gfp

-

Posts

8,121 -

Joined

-

Last visited

-

Days Won

20

Content Type

Profiles

Forums

Events

Everything posted by gfp

-

Well I am bullish but this is more just trying to replace a couple shares sold in my wife's IRA. I was hoping for more of a drawdown. There's always tomorrow..

-

You guys need to step up the panic selling. These fills are pathetic - do I need to post the Ge of Canada pdf another time?!

-

let me guess - you consider it a cash equivalent

-

I feel like this conversation repeats every year or so. Google “is Fairfax India a PFIC” or passive foreign investment company. Then you and your tax professional can explore the requirements of “following the rules” for a taxable US investor. Like I alluded to above, I’m sure many US investors own Fairfax India in taxable accounts and just don’t do anything. Not advice. Not a tax professional.

-

As a US investor, you should probably not hold FIH in taxable accounts. You are allowed to own it - there is nothing stopping you - it's just a huge pain if you follow the rules. The other option is to not follow the rules, which is common. Not advice

-

If you email the company they will probably send you one for free. They used to send out paperback versions but the last version they mailed me was hardcover. Try this email if you don't have a better contact over there -> [email protected]

-

Lets do it! "GE of Canada" !! Fairfax-Financial_FFH_MW_20240208.pdf

-

There's always the method that worked for Berkshire. Acquire a current TSX 60 company and they gotta add you

-

Even Prem sold his "excess" FFH. Sad

-

USAA is the best when the shit hits the fan. No shareholders. No adversarial stance toward members at all.

-

at least on my screen it looked like BTC traded $100,000 in the last few minutes

-

Didn't they already sell 11.5% of Anchorage to OMERS? Meaning the look-through ownership Fairfax India shareholders have in BIAL is less than 74%? Or did the OMERS / Anchorage deal never happen?

-

Here is some more color on the deterioration at GUARD from an AM Best note (h/t Kingswell substack) AM Best revised its outlook for some members of Berkshire’s GUARD insurance unit from stable to negative. “The negative outlook reflects sharp deterioration in GUARD’s underwriting results that began in the 2023 calendar year and worsened in the first nine months of 2024,” says the press release. But, on a happier note, AM Best lauded the insurer for taking “significant steps to improve its underwriting” such as discontinuing troublesome lines of business and bringing in an “almost entirely new senior leadership team tasked with restoring its operating performance”. The rating agency concedes that its concerns are “greatly mitigated by the group’s position as a subsidiary of Berkshire Hathaway” — and that a significant capital infusion from National Indemnity Co. in Q2 2024 shows that Berkshire remains committed to righting the ship at GUARD.

-

Fairfax went over 33% of Eurobank back when EUROB merged with Grivalia Properties, which Fairfax had a large investment in. (I should say large ownership stake, not large investment - FFH owned 51% of Grivalia, which itself had been spun out of Eurobank years earlier) The government would have had to approve the ownership level at that time. Prem has met with each Prime Minister since, so I'm sure he is on top of government relations. The dividends have just started to flow and I don't think Fairfax will sell any shares any time soon.

-

Latest presentation out of Berkshire Hathaway Energy, now 100% owned by the mothership https://www.berkshirehathaway.com/bhenergy/BHE2024InvestPresent.pdf note slides 19 and 20

-

Sorry if this was already posted - long letter from Warren https://www.berkshirehathaway.com/news/nov2524.pdf " By not stepping on any banana peels, I now remain in circulation at 94 with huge sums in savings – call these units of deferred consumption – that can be passed along to others who were given a very short straw at birth."

-

Other than very low interest rates at the time he borrowed I can't really answer that question for the big guy. He's not hugely short the Euro but Berkshire is short by issuing bonds denominated in Euros. General Re has a relatively small European investment portfolio that I suppose partially offsets some of that. Japan and Japanese debt issues have been his more recent focus. The eurodollar system (offshore synthetic dollar denominated instruments / derivatives not under the control of the US Treasury or Fed) is the de facto world currency. It is just a unit of account, like the metric system. Almost every large global currency related transaction has the USD on one side. Even someone swapping from Aussie to Euro will probably most efficiently / cheaply accomplish it by AUD -> USD -> EUR

-

Yes, Berkshire is essentially short Euros and Yen and is one of the single largest owners of US T-bills.

-

I don't know where that one came from (and it didn't really look much like Charlie to me..) but Etsy has a bunch of Munger "art" for sale https://www.etsy.com/search?q=Charlie Munger&ref=search_bar This lady in Canada, to the fkn moon!, has a lot of warren & charlie stuff. She found a niche LOL https://www.etsy.com/shop/ToTheFknMoon?ref=l2-about-shopname&from_page=listing And this hand painted example from Omaha - https://www.etsy.com/listing/1622185447/charlie-munger-abstract-painting?ga_order=most_relevant&ga_search_type=all&ga_view_type=gallery&ga_search_query=Charlie+Munger&ref=sr_gallery-1-32&pro=1&frs=1&content_source=248262301252d7421dee6baedb4ec502838b4dec%3A1622185447&search_preloaded_img=1&organic_search_click=1

-

I was looking at this off-road 911 Dakar and was happy to see the Charlie Munger quote and painting behind it -

-

perhaps ironically, the most likely thing to cause a downturn in the stock market would be a reduction of the deficit. Running a surplus would cause a depression.

-

BTW, I didn't know Fairfax owned 33% of the largest egg producer in Ukraine. https://interfax.com/newsroom/top-stories/104051/ https://open4business.com.ua/en/ovostar-owners-complete-squeeze-out-and-announce-delisting/

-

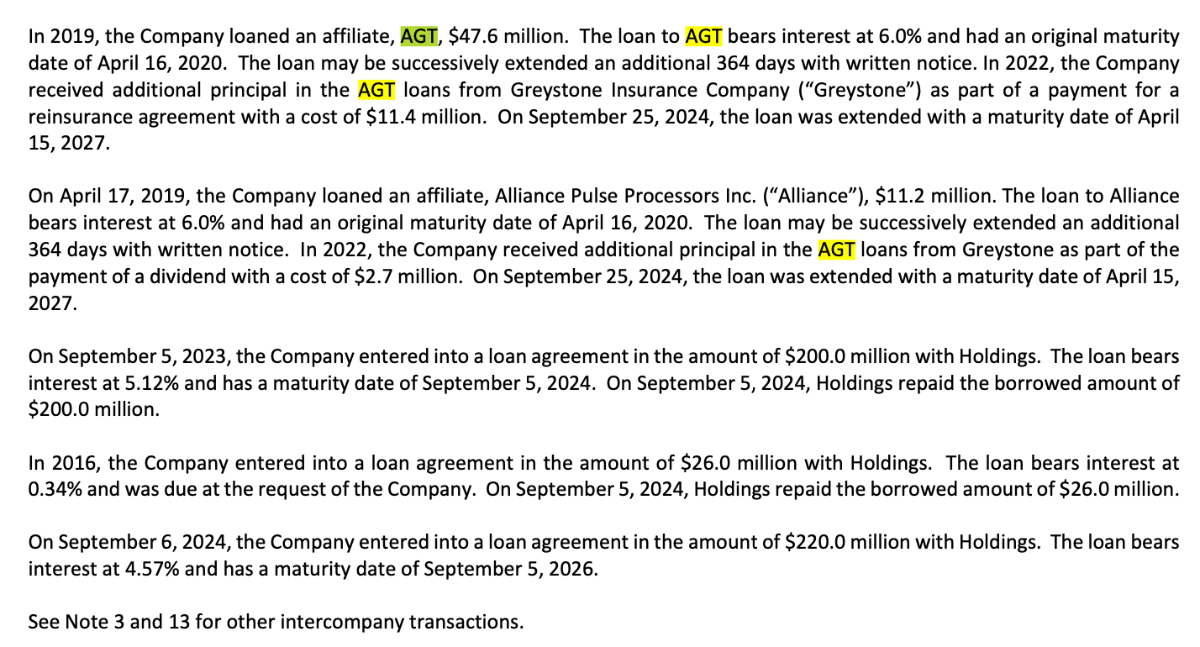

I found this in a Q3 Odyssey Re filing. Seems possible that Fairfax increased their ownership in AGT to 65.66%. AGT uses a lot of debt in their business and some of that debt does not show up on the consolidated financial statements because it is intercompany. Much like NICO at Berkshire. ("the Company" below is Odyssey. "Holdings" is Odyssey Group Holdings)

-

It would be consolidated, not equity method

-

https://www.eriksencapitalmgmt.com/investor-letters