changegonnacome

-

Posts

3,854 -

Joined

-

Last visited

-

Days Won

7

Content Type

Profiles

Forums

Events

Everything posted by changegonnacome

-

Yep and those forward earnings estimates are looking very very suspect

-

As I've said before - TINA dominated flows into equities up until very recently.....multiples expanded in response...........could it be that record bond issuances YTD and by extension purchases is demonstrating that TINA is over?.......and equities are facing competition for flows for the first time in over a decade?.......as allocators think about deploying that marginal dollar into competing financial instruments they are being presented with options with acceptable returns that aren't stocks for the first time in a long time. Retail investors/savers likewise - as CD's & high yield savings accounts paying 4% start to look like not such a bad place to be on a risk/reward basis vs SPY/QQQ that took you to the woodshed in 22. In a QT world with shrinking money supply such that marginal liquidity is contracting.......record flows into bonds like this have consequences......the marginal dollar game has become zero sum.......the liquidity/money supply pie is shrinking, not expanding as the Fed rolls off the balance sheet......and so for bonds to 'win' flow, equites have to 'lose'. I myself have a confession to make - I bought a 3M T-Bill yesterday with an annualized YTM of 4.4% with some cash laying around. Never bought a sovereign bond before. It felt weird. Pray for me.

-

Agree with Mark’s - optimism around falling inflation , the severity or otherwise of a recession and an impending Fed pivot pervade the market at ~3900 - 4000 I also agree with Mark’s about being bottoms up…..I have a top down view…..but a bottoms up methodology & approach….I remain pretty much a fully invested bear

-

Yep I agree - style drift....as I said The idiosyncratic ideas i spoke about was earlier in the funds history......today it looks like ARKK-lite, this was his downfall on 2022 performance anyway....lets see moving forward..........this is a tough tough game and a humbling one......one swallow does not make a summer........you can look like your winning or losing for quite a long time, even when your making horrible or indeed astute contemporaneous investment decisions......because the market simply going up or down feeds you confirmation bias.

-

Lying with statistics……you’d run out jail cells pretty quick for that particular crime ……. but a crime nonetheless

-

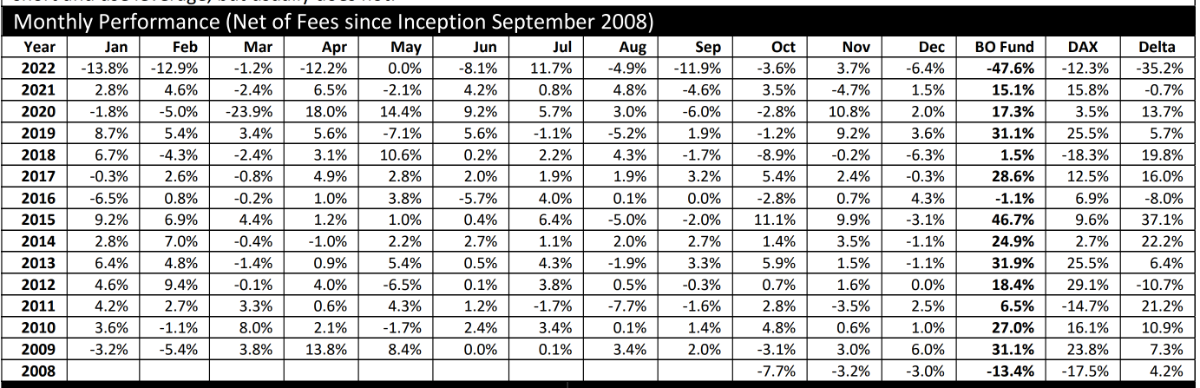

Part of the style drift I spoke about…..I remember seeing the portfolio years ago……and it was predominantly EMEA……and sector weighting was to financial services, if anything, back then. Everybody started to hear Cathie Wood in their head it seems towards the end of the great bull market Interesting on return fact sheet……if anyone cared too they should email him and ask…..I myself couldn’t be bothered.

-

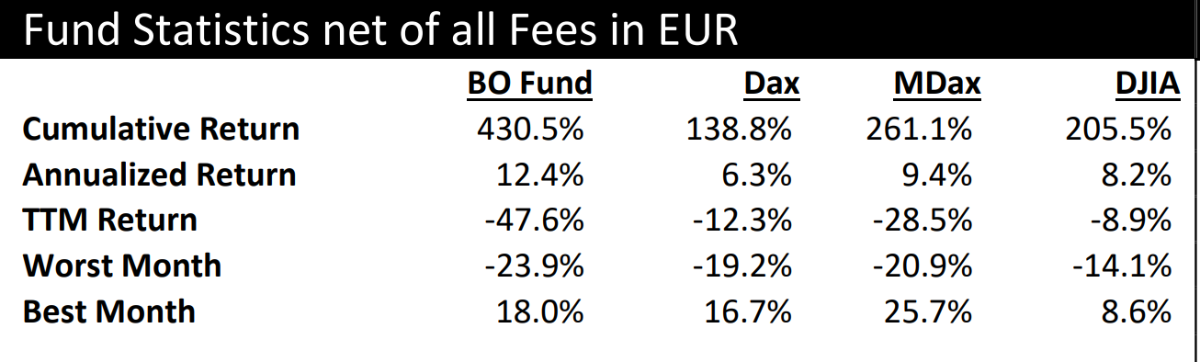

See below - European manager so EUR investor base........as European manager then your benchmark isn't really SPY.....however....returns net of fees annualized & including the 2022 drawdown for fund come out at a 12.4% CAGR

-

RVCapital it seems suffered from kind of style drift.........he started of as value-ish, then GARP.......but GARP worked so well during ZIRP in the late 2010's & his returns so good.....that he went from growth at a reasonable price to growth at any price and ended up owning Carvana in the end with shit loads of debt and growth that had to happen to keep the whole enterprise afloat......difference between RVCapital and Clifford Sosin's/CAS Parters.....who i think RVCapital coat-tailed into Carvana is that at least Rob didn't let Carvana get to be 60% of the fund......and so he'll live to fight another day. Regardless Rob has shown an ability to make the right calls on idiosyncratic ideas. The stuff he does with emerging managers is also to be commended. I would say the price for long-term outperformance in a fund managed by competent manager is occasional & sometimes spectacular underperformance....its to be expected when you hold things that don't look like the index & the cruelty that is mark-to-Dec 31st which by luck alone makes some managers look like geniuses or losers (for a short time).

-

What broker you using Spek think you said up thread your East Coast?

-

What are you listening to ? (Music thread)

changegonnacome replied to Spekulatius's topic in General Discussion

Jeff Beck ripping it up on Roger Waters tune -

3% Risk free rate + 3.5% ERP............is a PE of 15 no?

-

Where Does the Global Economy Go From Here?

changegonnacome replied to Viking's topic in General Discussion

& thats the point - the Fed hits in order & sequence (1) Financial instruments via money supply tightening/QE/QT (2) Credit creation via Fed funds (3) Income/Spending via a fall in no.2 the Fed can only directly control the money supply (QE/QT) but this only effects financial assets, not "real" assets like cars for example....they print cash, buy a bond and a financial market participant swaps one financial instrument the bond (treasury or MBS) for cash from the Fed then most likely turns around and buys another financial instrument ordinarily further out the risk curve (high yield, perhaps even equities). Anyhow you can see how the Fed 'put' and its transmission mechanism works very well flooding liquidity into financial instruments with relative speed, ease & directness......the Fed put is so attractive as a tool because it works so quickly........the real economy is different..........to effect it as a Central Bank, you need to hit the two source of funds available in the real economy to transact not for financial instruments this time but REAL goods and services......those two sources of funds to buy say a new car are either (1) Credit or (2) income/spending..........in some respects to get to No.2 income/spending....the Fed in a derivative manner has to go through (1) the credit creation channel first........and because credit becomes spending in the real economy.....and because one persons income is actually somebody else's spending eventually you get to a situation where the Fed.....first reduces credit creation but then by extension starts a chain reaction of failing spending/incomes....falls in income which manifest in unemployment & eventually a recession. An inverted yield curve as @TwoCitiesCapital quite rightly points out is EXACTLY what the Fed wants.....it wants to whack credit creation such that spending......and then eventually incomes get whacked. We've clearly seen the decline in credit creation for new homes and now it seems autos too.......so we are clearly firmly at the No.2 point with the most highly sensitive products hit first.......unemployment has held up but once it starts to go up.....what you are looking at in real time is actually like starlight - its an echo of a hypothetical credit creation event that did NOT occur a number of months ago.....these are the long and variable lags central banks talk about.......Sahm's rule suggests once the first 0.5 uptick of unemployment occurs above the 12M average low.....the unemployment rate goes on to complete a full 2 percentage point move up.........makes total sense in some respect the other 1.5 move got baked in the cake months ago as other credit creation events didn't occur and a historical spending 'hole' opens up in the economy and absent a time machine nobody can do jack shit about a loan that didn't get made six months ago.......its credit spilt milk.......rising unemployment in a very real sense then is the trickle down effect of loans that never got created......and this is ultimately why 'soft landings' are so rare........you want unemployment to go up to slow inflation/economy.......but at the time your actually raising rates your never quite sure exactly how much future unemployment your creating at the time.........and when unemployment does show up its only the months that follow that reveal how much joblessness you actually created in the past......and invariably you usually create a little too much given your fumbling in the dark......and in this particular instance the Fed it seems has signposted its willingness to create a little too much via its speed/aggressiveness, as opposed to too little given the stakes. When unemployment does show up............and I firmly believe it will.......and without sounding callous its going to be very curious to see the concentration/scale of jobless claims their unprecedented rate moves in 22 have created in 2023...one might expect in response unprecedented month over month rises in jobless claims at some point mirroring their earlier moves. -

Yep me too - personally I think Central Bank's should be given a floor on rates to stop them playing these silly monetary games......all investment should have a hurdle rate..........lets call the floor 2%.......crazy ZIRP world undoubtedly led to a lot of misallocation of resources......and why.......well because the god damn politicians didn't have the balls to step up and do what they are elected to do.........so they left the 2010's to a bunch of unelected technocrats in Central Bank's to figure out how to 'fix' the economy and we got ZIRP........it was IMO a real failure of the political class that didn't have the imagination/fortitude to tidy up after the GFC

-

I dunno @Gregmal we can chat & debate the other stuff...inflation and it sources/persistence etc.............but its been unusually and crazily and yes historically unusual labor market..........3.5% unemployment really isn't 'normal' see here https://fred.stlouisfed.org/series/UNRATE. In the historical record you've got to go back to like the 1952 - 1954 period to find any persistent period of anything similar...this post-war period was when USA was the only game in town industrially with Europe in ruins.......and the Marshall plan requiring the undamaged industrial base of the USA to rebuild Europe......now did unusually low unemployment back then trigger inflation? The answer is No - but the country was still 'young', easy productivity enhancing investments could be made..............Eisenhower built the god damn inter-state highway system for gods sake! Imagine if Biden had such a no brainer productive capacity enhancing project available to him......then you had women and immigrants from Europe joining the labor pool. So I dont accept cherry picked point in time as it pertains to the labor market - there is an anomaly there and one with likely consequences vis-à-vis inflation. We can debate the quantum.....but a 'hot' labor market clearly has an influence on inflation in an economy like the US which is as 'developed' as one can imagine...........and an economy which steadfastly seems to refuse to accept any immigration of scale/consequence to bolster it workforce/output capacity..............all against the backdrop of deteriorating demographics.

-

Yeah I agree - its a question of who is right or wrong here....... Option 1 - if inflation is going back to 2% all by itself then the Fed is wrong to turf a million people out of jobs for absolutely no reason. Guess this is your view @Gregmal that you know the inflation thing is a bit of nonsense at this point based on the data.......and 2% is just around the corner and really the first sign of trouble in the labor market the Fed should immediately pivot and deliver some cuts so as to support employment/the economy. Option 2 - The alternative view of course is that an historically unusually tight labor market is contributing to inflationary pressures that are real and not going away without meaningful intervention........those inflationary pressures if not dealt with expeditiously could result in a sustained persistent period of inflation one where inflation expectations become unanchored making them even more difficult to remove later............and so the lesser of two evils is to accept some labor market turbulence now and weaker economic growth, restore definitively & irrefutably price stability and then build out an economic recovery & jobs market from there with stable prices as its bed rock. When I think of the two options from both a risk management point of view and then from an unelected bureaucrats point of view attempting to minimize his career/reputation/legacy risk........overwhelmingly I can see why Powell is choosing the latter option. To choose Option 1 and turn out to have gotten it wrong (again, remember transitory!) would be a serious egg on the face moment and would resign Powell's tenure as Chair to the funny pages of Central Banking history books......Option 2 on a pure self-interested ego legacy driven Powell basis is the 'right' option. It ensures he's the Fed Chair that slayed the inflation dragon not the next guy or gal. If incentives drive outcomes - his 'incentives' are clear.......you go for Option 2 all day long

-

Yep - it’s called NAIRU and according to it - with a 3.5% unemployment rate the US should indeed be seeing some inflationary pressures……non-inflationary unemployment level, again according to it is ~5% Congressional budget office estimates the ‘natural’ unemployment rate to be 4.4% Whatever way you slice it we are in an unusually tight labor market. To have inflation above the 2% range in some respects is exactly would you expect if presented with just these data points. Suspect the Fed wouldn't lose a wink of sleep if unemployment went up to 4.5%…..issue with that is that you don’t move an economy from 3.5% unemployment to 4.5% without a contraction in GDP. Beyond 4.5% unemployment I think their fingers are on the easing trigger. https://en.m.wikipedia.org/wiki/NAIRU Other more interesting measure I check-in on is this: https://fred.stlouisfed.org/series/SAHMREALTIME Sahm’s rule - meant to signal the entering of a recession in real time based on the rate of change of unemployment

-

yep COVID supply chain/energy stuff is peeling off….no question……mathematical certainty…… this is made in China and made in Ukraine inflation….it’s disappearing and it’s disappearing fast in the data……..contemporaneously it’s already gone…..the trillion dollar question is whether underneath this exogenous inflation we have Made in America inflation….a hangover from too much fiscal and monetary largese……I suspect a modest 100-150bps of inflation of this kind exists….and the question is what happens when we hit perhaps 3-3.5% on CPI and the damn thing stops moving down as beautifully as the last few prints. The Fed has already sign posted their plan go to ~5% and hold there for not just as long as needed but it sounds to me like they’ll hold it, out of an abundance of caution, a little longer than might actually be needed. That idea of doing too little versus too much as being the greater of follys to commit. Not delivering a pivot at a time it would ordinarily have in the past is gonna be a scary moment for market participants raised on the VIX 30+ equals Fed put/ stimulus…..what’s going to be even scarier is if those equity folks are holding things at x17 times earnings (5.88% yield) when risk free, FDIC stuff or triple A-rated paper is yielding 4,5 even 6% YTM. The equity risk premium (ERP) is something I’m becoming highly attuned to as IBKR starts to pay me ~4% to hold cash….is SPY at a 5.88% yield (17 times earnings) based on what is highly probable to be peak earnings an appropriate ERP? I really don’t think so. Cash and Bonds are competing with equites for the first time in over a decade…..and equites need to step up their returns to compete for flows in this new world. The way they do that of course is by having their nominal price fall. We’ve had some of that but not quite enough to bring us to historically normal ERP spreads. P.S. - of course one requires a view of future risk free rates here too 5% Fed funds is a point in time…..you think 5% Fed funds is an anomaly and we’re going back to 0%….then yep 17 times on SPY is a descent ERP. Which gets us back to the more difficult post-COVID world question and musings as @Dinar correctly lays out……are we heading into a new paradigm where inflationary pressures will stalk the West such that interest rates aren’t going back to ZIRP.

-

Perhaps but I think the CPI dropping is going to accompanied by some pretty painful earnings misses....and in some respects falling CPI is the other side of the same coin which is to say CPI progress is in some respects a function of a weakening consumer & falling demand..........so you've got some positive impact coming perhaps on lower discount rates moving forward (higher multiples) as a result of clear CPI progress but ultimately what good is a slightly higher multiple when the thing your multiplying (earnings) are falling. 2022 - multiples get whacked 2023 - earnings get whacked Thats my basic take on things......Fed drove up discount rates in 22, market got whacked.......tightened financial conditions......is beginning now to feed through into the real economy via diminished demand/spending......market gets whacked again....this time on E............how do I know? Cause the Fed told me so . But lets see......there's about twenty reasons earnings have peaked out and very few reasons ive heard pointing to an earnings uplift......the balance of probabilities is to the former not the latter

-

I think they, the Fed, 'get' it quite well...a recession of sorts is the point of all this tightening..........they are happy to induce one to ensure the inflation target is met absolutely & definitively........you can question whether a recession is needed or not to get back to two.........I think folks here have a built a case that inflation might indeed be "done" as of right now...........but in some ways thats another debate............the Fed, it seems to me, isn't interested in running the experiment the bond market is asking it too or puzzling/musing as we are here to whether inflation is gliding back to 2% on its own.....this might be a a type of "show me" 2% inflation Fed where it really wants to see the eyes of 2% inflation again before backing off.......and to some extent the Fed has been clear in the last year on what it perceives to be the greater of two potential sins it could commit - doing too much or doing too little.........on this quandary they are crystal clear......when in doubt on inflation do TOO much and it seems that they might just go ahead and do exactly that.

-

What are you listening to ? (Music thread)

changegonnacome replied to Spekulatius's topic in General Discussion

yep up with the best of the best - shocked when I read it earlier -

Yep all through this period inflation expectations when consumers have been asked have indeed remain anchored ...........which is a very important part of not having a multi-year entrenched inflation issue via inflation psychology. Came across this little nugget - notwithstanding the click-bait inflation title.........what the CEO of Kroger actually seems to be saying once you listen to him is that the prices of some of these food stuffs are not expected to go up at ALL this year & to stay where they are.............which isn't inflation but rather stable prices! What the host is looking for is actually called deflation!

-

Any sense in the Bay Area whether the scale of other opportunities are such that she should be able to pick up something pretty quick or a bit of dislocation happening at the moment?.......the tight clustering of lay-offs in big tech and in Bay seem pretty large...........I've a developer friend who for years worked in FinTech.......but cool FinTech..........he just took a job with an insurance giant.........still technically FinTech but not the MacBook/Bean bag/Cortado kind he's used.......it wasnt his choice and as he says this less about building the future......and more about trying to drag legacy COBOL systems into the present while not breaking anything

-

sorry to hear that @fareastwarriors what industry does she work in?

-

Of course the other thing I’ll say is that the math says in a full employment economy unable to get productivity above 2%…….any aggregate average pay increases across the economy that exceed 4%….see you breach your 2% inflation target….~5% nominal wage growth in 2023 would result in some measures of inflation reflecting that ~3% delta…… Which indicates what we’ve talked about - that last bit of inflation above 2%…..let’s call it the canyon between 2% and 3.5%…….closing that gap requires more than background noise of tech layoffs taking comp discussion from CPI down to 5-6%…..but rather down to 3%.

-

What kind of level you seeing anecdotally?