as it should have. Buffett eventually had to lock them in a room and tell them they couldn’t come out until they had a viable internet strategy.

-

Berkshire has had stakes in a number of companies they then acquired: GEICO, BNSF, Precision Castparts.

-

Why wouldn't he exercise the options and sell the stock? One wouldn't normally do that, but this is a highly unusual case, and the "intrinsic value" of the options doesn't seem terribly relevant here given the dynamics. He dominates the GME options market, everyone knows exactly what he owns, and his selling would crater the price. If he exercised the options and blew out of the 12m shares at $32.50/share, that's $150 million in the till, and he could actually do it. Not bad for a day's work.

-

How do you know he hasn't exited the call position? Some cursory browsing indicates that the open interest is recalculated once each day. If he exercised the options and sold the stock, would we know that now or would we have to wait until the open interest is updated?

-

https://www.elitetrader.com/et/threads/kuppy-comments-about-spacs.357294/

-

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

oscarazocar replied to tnathan's topic in General Discussion

Dataroma has a good search site for insider buys that shows a running list of form 4 info and you can filter for various things. https://www.dataroma.com/m/ins/ins.php?t=m&po=1&am=10000&sym=&o=fd&d=d -

These guys who had dinner with Munger and then go around posting photos with him and saying stuff like he was their "mentor" and trumpeting his name at every opportunity - it's very distasteful behavior. Munger had dinner with a lot of people. It's like the joke, "How do you know if someone is vegan? They'll tell you."

-

What are some examples of the big discounts in smaller stocks that you are seeing? Thanks.

-

The part on Musk's algorithm for operating companies is very good. The algorithm, plus his raw intelligence and intense focus, are the reasons for his unusual success. https://medium.com/@alastairallen/the-musk-algorithm-c241d9d0ee3d

-

National Indemnity, See's, Buffalo Evening News, GEICO, Scott Fetzer, hiring Jain, KO, AXP, Mid-American, BNSF, AAPL. Scott Fetzer is a very underrated acquisition. Berkshire paid $235m net in 1986, took out $244m (net income = FCF) in first 5 years, $309m in next 5 years, and in year 11 earned $82m net, with Scott Fetzer segment at $32m net income (peak), Kirby at $39m (peak) and World Book still earning $10m. The entire thing did about 24% IRR with minimal leverage. All that cash went into equities and other businesses at attractive prices between 1986-2000.

-

Public Company Share Repurchase-Cannibals

oscarazocar replied to nickenumbers's topic in General Discussion

APOG has a great niche business, the Large-Scale Optical segment, that makes coatings for picture frames and is very steady and highly profitable. It is different in character than the rest of the APOG businesses, less cyclical, and provides ballast if the main business has a big down cycle. -

Public Company Share Repurchase-Cannibals

oscarazocar replied to nickenumbers's topic in General Discussion

The SEB repurchase wasn't just from a "major shareholder group", but the Bresky family which still owns over 73% and has controlled and run the company for many decades. It's a very odd transaction. Why would they sell a huge block at such a large discount to tangible book value when the stock has traded above that level for many years? Presumably they would get a decent premium to tangible book value if they sold the company outright. -

I recently came across the Tsai Capital 2023 Q4 letter on Reddit, turns out that the manger, Chris Tsai, is the son of one of the 1960's Go-Go investing OG's, Gerry Tsai. https://tsaicapital.com/files/Tsai-Capital-Annual-Investor-Letter-2023.pdf https://www.nytimes.com/2008/12/28/magazine/28wwln-tsai-t.html

-

Returns on fiber/broadband investments hugely depend on competition or lack thereof. As others have mentioned, if you are in an area with 3 or more providers, returns will be terrible. If you are the only option or there is one other mediocre compeitor, returns can be very good. Allo focuses mainly on small towns where they think they can have a high market share. Click below and you and see the places they are. It's mostly small towns in Nebraska like Kearny, Crete, and Gering. This is not competition central. They went into Lincoln because Spectrum (Charter) had a terrible local reputation and, as mentioned, I believe they got a good deal with the city who wanted competition in the broadband market. https://www.allocommunications.com/communities-that-want-allo/

-

NNI has disclosed Allo metrics over time and the penetration has been reasonably impressive. In 2017 they had 71k passings and 20k households served for 29% penetration, then ramped up and by 2020 had 150k passings and 59k households served for 40% penetration. I spoke with them several years ago and they indicated they would hit their financial targets with 50% penetration and in the 2022 letter they indicated results are ahead of initial underwriting expectations. My guess is that their Lincoln deal was probably a pretty good one given their long-time presence and deep connections there.

-

NNI is not really allocating much capital towards fiber. They invested $450 million in capex and net losses in Allo (their fiber business) through 2020, then in late 2020 sold a majority stake in the business to a private equity firm (SDC) for $260 million and retained $130+ million in preferred stock and 45% equity interest (at the time valued at $129 million), so they took out most of their invested capital. They have contributed minor amounts since, including $8 million in 2023 Q1, but Allo raised debt to fund its growth going ahead and I think there will likely be minimal future capital conributions.