Spooky

-

Posts

533 -

Joined

-

Last visited

-

Days Won

1

Content Type

Profiles

Forums

Events

Posts posted by Spooky

-

-

Interesting topic, something I often think about a lot is what is "value" and if GDP is the right metric / north star to continuously focus on. My view is the correct answer to this question is both yes and no. Clearly, some of the billionaires in the world (past and present) have created tremendous value for society and this is easily measured by dollars in the bank. Think of Henry Ford, the invention of the modern assembly line, Model T, etc... revolutionary. In the mid-1920s, his net worth was estimated around $1.2 billion.

On the other hand I think a lot of value created in the world is not measurable in dollars or the creator of that value does not necessarily reap the financial rewards. For instance, look at Adam Smith and some of the other Scottish academics that created the intellectual framework underpinning the modern world. Did Adam Smith's wealth equal his contribution / value to the world? Definitely not, even though his ideas help create trillions in value that we see today.

Lastly, there are so many "intangibles" in society that have value but are not measurable - like art. Look at Leonardo Da Vinci and the works of genius he bestowed on mankind. As far as I understand Da Vinci was not personally wealthy and was actually quite poor. Same with Van Gogh - he was basically destitute his whole life. Or look to philosophy - many of the great thinkers of the past were not wealthy. Socrates was a stone-cutter / mason. And what about civil service? Surely that has value but civil servants don't (usually) acquire much material wealth. Finally, works of charity - Ian Flemming is revered not just because of his discovery of penicillin – which has saved millions of lives – but also due to his efforts to ensure that it was freely available to as much of the world's population as possible. The full financial benefit of his contribution to society did not accrue to himself personally.

-

Just saw an insider filing that John Malone bought roughly $4.6M of Liberty Latin America Ltd. (LILA).

-

Please no

-

Constellation Software

Google

Berkshire

BAM

Verizon

BABA

-

Opened a position in BABA.

-

Any clues on what the mystery Chinese company Munger / DJCO are buying in addition to BABA?

-

A lot of controversial takes from Charlie at the DJCO annual meeting but they sure are original. His depth of knowledge is staggering.

-

2 hours ago, Gregmal said:

Waiting for a 90 year old dude to die is like waiting for the market to crash, the illusion of it happening tomorrow is real, and then however many years later you realize you wasted your time. Or then it does happen and you’re still paying more than if you had just bought on day one.

When Jobs died Apple was down 4-5%. So not much. And at this stage of the game I’d argue Jobs was way more important to Apple than Buffett is to Berkshire in todays form.

Agree. BRK is already my second biggest position so I have been buying when the price looks attractive. A 5% drop in the share price would still present a nice buying opportunity to add more although given BRK's focus on succession planning and long term oriented shareholder base I doubt the decrease in price will be very significant.

Hey this thread is about what we're salivating to buy at the bottom so I'm allowed to dream!

-

11 hours ago, james22 said:

I like to think it might dip significantly for a minute when Buffett passes?

Hope I can take advantage of it.

I'm want to be ready for this day too. I have faith in the Berkshire model for the long run and they are so well positioned for the future.

-

Spring of 2020 I bought GOOG for an easy double. BRK would be my ideal stock if it was ever having a fire sale (not super likely). In that environment you know that papa B is also going to put his cash pile to work on some wonderful companies. Problem is having enough dry powder to swing hard.

-

Started a position in SHOP and NFLX.

-

4 hours ago, Spekulatius said:

For Canadians, I would stick with stocks or buy real estate in the US. Canada residential real estate is clearly a bubble and sooner or later, there going to be a price to pay. Compared to Canadian RE, the US is downright cheap.

Agree with Spek 100%. I'm in Toronto and have been looking at buying a house and the value proposition just isn't there compared to the US. The dynamics here are that people are just borrowing larger and larger sums to buy houses since there is an attitude that you need to own a house no matter what. It seems like a mania to me. We looked at one semi-detached house that was West of High Park and it had 15 offers and went for nearly $500k over asking. People are just valuing houses based on comparables so if someone overpays that becomes the new comparable. If you buy a house here you are also taking on the interest rate risk because you can only lock in a fixed rate for 5 years. 30 year fixed rate mortgages are not available like they are in the US.

Personally, I think stocks are the way to go if you are looking to compound your wealth over a 30 year period. If you look at the historical performance of the TSX with dividends reinvested over the prior 30 year period it has crushed the Toronto housing market by like 4x (it's been a while since I ran this analysis so it might be somewhat different now). If you buy a house you are buying a depreciating asset (other than the slice attributable to land) whose top line revenue (rent) should logically only grow at the rate of inflation. If you buy a good stock, it will reinvest retained earnings into the business and increase its earning power over time at a higher rate than inflation. As others have pointed out the benefit of buying a house is the easy access to leverage but you could always replicate this in a stock portfolio through margin or options.

I think the picture changes if you are looking at US real estate since it is actually still pretty cheap compared to Canada / Western Europe and you can lock in the 30 year fixed rate mortgage. This McKinsey study was pretty interesting:

Particularly this chart which has the US at the bottom (they are saying real estate is 2/3rds of net worth):

-

3 hours ago, Thrifty3000 said:

Here’s a famous 1999 article in Fortune where Warren Buffett predicted returns for the next 17 years. (Spoiler alert, he nailed the prediction.)

And, more importantly, he lays out all the key factors you need to consider to make the prediction.

In short, don’t expect the next 20 years to look like the last 20.

https://archive.fortune.com/magazines/fortune/fortune_archive/1999/11/22/269071/index.htm

Interesting, thanks for sharing. Reading the article reminded me of a piece in the WSJ discussing investor's expectations for the future: https://www.wsj.com/articles/when-a-59-annual-return-just-isnt-enough-11625238010

Feel like a lot of people will be disappointed going forward. Assuming that US stock market returns follow a similar pattern over the next 17 years as outlined in Buffett's 1999 article (i.e. 4% real annual returns), what strategies can we use to get better results?

-

Is there a class of stock / security to own an interest in the mother ship similar to BAM? If I wanted to get exposure to everything under Liberty Media Corporation would I need to own positions in each of FWONA, LXSMA and BATRA?

-

16 hours ago, wabuffo said:

Can you elaborate? Because we just had 10+ years of massive and unprecedented deficits...and still didn't get massive inflation outside of asset markets.

We did not. We had a big deficit splurge in 2008-2009 and then quickly got back to deficits that were 3-4% of GDP. The numbers are large but as a % of GDP they aren't big. Now 2020-2021 was much larger and it was more in the form of direct payments to individuals (stimmie round 1, 2 & 3) and businesses (PPP forgiveable loans).

I think the key question is: Are these big deficits behind us and one-time in nature or is this the beginning of more deficit spending under this administration that will average much larger percentages of GDP?

I don't know.

But what I do know is that the Fed is a minor player in all of this action. The big gorilla is the US Treasury.

Bill

So I'm trying to think through the implications now of the Fed raising interest rates in this environment - based on your position it won't stop the inflation experienced due to the expansion of the money supply but will lower asset prices, increase interest expense for government / firms, potentially reduce demand for goods / growth. So it seems like we are possibly headed for stagflation (assuming the government continues to run large deficits going forward).

Also, can you contrast the environment now with the environment where Volcker broke inflation with significant rate increases? What is similar today and what is different? Trying to figure out why that worked then and why.

-

17 hours ago, wabuffo said:

Can you elaborate on this please?

Its simple - the Federal government offers to us (the private sector) three types of liabilities that exhibit "moneyness":

a) currency in circulation

b) bank reserves

c) treasury securities

(I compare this to a bank offering you: a) cash b) demand deposit or c) time deposit.)

There are three types of transactions that the consolidated Federal govt (US Treasury + Fed) does with the private sector that affects these three types of Federal government "moneyness" liabilities:

1) US Treasury deficit spending (net of taxes and fees received)

2) Federal Reserve buying/selling US Treasuries.

3) US Treasury issuing new treasury securities.

Of these three, the only transaction that increases money supply for the private sector is deficit spending.

The other two types of transactions with the private sector are asset swaps and change one form of Federal government liability for another and thus do not added to the total amount of Fed govt liability to the private sector.

Some say bank lending also increases the amount of money supply - but I say that this is a private sector transaction that adds an asset but also a liability - and thus does not increase total private sector net assets.

So the headline is - watch US Treasury deficit spending. Its the only thing that matters when it comes to money supply increases.

Bill

Thanks for the explanation, appreciate it!

-

3 hours ago, wabuffo said:

The Fed can't stop monetary inflation (i.e., currency debasement) with interest rate hikes - let alone tapering.

Bill

Can you elaborate on this please?

-

Been slowly trying to learn more about Malone and his different companies and investments. Does anyone know if there is a tracker to show what his key / major positions are?

-

Added a little bit of Agnico Eagle (AEM.TO) this morning.

-

Half baked thought here but it seems like the dividing line in the data is 1975 which is the last year before the US left the gold standard in 1976. One thing I have been thinking about is how much of the run up in the prices of homes is related to the incineration of the value of fiat currencies.

-

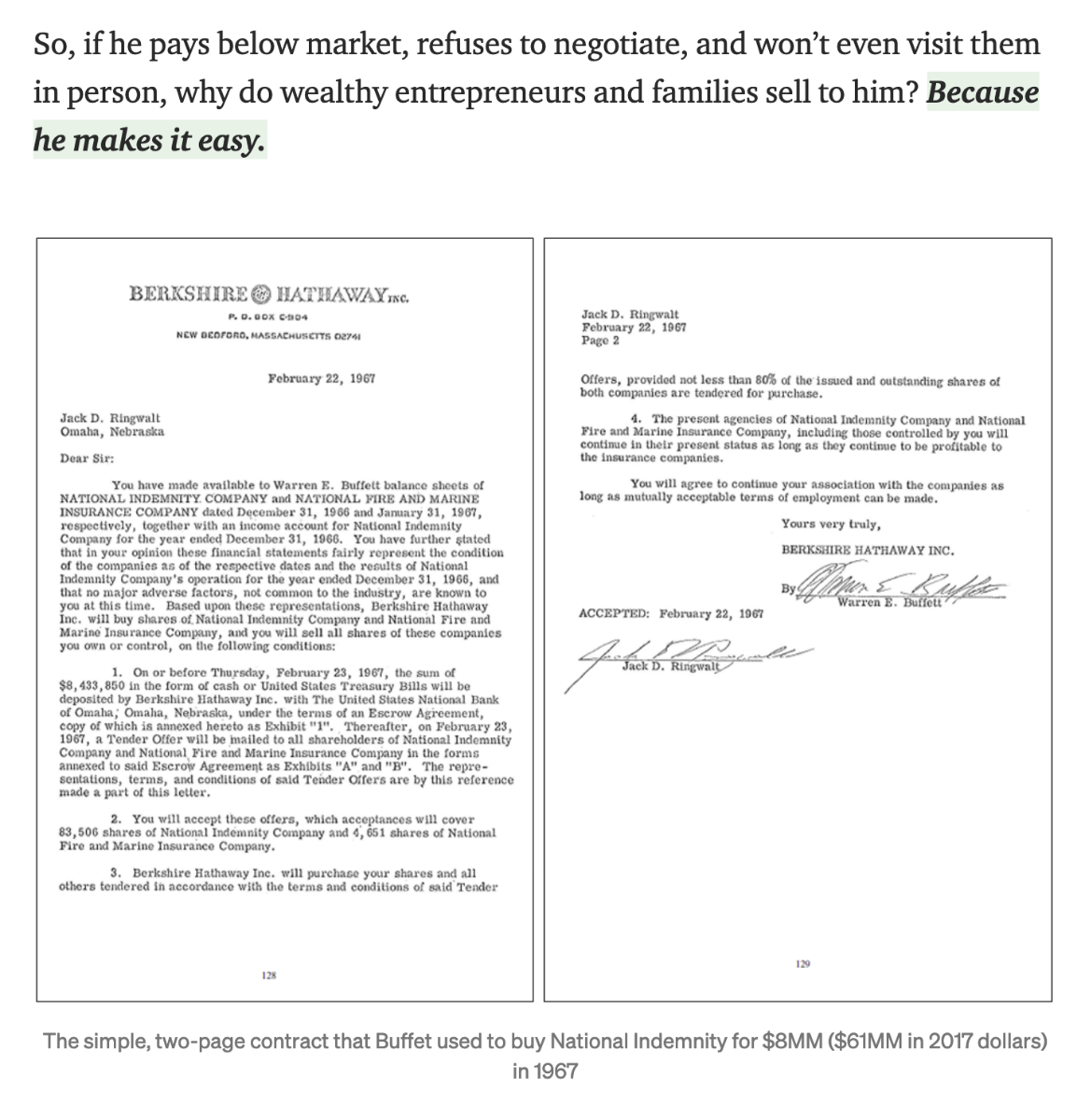

5 hours ago, formthirteen said:

This was a pretty interesting read:

https://awilkinson.medium.com/the-berkshire-hathaway-of-the-internet-391a8ee83db

I'm sure he has "better" lawyers now than in 1967:

This letter is interesting because it also incorporates all the representations / terms of the tender offer into the letter. Can't really say he does an acquisition just using a two page letter based on this.

-

10 hours ago, UK said:

Or you invest in smaller companies (or even large) and are being screwed by a management (or majority owners) instead of CCP?

You still have this risk with investing in China. It is an extra layer of risk on top of what I mentioned.

10 hours ago, UK said:Also I would like to ask: If Apple is good enough and safe then? Let say only 1/5 of their sales is China related, so no existential threat, but if you take that out while a company trades at like 40x earnings, I think you can go for a permanent loss of capital situation there also. And in a more nuclear scenarios, Apple is dependable on China for like 4/5 or 2/3 of its manufacturing. So is it investable or not?

This is definitely a big risk factor to consider when investing in Apple and a serious concern. However, if you are an apple shareholder and for some reason China causes difficulties in manufacturing, you still have an ownership right / legal claim on all of Apple's assets which are not located in China - their giant cash pile, their IP, etc. Apple also has the ability to move / diversify it's supply chain in a worst case scenario.

-

No doubt that China's growth and trajectory are extremely impressive. However, as others have point out above, how can you buy stock which is essentially a bundle of legal rights in a country that does not have rule of law or respect individual property rights? Any investment you make in the country is subject to the whims of the CCP. What are the odds that the CCP comes along and nationalizes a company or rewrites the rules resulting in a permanent loss of capital? Not zero. What are the percentage of returns captured by shareholders of Chinese companies resulting from China's economic growth? Lower than US stocks. Personally, I have no ability to estimate these percentages with more certainty than others in the market and am unwilling to take an unknown risk of a permanent loss of capital. Especially when I can invest in other jurisdictions with robust legal systems and shareholder rights where this risk is virtually non-existent. Maybe Li Lu and other investors can properly evaluate and navigate these risks but I can't. Also, to me it seems like China is actively taking steps to prevent US citizens and Westerners generally from benefiting from China's growth by limiting overseas listings and IPOs. Only favoured institutions like Blackrock / Bridgewater that toe the party line get access to Chinese markets.

To capitalize on the China growth opportunity I landed somewhere similar to SD - look for investment opportunities / companies in safer jurisdictions that have things China can't acquire or build at home that will benefit greatly from China's growth thus avoiding any CCP risk.

-

On 8/30/2021 at 6:06 PM, longterminvestor said:

Why buy bonds? Berkshire does not buy bonds for cash flow, they buy for store of value. and interest rates can only go up which means the price of the bond goes down. Agree, doesnt make any sense.

Two points here:

A) Bonds and cash would do well in a deflationary environment. I wonder what probability weighting Buffet attributes to this outcome in his scenario analysis / mental models. Listening to Powell's speech at Jackson Hole he highlighted a lot of dis-inflationary forces out there and it seems like the Fed's continued dovishness is geared to minimize the probability of this outcome (rather than the inflation scenario).

B) Bonds and cash also have an option value tied to them - if there is another large crash then perhaps some elephants become available at attractive prices.

Will Inflation Pressure Ease in the 3rd Q & 4th Q of 2022?

in General Discussion

Posted

I find it hard to buy the savers got screwed narrative - they are generally older and have assets which were all significantly inflated due to the fed action (including bonds). Boomers made out like bandits. It's really the young people / poor people with no financial assets that got screwed.

Also, we need to look at the alternative - if the Fed had let the financial system collapse and didn't recapitalize the banks we would probably have been looking at a second depression.

Was just watching this interview with Munger and he talks about the Fed's actions since the GFC and he thinks the Fed's actions worked and they didn't have much else that would work: