obtuse_investor

-

Posts

414 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by obtuse_investor

-

Maybe we are witnessing Computershare’s float in action.

-

Agreed. I put the back of the napkin aside and did some real math on the BVPS annual return since very first filing. The return has been 11.3%. Note that this return is after fees to FFH. For comparison, stock has returned about 3% over that same period. Buyer from 2015 IPO (with cost of $11) lost about 8% each year on multiple compression. Full disclosure, I am not planning to tender my shares. And no, I fortunately didn't buy at IPO.

-

I could see the book value rising at a reasonable clip, like it has. Can’t predict if it would be at 25. What do think has to be true for it to trade close to book value per share? Multiple compression has been the biggest detractor of return for security holders since 2015, while book has grown at about 10% per annum.

-

Interesting development! Fairfax India Announces US$105 Million Substantial Issuer Bid https://www.fairfaxindia.ca/news/press-releases/press-release-details/2021/Fairfax-India-Announces-US105-Million-Substantial-Issuer-Bid/default.aspx Curious timing. FIH stock was down 5.3% today. This press release came out after market close today.

-

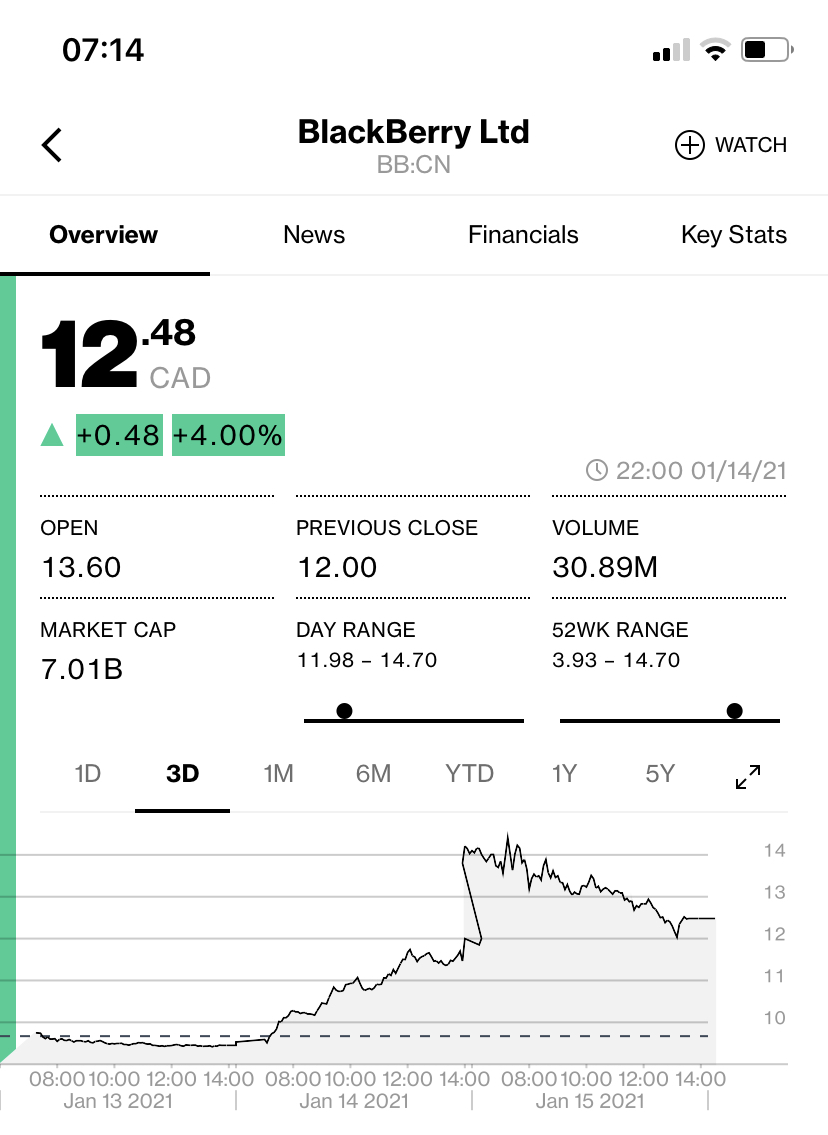

I expect they did something with their BB position, but it was probably something complicated and too smart. I miss the time when Prem and team only stepped over 1ft hurdles.

-

There was a disturbance in the space time continuum when that BB rip happened. Bloomberg caught it.

-

This is standard annual filing. Fairfax financial did a similar one at the same time.

-

Very lacklustre on repurchase front. This will disappoint the market. I am not surprised though. I have long maintained that Buffett is playing the very long game (which will long surpass his own expiry date). While market has basically discounted COVID-19 already, Buffett is likely thinking much longer term. Almost all scientists agree that we are in for the long haul of virus induced disruption. Market isn’t discounting that (yet).

-

What's your estimate for the current book value though? I don't have any fancy models. Two of their biggest assets are the airport and IIFL (finance & banking). Both these are going to get hit severely due to COVID, but we also know that the impact would not be forever. People will fly again and use their financial institutions again. Do a DCF of a sample company... even if first two years there is zero earnings, the value drops much less than 30%. If I simply assume that their Q4 book value has dropped ~30% similar to overall Indian stock market, then it will be around 11.8/shr. As of this writing FIH is selling at P/B of 0.57. If the underlying businesses return nominal 10% p.a. then at current price buyer is earning ~18% p.a.

-

Of all the things I own right now, FIH certainly looks the cheapest right now. If the book value growth is about 6-8% per annum for next 10 years, with current discount to book you can lock in a very healthy rate of return even after fees. Book should grow at a higher rate than that.

-

Canadians: Where can I get a TFSA that allows options?

obtuse_investor replied to Mark Jr.'s topic in General Discussion

TD allows it too. ••• I wish it didn’t. In May 2009, I bought small bit of Harley Davidson puts in my TFSA thinking it was a false rally since March. Rest of my portfolio was long. No leverage. The puts went to zero in 3 days with no capital losses to show for it. I recently calculated what that cash would have been worth today if it was invested long as rest of my portfolio. The answer: about $50k. -

Lol! There is so much truth in that. FFH’s business returns are highly variable year to year. Over medium (3-10yr) term they can range from terrible to outstanding. Effectively, as a long term shareholder you’re in for a ride. It will occasionally move like a rocket and other times it is a dud for years. The only reason to stay attached to the business is trust in management, which itself ebbs and flows. Frankly, I don’t know why I do it. :-) I also know that when I feel incredibly down about this firm it’s a time to buy rather than sell. In short, I don’t do a DCF on this firm because I am not smart enough. It would be garbage in and garbage out.

-

Technically, you’re right John. However, I would be very surprised if his suggestion wasn’t accepted by the *board* without question. He makes a suggestion because otherwise it would make him a hypocrite in the eyes of everyone who sees Buffett as a beacon of corporate governance. I am sure the irony isn’t lost on Mr Buffett.

-

I am wondering what the market sentiment for FIH is. As of this writing it is selling at 0.76 times year end book value. The assets are earning cash and are profitable. Whenever there is a relevant transaction they get marked to market. So the book value is likely a good approximation. Why the discount? No faith in management? Fees do not justify the discount. Is the market thinking that Indian assets are overpriced on the books? I am incredibly patient. Just wondering what the narrative is to justify the large discount to book.

-

As value investors we know that Mr market has his mood swings. Head scratching moments are the precise opportunities to make money. Good for you for taking advantage of the situation! :-)

-

I find it interesting that this group assumed this transaction is an attempt by FFH to draw fees from FIH. Peak pessimism on FFH management? Has anyone looked into foreign ownership rules? They did decrease beneficial ownership to 49%.

-

I voted. Although, I am more interested in the second question by OP. Best ways to park cash in Canada. Thanks for suggesting XFR.TO. I didn't know about that. I wonder what the tax and risk profile is compared to a money market fund. Something, I'll have to look into. I have been using Money Market fund from my brokerage's parent bank (TD, in my case). All other large banks have that offering. Although I am quite interested to see the large banks off "Investment Savings Account": See https://www.td.com/ca/en/asset-management/additional-solutions/ as example. The interest rate is higher than their own CAD money market fund. Any other ideas that Canadians have for having a ready place to park case. Ready, being available within 24-48 hours.

-

Woodlock House blog post about FFH

obtuse_investor replied to StubbleJumper's topic in Fairfax Financial

Good article from Mr. Mayer. Thinking a little bit more about the numbers. Looking at the market multiple mentioned in the article: 11% ROE at 1.7xBook. If I plug that into a simple NPV calculator, I see that market is using a 5.3% discount rate. FFH is selling 0.95xBook as of this writing. Assuming (and this is a big assumption) this discount rate as a constant, using the same calculator I see that the market is estimating that FFH will have a ROE of 4.8%. If you think FFH can produce above 4.8% of earnings (or US$21/shr a year) for a couple years in a row, then you should definitely consider buying this stock. ~~~ Why such a low ROE estimate, Mr. Market? I think the narrative says it all. The market has lost faith in FFH's ability to deliver. However, Mr. Market suffers from periodic case of amnesia. I am sure, this too shall pass. -

FIH.U keeps on hitting 52 week lows lately: https://web.tmxmoney.com/quote.php?qm_symbol=fih.u Do you think it is a macro thing? I haven't seen any news from holdings.

-

Buffett buybacks: Could Berkshire tender stock?

obtuse_investor replied to alwaysinvert's topic in Berkshire Hathaway

To corroborate the repurchase numbers you can always check CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY. The $443M number is plainly mentioned there. On a more strategic note, I can’t wait for the media to get bored and move on to some topic other than repurchases at BRK. Buffett is playing the long game. I am happy to play along. -

I appreciate the historical context. I can totally believe that one of the prime ways of attracting equity capital is to pay a stable or increasing dividend. It is a complete shame that people who buy equity for the 4% dividend would continue to hold, while the management issues 20% equity, wiping out ~5 years of dividends in one fell swoop.

-

I agree that there are likely other preferred shares that present much better risk/reward. I just haven't done my homework. With Canada's housing bubble finally unraveling after decades of credit binge, I wouldn't be counting on Canadian chartered banks' dividends to be stable. To me the worst case is quite horrible indeed. If the housing market reverts to the mean, we are likely talking a lot of pain for the Banks' shareholders. Back on topic... your arguments have convinced me to stay away from the FFH preferreds though. :)

-

Thanks! I missed that thread. It is interesting that that thread is focused on the ability of FFH to pay because it was mainly happening during the Q4 market swoon.

-

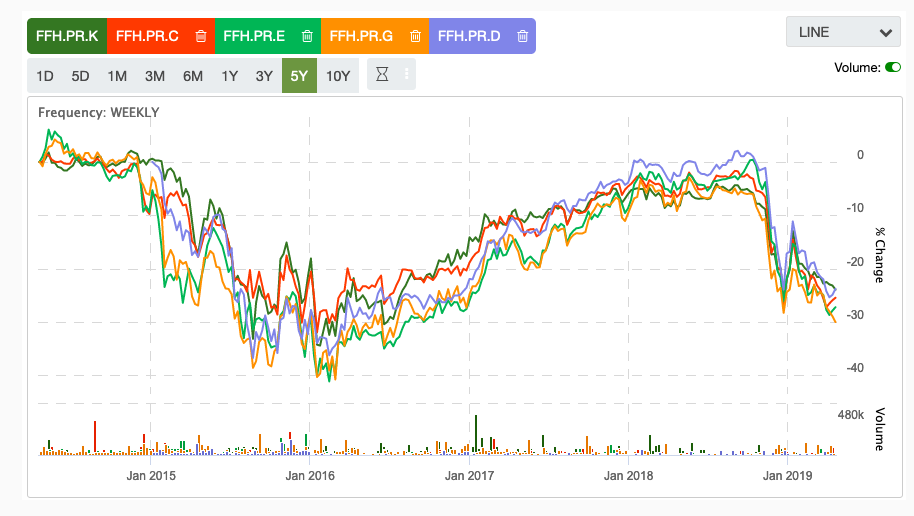

Bumping up this topic. :) FFH rate reset preferreds have been effectively tracking the Canada 5yr Bond (see attachment). Some of these are yielding to reset (YTR) at 6%. What confuses me is that they are trading at the same levels as 2016, when the Canada 5yr bond (https://ycharts.com/indicators/canada_5_year_benchmark_bond_yield) was at 0.6%. It is at 1.6% right now. Is the market forecasting that Canada 5yr bond will drop back to 0.6% (which would imply a recession from today's levels). Even if that happens, these preferred may be a good value right now, since they are already discounting a negative future. Best case: It is status quo 2 years from now, and these reset to (1.6 + 3.98 = 5.6%); which will lead to ~20% capital gain as well. Worst case: Reality is that BoC is unable to lower rates, if US economy is strong. So, in worst case US and Canada hit a recession, leading to a zero bound once again. These will reset to about 4.5%, with minimal capital loss on the books. You're making 4.5% while you sit through a recession. Not a bad risk/reward for a fixed income portion of the portfolio. Am I missing something?

-

Just to normalize, 50% over a 5 year period is 8.44% annualized return. I don't think anyone who owns FFH is expecting annual returns less than 10%. Maybe that is because of the 15% anchoring management has been doing.