gfp

-

Posts

8,121 -

Joined

-

Last visited

-

Days Won

20

Content Type

Profiles

Forums

Events

Everything posted by gfp

-

The company is a lot bigger but also I would assume it reflects greater participation in the various employee stock ownership schemes. Overall a good thing if employees are owning stock and Fairfax is using cash to buy the stock it uses for compensation.

-

Yeah they did a great job with the call. Prem wasn't even "with us today" - lol. I think he really intended to step back from the conference calls before that Muddy Waters report but got sucked back in for a couple after that short report.

-

Sounded to me like most of it was first mortgage secured by the actual apartments

-

Vacatia investment sounds like a high yield structure - only $25m in equity, 50/50 with the operating partner ($50m total). The rest of FFH's investment is 13.5%, 9.5% and SOFR+4%

-

$500-750m pre-tax loss estimate on wildfires. some or possibly all covered under "cat margin" in the quarter "primarily on reinsurance" Odyssey, Brit and Allied World typically 1 - 1.5% of industry losses. Industry losses cited at $35-45 Billion. Estimating closer to 1.5% - "the high side" since it is a reinsurance event

-

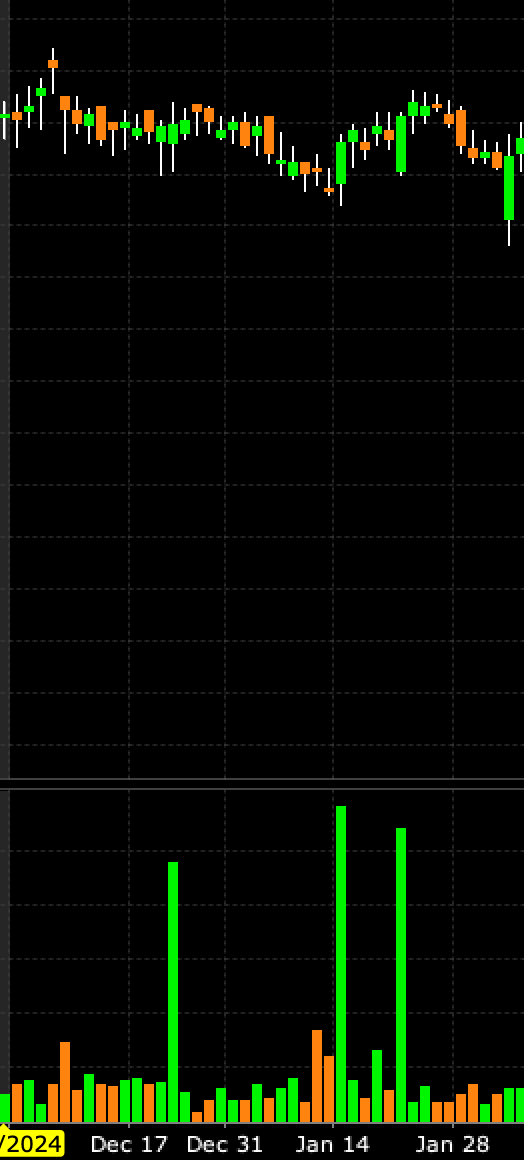

So we see the 12/20 block trade on the chart. I had assumed the two big January block trades were just the counterparties crossing shares once a year around the dividend but maybe we can ask them on the call if they terminated anything additional on the TRS in January.

-

Thanks - I see that now. I thought the ~340k run rate of repurchases was just their normal course issuer bid but I guess they used this block for most of it. Presumably if they hadn't bought this block of stock it would have hit the market and impacted the share price in December.

-

Yeah it's no fun when cash starts flowing out at the exact time you want to be getting aggressive allocating capital. I don't think Buffett loved having that huge notional short put position during the financial crisis even though zero cash flowed out and he knew they were fine to hold through expiry. You don't want to hold a derivative position like this through the last dollar - just the meat in the middle.

-

https://www.sec.gov/Archives/edgar/data/927066/000095017025020189/xslF345X05/ownership.xml https://www.sec.gov/Archives/edgar/data/927066/000095017025020183/xslSCHEDULE_13D_X01/primary_doc.xml First of the required quarterly sales of DaVita shares by Berkshire entities back to DaVita. The BRK group isn't allowed to stay above 45% so once each quarter they have to sell stock back to DaVita based on the VWAP that DaVita repurchased stock at in the quarter just passed. So GEICO sold stock at $156 on a day it traded for $173 but what can ya do...

-

I'm not sure I followed your post but that doesn't mean it isn't right. Basically it's just a financing deal - the banks hedge their end of the contract so they aren't taking any directional risk. That could mean balancing a portion of it with other market participants that want to put the opposite TRS on (unlikely in the case of Fairfax stock but quite likely for other assets) or, as in this case, just buying the shares to offset the directional risk completely. The fees and interest rate are where the bank makes money. They are the bookie, not a fellow gambler. The counterparty also gets the dividend, which is factored in to what they charge FFH. There is a cost to Fairfax to keep the trade going. But when the contracts are terminated - the hedge shares become available to either hit the market for sale, or as is more likely here, get bought up by indexers and closet indexers when Fairfax gets added to the S&P / TSX 60 index.

-

I get what you are saying but obviously they both terminated a portion of the TRS and bought shares for cancellation under their normal course issuer bid in the same quarter so they are certainly willing to both reduce the size of this atypical derivative trade while still continuing to repurchase stock. Likewise it made sense for Prem to sell hundreds of millions of dollars worth of FFH stock at a price that was also attractive for the company to be the buyer on the other side. I believe that when Fairfax notifies a counterparty that they will not be renewing a TRS contract they can certainly negotiate for the purchase of the underlying block of shares that has been held by the counterparty to hedge their side of the TRS. The big Canadian banks that facilitated this TRS trade were not short FFH shares this whole time. They likely have large blocks of stock that can be sold if FFH doesn't negotiate for their purchase upon termination. So if you are buying in your shares and you know of some big blocks it is possible you may simultaneously exit TRS exposure and buy the underlying hedge shares. Or not. But it wouldn't surprise me if it happens.

-

Thanks Viking that is helpful. Doesn't answer my question but it helps to see it all laid out that way over multiple years. I'm just trying to understand what the impact of closing out the TRS on FFH shares will be if the company decides to put up the cash to buy the shares from the swap counterparty (thus turning them into actual share repurchases). This quarter it seemed like they did this, partially, for $240m dollars worth. But it had no effect on effective shares outstanding even though $240 million bucks went out the door. Which lead to my question.

-

"the company purchased 207,974 of its subordinate voting shares for treasury at a cost of $240.4 million" Straight from their release. So where is this 208k shares in the change in "effective share count" ?

-

So from the numbers in my post above, they purchased and cancelled 334,047 shares in Q4. The effective share count went down by 322,137 shares. No big deal, employee purchases, minor net issuance, etc. Where is the other $240 million worth? I'm saying it must have always been counted as treasury stock in the "effective shares outstanding" language. Which means so are all the other TRS shares right?

-

Effective Share count end of q3 vs end of q4 " During 2024 the company purchased 207,974 of its subordinate voting shares for treasury at a cost of $240.4 million and 1,346,953 subordinate voting shares for cancellation at a cost $1,588.4 million, or $1,179.24 per share." "At December 31, 2024 there were 21,668,466 (December 31, 2023 – 23,003,248) common shares effectively outstanding." vs: " During the first nine months of 2024 the company purchased 1,012,906 of its subordinate voting shares for cancellation at an aggregate cost of $1,127.1 million. On September 30, 2024 the company renewed its normal course issuer bid." At September 30, 2024 there were 21,990,603 common shares effectively outstanding.

-

Yeah that is probably the 12k shares mentioned above. I don't think it explains $240 million worth of stock edit: I wonder if this means that they have been counting the entire TRS share count as treasury stock this whole time and that is why they term it "effective shares outstanding"

-

I agree that those look like the shares that went into treasury stock, but they didn't seem to affect the "effective shares outstanding" calc - which declined by a bit over 300k shares as expected (334k or 322k depending on how you count)

-

https://www.globenewswire.com/news-release/2025/02/13/3026350/0/en/Fairfax-India-Holdings-Corporation-Financial-Results-for-the-Year-Ended-December-31-2024.html

-

oops! posted the wrong press release!

-

End of year share count is: "At December 31, 2024 there were 21,668,466 (December 31, 2023 - 23,003,248) common shares effectively outstanding."

-

" On December 20, 2024 the company increased its equity interest in Peak Achievement Athletics Inc. ("Peak Achievement") to 100.0% by acquiring the 42.6% equity interest owned by Sagard Holdings Inc. and the 14.8% equity interest owned by other minority shareholders for purchase consideration of $765.0 million. The company was required to remeasure its existing equity accounted investment in Peak Achievement to its fair value of $325.7 million upon consolidation and recorded a pre-tax gain of $203.4 million in net gains on investments in the consolidated statement of earnings, which reflected Peak Achievement being now carried at approximately 8.5 times free cash flow. Peak Achievement is engaged in the design, manufacture and distribution of performance sports equipment and related apparel and accessories for ice hockey, roller hockey and lacrosse, under brands such as Bauer Hockey, Cascade Lacrosse and Maverik Lacrosse."

-

"The company recorded net gains of $1,033.5 million (fourth quarter of 2024 - $341.9 million) on equity total return swaps on Fairfax subordinate voting shares. During the fourth quarter of 2024 the company closed out derivative contracts on 203,800 Fairfax subordinate voting shares with an original notional amount of $68.5 million (Cdn$88.9 million). At December 31, 2024 the company continued to hold equity total return swaps on 1,760,355 Fairfax subordinate voting shares with an original notional amount of $664.0 million (Cdn$846.1 million) or $377.19 (Cdn$480.62) per share."

-

https://www.globenewswire.com/news-release/2025/02/13/3026345/0/en/Fairfax-Financial-Holdings-Limited-Financial-Results-for-the-Year-Ended-December-31-2024.html Book value per basic share at December 31, 2024 was $1,059.60

-

I'm just a degenerate trader that needs to pay his bills and keep food on the table

-

Back on the Q3 call they were still having Milton losses trickle in slowly so they didn't have a full picture, but this is what they said at the time according to my notes: " From the conference call they are predicting Milton losses "within the cat margin" and not having much of an affect on the expected combined ratio for Q4. They mentioned claims are coming in slow so it is still uncertain but obviously a much better outcome than the direct hit on Tampa they had modeled. For "cat margin" they mentioned they have been absorbing about $1 Billion of cat losses annually, maybe 5 combined ratio points "