changegonnacome

-

Posts

3,854 -

Joined

-

Last visited

-

Days Won

7

Content Type

Profiles

Forums

Events

Everything posted by changegonnacome

-

I expect the exact opposite….the ARKK stuff is in trouble again IMO….most likely catalyst is another hike & even more higher for longer talk but more importantly repricing of that reality

-

Yep exactly what I mean - the growth stuff is in for another shalacking IMO. Inflation isn’t just going away….soft landing are fairly tales….and the idea that we may somehow be going back to ZIRP with the inflationary pressures sitting in the background, the decoupling from China & the outrageous government deficits & bond issuances has just completely killed the idea that rates will settle back into a 2010s ballpark….the bond curve has permanently shifted up.

-

Yep lets take a step back here........SPY has gone absolutely no where for over two years..........we were at this level back in June 2021.......its never regained its interim high of 4800. Lets also be clear......SPY earnings have fallen during this period......in nominal terms by a descent amount......and in real inflation terms by double digits. This has all occured during a period when the economy & consumer has remained surprisingly resilient....which is to say earnings have been falling in a 'good' economy...no bueno...which is just never a good thing and certainly doesn't IMO presage a new bull market (whatever that means) The index itself in recent years has become heavily skewed by large cap tech as everybody knows.......the mini AI bubble of early 23 + admittedly more robust earnings by what I would call the 'monopoly 7' as opposed to the magnificent 7 is a function of (1) the surprisingly good economy that was way more rate resislant that anybody had forecasted & (2) well they are monopolies they have unlimited pricing power that they can flex on the pricing side & they have to a certain extent untapped OpEx flexibility too.....because well.....they're monopolies. Dont have time to go look at the median stock in the S&P and hows it performed......dont need too....it hasnt been great.....and again when everybody talks about SPY being flat for two year.....yeah great....but thats not the truth....cause in those two years you had nice big chunks of inflation lets call cumulatively perhaps 15%.....so SPY looks flat over two years....but you actually lost 15% of your purchaisng power. Not good.....but it doesn't feel as bad as your account saying your down 15%. Like I've talked about for an extended period on here......the sources of funds for folks are being slowly constrained...much slower than I appreciated given rate insensivitiy....long duration stuff had a rally as it appeared through the final fall off of transitory inflation in the data that somehow inflation was done (minus any pain) and that a soft landing was incoming. That game is over now........inflation is rising again on the volatile stuff (energy/food) the issue is that volatility upwards is sitting on a foundation of core made in america monetary inflation that was hiding out the whole time and didnt budge in response to 500bps of rate rises......it didnt budge for the exact reasons I outlined in earlier threads.....it was monetary inflaiton driven by too much money chasing too few goods in a economy that was growing nominal spending way in excess of productivity growth such that inflation couldnt go down on this core number.......it is more correctly called wage-price-producvity inflation.....rising wages dont push up prices if productivity is rising by a commensurate amount..what we've had is nominal wages rising feeding into nominal spending that is rising far excess in of productivity such that we breach 2%.......that sticky underlying monetary inflation at around 3.5% is now the basis from which we will take unexpected and uninvited trips back up to 4 or even 5%+ on the headline number unless we tackle this core monetary....there is no painless way to tackle this core inflation....falling credit creation solves a tiny fraction of the nominal spending problem....but it isnt the main source of funds in the economy.....the main source of funds that become nominal spend is wages. The setup remains the same as 2022 IMO.......value is the way you play this......not growth.......and given stagflation is looking more and more likely given I see Powell + Fed board beginnnig to chicken out already......I think you play this more & more with hard assets & commodities....that old dog Buffett buying oil & monoploies like Apple is spot on......I've come to appreciate JOE as a bit like OXY......oil in the ground & land in the panhandle will always command a steady percentage of the endeavours of others......the same way an hour with the best doctor in town will always be exchanged for whatever the nominal sum is that would secure about 8hrs of lowly unskilled labor.....that barter relationship remains constant....its just the quoted nominal price of the currency that intermediates that exchange changes over time.

-

Good deal

-

In the same Dimon vein - the whole yield curve is shifting upwards Wasn't about now the time when the Fed was supposed to be cutting rates. The steepening at the long end......or an un-inversion/flattening by another means....is really the most interesting part of this period.........the yield curve shifting permanently upwards and resetting at a higher level is the kicker for assets prices.....a curve that looks something like 2.5% at FF, 4.5% at 10yr & ~5% at 30yr........is just a different world to the one we've been in the 2010's. Reminds me of supply curve shocks in economics.....

-

Interesting graph - the rise of indexing & automatic buying via ETFs is very interesting during this period. Its a great achievement to get so many participating in the market. Perversely I've always thought how if your running a effectively a stock promote.....the best thing that ever happened to you in your life is the day your so called 'company' gets added to the Russell 2000 or similar......you've just achieved the promised land of stock promoters & fraudsters.........at the end of every month a bunch of disengaged price agnostic capital is flowing into your paper. It must be like winning gold in the olympics for these folks. Big picture however getting to 61% participation in the market is a great outcome....and its being done via vehicles (401k's + ETF's) where the worst behaviour of folks is minimized.

-

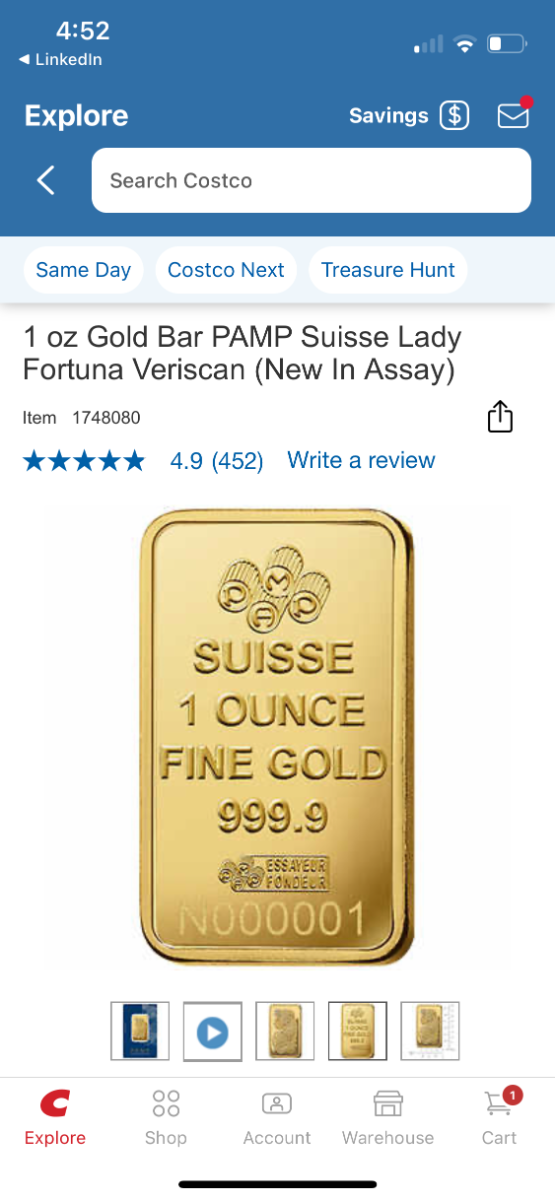

Forget bonds & equites….get 24ct gold bars this week at Costco…i shit you not just got the notification on my phone and had to look…...takes the treasure hunt aspect of Costco to the next level - $1,979…no idea if that’s good….Costco 14% margin is there for sure…then the Suisse Lady needs to get paid too!!!!

-

Howard Mark's latest memo has a bit about bond investing vs. stocks....how it's what Ben Graham called a negative art......in bonds as long as you can avoid the losers in a specific credit risk pool...the YTM you saw on the day you bought them is what you end up getting......your job is to weed out the losers........the beauty in the bond market ( at certain credit risk strata) is there are so few outright losers anyway......and so it takes in some respect LESS skill to assemble a portfolio where the anticipated YTM on Day 1 gets delivered upon maturity.....and conversely, cause they are so few outright losers, only a modest amount of diversification is required to get you close to the 'advertised' return even if you end up with a loser or two i.e. the delta between your anticipated & actual returns is highly highly likely to be minimal.....which is to say your probabilistic expected & risk adjusted returns are high on a relative basis.....not as high on an absolute basis as the potential in stocks but then you know that already. @thepupil is right the predictably of payoff & risk of nominal loss in the bond market with the yields where they are now is very interesting......and I'd argue we are in a curious time.......I think Buffett said once that when bonds become attractive as investments..... it's highly likely you should be buying stocks.....the curious thing today is that certain bonds do now offer attractive risk adjusted returns here.....equity like in their profile.......yet stocks haven't become attractively cheap IMO in response & it somewhat breaks Buffett's heuristic. Link to Howard Mark's memo below....I find his writing style kind of tedious so recommend the audio/podcast version of these things that Oaktree has started putting out at the same time: Audio - https://www.oaktreecapital.com/insights/memo-podcast/fewer-losers-or-more-winners Memo - https://www.oaktreecapital.com/insights/memo/fewer-losers-or-more-winners

-

Public Company Share Repurchase-Cannibals

changegonnacome replied to nickenumbers's topic in General Discussion

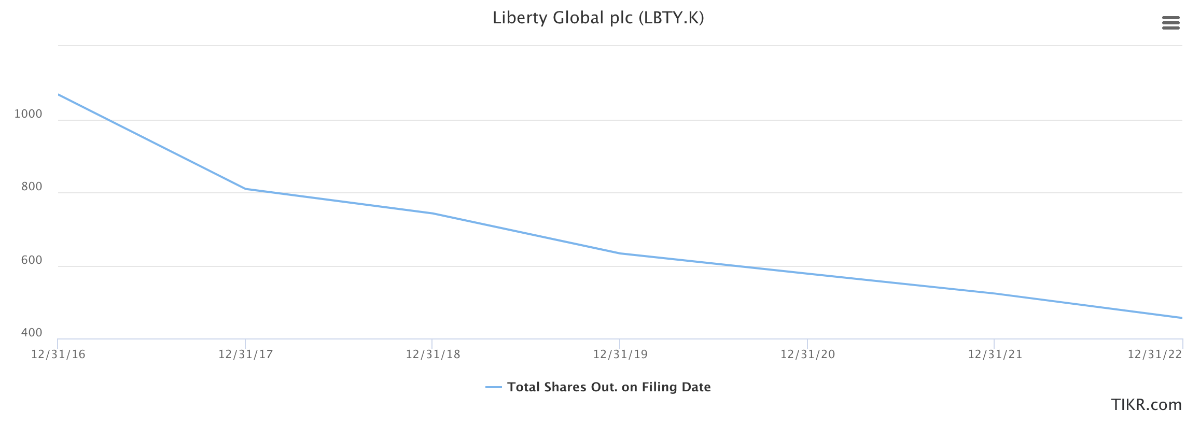

Cutting your shares outstanding by 50% in six years is pretty impressive for LBTYK....now not a perfect buyback....in the sense that they liquitated big chunks of the FCF in the business in sales.......so the s/o shrinking against stable or growing FCF base started to occur around 2019......so they've dropped s/o by about 30% on the stabilized/growing FCF business in the last three years

-

Joe Sixpack buying a six pack..or a carton of milk...isnt looking for finality of settlement & censorship resistance.....he's looking for ubiquitous acceptance, low friction & speed....and if/when his payment method (phone/card) is stolen...or a merchant scams him.....he's looking for chargebacks and theft protection. The value proposition where a lightning network beats M & V's value prop above is embarrassingly small..surprise surprose again....the TAM extends to paying for illicit goods and services. . The network simply didnt work in El Salvador........it was a disaster....an implementation flop. Scaling & driving acceptance when you cant support at best a few thousand merchants/customers in your pilot market does not bode well. The technical deficiencies of lightning are stark.......first that any lightning network/layer2 payments solution.....is contrary to crypto ideal.....see the more you want it to actually work.....it requires that layer2 solution to get very centralized very fast....payments at scale are hard....and like every decentralization project I've reviewed trying hard things....its starts to get centralized (in practise) very quickly. There is the age old problem....that is as the complexity of a problem grows so too does required effective centralization & concentrated control required to ensure its continued successful functioning & improvements.......its analogous to anyone that has worked on college group project or on a company project.......every successful project begins somewhat decentralized and shared across the group.....very soon as folks go around in circles getting nowhere a natural and needed centralization occurs...a natural hierarchy of responsibility & control....the crypto decentralization dream....that complex problems in the economy can be replaced by decentralized autonomous blockchain solutions is the deluded dream of mainly solo computer programmers who work always on their own in their basement or folks who never really had to deliver a truly complex robust solution at scale to the public.

-

Yep - inflation expectations are still the big thing....they remain anchored through this whole thing which is really a big win in an age where so many have lost faith in institutions.........lots of the recent pay disputes are somewhat about restoring purchasing power back to 2019 levels.....the danger as always broadly is that. (1) consumer inflation expectations move up such that wage disputes start to become about front running future inflation & (2) more importantly for investing that the long end of the curve begins to incorporate higher long run inflation expectations from the bond market and you get the 10yr/30yr moving up.

-

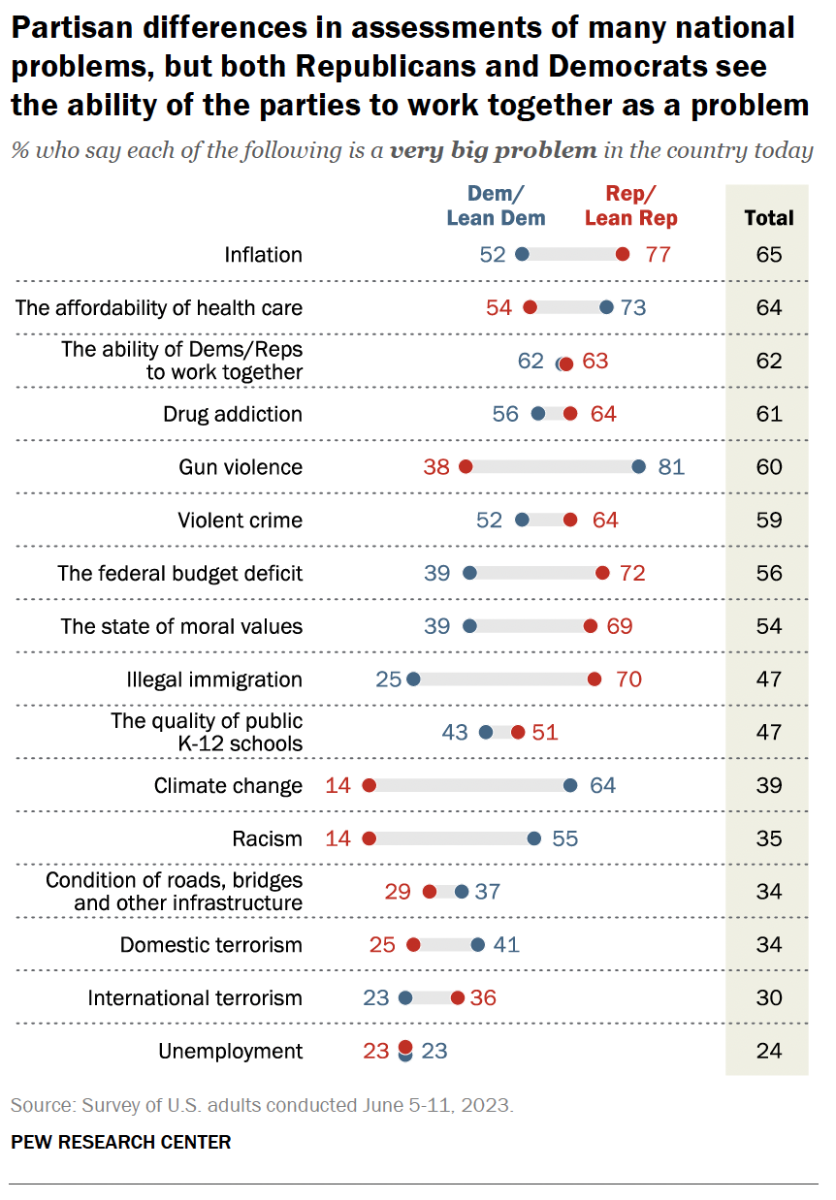

Yep.....especially economists of the left heading into a presidential cycle. You can call inflation data bullshit...it for sure has flaws....but the reality is the best inflation indicator is do people notice inflation in their daily lives or do they not.....and how much they care about it. The reality is contemporaneous political polling speaks to the inflation problem better than CPI....Core or SuperCore ever could....inflation isnt over when its sit as the the No.1 political issue (above healthcare!!!!) when pollsters speak to voters:

-

Listen it’s time to accept Bitcoin as a future method of payment beside Mastercard & visa rails for digital payment dream is over….layer2 protocols and the lightning networks chance to shine was in El Salvador….apart from the fact that layer2 protocols break the religion of crypto decentrlaization (cause it turns out to run an instant payment method that hopes to have V/M level transactions it actually requires a lot V/M centralization to pull it off). So now you’ve built something that looks like Visa Mastercard…a centralized-esque layer2 solution…with inherently less consumer protection/chargebacks/disputes such that it’s less consumer friendly…ok maybe it’s cheaper….but driving adoption for payments via cheaper interchange fees has failed….debit carrys tiny fees/discover has tried to undercut fees at times…merchants god bless them can’t get people to use them instead of CC’s…..the consumer is in the driving seat here…..but to top all that business dynamics & competition setup off….whatever layer2 protocol built on BTC has one MASSIVE problem….it ultimately has to phone home to BTC’s crippling slow spreadsheet to update….a spreadsheet that would make an oracle database solution from 1985 look like it was designed by aliens from another planet given its relative ability to process database changes. Gold is never going to be a currency it’s a store of value BTC’s last hope isn’t global payments enabled by layer2 nonsense built on it…..it’s a digital gold….a more portable virtual lives in your mind version of gold. This it has a shot at….id advise those in space….get down to business and make that dream come through….and don’t waste your time with this payments pipe dream.

-

Yep agree with this...and as expected from my point view and flagged a number of months ago......the problem for the inflation is toast folks.......is that during this whole time as the headline mathematically fell MoM in a kind of super late transitory COVID inflation rollover glide.....what didn't go away, in fact hasn't budged nearly at all in response to 500bps of monetary tightening is a very unpleasant fact....stuff that doesnt get on shipping containers in China but is rather produced domestically here in the US.........services......which account for 'only' about 70% of GDP......have been bubbling away consistently under the headline inflation is falling narrative at around 4% annualized....in the best month over month readings so more contemporaneously in mid/late-3's. The issue at hand as the Fed knows all too well........is that those types of numbers create an inflationary floor of 3%-3.5% for the US.....what I would call a fair weather floor.......on top of which inflationary surprises known (energy, commodities) and unknown move you up very unpleasantly, surprisingly & quickly into the 4 or 5% ranges. It will be interesting to see what happens next.......Fed Funds relative to inflation today.....has created 200bps of genuine monetary tightness......that tightness has emerged only recently and in response incremental modest rate rises (the last few 25bps rate rises) twinned to genuine falling in inflation. The big mystery is whom is actually feeling that tightness and is it enough to drive down aggregate nominal spending growth sufficiently...its not quite showing up.......corporates & a great many households fixed significant debt during ZIRP.......higher for longer has always been my base case......but its starting to feel like some more tightning might be required to end this inflationary cycle.......Fed funds perhaps needs to go higher at the short end.....but in fact the tightening may come from other sources....and that's an un-inversion of the yield curve in a way that folks haven't been predicting and that's an universion driven by the long end.

-

Exactly - to us the NATO expansion is of course innocent “we” would never be the aggressor….NATO is a purely defensive organization with benign aims*..…an opposing power however, Russia in this case, must assume the worst of NATO….paranoia is both the natural order of the international system but ultimately the correct posture. As great power the US has this exactly correct with the Monroe doctrine…..not a single piece of foreign military hardware can be placed anywhere in the Western Hemisphere. End of story. The cost of assuming the best of intentions from your enemy and getting it wrong - is that you don’t get to exist anymore. *lets be clear however it’s well understood and accepted….NATO was a mechanism by which the USA post-WWII got to contain the USSR as a peer global competitor

-

NATO membership for Ukraine in my opinion is simply never happening as long as Putin is President of Russia.........again it goes to the question of what was the driver of the invasion in the first place.....if your still wedded to Putin the imperialist theory then yes this NATO membership outcome is very possible, indeed likely - this was at the end of the day a greedy land grab that has failed miserably and the costs are becoming too high to sustain for Putin & justify its continuation and as such then you end the conflict with concessions (NATO, give up land captured). The alternative theory and the one with the most evidence IMO is Putin/Russia as existentialists.......globally isolated, shrinking economy, bad demographics, greening of the economy runing their long run biz model, cornered, scared rats concerned chiefly with the Russian's states security & survival over time..............this existentialism paranoia manifests itself in Russian-European foreign policy vis a vis Ukraine AND Belarus......which have always been the highest priority as bulwarks for Russia against a Europe & NATO it does not trust......as I've said before, using the existentialist paranoia framework, it is through the lands of Ukraine & Belarus that Russian state perishes as it nearly did in WWII. Now you can say its impossible what has Russia to fear from any invasions from anyone in Europe......."we" iwould never invade them.......it's crazy to think like that......but this is not the way the real world of nation states work........the ultimate intentions of your opponents are never clear......put simply in the international system of nation states......only the paranoid survive......or put another way as a leader of nation your main job is to maintain its existence.....so when your opponents/enemies make strategic moves (even if they are truly innocent & defensive in nature) the correct posture for long run survival (your ultimate core job responsibility as a leader of nation) is to assume rather that EVERYTHING is an offensive move. This idea, this existentialist idea is enshrined in the USA and many other nations in the very structure of their governance.....in democracies everything is up for debate & power dolled out to the house/senate/judiciary with all the checks and balances......there is one area where the President of the US retains almost unfettered control.....and that is in regards to military foreign policy.......see everybody gets it.....when it comes to the very survival of a nation.....there is very little space debate or consideration...look at the paranoia emerging around China in the US and its long-term threat to the USA.......the job of a nation is to be to paranoid.......Putin is paranoid.......Xi is paranoid.....Biden is paranoid......paranoid people dont think rationally.....therefore dont expect Putin to act rationally. I dont think this invasion was driven by rationailty or imperialism.....I think it was driven by existentialism & paranoia. NATO membership for Ukraine is therefore not a deal on the table that Putin will ever accept.

-

My comment about Ukraine running out of men before Russia was a combination of population AND casualty exchange ratio combined. Ukraine running out of men before Russia is just patently clear just based on the strategic aims of the two sides. Attrition ratio imbalance is patently clear based on the strategic posture/aims of the sides - dont forget Ukraine is trying to TAKE land, Russia is DEFENDING land.....the short hand military math for the casualty exchange ratio based on this posture alone is at best 2 to 1......more likely 3 to 1 in Russia's favors. It is the Ukranian men who are the end of the day going "over the top" and getting mowed down by entrenched Russian forces. Then on top of this you just layer on the clear male 16 - 65 population size advantage Russia has over Ukraine......sure lots of bodies being put through the meat grinder on both sides......but a proportionally higher percentage of Ukrainian males aged 16-65 are getting put through it everyday.

-

This is the math problem at the heart of the conflict. Ukraine runs out of men aged 16-65 before Russia does. Ukraine runs out of artillery, supplies & various weaponry before Russia does. & finally 'the West' runs out of perseverance & staying power before Russia does. If there was some kind of imperfect deal to be had in May 2022.......and Boris Johnson et al told Zelensky 'no dice' in a Churchill fever dream......then its really a terribly sad situation for every life lost on both sides since then.

-

Remind me of this from an Adam Curtis documentary I recommend folks check out - Hypernormalisation.....modern Russia is a bewildering mess of propaganda, fake news & psyops........all designed to ensure that people there are never really sure what is exactly happening & by whom...even the 'opposition'...it's designed to lead to civic paralysis which in and of itself is a form of power.......and based on the evidence of the last couple of decades its worked quite beautifully....as measured by civil disobedience that has ever seriously threatened the Putin regime in that time

-

Yep - the basic hard landing thesis didn’t go away it just got delayed this movie ends one way it’s only the running time that’s TBC….the US is running a deficit as if the GFC just happened yet unemployment is at a 60yr low….the bond market it seems is starting to think through the implications of that relative to issuance to come, structurally higher inflation and as a consequence is pushing up rates at the long end. Folks wanted the yield curve to on un-invert….it is….but not in the way that is positive for asset prices.

-

Agree - its destabilizing to let it go too far.......its implicitly understood I think at the Fed....and certainly by the Fed chair......4% inflation is another form of stealth wealth transfer......its a game I benefit from, holding hard assets financed with low rate fixed term debt.......but I always think of the situation something akin to how I think about companies......are they short term greedy or long term greedy.........short term greedy is sitting with a 3% mortgage on your hard asset base and smiling at 4% inflation knowing that your 'winning'......but what is winning if you de-stablize the whole system and end up with AOC or Marjorie Taylor Greene as president in five years time. Long term greedy or what I consider to be the optimal long term solution is what I think happens next.......Fed keeps pressuring financial conditions & remains resolute in the face of weakening......with true domestic disinflationary pressures in place.....corporates start to meaningfully give up margin that get translated into hopefully REAL gains in wages for median American worker. The US fiscal authorities start to get the budget under control by increasing taxes while reigning in and reforming dumb spending The lunatic fringe of the American right and the American left haven't come to prominence by accident.......a whole generation maybe two of median American workers have been left behind in terms of proportional participation in growing output of the US.....the wage data is clear on this.......the fact that each party in the USA is beginning to be hijacked by its lunatic fringe is a symptom of this......Jan 6th is a symptom of this.......and IMO it needs to change.......not because I'm some bleeding heart for 'poor' people.......but because its the best LONG term for my family's wealth & happiness accumulation to live in a country/society that isn't falling apart at the seams. Dont forget the simple maths......any number times ZERO is a ZERO......best way to not end up at ZERO is to not mess with a pathway that looks like its heading there

-

Is Europe becoming uninvestable?

changegonnacome replied to lnofeisone's topic in General Discussion

Europe isnt one 'place' - you invest in Italy you expose yourself to crazy italian politics......the short version of how I think about Europe is I want to own things in countries that are closer philosophically to the USA. Which is to say that they respect and champion something closer to free market enterprise. My shortlist of European countries I consider investable are: UK Netherlands Switzerland Ireland Luxemburg Germany These are in the main the 'centre right' countries in Europe....with some exceptions the rest of Europe is very much left or centre left......and prone to bananas economic policies at times where they can swing wildly left....the above on balance tend to default to free market solutions with minimal interference. -

This is one of my favourite thought experiments - for the bitcoin maxi maxis...who think that it might replace sovereign currency one day.......fine.....lets say it does.....we have ultra hard money (21m bitcoins), not controlled by a central authority.........and then a pandemic comes......the monetary largesse that occured in 2020/2021 stabilized a very difficult situation....it worked because it WAS centralized (Jay Powell/Jannet Yellen open the flood gates) and it worked to stablize things because it was FIAT money (we just printed more). There is not 'perfect' monetary system...always trade-offs in complex systems......the one we have is the least worst

-

Wall St pleasing capex underinvestment + ESG mafia have for sure created bottlenecks......and doubly so as @Spekulatius says bottlenecks in on/near/friend-shore locations

-

Good argument out there that due to Wall St.'s aversion for capex over time (see O&G) that lots industries that supply physical goods predominantly input goods acquiesced to shareholder demands & have systematically underinvested in capacity.......you know all the stats no new steel plants built in X years, refineries etc.