Crip1

-

Posts

568 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Posts posted by Crip1

-

-

10 hours ago, petec said:

I’ve said this before, so at the risk of sounding like a broken record: why is the cash position a macro bet rather than a risk-reward bet? When curves are as flat as they’ve been, there simply isn’t enough interest rate reward to justify duration risk. The AGM deck is good on this - look how much higher the duration on a 30y treasury is compared to 30 years ago. Bond price risk is real. You guys are all focussed on the absolute level of rates, but how steep the curve is matters just as much. To invert, when the curve is flat, to go long you *must* believe rates are going to *fall*.

*That’s* a macro bet. What Fairfax is currently doing is actually macro agnostic in my view.

I completely agree. I think to an extent the financial press refers to anything and everything as a bet. It's a lot easier to say that than it is to explain the risk-reward analysis.

-Crip

-

1 hour ago, Parsad said:

The week before the AGM, and no one is posting? No Viking spreadsheets? No Daphne asking about estimates? No insights by Stubble?

Or are you guys all on the way to Toronto or something? Cheers!

Honestly, I am not sure there’s too much more to be said until the results come in. It will be interesting to see:

• The level with which the hard market is still in force (CR and Premium growth)

• Whether or not they’ve moved ST money into longer term instruments (I am guessing the answer is “no”)

• What changes have taken place on marketable securities

Chatter should pick up on these and other matters.-Crip

-

42 minutes ago, KFS said:

Fair point. I guess I tend to assume Bradstreet & gang would be able to make some intelligent decisions if/when the opportunities arise, but of course you may be right.

It would also be interesting to see whether the correlation and subsequent disconnect impacted other "peer" companies such as Markel. Cinc Financial, etc to determine whether this was a macro thing or specific to FFH.

-Crip

-

10 minutes ago, StubbleJumper said:

I hope that FFH is making use of its NCIB these days. The price is currently US$461, which is a considerable improvement over what they paid for the SIB. You don't get much volume from the NCIB, but it would be nice if they could even get 100k discounted shares during March.

SJ

You beat me to it.

-

Did anyone else have the conviction, and the dry powder, to add sub US$12 yesterday? I added 25% to my position.

-Crip

-

On 2/19/2022 at 7:40 AM, cwericb said:

Sometimes it is interesting to see how others (non COBF members) see Fairfax. Here is an article from Seeking Alpha.

“Fairfax Financial Holdings: Further Growth Possible, But Catastrophe Losses Pose A Challenge”

While it seems that the writer doesn’t quite grasp how a P&C insurance company operates, but I thought some might find it interesting. Certainly Cat losses and inflation are a concern but one would assume that Fairfax is well aware of that and accounts for it in its premiums.

Glad to see a number of CBOF members responded to the article.

Before I say anything it's gotten to epidemic proportions the level with which people hide behind a computer keyboard and harshly criticize just about anyone. I refrain from doing that just because I find it so distasteful. That said, I saw this on Seeking Alpha and was pretty surprised somebody took the time to write about a subject on which they have extraordinarily limited insight. Beyond that, the author could have I really did make his point about a third of the way through article. The rest of it was simply rehashing what he'd already said.

It's not right to impune this individual's character or mock their intelligence or knowledge. But this person ventured a little too far outside their circle of confidence.

- Crip

-

45 minutes ago, Sullivcd said:

The release says they bought 5% of the shares outstanding at $12 a share from two individuals. Maybe a divorce or something? I don't get it.

We can only speculate and, honestly, I am not as concerned about that as I am about the fact that the investor who knows FFI inside and out, arguably better than anyone, determined that $12/share was an attractive price. It could be argued that the same investor felt that FFI was more undervalued than FFH.

-Crip

-

While bemusedly shaking my head, I bumped up my position by 50% just now. I simply can't believe that the market price will stay this disconnected from the BV forever. Furthermore, BIAL really has to be a tailwind here...the combination is too good to pass up such that I am considering adding more.

-Crip

-

Seeking Alpha may not have proofread the headline terribly well:

FRFHF: Fairfax Financial GAAP EPS of $122.25 beats by $1.78, revenue of $26.47M misses by $25.22B

I mean, nice earnings number but it's kind of a miss to fall $25.22B short on revenue.

-Crip

-

7 hours ago, Viking said:

With Fairfax earnings being released after markets close Thursday what are the things people are watching most closely? Here are a couple of things for me:

1.) does net written premiums growth stay close to 20%?

- hard market: still alive and well as we enter 2022?

2.) CR: are we able to get below 96?

- Northbridge: impact of BC flooding?- Brit: and more covid charges? Ki? New CEO…

- reserving? I think Q4 is when annual reserve review is done.

3.) interest and dividend income: do we see bottoming?

- how does total compare to Q3?

4.) realized gains? Stock holdings were up nicely in Q4.

- do we see impairment charge for Farmers Edge? Altas Mara? Others?

- any change to FFH TRS position size?

- Digit update? Did Indian government give approval? Or is this still pending?

- were any equity positions sold?

5.) runoff: do we see another big asbestos related addition to reserves?

- this business is now included with Eurolife…

6.) sale of 10% of Odyssey: how does this flow through financial statements?

- does transaction impact value Odyssey is carried at in BV?

7.) YE BV/share: how much over US$600? This is the big one

Inverting the question. The items above represent mainly good news but I think the market is focused more on bad news for Fairfax (Additional reserving, impairment charges, unexpected insurance losses, etc). To the extent bad news can be eliminated or minimized the closer to intrinsic value the market will value Fairfax without the current discount.

-Crip

-

2 hours ago, petec said:

I'm not entirely sure this is true.

I think it's about assessing whether you are being paid to take duration risk.

In other words it is about analysing the spread between short term and long term debt, and deciding whether that spread adequately compensates you for the risk of capital loss if rates rise.

You can forecast interest rates to do this, but you don't have to, because you can just do it by looking at how much you'd lose if the bet went wrong vs. how much you'd make if it went right, and deciding whether you like the payoff.

Not sure I am making sense here but to put it another way: if 2y rates = 30y rates it might be very stupid of Markel to duration-match a 30-year liability. They'd be taking a totally un-necessary risk.

I was thinking along similar lines that there is a risk-reward analysis at play. Is it worth some additional yield in the short term with to open one’s self up to capital loss in the intermediate-long term? If the difference is 300 basis points per year, maybe. But if the difference is 50 bps per year the reward is substantively less attractive.

-Crip

-

9 hours ago, Viking said:

I am a big believer in Druckenmiller’s strategy of sizing positions based on how asymmetrical the bet is. What are the chances Fairfax’s stock price drops 6-8% after earnings come out? What are the chances Fairfax’s stock price rises 6-8% after earnings come out? (Let’s say in the 30 days after earnings are released.)

Today i think the chance of a positive reaction in the stock price from a positive earnings surprise is much higher (70%?) than an negative reaction in the stock price from a negative earnings surprise (30%?). Why?

1.) 7% reduction in share count. Will this not materially impact year end reported book value? In a very good way?

- now i really do not understand how the sale of 10% of Odyssey will impact the financial statements (exactly where the ‘cost’ will show up). Or is the cost largely to be borne in the future via payments to lenders of $900 million?

2.) based on reporting from other P&C insurers my guess is Fairfax should report solid top line growth (+15-20%) and a decent CR (96?)

3.) solid investment gains in equity holdings - based on market moves in Q4

My guess is the benefit of the final mark up of the Digit revaluation will now come in Q1 given there have been no press releases on this topic (a +$35/share benefit).

With shares trading at US$495 (near historic lows… looking back 5 or 6 years) my guess is there is a higher probability that Fairfax shares trade higher after earnings given all the current tailwinds.

—————What are the key risks?

1.) big increase in reserves for runoff2.) big increase in reserves for Brit

3.) large losses at Kai - as it continues to scale (or busts)

4.) large write downs on one or more equity holdings - Farmers Edge?

5.) large loss on short position in Tesla… just kidding… couldn’t help myself

Personally, I’ve given up trying to predict how the market will look at the earnings. Markel had a great quarter, beating all estimates handily yet is down 2-3% from where it ended pre-earnings-announcement. I really don’t disagree with anything you said about Fairfax as it is still my largest holding despite my tendering some of my shares to the Dutch Auction, but it’s hard to handicap the level with which this is asymmetrical when the market is so irrational.

-Crip

-

10 hours ago, glider3834 said:

great summary Viking - not much to add

Just on those equity swaps - their avg cost I believe is US$373 - so likely sitting on a US$215 mil gain

Looking forward, I am curious if they made any additions with the recent market sell off.

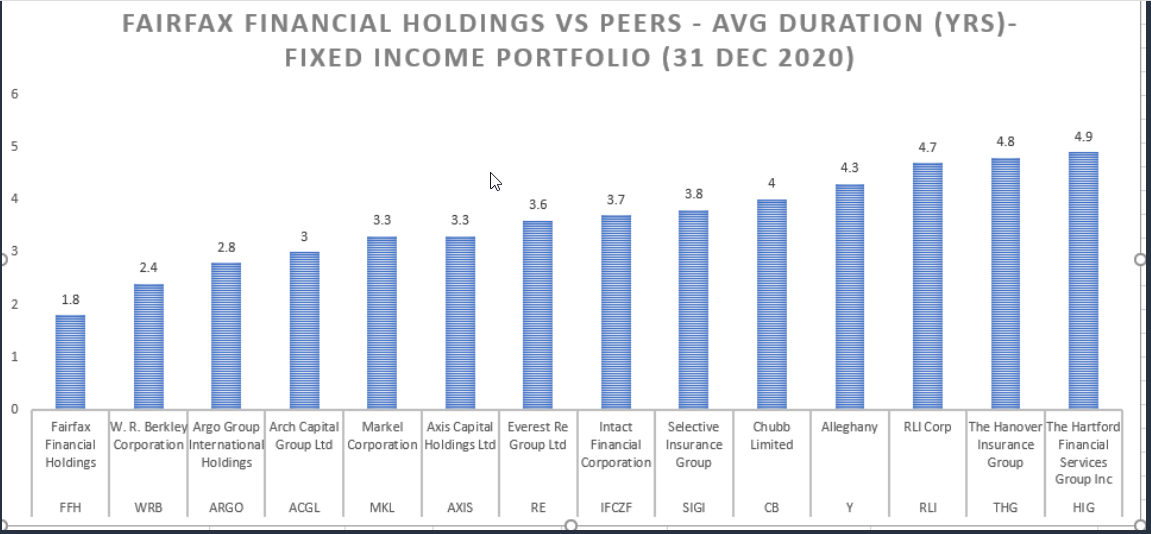

Fairfax is certainly better positioned than most of their peers to take advantage of higher interest rates, with shorter duration on their fixed income portfolio - I actually did a chart & posted on twitter but re-posting it below ( source Company Annual Reports 2020)

The advantage of FFH's low duration is not going to show much in this earnings cycle. The 10-year treasury, for example, did not move terribly much in Q4 of 2021 compared to 2022 YTD. There will be an element of “Only when the tide goes out do you discover who's been swimming naked" when the Q1 2022 earnings are released. My curiosity with the Q4 2021 earnings release will be to see to what level, if any, FFH moved into longer duration bonds.

-Crip

-

Guessing that part of the decline today is due to Wednesday being the ex-Divvy date. So far the strategy of tendering shares hoping to buy back 10-20% lower like folks did with FFI was not looking too good, but a few more days like to day and that's going to start looking better.

-Crip

-

3 hours ago, Xerxes said:

between the x-dividend date late next week and the Q4 results in mid-Feb, some steam should come off, as flippers move on greener pastures

No opinion on what’s driving the recent runup, and I honestly don’t care. The factors of short term movements are more a matter of speculation and/or Mr. Market’s mood swings. Longer term, market price and book value are converging (though not in a straight line) such that, eventually, the price is going to get to or beyond BV. The questions are…what will BV be when this happens and when will it happen? It may be six months down the road and US$645, or three years down the road at $825. The fewer errors that are made (ill-advised company purchase, big investment decision gone bad, etc.) the sooner it will happen and the higher the BV once it gets there.

So, the past month or so have been nice, but it’s noise. Just want to see FFH keep executing and avoid unforced errors.

-Crip

-

On 12/26/2021 at 12:39 PM, Viking said:

@Xerxes i am not convinced the crazy discount we see with Fairfax India shares today is permanent. Now I have no idea what the catalyst will be to close the discount. Or timing. I do expect Fairfax India to be very aggressive with share buybacks. Regardless, buyers of Fairfax India at under US$12 should be able to earn an acceptable return (10-15% per year moving forward). And if it closes the valuation gap then returns would likely be exceptional (+25%). So i will be happy to re-establish a position in Fairfax India with some of the proceeds from Fairfax from the dutch auction.I think the catalyst would be performance. If FIH can return 10% on the $20 Book Value, that would be in excess of $4 over two years. $4 on the $12 current price is roughly a 15% annualized return on purchase price. Returning anything more than 10% would amplify the 15%. That’s gonna get the attention of the market.

-Crip

-

Well, the $64,000 question is whether or not any folks who tendered, and I tendered roughly 25% of my position, are going to be able to buy back in the US$450 range.

The other question for those who tendered and will have more cash available is whether it be better to plow that cash into Fairfax India?

-Crip

-

8 hours ago, mjm said:

anyone receive an offer from their brokerage for the FFH dutch auction? nothing from Fidelity.

Yes, from Schwab.

-Crip

-

11 hours ago, Viking said:

@StubbleJumper i really do not understand why so many are in such a panic forFairfax to unload Resolute. Yes, it was a dog for Fairfax for many, many years. However, the company the past 3 or so years has made lots of money; and made lots of very good decisions with that money. The company has successfully pivoted to lumber and more:

- it bought 3 lumber mills in the US South at the bottom of the cycle in 2020

- bought back a bunch of stock at crazy cheap prices

- paid 2 large special dividends

- paid back most of its debt; refinanced whats left at low rates

The shares hardly look expensive. Especially if average lumber prices stay elevated (compared to historical norms) the next few years. Now i am not saying Resolute is some wonderful company. But i also do not think it is the terrible company it was 10 years ago.

Yes, Resolute has been hit much harder with duties than most other Canadian lumber producers. Not sure why. They will shift and focus on selling their Canadian production in Canada. Other Canadian producers (with lower duties) will shift to selling more Canadian production into the US. Resolute does have three lumber mills producing in the US south. Bottom line, if lumber prices stay elevated Resolute will continue to earn very good money for shareholders. I think there is a good chance US housing starts will remain elevated for the next 5-10 years. If so, lumber prices will average much higher prices than in the past. I understand if Fairfax is patient with Resolute.

Resolute is also sitting on more than $300 million in lumber duties (on deposit). I think the last time this happened (softwood lumber dispute) when it was finally resolved a big chunk of the duties actually went back to the lumber companies. Something to keep in mind.

I can't speak for everyone, but from my perspective the desire to not own RFP is summarized by the Buffett quote of "It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price". The info you shared suggests that management is doing an admirable job with the company, but the fact that it's a commodity business is the reason why I would love to see FFH reduce/eliminate their stake.

-Crip

-

41 minutes ago, ERICOPOLY said:

Cardboard was pissed.

I seem to remember that.

-Crip

-

9 minutes ago, maxthetrade said:

I had expected bad results from Brit but I'm kinda dissapointed by Odyssey Re. On the other hand Allied results looks pretty good and better than I expected. FFh still looks too cheap.

This may be reinsurance-specific as Markel's Reinsurance combined in Q3 was 112% and is 108% for the 9 months. Fairfax' results compare favorably at 109.5% and 101.3% respectively. Though certainly possible, I am disinclined to think Odyssey Re has lost their expertice.

-Crip

-

On 11/1/2021 at 8:25 AM, StubbleJumper said:

Once again, can we please stop using the terms equity "hedges" and inflation "hedges?" Those terms imply that FFH was engaging in responsible risk management practices. What FFH actually did was "hedge" more than 100% of its equity portfolio and it had deflation "hedges" with a notional value of more than $100B for a company that had annual revenues that were less than one-third that high. When you "hedge" more than 100% of your exposure to the underlying, you are no longer managing risk, but rather speculating.

So, let's instead tell the brutal truth. What FFH actually did was use derivatives for the purpose of market speculation. Management did this, it didn't work, and it cost shareholders dearly. We should not use the word "hedge" as an euphemism to somehow suggest that management made responsible choices with respect to position sizing.

SJ

This is coming from someone who "Drank the hedging Kool-Aid" several years ago. You are 100% right, SJ. Even if the market moved sideways it was a flawed idea. My bad for not seeing it at the time and you are right, it was pure speculation.

-Crip

-

On 10/27/2021 at 6:52 PM, Parsad said:

I spoke to Francis today, and he said the specialty lines aren't increasing much, but reinsurance is very strong. So I would imagine that Fairfax's reinsurance businesses are going to continue to do well into 2023, but their more generalized specialty lines will not benefit nearly as much. Fortunately, they do a ton of reinsurance! Cheers!

I just finished looking at Markel's earnings which were released today. Their insurance including specialty showed underwriting profitability and roughly 20% growth year over year compared to their reinsurance which showed a 112% combined ratio for Q3 2021.

Seems like a lesson in "stick to your knitting"

-Crip

-

1 hour ago, maplevalue said:

Much

Ado

About

Nothing (IMHO)

But considering that FFH is up about 2.5% today where the market averages are up roughly half that much compels me to think that the market looks at any distancing from BBY is a positive for Fairfax.

-Crip

Fairfax 2022

in Fairfax Financial

Posted

I respectfully disagree. This looks/feels to me like risk-reward analysis. The yield spread between the 2 and 10 year treasuries is 27 bps. The spread between 2 and 30 year is 35 bps. The question is whether or not it is worth the risk of capital loss to extend past 2 years in bond duration. Looking through the prism of 2010 through 2021, the answer is "maybe". Looking at it through the prism of 1960 through 2022, IMHO the answer is a resounding "no". It's less of a "bet" that rates are going to rise and more of "it's quite possible, and I don't want to lose my a** if it happens".

-Crip