Leaderboard

Popular Content

Showing content with the highest reputation on 03/01/2024 in all areas

-

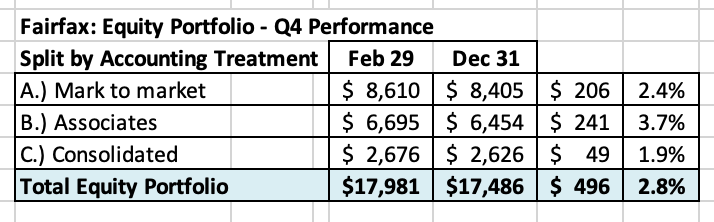

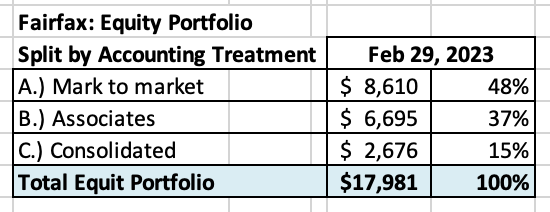

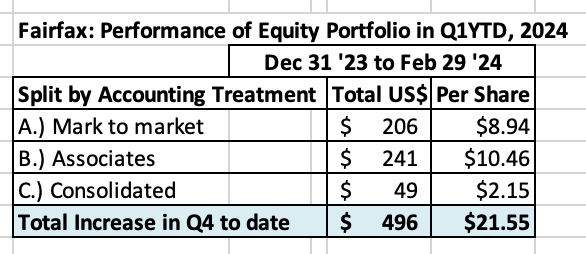

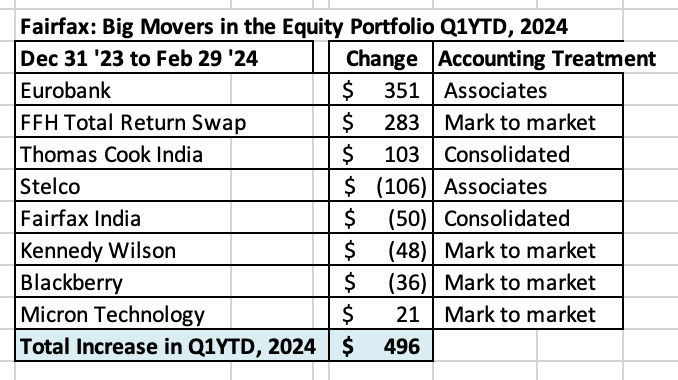

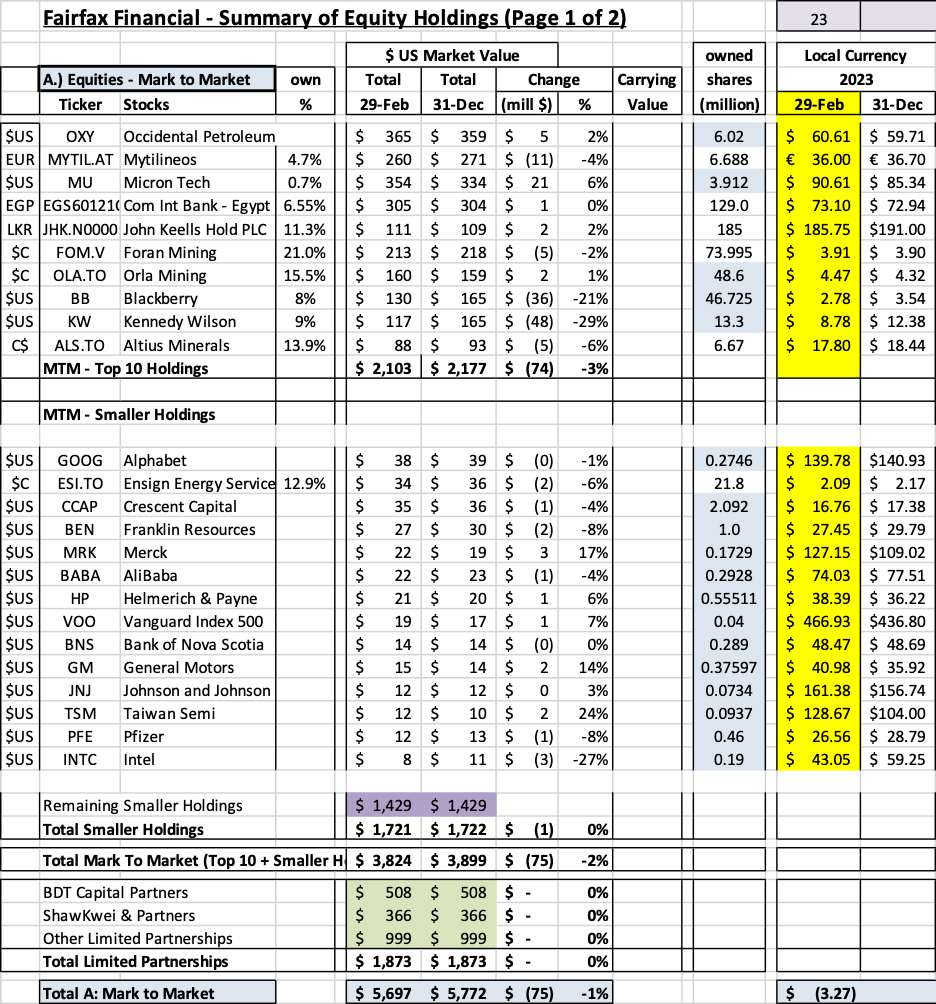

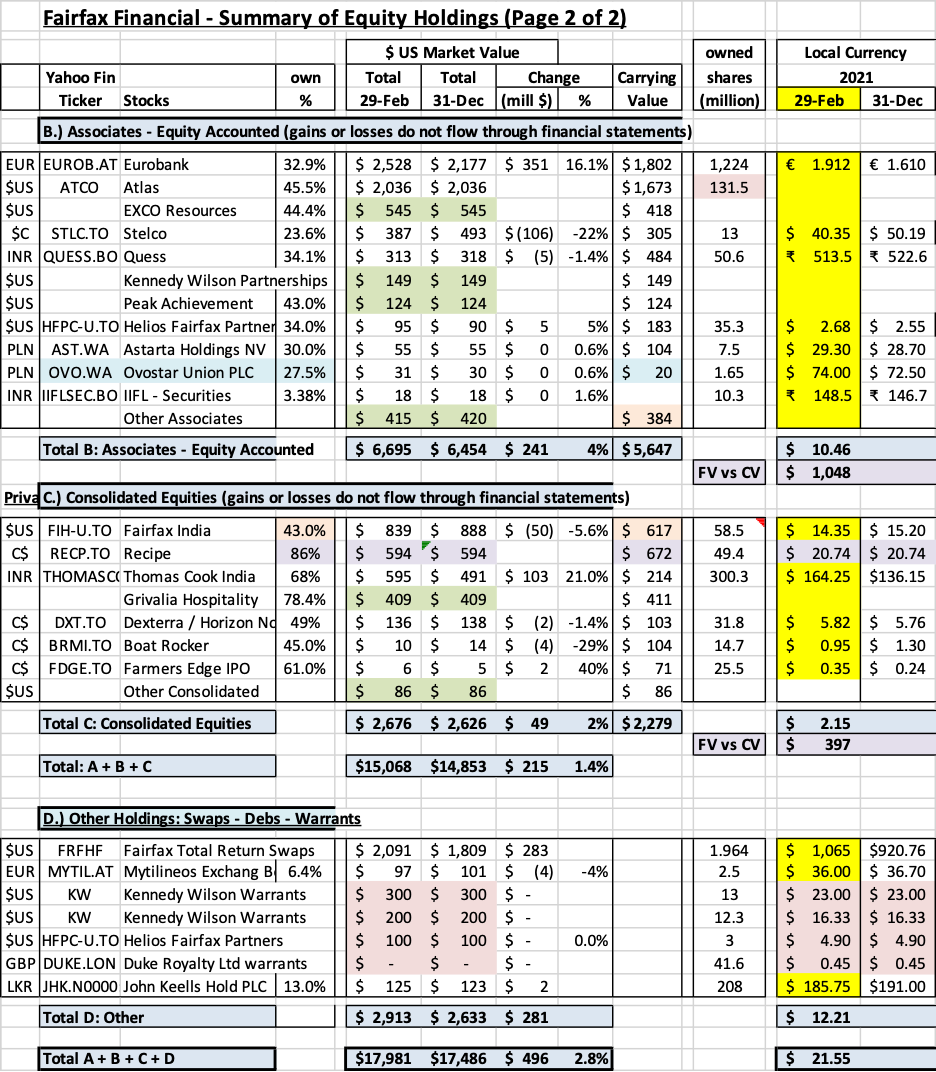

What was the change in the value of Fairfax’s equity portfolio to Feb 29, 2024? Fairfax’s equity portfolio (that I track) had a total value of about $18 billion at February 29, 2024. This is an increase of about $496 million (pre-tax) or 2.8% from December 31, 2023. The increase two months into Q1 works out to about $21.45/share. I include holdings like the FFH-TRS position in the mark to market bucket and at its notional value. I also include debentures and warrants in this bucket. My tracker portfolio is not an exact match to Fairfax’s actual holdings. My summary contains no information from Fairfax’s 2023 annual report, as it has not been released yet. As a result, my tracker portfolio is useful only as a tool to understand the likely directional movement in Fairfax’s equity portfolio (and not the precise change). Split of total holdings by accounting treatment About 49% of Fairfax’s equity holdings are mark to market - this includes 'A.) Mark to Market' and 'D.) Other Holdings' - and will fluctuate each quarter with changes in equity markets. The other 51% are Associate and Consolidated holdings. Over the past couple of years the share of the mark to market portfolio has been falling. This means Fairfax's quarterly results will be less impacted by volatility in equity markets. That is an important development. Split of total gains by accounting treatment The total change is an increase of $496 million = $21.55/share The mark to market change is increase of $206 million = $8.94/share. Only changes in this bucket of holdings will show up in ‘net gains (losses) on investments’ (along with changes in the value of the fixed income portfolio) when Fairfax reports results each quarter. What were the big movers in the equity portfolio Q1-YTD? Eurobank was up $351 million and it is now Fairfax’s largest equity holding at $2.5 billion. Eurobank reports results March 7. It will be interesting to see if they initiate a dividend. The FFH-TRS was up $283 million. This position is now Fairfax’s second largest holding. The investment is up a total of $1.356 billion over the last 3 years, which is a gain of 185%. Simply an amazing investment. Thomas Cook India delivered a very strong Q4 to cap off a stellar 2023. Fairfax’s position was up $103 million. People are travelling again in India! Kennedy Wilson was down $48 million. The company has been hit hard by concerns in office real estate segment. The value to Fairfax from this holding is not its equity exposure. The value is the extensive partnership the two companies have established over the past 12 years, most recently in significantly expanding the real estate debt platform. I wonder if Fairfax does not use the current weakness in KW's share price to materially and opportunistically increase its stake in the company in 2024. That was the playbook Fairfax used with a number of holdings that were negatively impacted by Covid in 2020 - and these incremental investments have worked out extremely well for Fairfax a couple of years later. Blackberry continues to shrink in size, down $36 million. Blackberry is now a $130 million position = 0.21% of Fairfax’s $60 billion investment portfolio. In Q1, Fairfax also ended its $150 million debenture investment in Blackberry and Prem resigned from Blackberry’s board. The debenture was a $500 million dollar position in Sept 2020. This is another good example of Fairfax exiting from a poorly performing legacy investment (financially and also in terms of involvement from the management team). Capital at Fairfax continues to shift to better opportunities. The clean-up of poorly performing equity investments looks largely completed – understanding that there will always be a few underperformers. Excess of fair value over carrying value (not captured in book value) Carrying value in this section is understated by quite a bit as it does not capture Q4, 2023. I will update this once the annual report is released. For Associate and Consolidated holdings, the excess of fair value to carrying value is about $1.445 billion or $62/share (pre-tax). Book value at Fairfax is understated by about this amount (less the tax impact). Below is the split. Associates: $1.048 million = $45/share Consolidated: $397 million = $17/share Below is a copy of my Excel spreadsheet (next 2 pages) if you want a closer look. Equity Tracker Spreadsheet explained: The summary below attempts to track all equity holdings at Fairfax. Each quarter the spreadsheet is updated to capture any ‘new news:’ purchases and sales. We have separated holdings by accounting treatment: Mark to market Associates – Equity accounted Consolidated Other Holdings – derivatives (total return swaps), debentures and warrants We come up with the value of each holding by multiplying the share price by the number of shares. Are holdings are tracked in US$, so non-US holdings have their values adjusted for currency. Important: the list is not complete. Some information we only get once per year when Fairfax published their annual report. Fairfax also makes changes to their portfolio each quarter. Fairfax Feb 29 2024.xlsx

1 point

1 point -

I rarely eat at MCD's but the wife and I were road tripping and stopped for a "quick and cheap meal." Small fry - $3.69 Large fry - $4.95 Quarter Pounder meal - $13.69 McChicken - $3.99 McDouble - $3.19 4-Piece Nugget - $3.69 We kept driving...absurd prices for borderline garbage food. Can go to a local sit down burger joint for those prices.1 point

-

@Luca I came across this short article that you might find interesting regarding the value proposition of Bitcoin. Bitcoin's unique value proposition | BitMEX Blog There are a number of technical articles as well here. I downloaded the Block Size Wars - The Battle for Control Over Bitcoin's Protocol Rules by Jonathan Bier. I just started it, but it shed some light behind the scene of its development. You might also find it helpful.1 point

-

Hi folks. Longtime lurker, first-time poster here. Just wanted to chime in with a few comments, some general, some related to the topic of this thread. First, I want to echo those who have highlighted @gfp's contributions to this board over the years. Thank you for your thoughtful posts—I hang on every word. (I'm grateful to all the members of this forum, I should add!) Re: the topic of this thread, a comment that Seth Klarman made in an old issue of Outstanding Investors Digest (at least, I think that's where I found it) comes to mind. An interviewer asked Klarman about his hurdle rate, clearly expecting his answer to be some crazy nominal figure like 20%/yr. Klarman emphatically replied that he never targets nominal returns, only risk-adjusted returns. I agree that that's the metric to target. I would hazard that Berkshire has pretty much always (and maybe literally always, but I won't go that far) offered at least plausible risk-adjusted returns, including over the past two decades. As gfp mentioned, the key is not to interrupt quality compounding, and the easiest way to avoid interruption is to own low-risk assets that you know intimately. The stock's decent risk-adjusted prospects hold even today. Compare owning (an admittedly slightly pricey) Berkshire now with owning the S&P 500 at a Shiller P/E of 34 and with after-tax corporate profits/GDP near all-time highs, not to mention a degree of concentration that Ben Inker of GMO argues all but ensures underperformance in megacap stocks. So, has Berkshire "killed it" since 2000? On a risk-adjusted basis, yes, and it has a good shot of continuing to do so for the next ten+ years, especially if its dividend policy holds. My 1991 shares have done 14.46% p.a. for 33 years, my 2011 shares have done 15.04% for 12 years, and my 2020 shares have done 25% for four years. If you bought conservatively over the past three decades, you probably killed it in non-risk-adjusted terms, too. Anyway! Nice to meet all of you. Looking forward to many exchanges on this forum.1 point