gfp

-

Posts

4,809 -

Joined

-

Last visited

-

Days Won

8

Content Type

Profiles

Forums

Events

Posts posted by gfp

-

-

-

"

PacifiCorp increased its liability for estimated pre-tax probable Wildfire losses, before expected related insurance recoveries, by $1.4 billion in the third quarter and by $1.9 billion in the first nine months of 2023. Expected probable Wildfire losses, net of expected insurance recoveries, were approximately $1.3 billion in the third quarter and $1.7 billion in the first nine months of 2023. Such amounts were included in energy operating expenses in the accompanying Consolidated Statements of Earnings. PacifiCorp’s cumulative charges to date for estimated probable Wildfire losses were $2.4 billion through September 30, 2023."

-

Looks like they sold around 12.8 million CVX shares (~$2 Billion worth) in the quarter. Not hugely surprising given recent trends in their CVX trading.

-

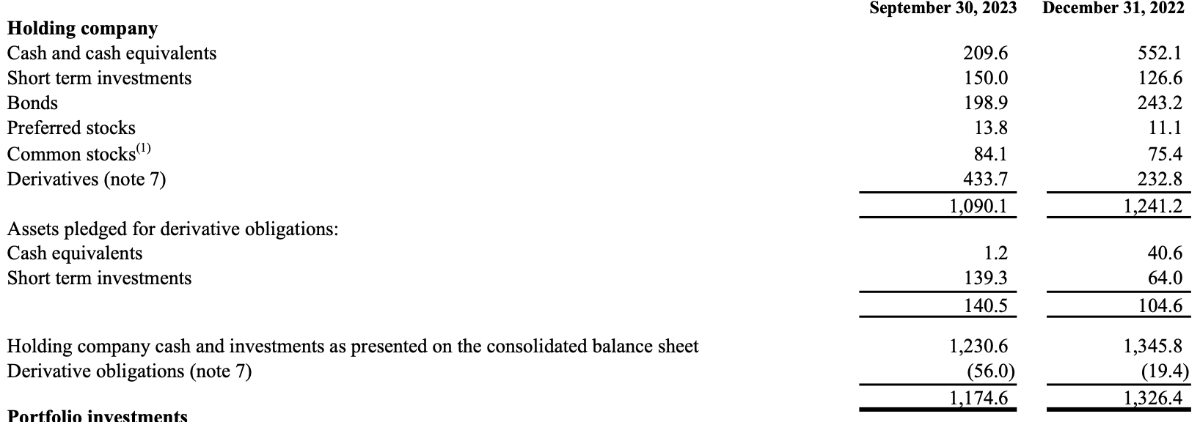

The Berkshire Bond Portfolio! $22.4 Billion on a Trillion dollar asset base, with 78% of the "Bonds" maturing in a year or less

(yes, Berkshire also has a $24 Billion mortgage business but I believe that is largely a spread business funded by BH Finance borrowings)

-

It's Saturday morning nerds!

https://berkshirehathaway.com/news/nov0423.pdf

https://berkshirehathaway.com/qtrly/3rdqtr23.pdf

"

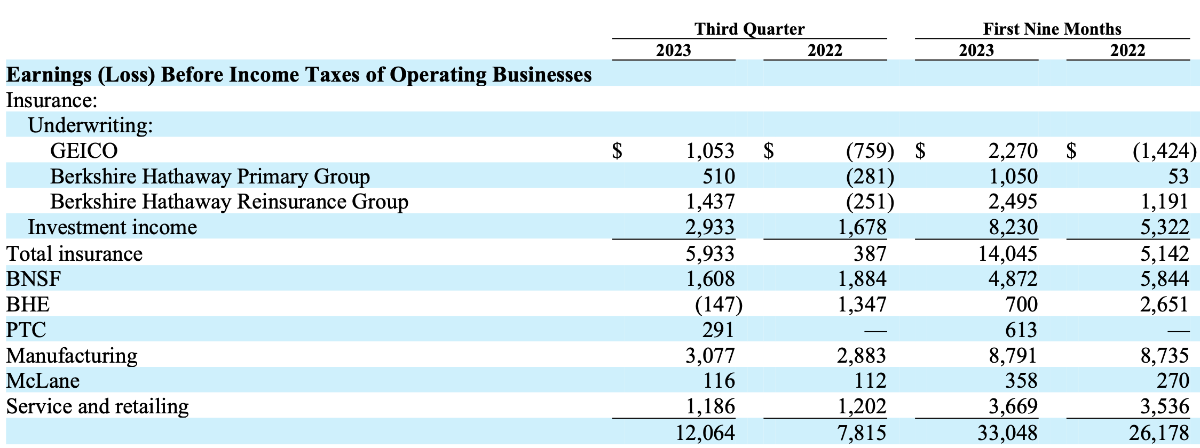

Approximately $1.1 billion was used to repurchase Berkshire shares during the third quarter bringing the nine month total to approximately $7.0 billion. On September 30, 2023 there were 1,445,546 Class A equivalent shares outstanding. At September 30, 2023, insurance float (the net liabilities we assume under insurance contracts) was approximately $167 billion, an increase of $3 billion since yearend 2022."

At 10/24 the share count was 1.444 million A-share equivalents (2.166 Billion B-share eq.)

-

Here is one more soundbite from the WSJ interview with Charlie, Re: Apple

Charlie Munger isn't too worried about Apple's valuation.

During a recent conversation with the Berkshire Hathaway vice chairman, I asked if he thought the tech giant's shares have gotten expensive to continue being a major Berkshire holding.

Apple is trading at about 26.7 times its projected earnings over the next 12 months, compared with a 10-year average of 18.5, according to FactSet.

“I don’t think we’ve got any rules about what we do at Berkshire. If it makes sense at the time in a rough kind of way, we do it. And that’s our system,” Munger responded. “I would argue that Berkshire would have less advantageous future prospects if we didn’t have our Apple.”

-

1

1

-

-

What do they make on the TRS on a day like today? Like $125 million bucks?

-

-

Just now, Crip1 said:

So...this is when they extended durations?

Are you asking what the definition of October is?

-

Cathie! She expects deflation and Bitcoin wins no matter what

"Bitcoin is a hedge against both inflation and deflation because there’s no counterparty risk, and institutions are barely involved.” It’s “digital gold,” she said."

-

You know they aren't a widely followed hot stock when there are barely any questions asked on the call!

-

The seasonal fake-out has concluded! Long live the September effect

-

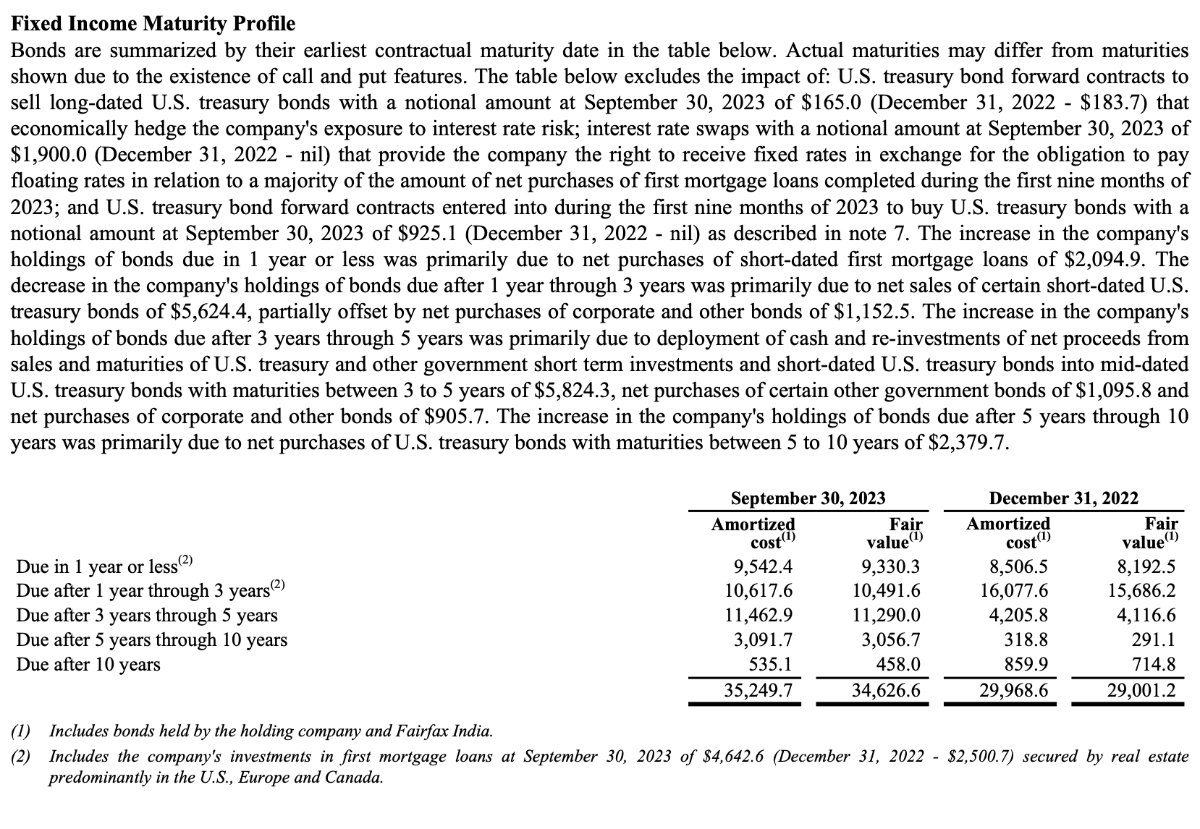

So end of Q3 the duration was still 2.3 years. The best part of the extended duration to 3.1 years (current situation) is that it occurred in October! An excellent time to grab those 3 and 5 year notes.

-

23 minutes ago, ValueArb said:

I thought Porter Stansberry has been long outed as a total fraud? Why would Tilson reference him at all?

The only Porter I trust is Porter Collins.

Tilson works for Porter

-

25 minutes ago, Thrifty3000 said:

Yeah, was surprised to see a pullback on premium growth. Maybe they're just being conservative in the third quarter and waiting to back up the truck on higher volume in Q4 and Jan1.

Did you notice this footnote?

(2) Excluding Ki Insurance, gross premiums written decreased by 4.0% and 4.6% in the third quarter and first nine months of 2023 and net premiums written decreased by 9.5% and 1.2% in the third quarter and first nine months of 2023. Excluding Ki Insurance, the combined ratios were 92.4% and 93.1% in the third quarter and first nine months of 2023 and 114.8% and 101.2% in the third quarter and first nine months of 2022.

To be clear, this footnote only applies to Brit, not Fairfax as a whole

-

2 minutes ago, hasilp89 said:

Maybe covered elsewhere but why aren't they buying back more stock?

Also am i understanding the swap correctly - they basically have the option to purchase 1.9M shares for ~$370/share

Because they are keeping the capital in the insurance subs. There isn't much excess capital at the holding company level

-

-

"At September 30, 2023 common shareholders' equity was $2,833.4 million, or book value per share of $20.89"

"

- The company continued to buy back shares under its normal course issuer bid and during the first nine months of 2023 purchased for cancellation 2,609,481 subordinate voting shares at a net cost of $33.9 million ($12.98 per subordinate voting share)."

-

"Book value per basic share at September 30, 2023 was $876.55"

"We achieved an underwriting profit of $291.6 million on an undiscounted basis and a consolidated combined ratio of 95.0% for the quarter, reflecting significantly lower catastrophe losses and excellent current accident year underwriting margins. Gross premiums written grew by 5.0% and net premiums written grew by 4.8%, primarily reflecting new business and continued incremental rate increases in certain lines of business."

"At September 30, 2023 the company's insurance and reinsurance companies held portfolio investments of $56.8 billion (excluding Fairfax India's portfolio of $2.0 billion), of which $6.4 billion was in cash and short term investments representing 11.2% of those portfolio investments. During the first nine months of 2023 the company used cash and net proceeds from sales and maturities of U.S. treasury and other government short term investments and short-dated U.S. treasuries to purchase $5.8 billion of U.S. treasuries with maturities between 3 to 5 years and $2.4 billion of U.S. treasuries with maturities between 5 to 7 years, and to make net purchases of $2.1 billion of short-dated first mortgage loans and $1.6 billion of corporate and other bonds with maturities primarily between 2 to 5 years. These actions should result in continued higher levels of interest income for approximately the next 4 years."

"At September 30, 2023 there were 23,115,838 common shares effectively outstanding."

FFH_-_2023_Q3_Interim_Report_.pdf FFH_-_2023_Q3_MD&A_section.pdf

-

1

-

-

2 minutes ago, tede02 said:

This seems like semantics. If the Fed is expanding its balance sheet to buy the debt that the treasury is issuing to finance the deficit, is that not money printing?

At the time they were ramping up their balance sheet doing quantitative easing, it was actually functionally the opposite of money printing. The net effect was like a tax - the opposite of stimulus. QE exchanges one form of government liability (which is "money") for another. The Fed buys treasury securities and the seller of treasury securities gets reserves. Both are government liabilities, both are "money," but at the time, the treasury security paid more interest than the reserve account at the Fed. So the Fed removes that interest income from the private sector and replaces it with reserves which at the time earned basically zero. That is why during QE the Fed was reporting large profits on their balance sheet that they would remit to the Treasury (which reduces the deficit like a tax).

Today, however, the long dated treasuries on the Fed's balance sheet earn less than cash and the Fed is running a loss on their balance sheet. This is stimulus - the Fed is paying net interest into the private sector. Much closer to money printing today than when they were building up the balance sheet doing QE.

-

2 minutes ago, Spekulatius said:

We have had this discussion before but QE is not "money printing". It's just an asset exchange of a longer duration treasury for reserves (or essentially a shorter duration asset).

It seems to have accomplished very little other than damage the banking system. Only deficits are money printing and we do plenty of this. Deficits are inflationary. The treasury drives the bus much more so than the Fed.

I agree with all of that except that it IS "money printing" when the Fed runs a loss on their balance sheet like they are currently. Just like it is a form of tax when they were building up their balance sheet with QE and had a positive carry and were remitting the "profits" to the treasury each quarter (lowering the deficit).

So ironically, QE acted as a tax because the Fed took interest income out of the hands of the private sector, made a profit on the carry, and remitted that profit to the treasury.

-

I mean look at this chart of reserves. We barely needed any (relatively speaking) and then this:

-

Aaaannnd the 30 year yield is back in the 4's! Will the 2 year yield also lose the 5-handle? I will say it again: There is a lot of demand for US treasury securities with a 5 handle across the entire yield curve.

-

I don't think QE does much of anything and I think the Fed is starting to realize that themselves. Hopefully they won't bother with it anymore going forward.

"Money Printing" is deficit spending. That is what we are currently doing that people claim is causing the big unsustainable debt problem.

Just remember when you hear folks handwringing over "who is going to buy our debt??!!!" that the government spends the new USD money into the economy first.

edit to add:

What we saw happen with quantitative easing is just the exchange of securities for a shit-ton of excess bank reserves. We operated without all those excess bank reserves just fine for 100 years and lending by large commercial banks is in no way constrained by the level of bank reserves in the system. So all those excess reserves just got parked at the Fed or reverse repo and basically accomplished nothing except the signaling effect of "QE! QE!." (and according to the Fed's own research paper maybe a few basis points of difference in long term yields for a short period of time) And now that the short term reserves are earning over 5% and the long dated paper on the Fed's balance sheet from QE is earning way less, the Fed is running a huge loss, paying net interest into the economy - which is another form of stimulus at the moment. Net interest paid by the Fed on their upside down balance sheet should be added to deficit spending to get the total (highly regressive to rich people) stimulus figures...

Nobody can explain it better than Mosler -

https://www.youtube.com/watch?v=CO6GS13rEuE

Berkshire Q3 2023

in Berkshire Hathaway

Posted

I think you guys have it right on the A-share preference. It is likely a combination of factors -

1. He prefers to have fewer A-shares outstanding after his death

2. The A-shares are so illiquid and hard to buy in size that he is in the market more steadily buying some, instead of turning it on and off

3. The phone number for larger holders to call Mark Millard with blocks of shares to offer probably has some OG families offering A-share blocks.