gfp

-

Posts

4,806 -

Joined

-

Last visited

-

Days Won

8

Content Type

Profiles

Forums

Events

Posts posted by gfp

-

-

2 hours ago, mattee2264 said:

The economy seems to do just fine with higher interest rates. The main people complaining are investors who need low interest rates to pump up their long duration assets such as Big Tech.

You really think it's investors in Big Tech that are complaining? I'm thinking it is commercial property owners and their lenders that are obsessing over the dot plots.

-

2 hours ago, mattee2264 said:

What I always find scary is how correlated the S&P 500 is to the Fed balance sheet. Since 2009 the Fed balance sheet has increased fourfold. And the S&P 500 has as well.

It does beg the question as to how much of this long long bull market is simply just the result of asset price inflation.

And of course the Fed has no serious intention of decreasing its balance sheet especially as the banking system will continue to need bailouts and the market will taper tantrum if QT ever picked up any kind of speed.

I'm not sure what the difference would be between a bull market and asset price inflation, but I wouldn't read to much into any correlation with the Fed balance sheet and the S&P 500. QE doesn't create "real economy" money that can be invested in stocks. Excess bank reserves don't do much at all since US bank lending is not constrained by bank reserves. I believe QE does basically nothing, but it is possible that the way the US did it, there was a tightening of MBS spreads that goosed the refinance boom a little bit more on the margin that what would have occurred with slightly wider spreads.

-

1 minute ago, DooDiligence said:

I'd crap my pants if it was Nintendo.

Well he can buy Nintendo any time he wants and it won’t show up on a 13-F.

-

5 hours ago, jbwent63 said:

I'm looking forward to tomorrow's 13-F filings....in particular if there are amendments to the 9/30 filing to remove the requested permission to not disclose a position, or if that permission is still granted. Is there any scuttlebutt as to which name it could be?

There is no scuttlebutt on what it could be except that it almost certainly falls into the category "Banks, insurance and finance" on Berkshire's filings. We couldn't figure out what it was by looking at the NAIC filings because it was hidden within the Harney Investment Trust.

-

3 minutes ago, SafetyinNumbers said:

Makes me think that’s just the CAGR to the end of Q3, which makes sense if they didn’t want to release financial information early.

Good point - that sounds right to me, given I expect higher reported book value growth in q4.

-

17 minutes ago, Maverick47 said:

Using the same sort of calculations I’m estimating a 34.6% gain in book value in full year 2023, not far off the 33.3 non annualized value through Q3. So maybe an $884 book value per share when we see the full year report Thurs evening?

Hard for me to estimate but I would expect a pretty decent mark to market gain on the bond book for the quarter.

-

You should not use the 17.8% BVPS growth figure to compare to the 18.9%. You should use the 18.5% figure that includes dividends.

-

1 minute ago, MMM20 said:

The question is if/when this ever becomes the consensus view. Maybe a fool's errand to even think about.

I wouldn't hold your breath. Berkshire is still being valued based on price-to-book value all these years later.

-

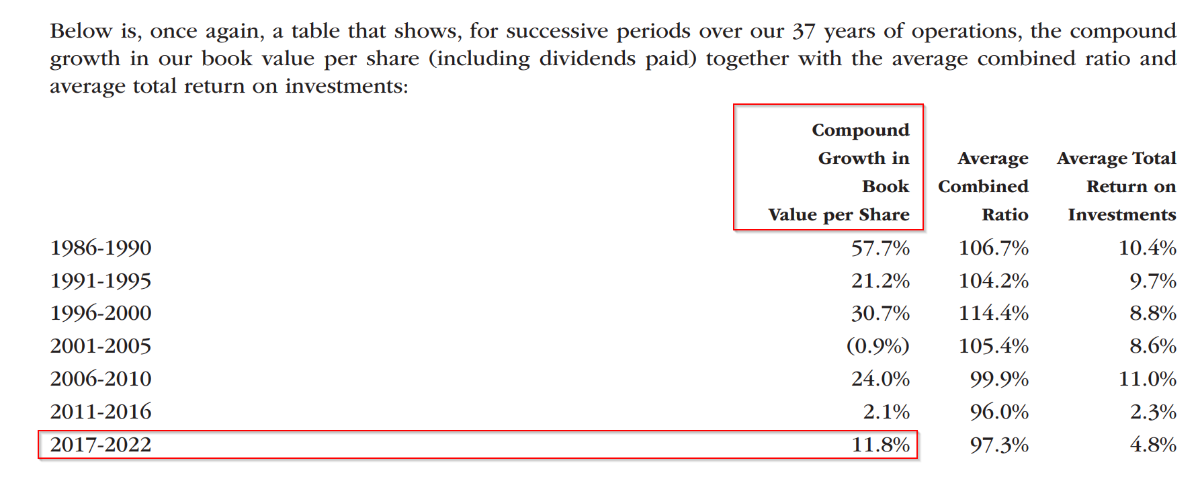

46 minutes ago, glider3834 said:

Looking at MW chart table below for years 2017-22 - how does that reconcile with Fairfax's number from their 2022 Annual report for 2017-22 period? Or am I missing something?

The Muddy Waters graph of book values appear to be each year's CAGR in Book value since some arbitrary day they are calling "the GFC." So it isn't the book value growth for those years, but those end-dates.

The actual BV growth for those years (which is probably what most casual observers understood it as) was this:

2017: +24.7%

2018: -1.5%

2019: +14.8%

2020: +0.6%

2021: +34.2%

2022: +6%

(and 2023 comes out this week and should look pretty good)

* one thing about posting Fairfax's actual annual results as above is that the bumpiness goes against the narrative that this is a GE-style smoothed manipulator.

-

It's funny because my hometown team was not involved in that game but Nola has such a deep rivalry and hatred for the Atlanta Falcons that it is not uncommon to see murals of the 3rd quarter score, flags memorializing the score, etc, all over town. There was even someone that rented billboards memorializing the choke/comeback.

-

We use a lot of hot sauce in my household and Huy Fong Sriracha is still not available in stores down here. We have been buying the products directly from Underwood Ranches, the grower that Huy Fong tried to replace. The Sriracha is slightly spicier but works just fine for us. We also use a Sriracha out of Thailand under the Polar brand name that is very good but sweeter than the Underwood Ranches. We still have Huy Fong Sambal Olek in our fridge but the Underwood Sambal is also very good. One of my friends loves the yellow Trader Joe's "sriracha." We don't have any of that so far. Just say NO to Tabasco. I don't think anybody actually wants Tabasco I think it is just ubiquitous and well distributed. I even know some McIlhenny family members and still won't touch the stuff. Maybe the green or chipotle but never the original. Definitely not their "sriracha" product - blech.

-

Kind of funny that they are going to phase the margin increase in "over multiple days" and then say those days are from after the close on Friday to trade date Monday. That's one day, not phased in.

-

1 hour ago, ValueMaven said:

FFH is a VERY dangerous stock to short unless you think its a $0

There is a controlling chairman who controls about half of the 25M shares o/s. There are 2.2B shares outstanding of BRKB btw

You have a long-term holding base, figure thats several million shares ... The true float of FFH is very low!!! This could actually blow-up on MW.

Why do you say Prem controls half of the shares? There are not 25m, there are 23.1 million shares. (brk.b has 2.166 billion b-share equivalents outstanding)

-

38 minutes ago, SharperDingaan said:

Sadly, I'm nowhere near as eloquent as James Joyce!

Just to throw some random numbers out ...

Start at 1400 pre-announcement. Short 1,000 shares, long 10 out-of-the-money puts at 1300, publish report, media tour

Drive the price < 1300 by expiry date. Have the 1,000 shares assigned, off exchange. Long 20 calls between 1300 and 1400.

AR is announced, squeeze the shorty! Price moves to 1500, sell the 20 calls at 1500, return the 1,000 shares to the lender.

Buy today at 1260. Sell at 1500 post AR (240 profit), buy back at 1260 on MW round-2 (240 profit). MW eventually walks away, shares sold for 1500 (240 profit). Total gain of 720 on a 1260 investment is 57%. If you only capture 2/3 of this ... about a 38% return.

Just one of many possibilities .....

SD

Hopefully, a good $300+/share on the turn before any option/margin leverage!

We would also be very surprised if MW didn't intend to exercise on existing options, as the mechanism by which to raise the shares to repay the short loans; plus accumulate some additional - offered for a buyback. We also expect them to have used the drop to lay in a stack of out-of-the-money calls; FFH buys in the stock at a price well < 1401, MW walks away, the price quickly returns > 1401 & all those calls go deep in the money.

What options?

-

3 hours ago, SharperDingaan said:

Hopefully, a good $300+/share on the turn before any option/margin leverage!

We would also be very surprised if MW didn't intend to exercise on existing options, as the mechanism by which to raise the shares to repay the short loans; plus accumulate some additional - offered for a buyback. We also expect them to have used the drop to lay in a stack of out-of-the-money calls; FFH buys in the stock at a price well < 1401, MW walks away, the price quickly returns > 1401 & all those calls go deep in the money.

.... Now of course, if an enterprising lad had learnt from ericopoly, and also knew how to work this trick!

Interesting times

SD

Honestly I can never make any sense of your posts.

-

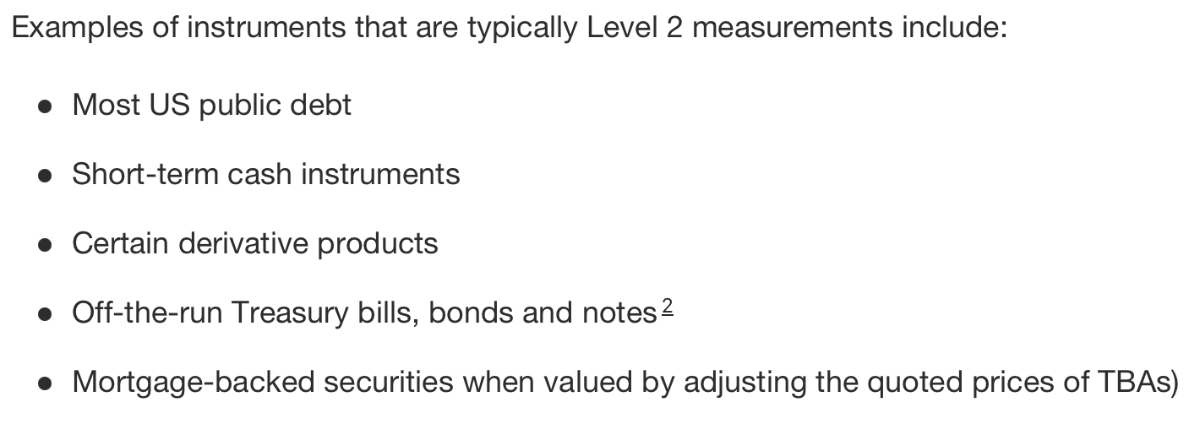

10 minutes ago, LC said:

Thank you, I must have missed your post - so I'm guessing mostly the off-the-run treasuries, so no big deal at all.

Some accounting reading for anyone interested: https://viewpoint.pwc.com/dt/us/en/pwc/accounting_guides/fair_value_measureme/fair_value_measureme__9_US/chapter_4_concepts_u_US/45_inputs_to_fair_va_US.html#pwc-topic.dita_1533084709184712

Carson Block in shambles.

Yeah, from your link:

-

22 minutes ago, LC said:

The only outstanding question I have is on the Level 2 classification for FFH's bond portfolio. My guess is there are covenants/options linked to these bonds which cause the L2 classification. Even with that question mark outstanding, the interest income generated from these bonds is observable so it is really more of a curiosity vs. a concern.

I already posted about this, but all off-the-run treasury securities are classified as Level 2. Also any bond that requires a dealer quote to mark to market is also a Level 2 security. So that leaves basically on-the-run treasuries, bills, cash equivalents, as the only level 1 bonds.

-

18 minutes ago, Gmthebeau said:

Bitter little man cuz your stock crashed. Ok, the analysis was 2 times accused of creative accounting just because you don't understand the analysis doesn't make it less useful.

We will see if it "crashes." So far we are re-living the morning of January 17th, 2024 (at least in USD terms). I did most of my purchasing yesterday so I won't have much capital to buy a crash if it comes.

-

1 minute ago, Intelligent_Investor said:

Wouldn't that be insider trading if Muddy Waters shorted due to knowing insider info that a large shareholder was selling? That sounds pretty illegal to me

That's not what "insider information" is. Material non-public information is about the company itself, not the behavior of other shareholders.

-

I think they are talking about the US over the counter ticker FRFHF.

Interestingly, it seems like Interactive Brokers changed margin requirements for FRFHF mid-day today to 100% initial and 100% maintenance. FFH shares remain at 30% initial and 30% maintenance.

-

Block tries to imply that Fairfax holding much of their government bond portfolio as Level 2 assets is somehow strange and untoward and ripe for manipulation.

Off-the-run treasury securities or really any bond that requires a dealer quote to get a valuation is Level 2. That is how off-the-run securities are supposed to be classified.

-

That zeroes - tv interview is better than the CNBC interview, that's for sure. He still does a lot of assigning motive as being accounting write-ups without mentioning what they wanted/needed the money they borrow from OMERS for.

He seems to think that APR Energy has something to do with WTI oil prices because it has "energy" in the name.

He is right, of course, that the 10% of a subsidiary deals with the full intention to repurchase the interest is fixed rate preferred equity financing. I don't think that has been hidden. It's not structured as debt, it has a fixed, known cost, the partner fully expects to have the equity interest repurchased by Fairfax. Fairfax fully expects to repurchase the equity interest. It IS financing. I don't think that's a bombshell. But I guess it looks bad if you assume the motive was the accounting write up.

https://www.zer0es.tv/big-announcements/fairfax-financial-the-oracle-of-nothing/

-

Might be lost in the news of the morning, but Prem resigned from the Blackberry board of directors today (as of 2/15)

"in connection with the Company's repayment at maturity of its $150 million principal amount convertible debentures held by Fairfax"

-

What good are record earnings when Farmers Edge is bleeding millions!!!?

Have We Hit The Top?

in General Discussion

Posted

Sure, wrong-way macro guys are complaining as well. But if I'm on year 4 or 5 of a 5 year commercial loan at 4.5% and it's about to reset at 8+% with banks willing to do 55% loan to value - I'm watching that short term rate and interested in the timing and magnitude. And the banker is too.