All Activity

- Past hour

-

How to remove a deer from a fence

DooDiligence replied to DooDiligence's topic in General Discussion

I've heard similar stories from others after telling them about this. Apparently deer aren't very good at jumping fences. -

We need age limits on these bums!

-

It’s a real loss in the sense it hits book value, increases leverage ratios giving less financial flexibility and reduces the ability to grow premiums. I think the reason why Berkshire and Fairfax to a lesser extent keep a short duration is so they can take advantage of a hard market if it shows up the same time rates are going up like in 2022. It’s optionality that in theory is at the expense of higher yields but when the term structure is relatively flat, it doesn’t pay to extend duration. I can see a scenario where Fairfax extends duration but the yield curve will likely be much steeper. One of the features of FFH and BRK is there ability to take advantage of volatility as @Viking has pointed out. That’s with respect to premium growth as discusses above but also by holding more cash than they need to at the insurance subsidiaries. They can take advantage of big dislocations if they happen. Their equity holdings which are separately financed could do the same. It’s another reason FFH should trade at premium.

-

Yup, lot of them there.

- Today

-

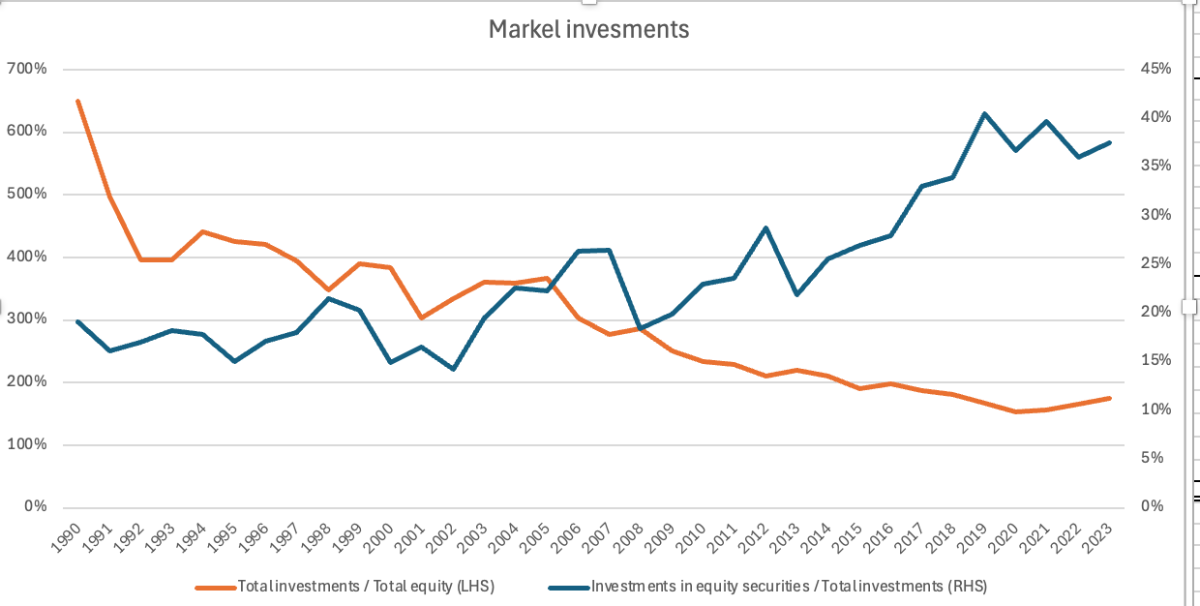

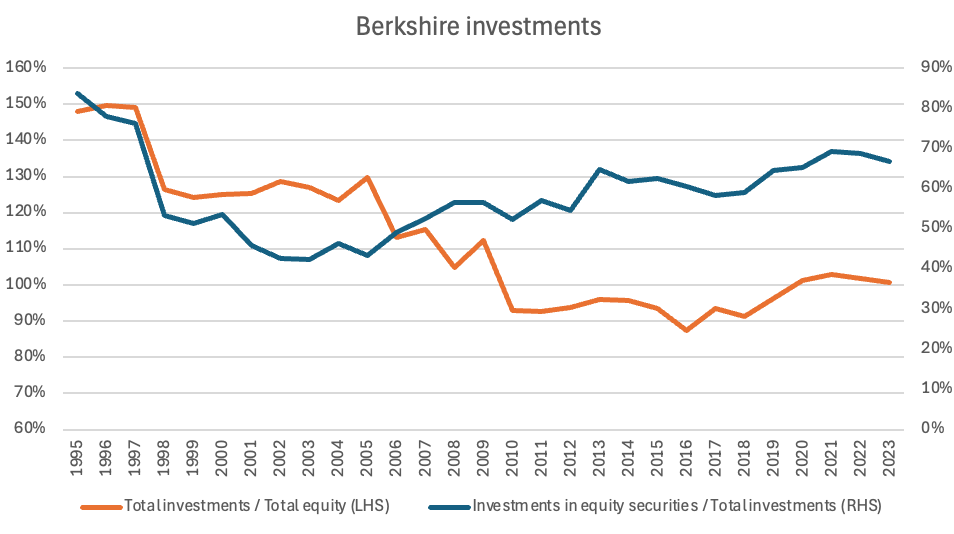

Thank you everyone for the feedback and in general I have to shout out to CoBF. For no company have I learned so much by just being engaged on a forum with so many informed posters who in my opinion are in the top 1% of investors (maybe even better) w.r.t understanding the nuances of Fairfax in a deep way. And the best part its free...When I presented, I mentioned a big part of my conviction building was reading Viking's book cover to cover (and 25 of Prem's annual reports in a row). RRR, I have thought about this question and it's a good one. There are two angles I would answer it with: i) The investment leverage an insurer operates with is linked to the mix of equity proportion in the investments. Equity requires more regulatory capital against it, fixed income less. So all else, if you have more equity in the book, you investment leverage has to run lower. Take a look at the leverage Berkshire and especially Markel had in earlier days. When they had a lower proportion of equity in the book, their investment leverage was much higher. These charts are evidence and should give you confidence that Fairfax is operating at a higher leverage partly because they can because their equity book is smaller than Berkshire and Markel. What is great about that set up today is that, have a meaningful part of the book in Fixed income is great because you earn 5% on it! Which is why today, Fairfax has the best set up with the highest ROE (as shown in my presentation). (In a zero rate environment it won't work as well i.e you would rather have lower leverage with as much in equities as possible). ii) The second lens I would use is to say, the amount of leverage Fairfax can take is highly regulated and scrutinised. So they are maximising the amount of leverage they can take based on regulatory constraints. The reason that's not risky as typical leverage because majority of the leverage comes from float which can be though of long term negative cost of capital debt. As opposed to debt which has positive cost of capital (ie interest payments) and covenants against it which can hinder you in the short term even if 1 year is bad eg. Covid but float doesn't have the same downside.

-

The way I look at it, Fairfax is leveraged, but it is a relatively locked in and safer type of leverage than a margin loan for example. I'm always hesitant to put leverage on top of leverage. Which is why I have kept away from that even when equities like Berkshire were in the doldrums. In retrospect, I could've made much better returns, but I think my sleep is worth a lot more to me. I'd rather let the masters take the leverage risk and show me good ROE numbers. As you pointed out there was a time just this past decade where Fairfax traded under 0.6x BV. In Fairfax case, I notice they are very careful with investing the float. The bond portfolio is purposefully kept to a relatively short duration often times even shorter than liabilities. Even though it's not a real risk because they don't sell these bonds, it's nonetheless a paper loss, and the market and rating agencies often consider this even if it's a transient paper loss. I think they watch this very closely. They may take additional risk on the equity side, but I think they are very careful with bonds. They're currently averaging 5% on the fixed income side without taking much risk. Thats frankly impressive. They've actually done better of late on the private equity side(cons/aff) than in publicly listed investments. It's just great to see them with so many options to reinvest cash.

-

@Viking and @Maverick47 have provided great responses. From my perspective, I have FFH at over 50% of my net assets and I’m adding my own leverage (via margin) to own it so I worry about leverage in terms of the real risk of impairment and about price volatility which could cause problems for me given my variable source of capital (the margin loans) forcing me to liquidate at the worst time. I don’t recommend anyone do this but I don’t lose sleep with respect to Fairfax based on the structure of the balance sheet, the conservatism of the valuations and the low starting valuation. The sources of Fairfax’s leverage are the float and long term non-callable debt with no near term maturities. @djokovic1 succinctly explained how Buffett thinks about insurance float for a high quality insurance company. I don’t see this leverage to be anywhere as risky as bank debt as for a well run insurance company it’s always growing. No near term maturities and long duration of issued bonds along with large revolving unused debt capacity also makes it unlikely the debt at the holdco becomes a problem. The balance sheet is conservative with respect to valuations on both sides as @Maverick47pointed out. Carrying value for the equity portfolio is well below fair value for not just what we know about (Eurobank, Poseidon etc..) but also for the positions where there is no reference price. It’s not hard to get $8b in fair value over carrying value which is 2x what we know about. The liabilities are also over stated due to the conservative reserving during hard market’s as was highlighted above. The normal interest rate environment also means holes are filled in very fast for negative surprises that show up in the equity portfolio or due to unusually large cat losses beyond reserve releases. Despite the low starting valuation for Fairfax, it’s still a stock. So bad things can happen. I have my leverage at 25% of assets so I can take a large drawdown before I need to start selling. Fairfax would have to trade below 0.95x BV. It was there a few years ago so of course we could go back but I’m making the bet that we won’t. It’s a risk I’m willing to take. What helps is that BV is growing 3-6% a quarter for the most part so my risk goes lower every day. The higher leverage should be why Fairfax trades at a big premium to MKL and BRK but the market structure keeps it at a discount. That’s the opportunity.

-

Maybe he will issue a "Taco" executive order.. Meanwhile, listen carefully to your buddy, Schumer:

-

This pretty much sums up 2026 for me!

-

Sold my FPE.DE (Fuchs Petrolub SE), KNOS.L (Kainos Group PLC) and the remaining half of my RBB positions

-

Sanjeev [ @Parsad ] Honestly I think understand good enough its's not any real importance to you [I may be wrong, btw.!] If it's bothering one, there is the solution to 'plant new trees' [like Elon Musk!]. Does it even matter to anyone? To me, it doesen't matter at all! - As long as you behave here as the person you are!

-

I hope trump pardons him. Game gotta recognize game.

-

You mean this happens regularly? Geez! Cheers!

-

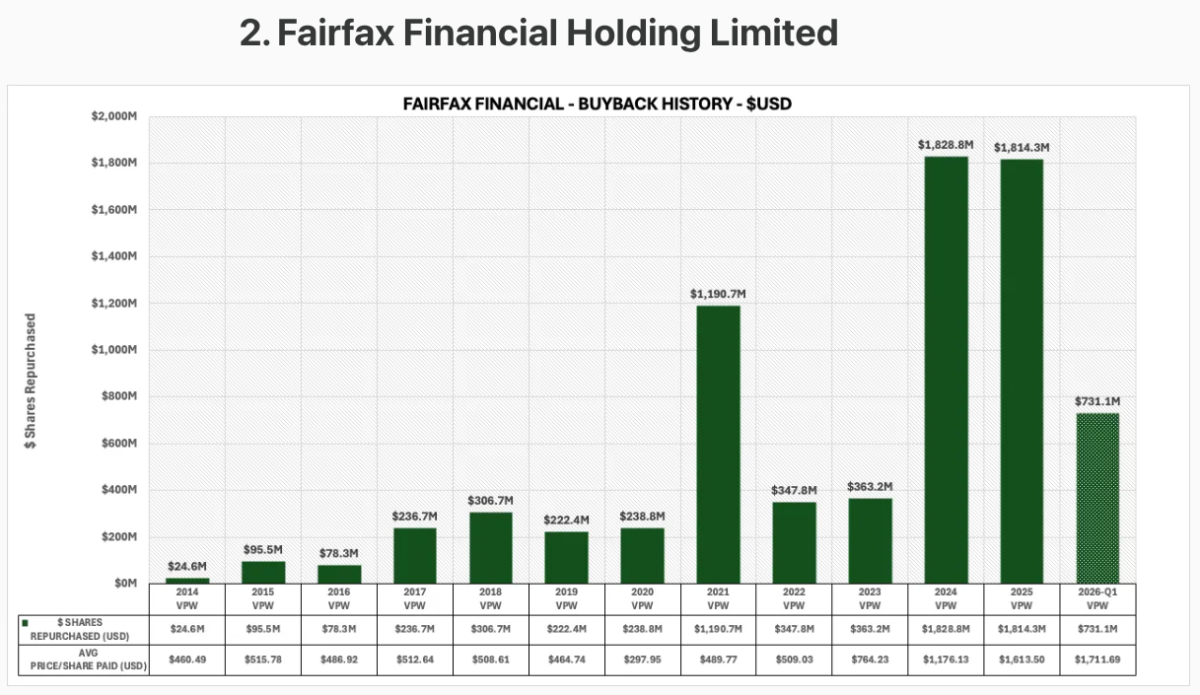

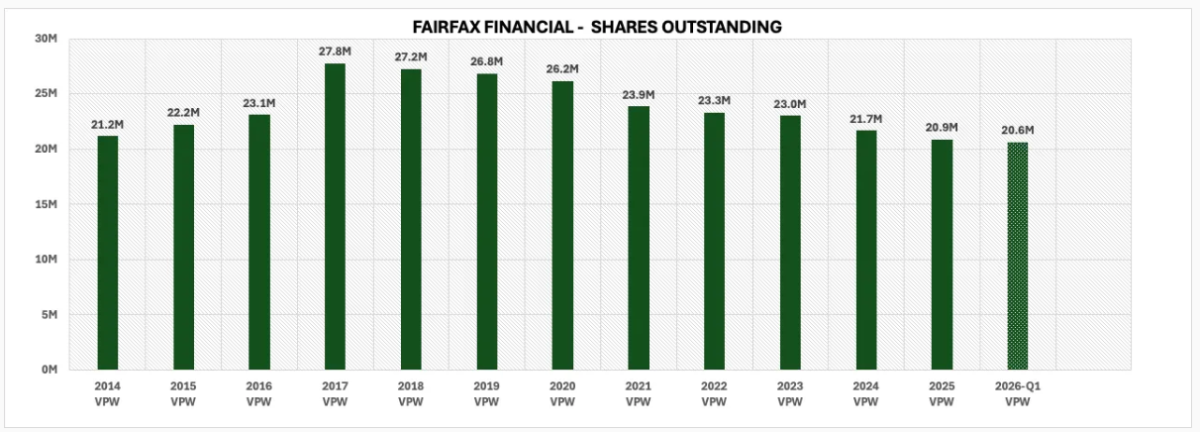

Tracking Buybacks of a select few companies here (https://mananainvesting.substack.com/s/buyback-tracker-series). Below is Fairfax Financial.

-

LOL! Hey I need one of those...does it come in rosemary or thyme...I have straighter hair! Cheers!

-

I don't have enough hair for a combover. I flip up the front a tiny bit to make it look like more, but there is still a bald forehead in front. Cheers!

-

https://www.telegraph.co.uk/us/news/2026/07/16/explosive-diarrhoea-outbreak-sweeping-america-donald-trump/ DOGE dopes strike again! Hopefully none here are reading this from the porcelain throne!

-

I Need a Laugh. Tell me a Joke. Keep em PC.

DooDiligence replied to doughishere's topic in General Discussion

maga dating.mp4 -

Buffett/Berkshire - general news

John Hjorth replied to fareastwarriors's topic in Berkshire Hathaway

Yeah @CassiusKing1, All good. -

Buffett/Berkshire - general news

CassiusKing1 replied to fareastwarriors's topic in Berkshire Hathaway

Greg seems to be more inclined to do buybacks. Hope they continue, plenty of excess cash coming into Omaha. -

CassiusKing1 changed their profile photo

-

Wow. Disgrace is right. Another bad apple in the White House. Maybe he can get a job with Paul Pelosi !

-

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

villainx replied to tnathan's topic in General Discussion

I am so bad at timing these things, used up a lot of cash at initial drop, didn’t average down much after. -

Agree, I do love the impact of the Euro players on the league. Their footwork and ball handling skills are amazing.

-

The Hill [July 16th 2026] : White House suspends teleprompter operator accused of placing bets on speeches: ‘Disgrace’ - - - o 0 o - - - So much for betting on insider knowledge as a maybe poor man working on POTUS' telepromter, with perhaps really not so much means - 'disgrace' - It's almost killing me!

-

Buffett/Berkshire - general news

ValueMaven replied to fareastwarriors's topic in Berkshire Hathaway

looks like buybacks have started up again!