mananainvesting

-

Posts

329 -

Joined

-

Last visited

-

Days Won

1

Content Type

Profiles

Forums

Events

Everything posted by mananainvesting

-

What's the quick pitch on this? If you dont mind sharing. Thanks

-

I agree stock price is not a great yard stick for value creation (in the short run), but in this case the >75% of the $KW shareholders who didn't take it private would say otherwise. I am guessing there is hidden value and will be interesting to see in the coming years how this investment/partnership fares.

-

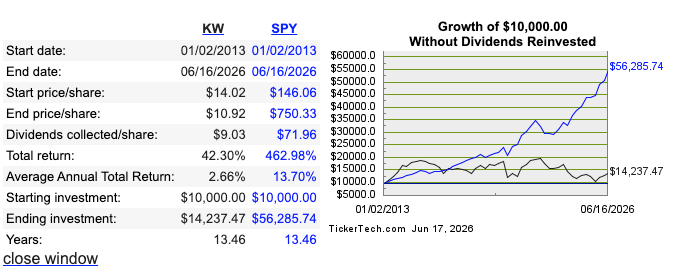

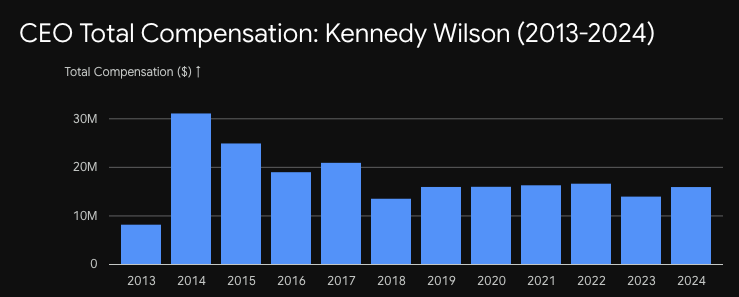

$KW - Kennedy Wilson, this investment of Fairfax has been a curious one for me. I know Prem has high regard for William McMorrow, but $KW was a disaster to its shareholders. The shareholder return vs management pay makes my stomach churn. I wonder how Fairfax will be protecting itself in this investment? I hope they keep an eye on Pay vs Performance! $KW Performance vs SPY and Total comp of CEO over the years (Via Gemini).

-

Andrew Peller Ice Wine Portfolio imo is super under penetrated outside of Canada. I think India is going to be an amazing market for the company. My grandma loves wine (but adds sugar to it) so this time when I went to India took her a bottle of Ice Wine and she loved it, in fact all my cousins did too! This could potentially be the Moutai of India! (I know it is a long shot!, but we are not paying anything for it!)

-

Another important thing is the retail wine store licenses the company owns.

-

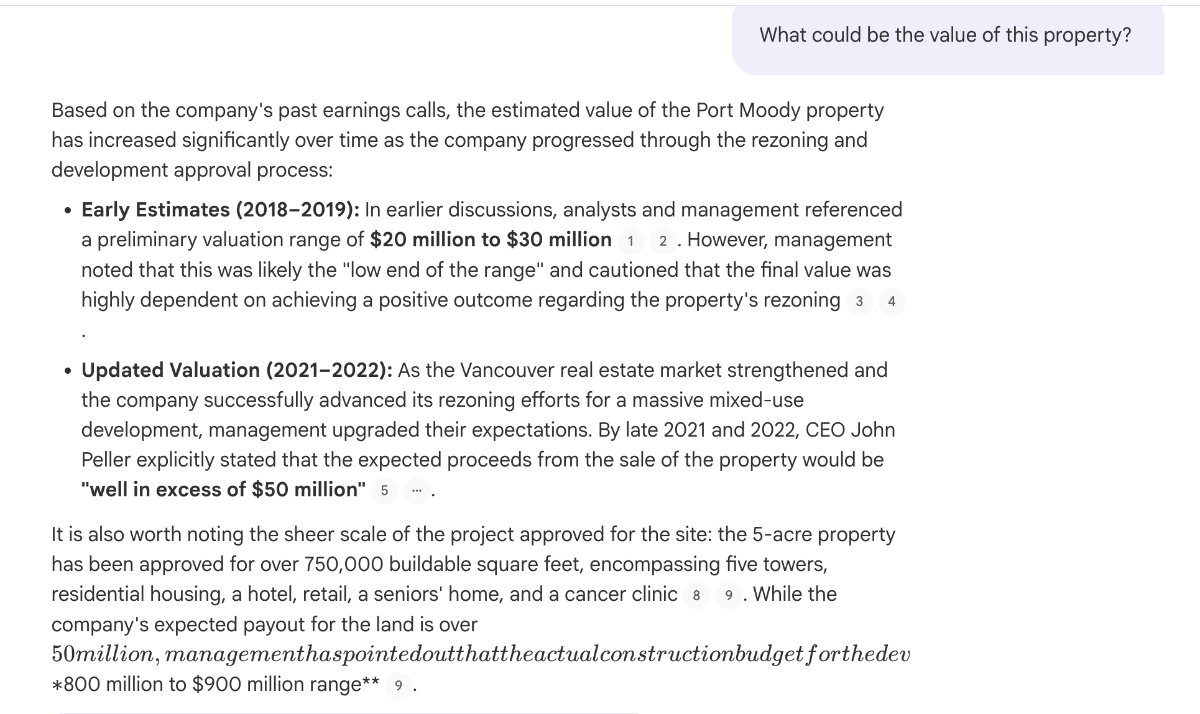

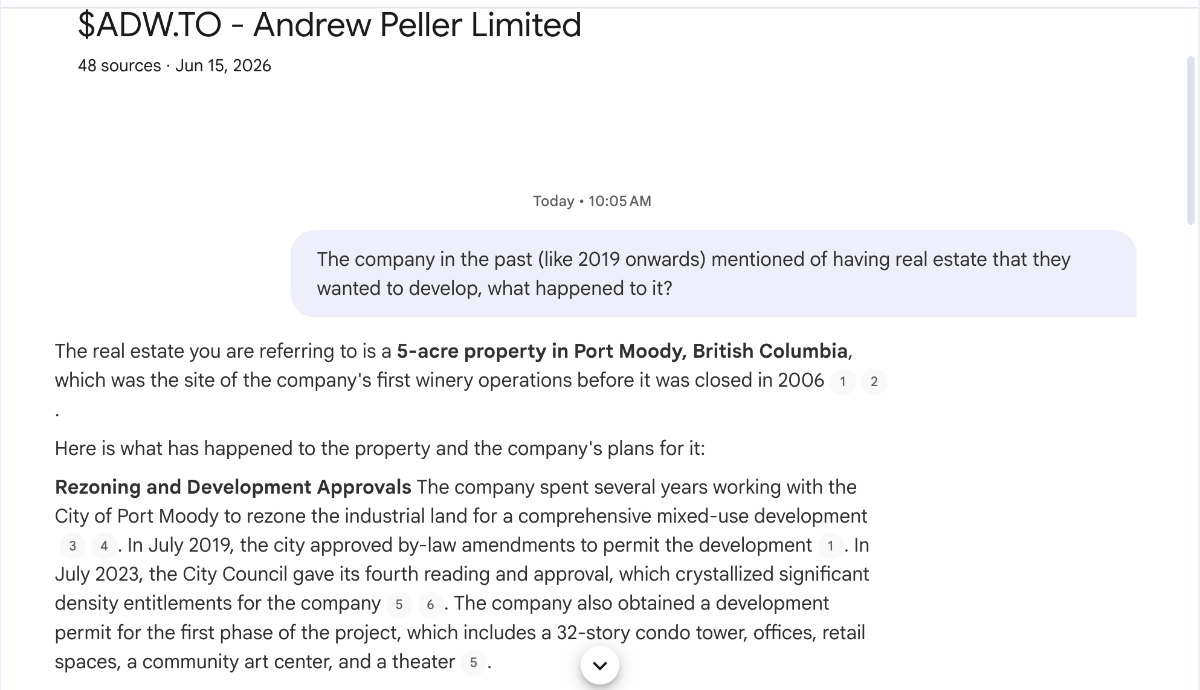

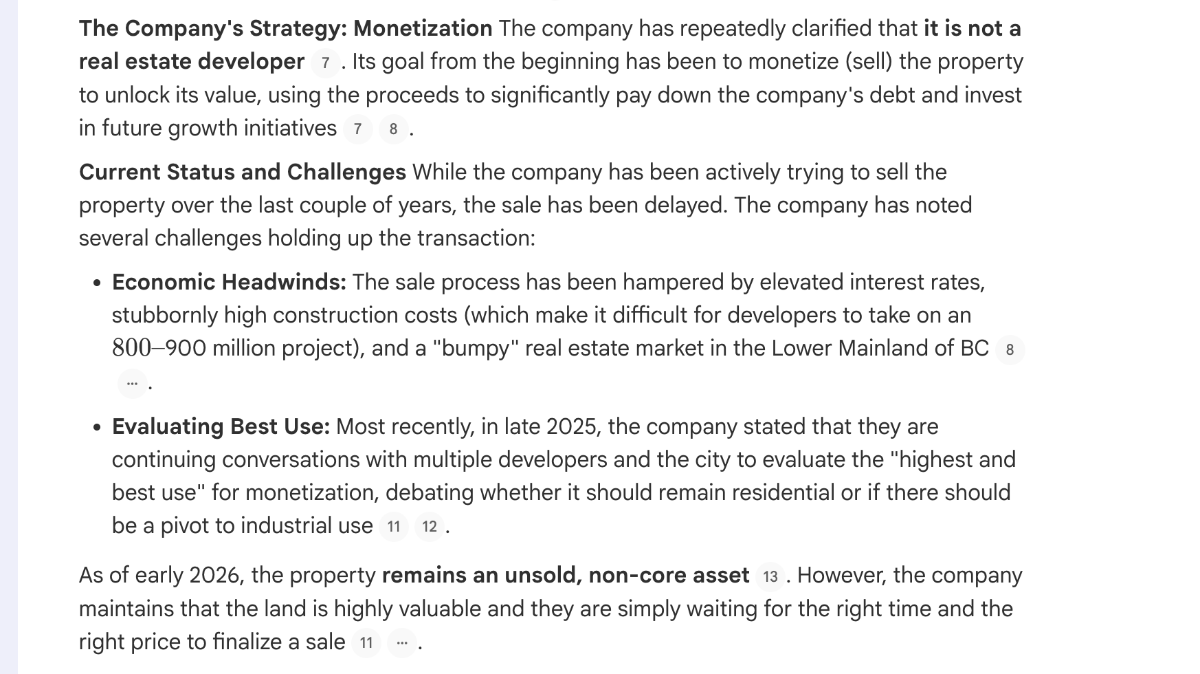

The construction project for a developer at Port Moody Winery would be in the range of $800- $900M CAD per John Peller (Prior CEO). See transcript from their 2023-11 call. Now, where Real Estate is currently in Canada it might not be Viable, but definitely worth a lot in the right hands over time.

-

I wrote about it on X

-

Do you think they did the deal to help a Canadian Company? ex like how Blackberry investment likely was about saving a Canadian company (my guess)? or do you think they understand Canada better? I think there is a lot of hidden value in Andrew Peller real estate portfolio that could be unearthed with Capital that Andrew Peller could not.

-

-

Andrew Peller owns a good property that they have been wanting to develop to sell.

-

I appreciate this forum, both the bears and the bulls. How I think about Fairfax: • Fairfax seems like a fun place to work, people are happy (long tenure), partners are happy (long term partnerships) and my guess customer are happy too. Usually, such places are where amazing things happen! • I don’t have the scar tissue like some of the other holders from Fairfax, but I do have scars from other holdings. The lessons are similar. • The management has been clear, they prefer lumpy higher earnings than flat lower earnings and they measure this over the long run. So I think shareholders/potential shareholders must stomach short term fluctuations to get better long term returns. • The issues of the lost decade has management addressed it? Did they learn from it? Yes, Prem has mentioned this. 2018 Annual Report: “After much thought and discussion, it became clear to me that shorting is dangerous, very short term in nature and anathema to long term value investing. As I mentioned to you in last year’s annual report, shorting has cost us, cumulatively, net of our gains on common stock, approximately $2 billion! This will not be repeated! In the future, we may use options with a potential finite loss to hedge our equity exposure, but we will never again indulge anew in shorting with uncapped exposure. Your Chairman continues to learn – slowly!!” • I see them leaning towards investing along side proven/capable operators/investors like Adam Waterous, Pierre Lassonde, David Sokol, Dan Myerson. Likely one of the reasons why their investing performance has improved recently. Also they seem to change management/operators if things aren’t working out Ex: Dexterra Group. • Prem has mentioned they will make use of opportunities to buyback stock if at attractive price. They said that sometime around 2018, we know most of the cash went into growing premiums during the hard market. They seem to be walking the talk! My hurdle rate is ~10-15%, and I believe at these prices Fairfax will meet that.

-

-

https://x.com/MananaInvesting/status/2062329952679403603?s=20

-

$FRFHF/$FFH

-

I did a writeup on $GFR - Greenfire Resources, one of Fairfax's stock position. It is free to read, link to the writeup: https://mananainvesting.substack.com/p/1-greenfire-resources-ltd-tsx-gfrto Let me know your thoughts/feedback. Thanks. Disclosure: I am long $GFR, this is not investment or financial advice.

-

https://economictimes.indiatimes.com/news/company/corporate-trends/fairfax-india-makes-open-offer-to-buy-additional-26-in-iifl-capital-services/articleshow/131170147.cms?from=mdr

-

Agreed! Key is even when the company is severely undervalued management won't sell or take private! $KW management is probably everything I do not want to see in a company. Extremely high compensation (imo) and for what? taking it private when the market mispriced (likely) it!! Hoping Fairfax is careful with that team!

-

This is a small position for Fairfax, but Ensign Energy services is up ~72% YTD! Fairfax owns ~20% of $ESI.TO. Current Mcap of $ESI.TO is ~$800M CAD.

-

More $FFH.TO/$FRFHF

-

Haha! Epic!

-

Francis Chou video at the recent Value Investing Conference. The 1:29 mark, he expands on the float/equity ratio!!

-

I hear you and I will be watching the results of the company closely. In the spirit of learning (mostly for me), by your logic, don't most good insurance companies/their investors during soft market just give up on insurance and come back only during hard markets (assuming they can time it perfectly)? The insurance business through cycles but generates float which when managed prudently along with a good combined ratio is what attracted Buffett and similar people? I think where you are coming from is a valuation perspective, but shouldn't we just let winners do their thing and not disturb compounding? Unless the valuation gets crazy, in this case I think most would agree that is not the case.

-

Agreed, they don't have to reach for premiums/float!

-

I pulled this with the help of Notebooklm and chatgpt (could have errors and the table is missing some years). Fairfax has compounded book value over the years even when combined ratio has been high, only over the last 5-10 years has its insurance combined ratio gotten better. Also, one can see they have for the most part always had more float to equity, which means most of their returns came from investing. Now over the last few years I believe this has changed, their insurance operations have gotten much better and their investing returns will only have to do modestly well going forward to get really good overall returns (as long as the insurance operations keep performing), I think they have enough float leverage that even if premium growth rates slow down or even go down, imo it will still result in very good return (>15%). Obviously nothing is given but imo this is one of the very few companies out there at such low valuations levels for such a fantastic business + management! I am extremely long Fairfax Financial and open to changing my mind if circumstances change (basically not married to the idea).

-

update: Corrected the Fairfax table to correct for a few non-per share values. The ratio remains the same irrespective. I used Chatgpt and Notebooklm to generate these. I haven't double checked the numbers. FYI. Clearly from below, Fairfax has always had higher float to equity compared to Berkshire.