Value_Added

-

Posts

238 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by Value_Added

-

Fast Growers - What Are Your Top 5 Picks Today?

Value_Added replied to Viking's topic in General Discussion

Japan Material 6055 looks interesting. Been looking into a few Japanese companies since I’m stuck in yen due it’s drop versus the USD since selling my Shinoken position. They are reliant on the memory business of Toshiba (Kioxia) which is a risk as it’s pretty much their main customer (although a very large player in the memory business), but their growth has been steady and they provide a high return on capital. Quick summary is they have their hands in a few random businesses but their core business is providing high purity gas, water, and equipment to Kioxia. They also began providing clean room management services within the Kioxia’s plants. I’m not very familiar with the inner workings of a semi conductor plant or how common it is to contract these services out, but it seems they may have found a niche will help them rise with the tide of the industry. -

Wrote a few $7.50 puts with Dec. 16 expiration on PCYO to push myself to finish my deep dive before making it a full position. Will very likely turn this into a full position but I’m still working through everything to ensure I feel comfortable with it.

-

A lot of the conversation here is about dealing with the macro such as inflation, jobs, QE, QT, etc… and how that will affect the market. Then theres statements like this from @changegonnacome which hit exactly my investment style and completely bypasses all macro outlook and forecasting. From my perspective, that’s exactly how it should be if one believes the market is a weighing machine over the long term…it should boil down to understanding a business well enough to know what the normalized FCF or earnings are, placing a value on it, and buying it up when it reaches an appropriate margin of safety. 15% FCF yield is insanely cheap for a good business! I firmly believe you can’t time the market but there are some pretty good indicators that exist which we can at the very least use as a rough guide to help us gauge the market and classify it as cheap or expensive. To name a few, some of which have been discussed already, are the Shiller PE, Buffet Indiciator, Buffett himself, and the individual valuations based on normalized earnings or FCF (see below). Going back to the comment from @changegonnacome, have you found opportunities that have these numbers (7x FCF multiple and growing 10% next year)? If so, are they a covid beneficiary in any way whatsoever? Also, what’s your best reasonable estimation of their FCF in 3 or 5 years? Not to be long winded but, I ask because those numbers (without having any further context) represent a 6” bar and while the market is down substantially from its highs, I don't see a lot of 6” bars. I see a whole lot of optically cheap companies that were a covid beneficiary to some degree (value traps), I see some really good companies that are trading at a reasonable price to justify at least a starter position, I see a few asset plays that make some sense right now, and I see some merger arbs which you could view as a cash equivalent. But as a whole and based on my intermediate level of investing knowledge, this market hasn’t thrown up any 6” bars based on the measures mentioned. There seems to be several folks with a-lot of experience here who have found ample opportunities in this market and I think that’s great but I also think it’s very important for people like myself with less experience in markets like this (and others who fall into this category) to realize what you don’t know and are likely incapable of learning to the extent of getting comfortable enough to make them 10% plus positions. It’s easy as a human-being to get antsy in a market like this, especially reading post after post about this opportunity and that opportunity. This is when mistakes happen if you truly don’t understand the business you’re buying. You force yourself into having a false understanding of a business just because its down and you feel like you need to be doing something because others are, so you buy. This could easily lead to buying a value trap and it really feels like that’s what the market is mostly offering up unless you have the skill and experience to find hidden or undervalued assets (but these aren’t 6” bars in most cases) with some certainty behind your findings. What you absolutely don’t want to do is leave yourself zero opportunity when these 6” bars are offered by the market. I have a goal to make 15% CAGR over my investing life and I understand it is no easy task but if you buy right and have some patience, it is possible. Discipline is key and while I’ve never invested in an environment like we have now, it really feels like danger is everywhere and the utmost care should be take to ensure you buy right. I don’t believe in using indicators as decision makers, but used collectively I think they can serve as a useful gauge when buying. Shiller PE - Maybe its coincidence - maybe its not, but when the Shiller PE is high, it’s shown time and time again market underperformance in the years ahead. This is a reflection of the entire market and its obvious that many great opportunities still exist with a high Shiller PE (especially asset plays and merger arb) but generally the opportunities need to be created by some sort of company or industry specific turmoil that you are able to look past with a long term mindset, understand it effects on the business, and know it will pass with the company still intact. It could also be some sort of catalyst that is assumed to be mostly unknown by the market as a whole but care should be taken assuming the catalyst isn’t priced in. Again, maybe theres underlying factors at play each time the market mean reverts with a high Shiller PE but i think it is wise to assume when its elevated, more care should be taken to ensure you understand what you are buying, especially with the amount of optimism built into the market. Buffett Indicator - Again, just an indicator and a seemingly flawed one at that. I mean c’mon, it doesn’t even factor in private companies not trading in the Wilshire. But like the CAPE, it mean reverts from high levels and paired with the CAPE, can act as a tool to make you aware of when more care should be used because again, at elevated levels, optimism exists. Following Buffett - I know Buffett is in a different league and has very limited opportunities due to Berkshire’s size, but history shows that when Buffett is building cash, the market isn’t throwing out many 6” bars. I know he has been spending heavily recently on oil, and for those who understand oil to a level to make it a position like Buffett has, more power to you. Even while spending billions of his cash pile, it still has a significant amount remaining and as a whole, he isn’t buying the market as he has in previous periods. Blood doesn’t seem to be in the streets yet from an overall market perspective and again, while deals can be found - they generally aren’t 6” bars right now. Break it down to individual business valuation without regard to anything else - This is what should be happening anyways, but if you want to know generally if the market is cheap, you’ll find it with 6” bars everywhere based on sound valuation. Sound valuation meaning the earnings and FCF used for the valuation are normalized. Even in a bad market environment, the business and FCF will continue to grow and create shareholder value because the business is good and their capital allocation toolkit is utilized properly. When you find these, they should be very obvious! Again, these opportunities are everywhere when blood is in the streets and darts can be thrown at anything that fits the aforementioned criteria with a high likelihood of appreciating greatly into the future. But in markets like what we have now, care must be taken to ensure you aren’t buying some sort of value trap. I think it is prudent to demand some sort of company or industry specific turmoil that you can understand and know with a high probability the outcome on the other side. The short-termed market sells these things off like crazy but with a long term mindset, turmoil creates opportunity. I don’t think missing earnings due to the falloff of covid earnings counts as turmoil, and if you think it does, just exercise care and ensure you understand business and its earnings well and most importantly, ensure you have a margin of safety. I’m done rambling…back to the 15% FCF yield and 10% growth.

-

I remember reading some of his old comments back from his early college days while he was investing as a side hustle in medical school. If I recall correctly, he uses an EV/EBIDTA screen to find the cheapest companies and then uses a combination of trend charts to catch upward momentum such as simple moving average, MACD, and stochastic slow. Again, I’m regurgitating this based on memory from a while ago but this is why you see him moving in and out so often. He’s really looking for a quick trend upwards based on momentum and then exiting. Obviously there’s more analysis that goes into than these simple metrics but if you analyze most of his holdings and his entry points, you’ll largely find he still sticks to these metrics.

-

Constellation is actually partnered with Rolls-Royce to aid in the study and potential operations of the SMR’s.

-

Systems within the stations can be upgraded to modern/newer technology and often are. Mods are common and while they create more reliability and have better safety measures, they typically are very expensive due to the engineering requirements needed and rarely do they allow you to reduce staffing…nor do they create a power up-rate to allow for more power generation. A perfect example of a huge maintenance capital expense. Even modern nuclear plants such as the Westinghouse AP1000, require extensive staffing to operate due to the “tech specs” mandated from the NRC.

-

I’d like to make it known that I am in a position which has no inside knowledge or decision making on CapEx spending or regulatory actions. However, I am aware in a broad sense of the operations and economics. Again, I work for Constellation (was recently spun off from Exelon) which is mostly present in IL as far as nuclear power goes but they also have plants in New York, Maryland, Pennsylvania, and New Jersey. IL, NY, and NJ all have subsidies in place to keep nuclear plants operating and without these subsidies, some of the nuclear plants within these states would likely close due to the economics. It has been a common theme in the industry to shutter money losing plants and it appears this will be the case until the power market offers higher prices or subsidies become more permanent. All subsidies currently in effect are state level and have expirations ranging from 2025 - 2029. Each plant has a different cost structure but a goal would be to keep operating costs to about $25/MWh. Some plants are there, some are nowhere near this number. Single unit plants cost drastically more to run due to lack of scale efficiencies and will never meet that cost. There were times in recent past in which our market had negative power prices causing us to effectively pay to have our power taken. During these times we essentially down power to cause a demand spike which increase prices. A nuclear plant isn’t designed to increase and decrease on demand and it is a slow and in depth process which takes lots of focus and perfect execution each time we do it. The market is much better now with inflation running rampant but is it sustainable? If not, some sort of subsidy will need to exist far into the future in the states which are unregulated. Natural gas is so difficult to compete against. As a quick example… nuclear plant takes roughly 600 - 900 employees to run and the fuel isn’t cheap and the cost and time to build is absolutely off the charts due to regulation and the nature of the technology. Constellation recently built a gas plant in Texas which produces the same amount of power as a large nuclear plant (1200 MWe), costs a fraction of money and time to build, and takes less than 30 employees to operate. The playing field isn’t even close to level but it is what it is. Input costs such as fuel and staffing are out of the hands of the plant just as much as the power prices received from the power produced. The regulations will never disappear in nuclear and I don’t see them lessening much either. Electricity is a commodity and nuclear plants are expensive to operate so the only advantage they have is being a strong player in the ESG world or the fuel source becoming hugely cheaper than that of natural gas. But is ESG just a fad? How do you value a company like CEG? I personally can’t and don’t own the stock because of it (even with a stock purchase plan). It’s very complex as can be seen by their 10k being 800 pages. They do have substantial value in regards to barriers to entry. They are valued at an EV of about $26 billion currently and there’s absolutely no way a competitor could recreate their assets with even $100 billion. But is that really value when your producing and selling a commodity from a highly regulated plant? If one can figure out the future of green energy in America, it could be a great play. At this point in time I think there’s high certainty of a nuclear presence in the future. But what will it look like?

-

I don’t have an exact percentage on that but I can shed a bit of light on it. Without going into great detail, almost everything in a nuclear plant has an abundance of regulation associated with it. This ranges from staff to equipment…especially safety related equipment. While staffing isn’t a CapEx, some if not most of the components being replaced fall under CapEx (some fall under SG&A expenses). Anytime a component or piece of equipment is replaced and/or modified, regulation deems it must be rated for specific requirements that make it safe for nuclear plant use. A lot of the components are highly specialized to nuclear plants and are purchased from companies who specialize in making these components and they have significant costs associated. For example, while I’m not familiar with requirements at O&G plants, I can say with high certainty that if a nuclear plant needed a valve versus a gas plant, our regulations would cause drastic price increases to deem that valve “nuclear grade”. Regulations are intertwined in nearly every aspect of operations. However, nukes generate a whole lot of very reliable base load power and some make boatloads of money during peak summer and winter seasons even with the associated costs.

-

Nuclear is the best, cleanest and safest option yet many unregulated plants still need subsidies to remain competitive. Energy prices now would make them profitable but this is likely not permanent and they will need subsidies to continue running far into the future. They are very CapEx heavy requiring high staffing numbers, numerous regulatory guidelines above and beyond what’s required at gas plants, special safety ratings for almost all equipment, etc…. I work for Constellation at one of their nuke plants so I am biased and very pro nuclear. However, having the risk of early retirement due to poor economics makes you wonder what the future holds for nuclear as a whole in the U.S. Currently we are hoping for federal policies to displace state policies for the long term.

-

$291 million AUM as of December 31, 21.

-

Depending on your broker the process will be slightly different so just Google how to do edit your tax basis based on your broker. It is typically done post trade so you’d have to sell first, then go in and edit which shares you want to sell. You’ll get options such as FIFO, LIFO, and custom. Select custom and manually select the shares. Pretty easy process…at least on TD Ameritrade.

-

About 4.25x. Had about $100k in equity and $425k in mortgages.

-

Long post but I wanted to explain it well to put a better light on our decision making. We sold 3 of our investment properties (vacation rentals) in November of 2020 after owning them for 7 yrs, 4 yrs, and 2 yrs. Probably a mistake in the long run but the market offered us an amazing opportunity and after weighing the then-current environment, we decided to sell. They we’re amazingly profitable and overall, I mostly enjoyed managing them even with a full time job. It was kind of a perfect storm of factors hitting all at once that pushed us into selling. It was a VERY tough decision because they performed so well…better than anything I’ll ever invest in again honestly. We in hindsight timed the market perfectly when we entered, though, not so much when we exited. We got our first property by putting down $40k including down payment, closing costs, and minor repairs and it was immediately earning about a 25% annual cash on cash return. We used the FCF to purchase our second and then the third property. We entered the market when it was relatively depressed and values were still reasonable compared to the rents vacation rentals brought in around the area. Vacation rentals weren’t hugely popular but we still managed to maintain about 70% occupancy on our first property because the market wasn’t overly saturated versus the demand at the time. By the time we got our second, the vacation rental market was heating up as far as travelers accepting them and renting them, but the housing prices weren’t really on the rise to reflect it yet. Hell, our second one didn’t even appraise out at an already cheap asking price and the realtors cut their commission to make the deal work. By the time we got our third, prices began to reflect to popularity of vacation rentals and we were rolling with about 85% - 90% occupancy. Probably an easy 40% yearly cash on cash return averaged between the 3 of them at this point. We relied heavily on ABNB and Vrbo, but had a huge focus on obtaining more direct bookings through our website because I knew relying on listing sites would create more risk because we lacked overall control. The market was very competitive and nearly impossible to rank on google for our personal booking site without some serious cash for SEO. So, we kept relying on the listing sites. Enter Covid and holy hell did it change things in short order. Massive cancellations (to be expected) and mass confusion as restrictions rolled out state by state. We got through the initial phase thinking the worst was over but no way. Vrbo wasn’t too bad but ABNB took the ownership and decision making completely away from the owners and began overwriting our policies and contracts that the guests signed giving full refunds at anytime a guest asked for it. Day of check-in, a day after check-in…didn’t matter. Guests took huge advantage of it and we couldn’t do anything about it. Needless to say, we and our business felt very vulnerable to something completely out of our hands. What was once our biggest asset, became our biggest liability. Even with an amazing rental business and high returns, I couldn’t see going forward with both Vrbo and ABNB getting bigger and gaining more authority in the market. It was a huge headache and I could no longer sleep well at night because I couldn’t rely on our reservations going through. Demand skyrocketed and reservations were easy to get even after raising rates nearly double during certain times…but you only got paid if they actually stayed and many people took advantage of the rules that Vrbo and especially ABNB put in place to protect the guests from Covid. Ultimately the quality of guest quickly deteriorated and while we were making tons of money from the boom Covid caused, I felt more nervous about the future than when we first entered the market as rookies. Property prices eventually soared because of the huge rental demand and increased rental prices and after weighing our options, we sold. Again, probably a mistake but I don’t regret it one bit because of the huge uncertainty I felt knowing I had to rely on Vrbo and ABNB who basically owned my ass. The investments worked out great as I was able generate an approximate 52% CAGR after taxes over the 7 years. We weren’t timing the market by any means… We simply felt the market presented us a gift after the factors mentioned above took place. Turns out we sold too early and if we sold now we would’ve had a CAGR of 64%. But I don’t regret selling when we did and wouldn’t change a thing. I think the vacation rental market has a lot of change yet to occur but it will likely work out very well over the long term. Sometimes if I really think about it I feel as though it was a short sighted and emotional decision to sell, but I very quickly remember the feeling of having the rug pulled out from under us and return to the frame of mind which is happy we sold. The story changed and I couldn’t see a certain future any longer…

-

I have a couple of things I want to cover in this post. First, I am a relative newbie at value investing and analysis which brings me to my question here about reinvestment rate and wrapping my head around it correctly. Is there anyone willing to explain what exactly the rate means from an analysis standpoint and what the number tells you about being a worthy investment versus a hard pass? The equation I'm using for Reinvestment Rate = Net Capex + Change in NWC / EBIT(1-Tax Rate) Where: Net Capex = Total Capex - Depreciation & NOPAT = EBIT(1-Tax Rate) I believe I have a basic understanding of the number, which is given as a percent. After numerous Google searches and sifting through content, it seems the reinvestment rate represents what percentage of cash flow the business has been reinvesting to grow. I also understand that it is important to couple the reinvestment rate with ROIC which should give you a reasonably accurate measure of how the intrinsic value of the business should compound into the future (i.e. a business that reinvests at a 10% rate and has a 25% ROIC will grow at a rate of 2.5%). All of this makes sense, but as I begin doing calculations and playing around with the numbers on random businesses I find that several actually have sustained negative reinvestment rates. I know why they have negative reinvestment rates simply by looking at the calculation which is due either to depreciation being larger than capex, or change in net working capital being negative (or more negative than net Capex). It will also be negative on businesses with negative EBIT but I don't plan to invest into businesses with sustained negative EBIT. Some of these businesses have really good ROIC numbers as well which I know isn't really a reflection of reinvestment rate simply because some businesses can have a high ROIC but can't necessarily reinvest all or even some of the cash flows which are a byproduct of the high ROIC. With that said, I always read/hear that businesses with high ROIC are good businesses to invest in and I've always sort of left it at that. However, now that I'm calculating reinvestment rate, I am having issues with understanding what it means for the business and for the investment success or failure. Questions that pop into my head that I'm having trouble grasping are: What if the reinvestment rate is negative and is mostly negative over time? At what point should this business be avoided even if it has other positives such as high ROIC? It should obviously be returning this uninvested capital to shareholders via a combination of paying regular dividends, special dividends, and performing material share buybacks with the money it can't reinvest into the business...right? Not all businesses are the same and to me it seems like the equation doesn't capture the essence of all business models. For example, what if a business is a serial acquirer? The numerator doesn't factor in cash outlaid to acquisitions which affect growth of the business, while the denominator certainly captures the EBIT generated from them. To expound on the above point, the numerator also doesn't wholly factor in cash outlaid for the purchase of intangible assets. Yes it accounts for amortization of these assets (assuming you are using the depreciation/amortization line on the cash flow statement to find Net Capex) but shouldn't it also be included in the Capex since intangibles can technically be seen as a capital expense? Reinvestment Rate is a calculation based on the past, just like most other metrics. Is there a way or a standard to measure or guide the future reinvestment rate based on previous trends? For those that rely on this metric for entry into a business, do you use it as a standalone number or do you always pair it with ROIC? Businesses run into hiccups all the time. How many years would a sinking reinvestment rate take for you to reevaluate your position in a company? Sorry for the long winded post. The second thing I wanted to mention...actually to request...was to create another section on the forum dedicated to learning. This forum is a wealth of knowledge and there is a huge knowledge gap between the members (which is exactly why forums like this are so valuable) so there are times when things aren't exactly easy for me to grasp. I'm assuming if I am not easily grasping an idea, that maybe others aren't either. With that, if it is possible to create a knowledge or learning section, those who need help understanding something can be taught by those willing and who have a grasp on said idea. Reinvestment Rate is a good example of something that could be taught in a knowledge section. Teaching is self-reinforcing and beneficial for the teacher and great for the one learning as well. Should be a win-win. Thoughts? Thanks

-

Added to BKEP below the $3.32 offer to reduce my basis a bit.

-

Both Amazon and ebay are creating a need for a high dollar marketplace built on trust. Gregmal nailed it with the descriptions of dollar store and pawn shop and I don’t see how they can get past these connotations with the scale they’ve developed in those markets. Not saying they are bad businesses because they are clearly not, but there is a huge void they’ve created in the high dollar market and someone will eventually fill it. It’ll be interesting who will be the first to get to scale and profitability with trust and reputation still intact. There are several sites trying to do this, but it still seems highly fragmented in terms of offerings and trustworthiness. It seems like most deal with fashion (farfetch, stock x). Then there is 1st Dibs who is the only publicly traded company I know of that you can dig into and they seem to be less fragmented with offerings from furniture and art to watches and fashion.

-

This may be the wrong place to ask this but I didn’t want to start a new thread for something that fits here. In a Japanese business I’m reviewing the financials for, there is a section that states the “total number of issuable shares” and a section that states “total number of issued shares”. Can someone please give me some guidance on how I should be looking at this in regards to valuation and any per share metrics? On all other company financial documents including the sections stating stock ownership and percentages, the percentages are based on the issued shares number, not issuable shares. The share repurchase documents also state repurchase of a certain percentage based on the issued amount. The shares outstanding on Tikr also show the issued amount versus issuable amount. there is a huge difference between issuable and issued: -Issuable = 120 million -Issued = 36 million Thanks

-

Is Everything Around Us Saying That....

Value_Added replied to Gregmal's topic in General Discussion

Definitely seeing this too, though I can’t help but feel it is mostly a race to the meta verse while trying to take large marketshare of mobile along the way. I think the meta verse is far into the future (not in application, but in wide adoption) and mobile will be the cash cow until then. It’s interesting to see how the large players are positioning themselves. TTWO seems to be positioning themselves toward a mobile focus based on their most recent acquisitions being pure mobile plays, while MSFT’s portfolio will be more heavily weighted toward traditional console/PC (King is a huge mobile player, but will account for a small portion of MSFT’s overall catalog). Mobile offers a more competitive landscape because the barriers to entry are much lower (basically nonexistent) than traditional console and PC. They are all competing for your time and the styles of games can range from ultra simplistic to very in depth - A very important point to take note of is that on mobile, budget isn’t a must for addictive entertainment creation. Arguably, the simpler the game, the better since most people play mobile in quick spurts. The TAM is also much larger as everyone has a phone. the mobile environment is more like Silicon Valley and tech in which the next big thing could be created by some random person in their garage. I believe that introduces some investment risk in highly focused mobile plays which is why I didn’t love seeing the price TTWO paid for the Zynga acquisition. It just seems to be banking on so much future success and revenue generation. -

Insider Trading By Politicians Should Be Stopped!

Value_Added replied to Parsad's topic in General Discussion

-

how about BKEP? Do you just use it as a cash substitute until you find better investments or are you long and looking for the potential long term upside, or a combination of both?

-

PERFECT, thanks. I knew I was missing something, but just couldn't figure it out. I appreciate it, I always learn a lot from this forum.

-

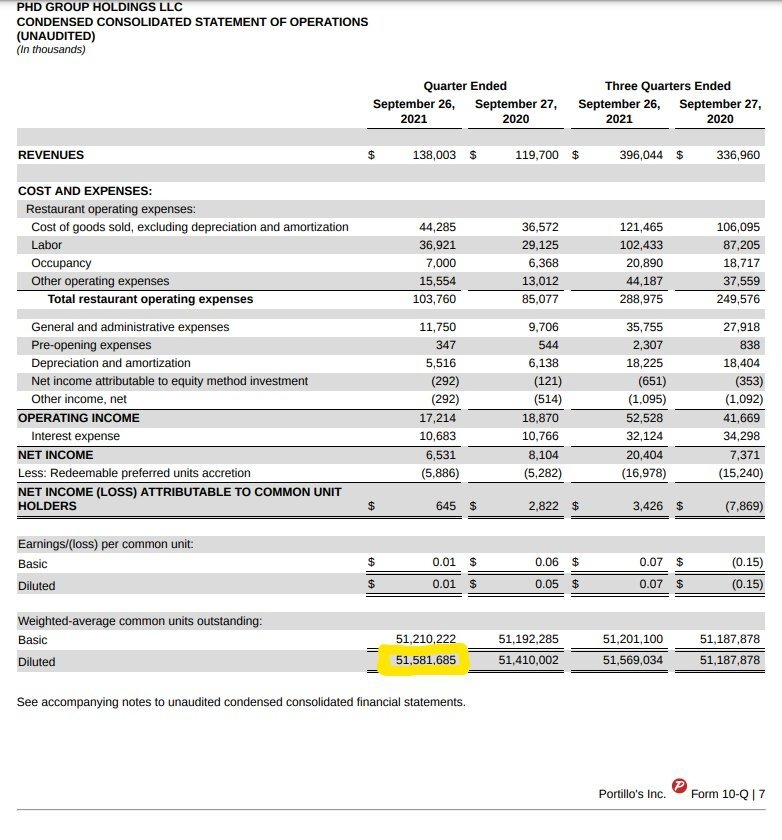

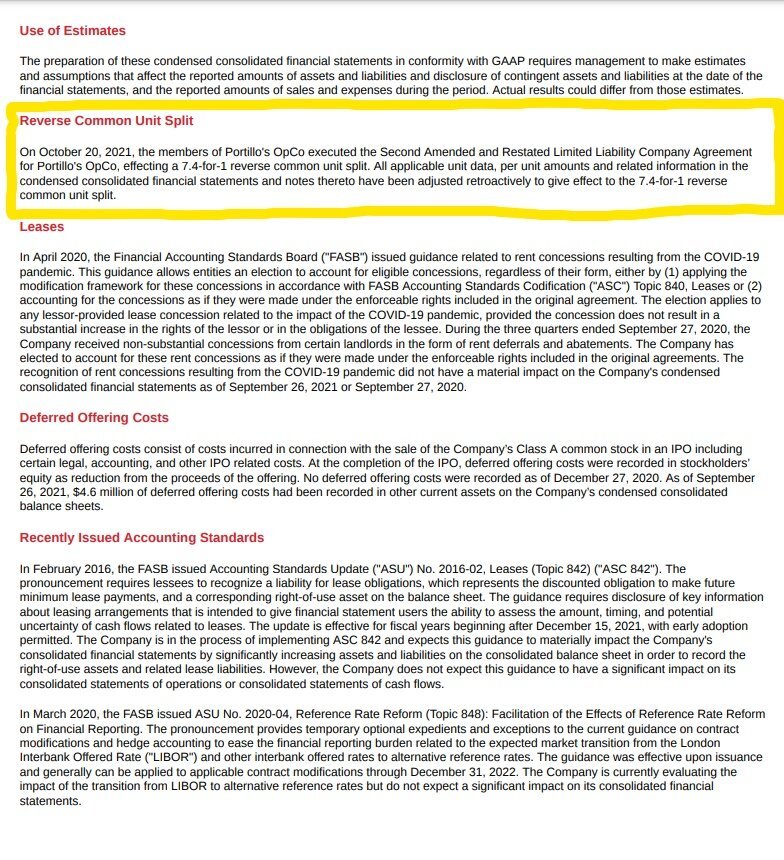

This makes perfect sense and I see that number represented here: However, my continued confusion comes from their most recent quarterly filing in which they mention this reverse split that occurred around the time of their IPO yet wasn't mentioned in their IPO filing. Their IPO filing which you've posted above, shows about 378m shares outstanding, yet it also shows as I've highlighted from the same document that the total number of LLC units is 71.5m. Now if we look at the newest quarterly report and account for the 7.4 to 1 reverse split they mention, it equals roughly the number of shares outstanding in this quarterly filing (51m). The only way to get there is to start with 378m shares... I'm not a guru at financial statements and am by no means correcting anyone, but it really seems there are discrepancies between the filings. Are you all pretty certain that its 71.5m and it is just misrepresented on the newest filing? Trying to dig into the business and this is throwing me off.

-

I love Portillos. I looked into them via their IPO report and the share count information was very confusing (could be something missed on my part). In their IPO documentation they had a total of 378m units/shares outstanding which was broken down by Class A, Class B, and LLC units totaling 378m. This document came out on 10/22/21. Their most recent quarterly report mentions a 7.4 to 1 reverse split which brought their count to 51m outstanding. The reverse split occurred on 10/20/21. Not saying anything odd is going on, simply that it’s a bit confusing as to why this wasn’t mentioned in their initial IPO documents. Maybe something to look into. Hope you share your thoughts on Portillos post analysis and look forward to hearing them if you do. From someone who has been eating there for years, it’s an amazing chain offering a great expirience.

-

TIKR.com | Free Beta with Coverage of 50k+ Global Stocks

Value_Added replied to Garpy's topic in General Discussion

Does anyone know why Japanese financials on Tikr show EBT on the cash flow statement versus net income? -

Makes a lot of sense and thanks for sharing.

_LI.jpg.81d0e82564f940da5651720520fc26aa.jpg)