gfp

-

Posts

4,806 -

Joined

-

Last visited

-

Days Won

8

Content Type

Profiles

Forums

Events

Posts posted by gfp

-

-

The same kind of volume spikes happened last January - I assume it has something to do with the timing of the dividend, the counterparties to the TRS and the calendar year.

-

1

1

-

-

12 minutes ago, cwericb said:

New high ($1302) this morning and high volume (nearly 200,000 shares traded). So far.

The opening trade was 185,000 shares

-

11 minutes ago, linus_md said:

https://maps.app.goo.gl/FbA8xynQW3Zojpfm6?g_st=ic is this the company?

Ha! Well maybe Avi's company is not great at customer service but Charlie sure was enjoying whatever they were telling him about the operation.

-

A happy guy in his happy place

-

I never met Charlie personally, but my impression was that he had a huge number of extremely high quality, stimulating friends, an absurdly active social life for a widower of his age (or really anybody of any age) and was in love with the independence his wealth gave him. He pursued many personal passions from the large catamaran to fishing to architecture. He loved projects like his multifamily apartment business with Avi and planting all those trees and pouring money into those apartment buildings to make them as nice as they could be as long term assets. (I kind of hope he gave that business to Avi in his will - we may never know). Charlie's family has said many times that it's not the "real" Charlie you see sitting up there next to Warren in the meetings, just the image he had cultivated for himself as the straight man sidekick.

Maybe you think he was miserable because of his appearance or maybe you think he was miserable because interviewers tended to ask him about topics they knew he was likely to give them a classic Charlie curmudgeon zinger soundbite.

Either way, I think you are wrong.

edit: I should add, he was literally constantly laughing

-

My impression was that "corruption" was just the cover story for removing people who might be critical of Xi from important government bodies. But what do I know.

-

Berkshire put out a short press release also. We should be able to see the price paid in the Q1 filings when they come out.

-

No surprise, but the CEO of Sumitomo commented to Barron's on Berkshire continuing to buy all 5 trading houses -

"

...

At the time, Berkshire Hathaway said it may increase its holdings depending on price, but that Buffett had pledged that it would not purchase more than 9.9% of any of the five companies before seeking approval from the respective boards.

That time may soon be coming, according to Masayuki Hyodo, the CEO of Sumitomo Corporation, one of the five general trading companies in which Berkshire has invested. Those investments represent its only public holdings in Japan.

“Through the information I have, it is increasing—not only Sumitomo, but all five trading companies. His share is increasing every day,” Hyodo told Barron’s in an interview on the sidelines of the World Economic Forum late Monday.

Barron’s has asked Berkshire Hathaway for comment.

Berkshire sold 122 billion yen ($837 million) worth of yen-denominated bonds in November, an offering that sparked speculation that Buffett may be raising cash to increase investments in Japan."

https://www.barrons.com/articles/warren-buffett-berkshire-hathaway-japan-sumitomo-davos-9d9310a3

-

When I was growing up, a wealthy older guy explained to me that is wasn't the ratcheting up to the bigger house, per se, that killed you - it was the fact that none of your furniture or stuff "worked" in the larger house. So it's not just the house. It's all new furniture, rugs, window treatments, art, design fees, on and on. You might love your couch in the 1500 sq. ft. place but as soon as you stick that thing in the living room of your new 4000 sq. foot house it just isn't scaled appropriately. On and on like that. One of the main reasons furniture sales plummet when mortgage rates keep everyone in their same house.

-

3 hours ago, nwoodman said:

Could I trouble you for a short anecdote on Dad and how he came to be invested in Berkshire in the first place? I realise you are travelling so no hurry.

Charlie can answer for himself obviously, but he has shared the story many times of Marshall Johnson of McDaniel Lewis and Co. in Greensboro, NC putting many of his clients in the same great stocks. Seems that quite a few families in that region (if they were wise enough to hold the stocks) owe a lot of thanks to Mr. Johnson.

-

5 minutes ago, Haryana said:

You got that right.

The point is that there are stocks and fund managers out there who have vastly outperformed Berkshire but nobody will know because of the Buffett brainwash syndrome and the scam of charts without the dividends.

Well not me, I had my entire net worth in Southern Copper since 1996 so I'm one of the special ones. (jk)

-

46 minutes ago, Haryana said:

No.

Next hint: it trades on NYSE.

Well it looks like Southern Copper to me.

-

22 minutes ago, Haryana said:

I would like to confirm that if the dividend is paid to shareholders of record on Jan18 and it takes 2 days to settle then the shareholders upto Jan16 will get paid and therefore the ex-dividend date should be Jan17 on Wednesday or is it Thursday?

Sorry, I was sloppy with my wording. Shareholders of record on Jan 18th, so you would have to own the stock by Jan 16 to receive the dividend. (with Jan 17th being the ex-div. date)

-

12 minutes ago, Tommm50 said:

Large volume on FRFHF the last few days, pattern seems to be price rises in the morning session and sells off as the day goes on. Very large volume on FFH.CA today with no movement in price. Any insights into the activity? Related to building a position prior to year end results announcement?

I would assume it is more related to the stock going ex-dividend on Thursday of next week than the results announcement over a month away. There are also usually some large share crosses around the turn of the year related to the total return swap counter-party but I haven't noticed anything.

-

-

Fairfax re-opened December's 10 year note offering and borrowed another $200m on slightly better terms, FWIW

https://www.fairfax.ca/press-releases/fairfax-declares-annual-dividend-01-09-2024/

(no clue why this is the file name, but it is the correct link to the note offering announcement)

-

Oh wow, yeah I guess I am bigger into "micro-caps" than I realized.

-

For very small stuff, Tim's investor letters and fund are very good. He also posts occasionally on twitter. (He used to post on this board infrequently) The problem with a nano-cap forum is that many of these don't trade much and discussing them publicly just guarantees you will have competition on the bid.

https://www.eriksencapitalmgmt.com/investor-letters

https://twitter.com/eriksen_tim

-

-

9 minutes ago, John Hjorth said:

Isen't there to some degree confusion about the numbers [money sums] involved in the description of the disagreement with the Haslams?

Not sure what you mean here, but there isn't really much disagreement over the number the formula spits out (for the final 20%). Berkshire had it at $3.23 Billion on their most recent 10-Q and the Haslam family would be happy with that number.

I think Berkshire believes, for good reason, that the EBIT that feeds into the formula that spits out the above number has been manipulated and would prefer to plug in a more normalized "un-gamed" EBIT in a year or two. That was not part of this week's scheduled trial however.

The Haslam's suit was mostly just not trusting Berkshire to use the above figure from their 10-Q. They wanted to know for sure, up-front, that Berkshire was not going to try to screw them, because they are used to living in a world where everybody is trying to screw their partners. The original contract had dispute resolution protocols for dealing with disagreements over the figure. The Haslams just wanted a guarantee they would know the exact number before they made a decision to exercise their put.

But there is value to putting it behind you and value to minimizing risk to Abel's and Berkshire's reputations. To Berkshire, I doubt it is predominantly about a further "unjust" $1 billion transfer to the Haslams. They already got gamed for a bigger figure than that and they knew it. Chaulk it up to character and incentives and file it with the rest of the lessons learned.

-

4 minutes ago, ValueMaven said:

Honestly Pilot was never going to win.

Remember that this trial was narrowly focused on the application of push-down acquisition accounting that inflated depreciation and amortization and not any of the "illicit incentive" payments.

If a settlement pushes the Haslam's put exercise out a year, it gives Berkshire's side a change to put up a "clean" year of EBIT to plug into their formula. Alternatively they could have just agreed on a number to part ways permanently with the Haslams.

-

Yes that is a good guess and I assume it is correct.

-

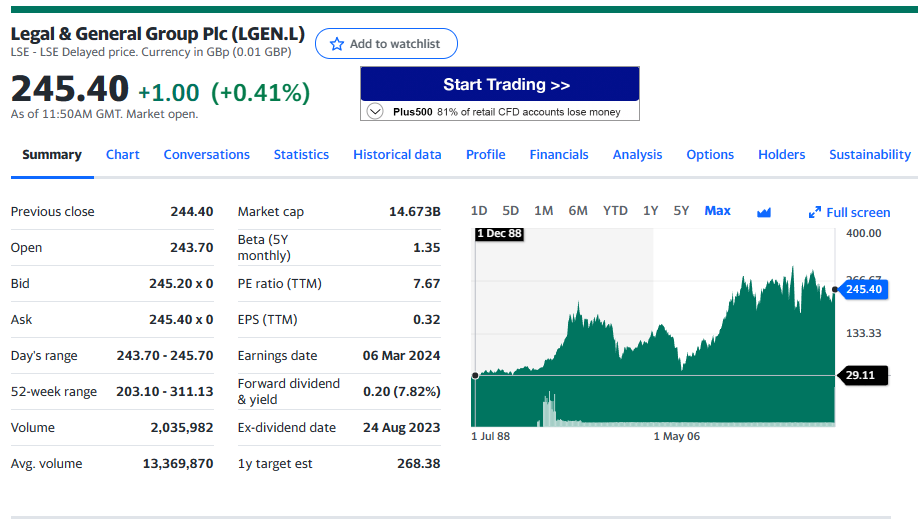

17 minutes ago, Sweet said:

Has anyone looked at the UK company Legal and General?

It is an insurance company (among other things) and has a fat dividend and a relatively low PE.

It has negative revenue in the past few years, something I cannot get my head around. The details of this company are over my head unfortunately.

A big annuity business like L&G with a big traditional corporate bond investment portfolio will trade in the short term with the direction of interest rates. So keep in mind your expectations for UK & US interest rates going forward.

-

You know that feeling when Berkshire rallies "unexplained" while the indices sell off? Not usually followed by a great time for stocks.

The sketchy world of Block Trades

in General Discussion

Posted

I mean, those kind of shenanigans sound like they would make it easier to beat an index fund. But I guess you said "most people" and most people aren't going to beat the S&P regardless of the opportunities these type of shenanigans regularly create.