jfan

-

Posts

583 -

Joined

-

Last visited

-

Days Won

2

1 Follower

Recent Profile Visitors

4,796 profile views

jfan's Achievements

")

-

Just went back to some of Satoshi's emails (from the book of Satoshi). There was a couple pages on his thoughts of 51% attacks. "According to the "long tail" theory, the small, medium, and merely large farms (server) put together should add up to a lot more than the biggest zombie farm" My interpretation here is that it would be more profitable for these smaller farms that knowing they can't pull a 51% attack, would merely comply to the bitcoin protocol to be profitable, and that it was his thought that there would be many more small server farms choosing this rather than do some complicit like double spend. He further discusses that chain formation where different miners are forming various block templates (with transactions) that are occurring at the same time, where ultimately the proof-of-work (ie the longest chain), will be the valid chain, and all subsequent templates will be invalid. This process can take up to 1 hour to be immutable, but within that time transactions could be placed back into the mempool if they end up in the invalid chain. With the transaction fees in place, there should be always some miner out there willing to incorporate transaction requests, but the question than goes back to whether they have enough computational power to solve SHA-256 puzzle. It would be then dependent on the long-tail of honest nodes running the system having proportionally more compute. This in turn is dependent on whether these miners are incentivized by bitcoin block fees. It seems to me that the incentive to join these mining pools might weight more heavily on having a steady stream of income in fiat dollars rather than earning bitcoin itself. It is not clear to me why any larger mining company would ever join a pool, and why a very small miner would need one if their electricity costs are de minimis. But perhaps, there are many more small miners with just a few 100+ TH/s ASIC miners that can't afford the ability to host their own mining equipment using these pools, where their incentive to be profitable in fiat terms rather than bitcoin terms.

-

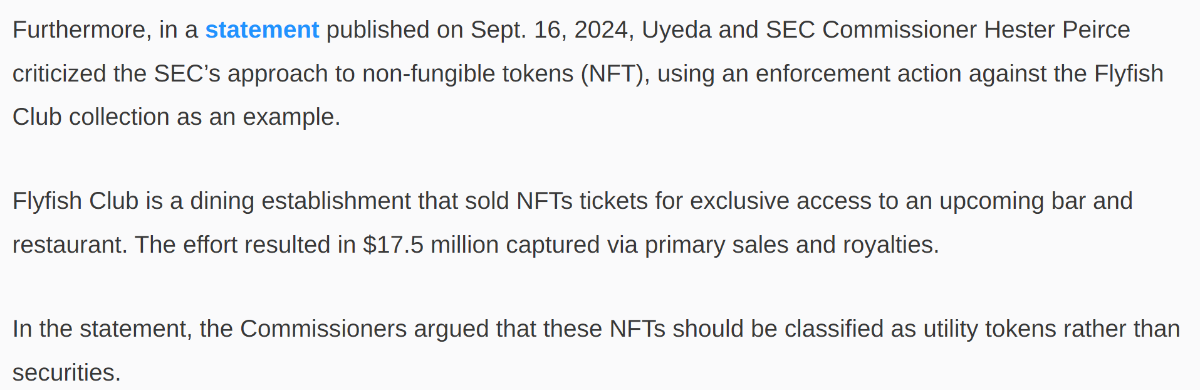

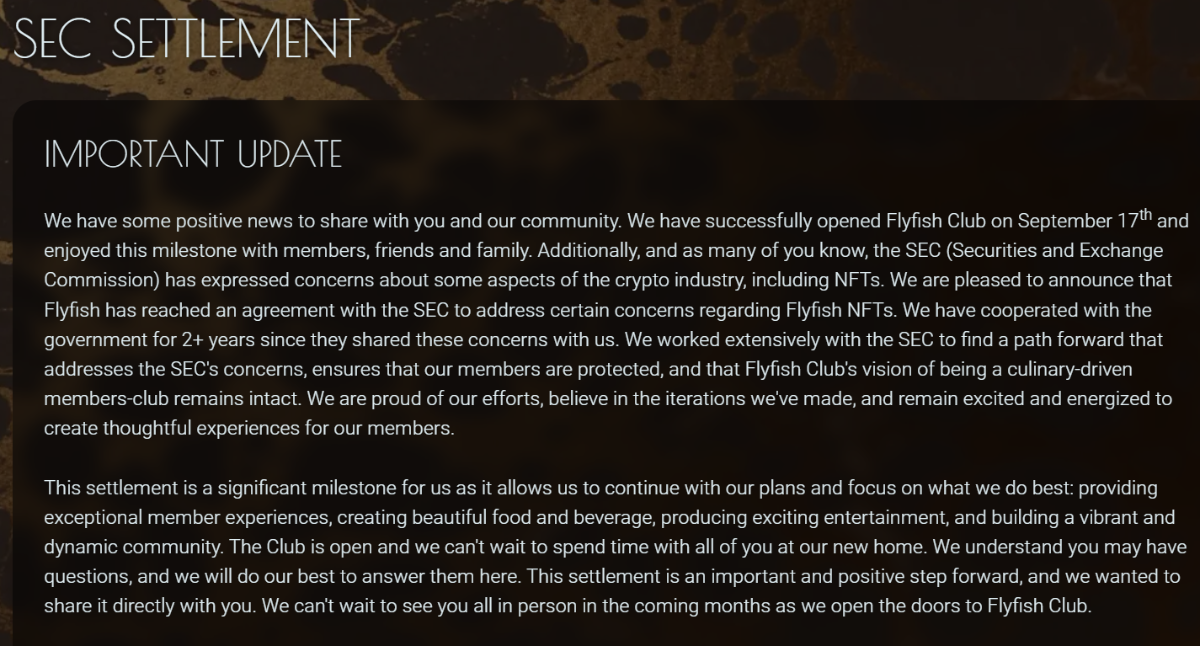

The Howey 4-part Test - Is it a security? (1946) 1) Is it an investment of money or assets? 2) Is the investment in a common enterprise? 3) Is there reasonable expectation of profit? 4) Is it reliant on the efforts of a promoter or others? I tend to agree that these tokens are more securities than "utility" tokens. 1) Joe public exchanges money for these tokens to get access to private Manhattan dining experience 2) There is a single enterprise involved - this is a bit grey, the more desirable the dining experience, the greater the restaurant's profit which suggests a scarcity in the supply for memberships, to which the token owner can lease out their membership to another for rent. 3) The ability to buy and sell tokens in a market place for the expectation for profit (assuming the demand for membership > supply of membership) or profit from leasing the token to another 4) It is reliant on the management team to create a desirable dinner (therefore profitable) experience. I'm pretty sure that FlyingFish probably took in the ICO proceeds and booked it as deferred revenues to avoid taxes (as in the case of booking these proceeds as current revenues) and avoid securities registration (ie booking the proceeds as equity). If there were a number of disparate restaurants with different owners participating in a network that issued tokens that people can use to buy-sell for a unique experience that restaurants could accept as payment, perhaps this system is more utility like than security. Below is the SEC settlement

-

You are absolutely right. Gensler's MIT course quoted ~ 1500 cryptotoken projects back in 2018. Only 1.5% of these projects actually had a working prototype network. >70% of them were just ideas that someone just published. Most of these stuff is junk and even if you create a popular coin, the originator, if they are holding a substantial number, can't offload without destroying the price. Certainly this is a reflection of people, their love of a narrative, their gambling nature, and tendency for people to cheat and fleeces others. These decentralized crypto-assets are a bit of a paradox. Decentralization and finality of data transfer among non-trusting parties face what Gensler terms it "collective action" problems ie how do you incentivize people who don't trust each other to jointly all use a network protocol that at the same time solves some cost issue (eg verification cost, governance cost, etc). Even permissioned blockchain projects such as the one the Australian Stock exchange was trying to get up and running failed and now facing legal action.

-

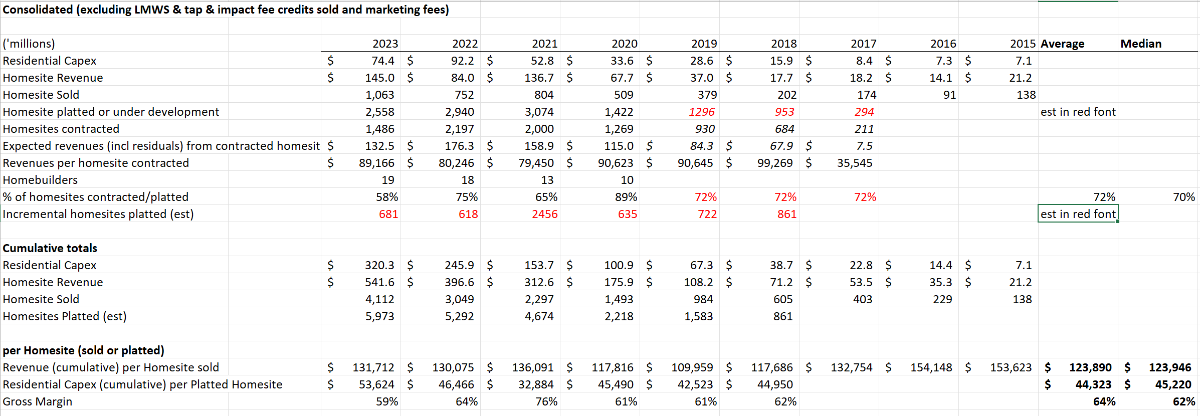

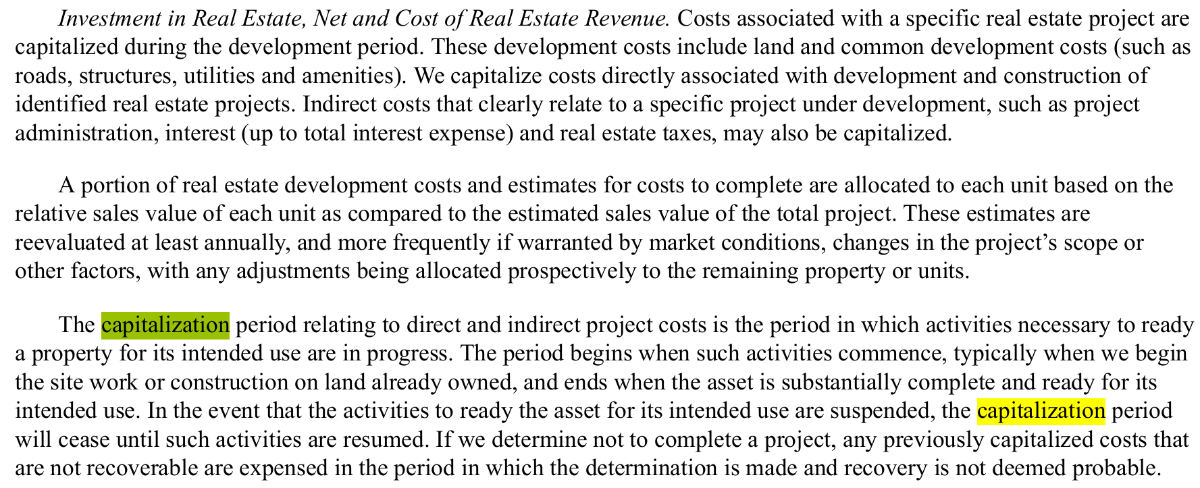

I went back to listen to the 2024 annual meeting and Marek was describing the 3 columns and the capital intensity (ie soft and hard dollars) at 44 minutes. He said that the majority of the capex spend occurred when the homesites move into platted/underdevelopment column. I assume the capex for homesites sold in 2024, probably occurred in 2021 to 2023 (? over a 3 year period) and that a larger portion is spent in the early years vs later on. They report total net residential capex each year since 2015 but not by individual community. Is the company willing to share with investors this granularity? @thepupil I'm not sure if this is the correct approach but in the footnotes, they describe capitalization of their real estate development expenditures (see below). This would smooth the numbers but may not reflect the actual cash expenditures. Since I don't have the community by community data, nor the exact timing or magnitude of the expenditures, I thought perhaps another way to look at this from an aggregate bird's eye view of the issue, is by looking at the cumulative totals over time and calculating the per unit revenues and capex with each passing year. My rough guess is that they moved ~ 6000 homesites through column 1 (platted/under development) since 2018. This is all backwards looking of course.

-

@TorontoChaosTheatre Francis has tremendously changed my families' lives. I have the utmost respect for him, his character, his values and his work ethic. He is not Buffett, Munger or Prem, but internalizes their wisdom to suit his own personal style. He is a gem. Being a mutual fund manager is challenging, always dependent on the fickleness of your fundholders and their lack of patience. I am truly glad that Francis has found a permanent capital vehicle to which he can do his thing. I know Francis is very private and humble but Wintaai has outperformed Fairfax and Berkshire by leaps and bounds over the past 4 years. I found it refreshing that he is doing this in private away from fickle fundholders, shareholders in a low cost manner. Is he infallible? No. But he doesn't carry himself to be all-knowing. This quality is very unvalued amongst money managers.

-

Contrast Gensler's interview with Coinbase's head of legal. It is extremely odd that a publicly traded for-profit business that relies on legitimacy from the government would be so audacious in such a public forum. I've been watching Gensler's MIT blockchain course and listening to John Brook's book the Go-Go Years (of the 1960s). Brook's description of the unscrupulous activities of brokers, stock exchange members, the stock exchange itself, the conglomerates undisciplined deal-making, leverage, mutual fund democratization for the uneducated investing public reminds me very much of this crypto space. This in contrast to the potential value that blockchain fundamentals could provide. This was recently posted. Haven't listened to the whole thing but seems useful.

-

-

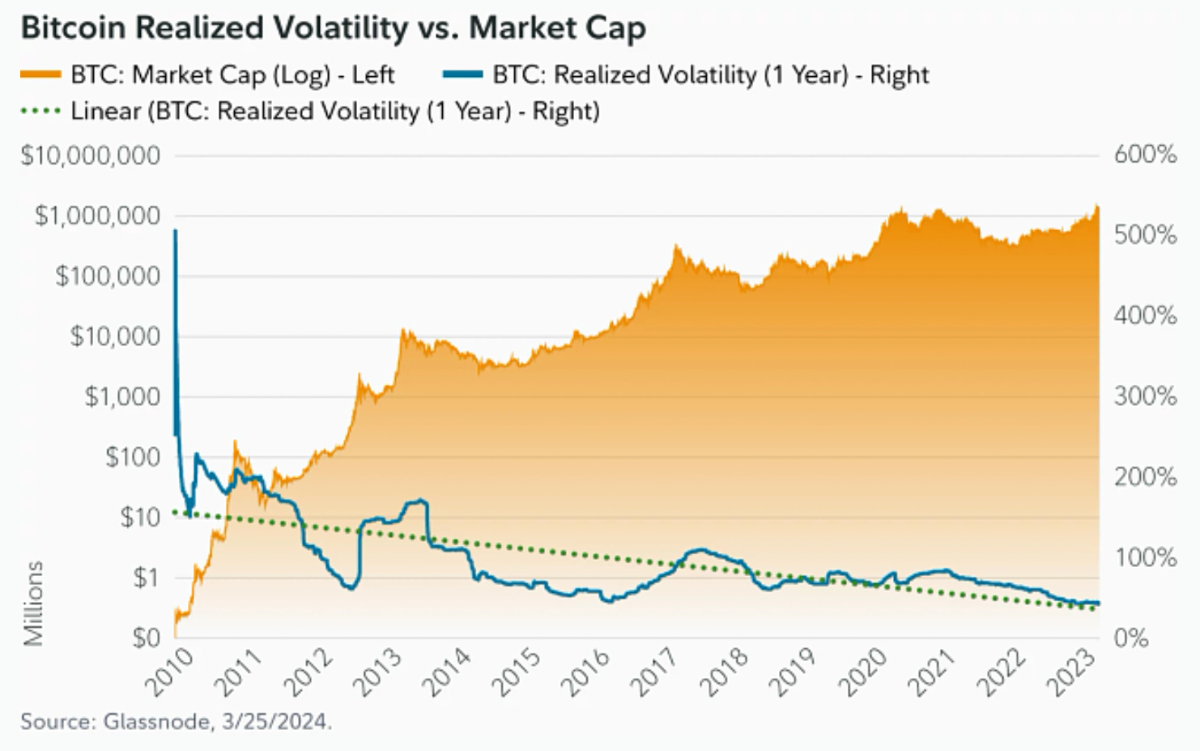

What was the Blocksize War? The Blocksize Wars Revisited: How Bitcoin’s Civil War Still Resonates Today Some reflections on the Bitcoin block size war 3 Links that review and summarize the blocksize war events, clues on bitcoin's governance and attitudes towards adopting new technological capabilities, and Vitalik's take on Bier and Ver's books on the blocksize wars. A Closer Look at Bitcoin’s Volatility The last link is a recent Fidelity write-up on bitcoin's volatility and its progression over time.

-

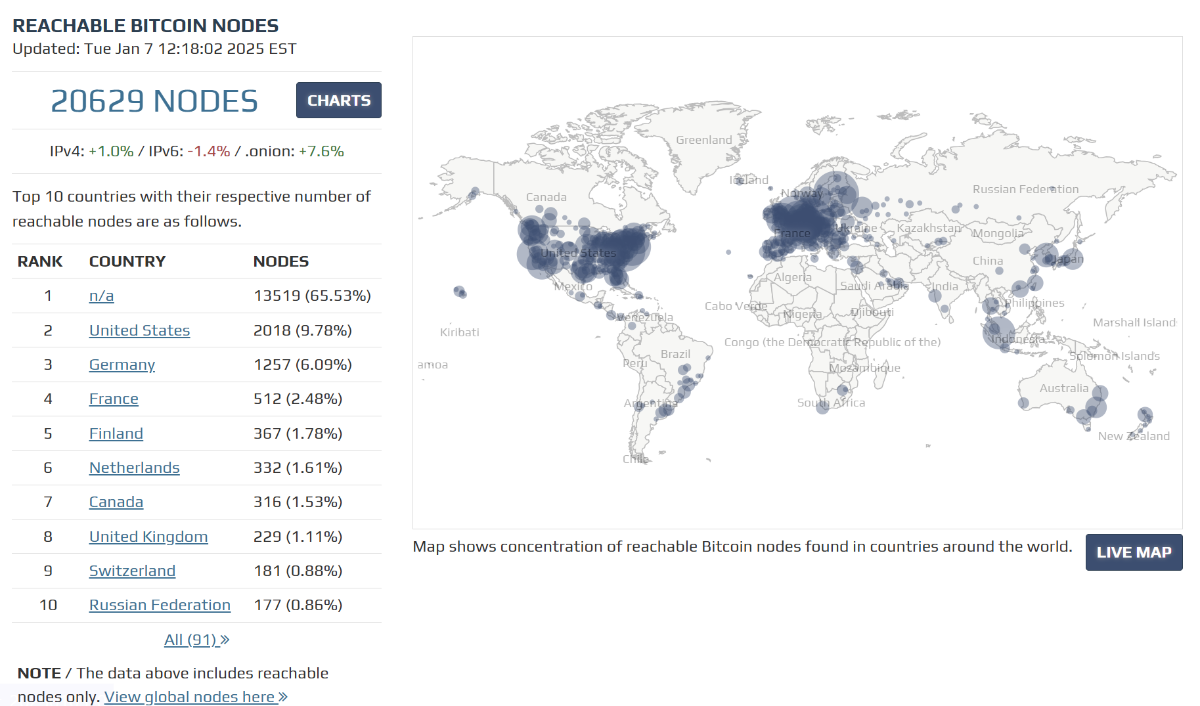

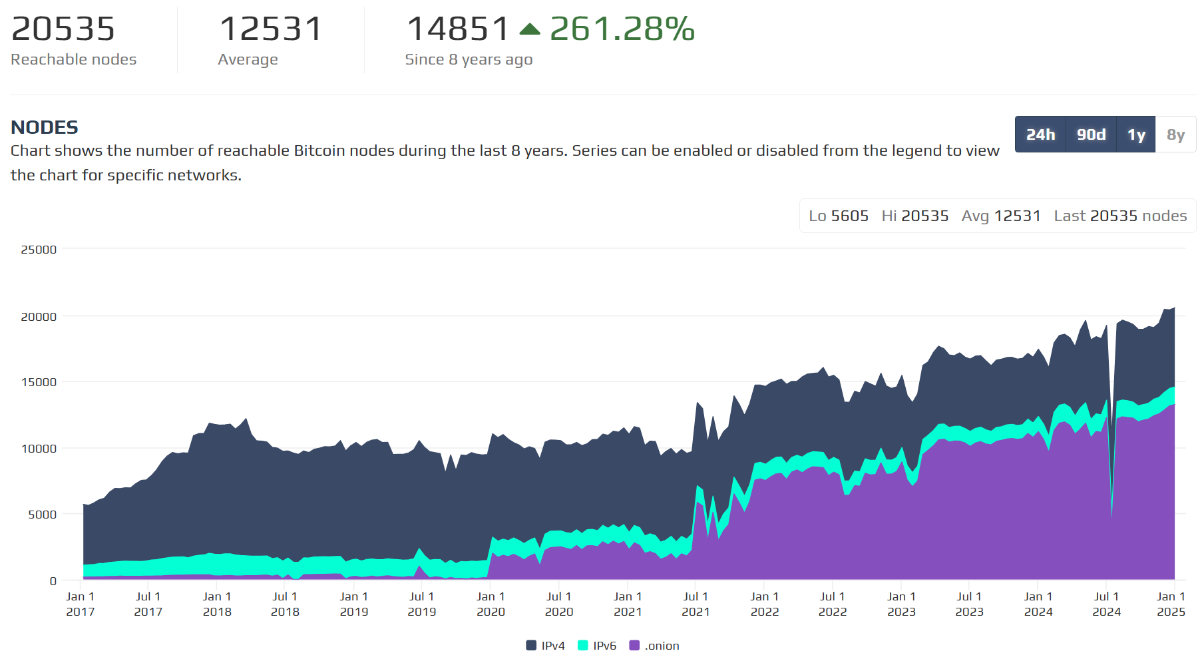

This website has a map (live and non-live) of reachable bitcoin nodes globally. Reachable Bitcoin Nodes - Bitnodes In 2018, there were 10,000 reachable bitcoin nodes to give some context. In terms of global reachable and unreachable nodes, today it is ~ 66,000. Over the past 90 days, there was a total of ~500K global reachable and unreachable nodes. Below is the number of reachable nodes over the past 8 years.

-

Are you referring to Murray Stahl specifically or the rest of the TPL board? Have you looked at prairiesky, it's a pure Canadian oil and gas royalty company (but no surface rights however)?

-

The crown jewel is the part ownership of helios the asset manager.

-

https://ocw.mit.edu/courses/15-s12-blockchain-and-money-fall-2018/video_galleries/video-lectures/ Gary Gensler's MIT blockchain course videos for those interested.

-

-

The Less-Efficient Market Hypothesis by Cliff Asness

jfan replied to Viking's topic in General Discussion

thanks for highlighting this article. I read this paper when it came out and coupled with Mike Green/David Einhorn's thoughts on this structure , have been thinking about where the puck is going in the next couple decades. I wonder if this is evolving into an age of conglomerates again. With small public businesses not getting any investor attention, it seems ripe for someone to consolidate them and control the cash flows in a private manner. Berkshire started this trend, and Fairfax is following, with increasing dollars allocated to private investments or take-private transactions. It is a bit of a conundrum wrt to the ease of accessing public investments at a low cost these days with more than plentiful information out there at our fingertips and the opportunity for decent future returns. The market structure seems to drive exponentially asset prices for those loved public equities and ignore everyone else. Coupled with the inherent laziness to actually do the work to understand what we are buying and owning, I feel people are just relying on the 1st order concept that "the market will return 7% indefinitely as they have in the past" which drives more market distortions. Investing is simple but not easy to do well. -

Can buying over-valued stocks be value investing?

jfan replied to jfan's topic in General Discussion

Curious, what did you try and why did you choose what you did?