nwoodman

-

Posts

1,105 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Posts posted by nwoodman

-

-

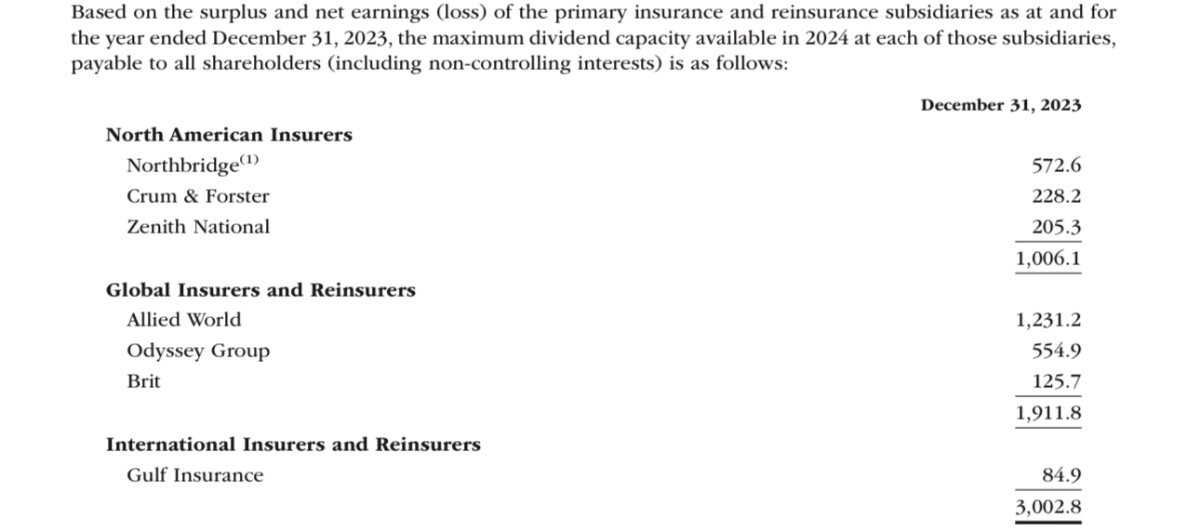

@Cigarbutt thanks for the heads up. On a sub level the RBC ratio is a lot lower than what I was calculating for the whole shooting match. It might be possible to calibrate using Note 19: Statutory Requirement, that Jen referred to as dividend capacity and assume that is based off an RBC ratio of 300%. Or perhaps it is as simple as seeing the total in Note 19 as the starting point in terms of the capital that could be reallocated as it is truly surplus if it can be dividended and the max is then some conservative multiple.

Will have a read and a think. The relevant section of Note 22: Financial Risk Management, you were referring to is reproduced from the AR below:

In the United States, the National Association of Insurance Commissioners ("NAIC") applies a model law and risk-based capital ("RBC") formula designed to help regulators identify property and casualty insurers that may be inadequately capitalized. Under the NAIC's requirements, an insurer must maintain total capital and surplus above a calculated threshold or face varying levels of regulatory action. The threshold is based on a formula that attempts to quantify the risk of a company's insurance and reinsurance, investment and other business activities. At December 31, 2023 Odyssey Group, Crum & Forster, Zenith National, Allied World and U.S. Run-off subsidiaries had capital and surplus that met or exceeded the regulatory minimum requirement of two times the authorized control level; each subsidiary had capital and surplus of at least 3.2 times (December 31, 2022 - 3.0 times) the authorized control level, except for TIG Insurance which had at least 2.0 times (December 31, 2022 - 2.0 times).

In Bermuda, insurance and reinsurance companies are regulated by the Bermuda Monetary Authority and are subject to the statutory requirements of the Bermuda Insurance Act 1978. There is a requirement to hold available statutory economic capital and surplus equal to or in excess of an enhanced capital and target capital level as determined under the Bermuda Solvency Capital Requirement model. The target capital level is measured as 120% of the enhanced capital requirements. At December 31, 2023 and 2022 Allied World's subsidiary was in compliance with Bermuda's regulatory requirements.

In Canada, property and casualty companies are regulated by the Office of the Superintendent of Financial Institutions on the basis of a minimum supervisory target of 150% of a minimum capital test ("MCT") formula. At December 31, 2023 Northbridge's subsidiaries had a weighted average MCT ratio of 255% (December 31, 2022 - 241% of the minimum supervisory target.

Brit is subject to the solvency and regulatory capital requirements of the Prudential Regulatory Authority in the

U.K. for its Lloyd's business and the Bermuda Monetary Authority for its Bermudan business. The management capital requirements for Brit are set using an internal model based on the prevailing regulatory framework in these jurisdictions. At December 31, 2023 Brit's total capital consisted of net tangible assets (total assets less any intangible assets and all liabilities), subordinated debt and contingent funding from its revolving credit facility and amounted to $2,545.7 (December 31, 2022 - $2,052.7). This represented a surplus of $1,050.4 (December 31, 2022 - $709.5) over Brit's management capital requirements.

Gulf Insurance is governed by the local capital adequacy regulations issued by the Insurance Regulatory Unit

("IRU") in the State of Kuwait. At December 31, 2023 Gulf Insurance had Regulatory Solvency Capital of 998% of the minimum capital required.

In countries other than the U.S., Bermuda, Canada, the U.K. and Kuwait where the company operates, the company met or exceeded the applicable regulatory capital requirements at December 31, 2023 and 2022.

-

2 hours ago, SafetyinNumbers said:

I was the “analyst” and was just throwing a number out there with hopes they would correct me with the right number! I appreciate though that’s probably not a number they want us to know as it could lead to a lot of second guessing if they aren’t as aggressive as they could be if an opportunity does present itself. I do think it’s important for investors to think about as it’s more right tail optionality that markets are ignoring and is another reason for multiple expansion.All good, it was definitely worth a try

. After thinking about it today I am not sure why it is such a secret. It strikes me anyone in the business probably has access to the weightings so could run the numbers on each other. There obviously comes a time though where you need to do a little convincing of the regulators about the “true” risk weightings and perhaps that is where things get a little more complicated and hence privacy is key..

. After thinking about it today I am not sure why it is such a secret. It strikes me anyone in the business probably has access to the weightings so could run the numbers on each other. There obviously comes a time though where you need to do a little convincing of the regulators about the “true” risk weightings and perhaps that is where things get a little more complicated and hence privacy is key..

The exercise at least gave me some insight into the process and a range of capacity. My conclusion, and I think we all knew it anyway, is that IDBI at $7-8bn is a stretch even for Fairfax (let alone FIH) and they will need to pull in some partners. Even if it turns out to be ~60% its is still a lot (30% government 30% Life Insurance Corporation)

Can they grow into it in 2-3 years, at a 60% stake of $4-5bn, I think very easily. Is it the wrong time/price to do it? Not sure, but a lot easier to digest now than 2 years ago. If they can get a deferred or staggered settlement (free option) then it looks even better.

All speculation of course, but as usual they appear to have been skating towards the puck in terms of their balance sheet. If not IDBI, then the number you intuitively threw out there for equities in general, iwas decent guesstimate based on my fumblings

-

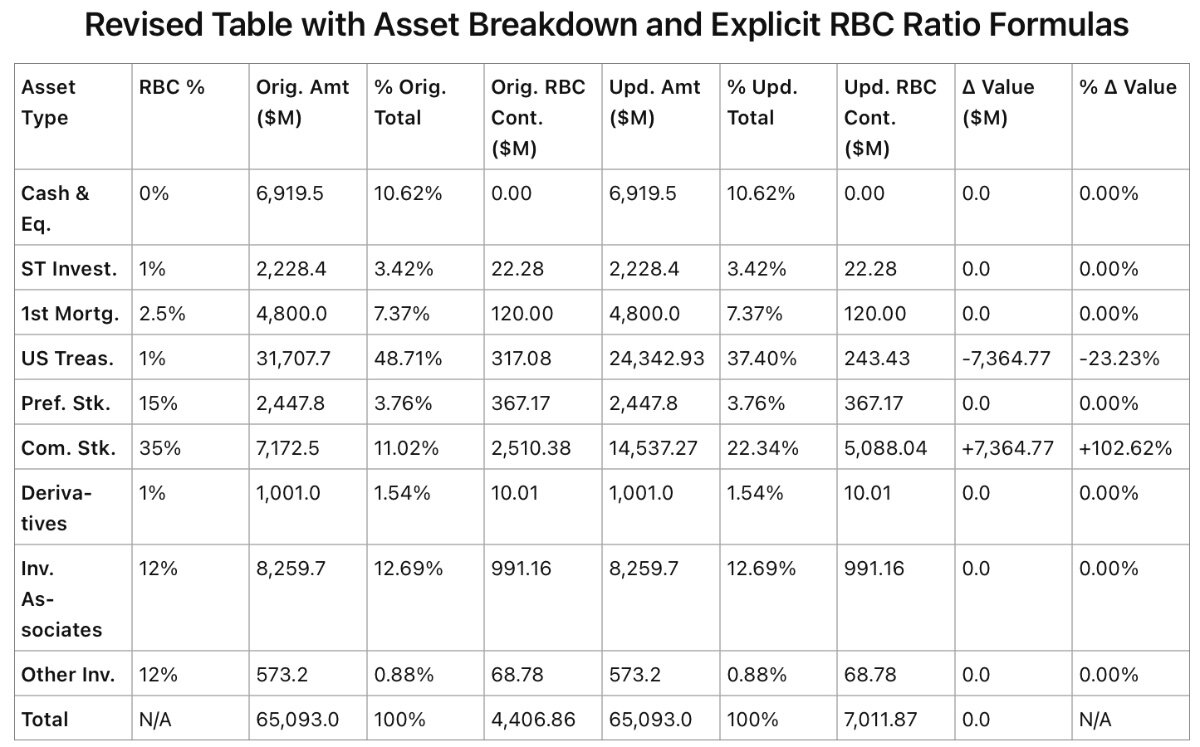

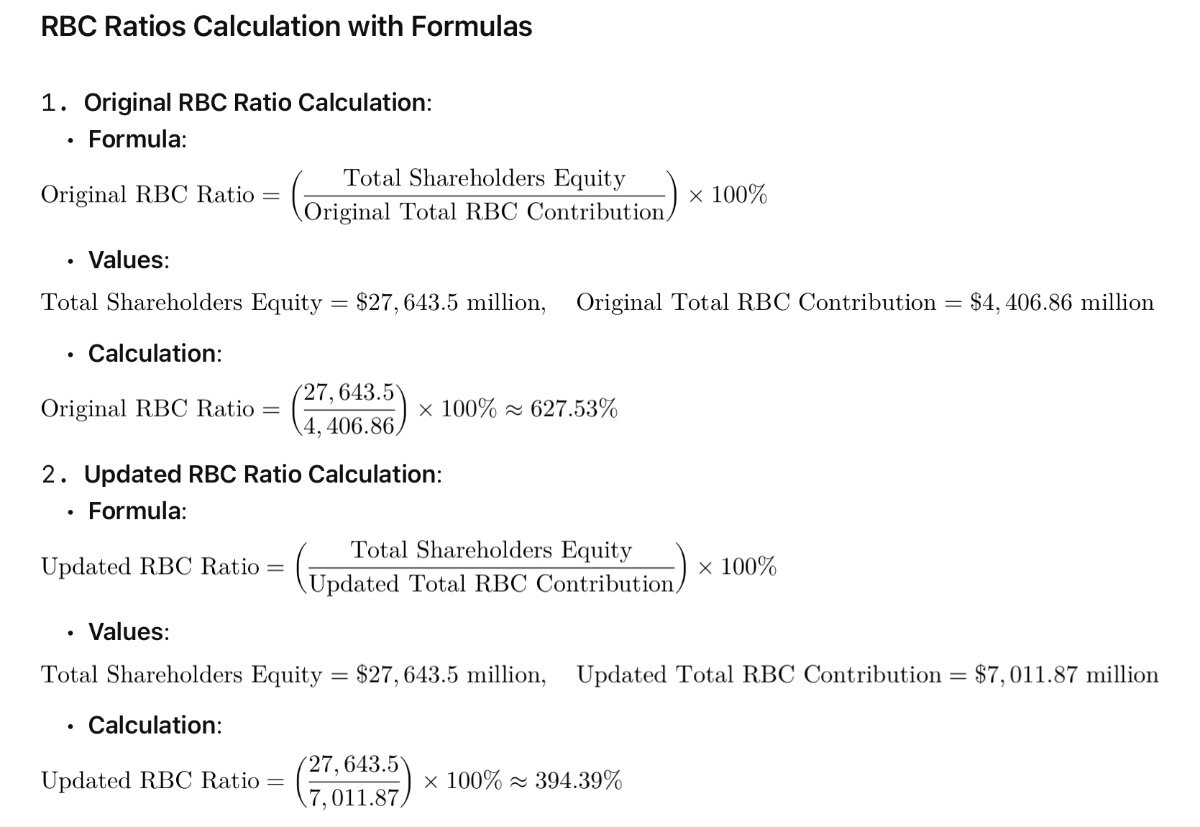

laws of diminishing returns but I took one last look at this from an RBC perspective. I split bonds into first mortgages and treasuries based on the CC.

The RBC weightings are important and I simply don’t have a way of checking them. Assuming the following I get a very healthy RBC ratio of 627% currently and if I run that down to a still conservative 400% then I get an answer of $7.4bn that could go from treasuries to equities. I think the answer lies somewhere in that range $2bn-$7bn. So perhaps the analyst is roughly right at $4bn. The reason I am also interested is Fairfax’s capacity to fund some or all of IDBI if that comes to pass.

Thanks for your help

-

@Cigarbutt, thanks again. This is a quick follow up in relation to a question that was posed in the Q1 24 Conference call regarding the potential to rotate into equities from the fixed income portfolio during a market sell off.

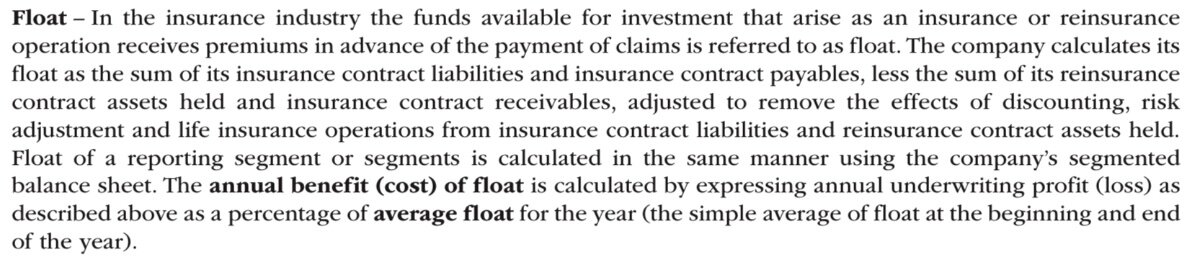

Running the numbers again based on Fairfax’s definition of float as provided in the annual, agree with you ratio of around 1.3 as follows:

Your CalcStep 1: Calculate the approximate insurance float

Insurance contract liabilities (Note 8): $45,918.1 million

Insurance contract payables: $1,065.0 million

Reinsurance contract assets held (Note 9): $10,808.6 million

Insurance contract receivables: $811.0 millionFloat = Insurance contract liabilities + Insurance contract payables - Reinsurance contract assets held - Insurance contract receivables

= $45,918.1 + $1,065.0 - $10,808.6 - $811.0

= $35,363.5 millionStep 2: Calculate the total cash and fixed income portfolio

Holding company cash and investments:

Holding company cash and investments (including assets pledged for derivative obligations): $2,496.4 millionPortfolio investments:

Subsidiary cash and short term investments: $7,801.6 million

Bonds: $36,131.2 million

Subtotal: $43,932.8 millionAssets pledged for derivative obligations:

Bonds: $115.5 million

Total cash and fixed income portfolio = Holding company cash and investments + Portfolio cash and fixed income investments + Assets pledged for derivative obligations (Bonds)

= $2,496.4 + $43,932.8 + $115.5

= $46,544.7 millionStep 3: Calculate the ratio of cash and fixed income portfolio over insurance float

Ratio = Total cash and fixed income portfolio / Insurance float

= $46,544.7 / $35,363.5

= 1.32Based on the information provided in Fairfax's Q1 2024 interim consolidated financial statements, the company's cash and fixed income portfolio is approximately 1.32 times its insurance float. However, as mentioned earlier, the float calculation is subject to adjustments for discounting, risk adjustment, and life insurance operations, which are not provided in the interim financial statements. As a result, the actual ratio may differ from this approximation.

At least I agree with your starting number of 1.3, thanks

MCT Approach with lots of assumptions (I think this might be flawed too)Ran the numbers in Chat GPT and end up with $3.6 bn realllcation based on MCT. The asset weightings and hence MCT ratios were completely different to Claude. So unfortunately it is numberwang. Not to mention we have two approaches MCT and RBC.

FWIW based on RBC it looks like this and solving for an RBC ratio of 300% (320% currently) gives you the following table:

Conservative RBC Ratio Standards:

- Very Strong: 400% and above. This level is often seen as very conservative, providing a substantial cushion against potential losses.

- Strong: 300% to 399%. This is still considered a robust conservative level, offering good financial stability and less risk of breaching lower thresholds under normal market conditions.

The National Association of Insurance Commissioners (NAIC) in the U.S., which introduced the RBC system, sets various action levels based on the RBC ratio. Here’s a general overview of these levels:

1. Company Action Level: When the RBC ratio falls to 200% of the required minimum, the company must submit a comprehensive financial plan outlining how it will improve its capital situation.

2. Regulatory Action Level: If the ratio falls to 150% of the required minimum, state regulators may intervene more directly, possibly requiring changes in operations or financial restructuring.

3. Authorized Control Level: At 100% of the required minimum, regulators may assume control of the insurer to protect policyholders and creditors.

4. Mandatory Control Level: If the RBC ratio falls below 70% of the required minimum, regulators are typically mandated to take over the insurer

The Risk-Based Capital (RBC) and Minimum Capital Test (MCT) are both regulatory standards used to ensure that insurance companies maintain adequate capital to support their risks, but they differ in their scope, methodology, and geographical usage. Here’s a detailed comparison:

Geographical Usage

- RBC: Primarily used in the United States, established by the National Association of Insurance Commissioners (NAIC).

- MCT: Used in Canada, specifically designed for Canadian insurance companies.Purpose and Scope

- RBC: Designed to establish minimum required capital for insurance companies to support their overall business operations while covering various risks, such as underwriting, credit, market, and operational risks. RBC aims to provide a buffer against insolvency by requiring higher capital for higher risks.

- MCT: Similar to RBC, MCT measures the sufficiency of an insurance company's capital, focusing on its ability to withstand financial instability or claims. It also looks at various risks but is tailored to the specific regulatory environment in Canada.

Methodology

- RBC: Uses a formula-based approach where different risk elements (C1 through C4) are quantified:

- C1 (Asset Risk): Reflects the risk of default and changes in market values of assets.

- C2 (Insurance Risk): Covers risks associated with underwriting liabilities and pricing.

- C3 (Interest Rate and Market Risk): Addresses the potential for asset and liability mismatches due to changes in market conditions.

- C4 (Business and Operational Risk): Concerns with business operations and management risks.

- MCT: Also formula-based, MCT quantifies assets, liabilities, and off-balance-sheet exposures, assigning them into various categories with corresponding risk factors. The calculation considers:

- Assets Quality: Different assets are assigned risk weights based on their likelihood of loss or impairment.

- Liabilities: Liabilities are evaluated for their potential impact on capital, including insurance liabilities and operational liabilities.

Calculation Outputs

- RBC: Produces a capital ratio that insurers must meet or exceed, which is set by regulatory authorities. Insurers are required to take corrective action if their RBC falls below the mandatory threshold.

- MCT: Produces a similar ratio, the MCT ratio, which indicates the capital adequacy relative to the risks the insurer holds. A threshold is set, and if an insurer’s MCT ratio falls below this, they must increase their capital or reduce their risk.

Regulatory Actions

- RBC: If an insurer’s RBC ratio falls below regulatory thresholds, a range of actions can be triggered, from requiring a comprehensive business plan to direct regulatory intervention.

- MCT: Similarly, falling below the MCT ratio can lead to enhanced regulatory supervision and may require the insurer to submit plans on how they will improve their capital position.

Adjustments and Sensitivity

- RBC: Highly sensitive to changes in asset values and risk profiles, requiring frequent updates and recalculations.

- MCT: Also requires updates based on changes in the company's financial condition and market dynamics, but may differ in how sensitivities are treated under Canadian regulations.

Both systems aim to protect policyholders and ensure market stability by preventing insurance company failures, but they do so through region-specific frameworks that reflect local market conditions, regulatory environments, and insurance practices.

-

@Cigarbutt thanks for the handholding appreciate it. I will post a reply to a separate thread in order not to clutter up this thread further

https://thecobf.com/forum/topic/20743-market-sell-off-equity-reallocation/

-

Thanks @Cigarbutt

That was very helpful to kickstart my thinking. Ultimately the management at FFH has their arms fully around this. However it prompted me to give your numbers a revisit and also do some quick and dirty numbers of my own

Key point

Statutory requirements for insurance companies typically include risk-based capital (RBC) ratios, which measure an insurer's capital adequacy relative to its risk profile. In the United States, the National Association of Insurance Commissioners (NAIC) recommends a minimum RBC ratio of 200%. In Canada, the Office of the Superintendent of Financial Institutions (OSFI) requires a minimum Minimum Capital Test (MCT) ratio of 150%.

Assuming Fairfax maintains a conservative RBC ratio well above the minimum requirements (e.g., 300% or higher), the company might have some flexibility to reallocate a portion of its bond portfolio to equities during a market sell-off. However, the exact amount would depend on various factors, such as:

- The overall capital position and RBC ratios of Fairfax's insurance subsidiaries

- The liquidity and credit quality of the bond portfolio

- The expected impact of the reallocation on the company's risk profile and capital adequacy

- Regulatory restrictions and approval from the relevant insurance regulators

Rerunning your numbers - we must be calculating different things

Using the ratio of the company's cash and fixed income float portfolio over its insurance float reserves as a proxy for the Minimum Capital Test (MCT) ratio is an interesting approach, but it has some limitations and may not provide a fully accurate representation of the company's capital adequacy.

The insurance float represents the funds generated by insurance operations that an insurer can invest until claims are paid out. Fairfax's float primarily consists of the following components:

- Insurance contract liabilities: $45,918.1 million as of March 31, 2024

- Insurance contract payables: $1,065.0 million as of March 31, 2024

The cash and fixed income float portfolio includes:

- Holding company cash and investments: $2,496.4 million as of March 31, 2024

- Subsidiary cash and short-term investments: $7,801.6 million as of March 31, 2024

- Bonds: $36,131.2 million as of March 31, 2024

Calculating the ratio:

(Cash and Fixed Income Float Portfolio) / (Insurance Float Reserves) = ($2,496.4 million + $7,801.6 million + $36,131.2 million) / ($45,918.1 million + $1,065.0 million) = $46,429.2 million / $46,983.1 million = 0.99

This ratio of 0.99 suggests that Fairfax's cash and fixed income float portfolio is nearly sufficient to cover its insurance float reserves. However, it's important to note that this ratio does not fully capture the company's capital adequacy for several reasons:

- It does not consider other types of investments, such as preferred stocks, common stocks, and investments in associates, which may also be used to support insurance liabilities.

- It does not account for the risk characteristics of the assets and liabilities, which are a key component of the MCT ratio calculation.

- It does not include other components of the MCT ratio, such as available capital, surplus allowance, and eligible deposits.

- It does not reflect the specific regulatory requirements and risk factors used in the MCT ratio calculation.

While this ratio provides a simplified view of Fairfax's ability to cover its insurance float reserves with liquid assets, it should not be considered a substitute for the more comprehensive MCT ratio. The MCT ratio is a risk-based capital adequacy measure that considers a wider range of factors and is specifically designed for property and casualty insurance companies in Canada.

In summary, while the ratio of cash and fixed income float portfolio over insurance float reserves can provide some insight into Fairfax's liquidity and ability to cover its insurance liabilities, it is not a perfect proxy for the MCT ratio, which is a more comprehensive and risk-based measure of capital adequacy.

Taking a stab at MCT

I take it MCT and RBC are actually confidential. Makes sense you don’t want to be giving your opposition a leg up in terms of capacity to write.

However upper level (and treat the numbers with contempt)

To calculate Fairfax's Minimum Capital Test (MCT) ratio based on the asset classes detailed in the Q1 2024 report, we will make assumptions about the risk factors associated with each asset class. Please note that these assumptions are for illustrative purposes only and may not reflect the actual risk factors used by Fairfax or its regulators.

Assumptions:

- Available Capital: We will assume that Fairfax's available capital is approximately 70% of its total equity.

- Minimum Capital Required (Risk Factors): a. Cash and cash equivalents: 0% risk factor b. Short-term investments: 1% risk factor c. Bonds: 3% risk factor (assuming a mix of high-quality government and corporate bonds) d. Preferred stocks: 15% risk factor e. Common stocks: 20% risk factor f. Investments in associates: 30% risk factor (assuming illiquid investments) g. Derivatives and other invested assets: 10% risk factor h. Insurance risk: 20% of net premiums written

Calculation:

Step 1: Estimate Available Capital Total Equity as of March 31, 2024: $27,643.5 million Assumed Available Capital = 70% × $27,643.5 million = $19,350.5 million

Step 2: Estimate Minimum Capital Required

a. Cash and cash equivalents: $7,023.2 million × 0% = $0 million

b. Short-term investments: $2,266.0 million × 1% = $22.7 million

c. Bonds: $36,722.3 million × 3% = $1,101.7 million

d. Preferred stocks: $2,447.8 million × 15% = $367.2 million

e. Common stocks: $7,172.5 million × 20% = $1,434.5 million

f. Investments in associates: $6,833.6 million × 30% = $2,050.1 million

g. Derivatives and other invested assets: $1,574.2 million × 10% = $157.4 million

Total Minimum Capital Required for Assets = $0 + $22.7 + $1,101.7 + $367.2 + $1,434.5 + $2,050.1 + $157.4

Total Minimum Capital Required for Assets = $5,133.6 million

h. Insurance risk:

Net premiums written (Q1 2024): $6,249.3 million

Annualized net premiums written = $6,249.3 million × 4 = $24,997.2 million

Risk factor for insurance risk: 20%

Minimum Capital Required for Insurance Risk = 20% × $24,997.2 million = $4,999.4 million

Total Minimum Capital Required = $5,133.6 million + $4,999.4 million = $10,133.0 million

Step 3: Calculate the MCT Ratio

MCT Ratio = (Available Capital) / (Minimum Capital Required)

MCT Ratio = $19,350.5 million / $10,133.0 million MCT Ratio = 1.91 or 191%

Based on the asset classes detailed in the Q1 2024 report and the assumed risk factors, Fairfax's estimated MCT ratio would be approximately 191%. This suggests that the company would have sufficient available capital to cover the assumed risk exposures associated with its investments and insurance operations.

However, it's crucial to reiterate that this calculation is based on illustrative risk factors and limited information from the Q1 2024 report. The actual risk factors used in the MCT calculation would be determined by the regulatory guidelines and the specific characteristics of Fairfax's assets and liabilities. Additionally, the MCT ratio is a comprehensive measure that considers various other risk factors, such as interest rate risk, foreign exchange risk, and operational risk, which are not captured in this simplified calculation.

In summary, while this calculation provides a more granular estimate of Fairfax's MCT ratio based on the asset classes reported in the Q1 2024 report, it remains an illustrative example based on assumed risk factors. The actual MCT ratio would need to be determined using the specific regulatory guidelines and a more comprehensive risk assessment of Fairfax's operations.

Equity Reweighting

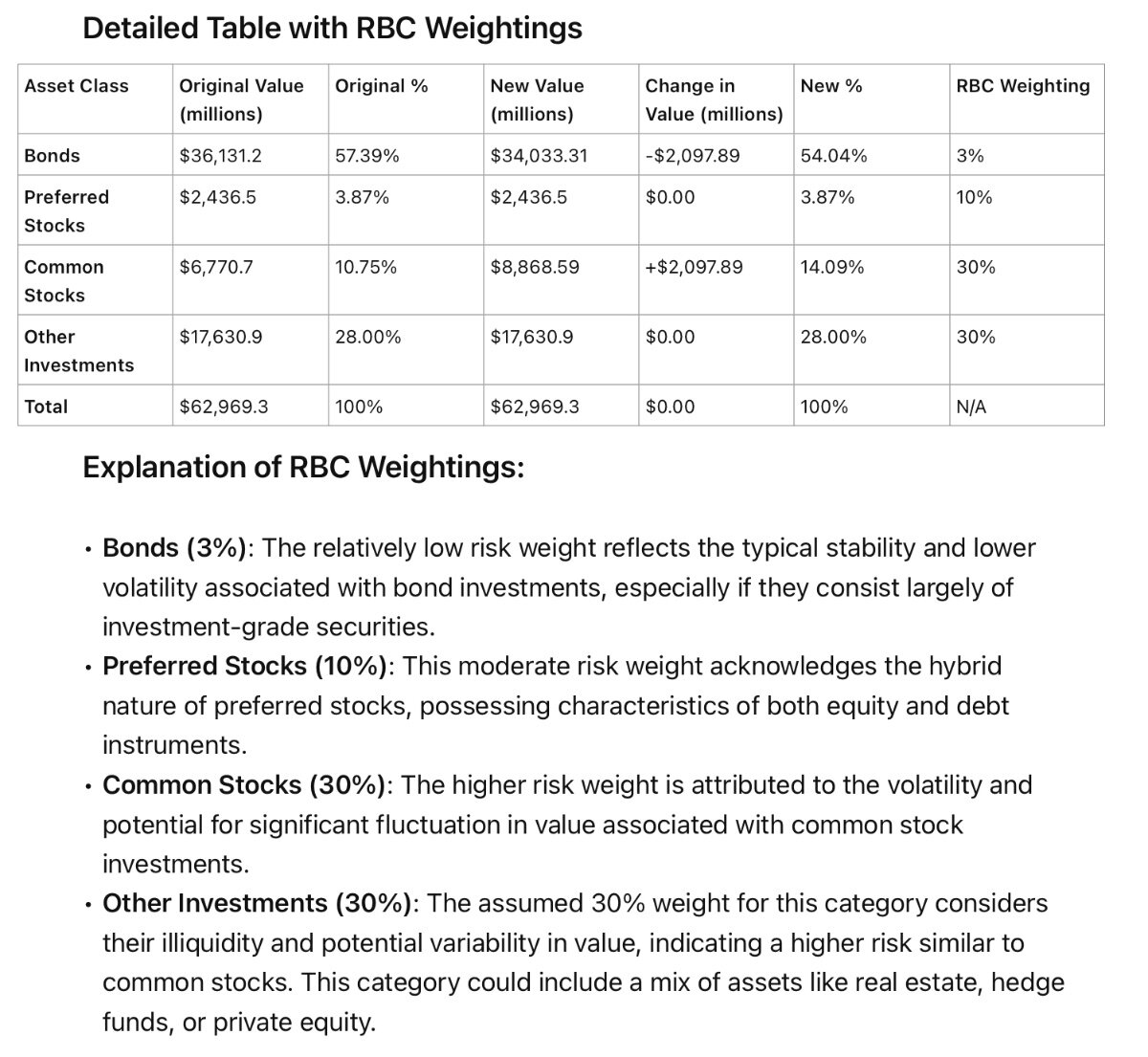

To determine how much could be reallocated from bonds to equities while maintaining a conservative approach, we will target an MCT ratio of 200%, which is comfortably above the regulatory minimum of 150%. We will also assume that the risk factors for the other asset classes and insurance risk remain constant.

Given:

- Current MCT ratio: 191%

- Target MCT ratio: 200%

- Current bond allocation: $36,722.3 million

- Risk factor for bonds: 3%

- Risk factor for equities: 20%

Step 1: Determine the excess available capital at the target MCT ratio

Target Minimum Capital Required = (Available Capital) / (Target MCT Ratio)

Target Minimum Capital Required = $19,350.5 million / 2.00 Target Minimum Capital Required = $9,675.3 million

Excess Available Capital = (Current Minimum Capital Required) - (Target Minimum Capital Required) Excess Available Capital = $10,133.0 million - $9,675.3 million Excess Available Capital = $457.7 million

Step 2: Calculate the amount that can be reallocated from bonds to equities

Reallocation Amount = (Excess Available Capital) / (Difference in Risk Factors)

Difference in Risk Factors = Equity Risk Factor - Bond Risk Factor

Difference in Risk Factors = 20% - 3% = 17%

Reallocation Amount = $457.7 million / 0.17 Reallocation Amount = $2,692.4 million

Therefore, based on the assumptions and the target MCT ratio of 200%, Fairfax could reallocate approximately $2,692.4 million from bonds to equities while maintaining a conservative capital position.

After reallocation:

- Bond allocation: $36,722.3 million - $2,692.4 million = $34,029.9 million

- Equity allocation: $7,172.5 million + $2,692.4 million = $9,864.9 million

It's essential to note that this calculation assumes that the reallocation would not impact the other risk factors or the available capital. In practice, any significant changes to the investment portfolio would need to be carefully analyzed to assess their impact on the company's overall risk profile and capital adequacy.

Furthermore, it's crucial to consider that this reallocation is based on a static view of the MCT ratio and does not account for potential changes in market conditions, asset valuations, or insurance risks over time. Any reallocation decisions would need to be made in the context of Fairfax's long-term investment strategy, risk appetite, and regulatory requirements.

In summary, based on the conservative target MCT ratio of 200% and the assumed risk factors, Fairfax could potentially reallocate approximately $2,692.4 million from bonds to equities. However, this calculation is for illustrative purposes only and does not consider the dynamic nature of capital adequacy or the specific factors that may influence Fairfax's investment decisions.

Final Take

So after all that and probably too many assumptions, and no doubt some AI hallucinations, the answer is 2.7 bn. i.e not much and below the $4bn the questioner suggested.

-

I thought Buffett’s comments on the weekend in regards to India were interesting. Not necessarily a validation of the Indian thesis for Fairfax but worth reposting

During the shareholder meeting, there was a question related to India and Berkshire's perspective on investing there. Here are the relevant quotes from Warren Buffett's response:

"Well, that's a very good question. And obviously India, you know, I'm sure there are loads of opportunities in a place like India. And the question is, do we have any advantage in either insights into those businesses or contexts, it will make possible some transaction that might what the parties in India would particularly want us to participate."

Buffett acknowledged the potential opportunities in India but questioned whether Berkshire has a distinct advantage in terms of insights or context to pursue those investments effectively. He continued:

"I would say that that's something that a more energetic management at Berkshire could pursue, because we do have the reputation. Now, Berkshire is known, not like it's known in the United States, but it's known around the world. And, you know, our japanese experience has been fascinating in that respect. So there may be an unexplored or unattended to opportunity in that area. I'm not the one to do it, but that may be something that in the future, it might be opportunities."

Buffett suggested that future Berkshire management could potentially explore opportunities in India more actively, leveraging Berkshire's global reputation. He drew a parallel to their successful experience investing in Japan. However, he stated that he himself is not the one to pursue it.

"There are opportunities. The question is, does Berkshire have some kind of advantage in actually pursuing those opportunities against, particularly against people that are using other people's money, that where they get paid based on asset met, on assets managed or something of this sort."

Buffett reiterated that while opportunities exist, Berkshire would need to have a clear competitive advantage compared to other investors, especially those who are more focused on simply gathering assets under management rather than long-term business fundamentals.

All very Buffett-like but reiterated to me the Indian connections that Fairfax have developed over the last 10-20 years are valuable indeed.

-

24 minutes ago, UK said:

https://steadycompounding.com/investing/brk-2024/

Re cash and market opportunities:

We will have Apple as our largest investment, but I don’t mind at all, under current conditions, building the cash position. I think when I look at the alternative of what’s available, the equity markets, and I look at the composition of what’s going on in the world, we find it quite attractive.

...

But if we had 10 billion, I wouldn’t basically see many more opportunities than we found now. It’s true that something like Japan, we could have done, if the company had had a 30 or 40 billion, and we’d make. We’d have had great returns on equity. But if I saw one of those now, I’d do it for Berkshire. It isn’t like I’ve got a hunger strike or something like that going on.Thanks for the transcript link

-

Finally found some time to run some summaries for FIH

Overview

Here are the key points from Fairfax India's Q1 2024 interim report:

Financial Performance:

- Net loss of $293.2 million in Q1 2024 compared to net loss of $51.6 million in Q1 2023. The increase in net loss was primarily due to higher unrealized losses on investments.

- Book value per share decreased by 10.1% from $21.85 at December 31, 2023 to $19.65 at March 31, 2024.Investment Activity:

- During Q1 2024, the company completed the sale of 70.1% of its equity interest in NSE for proceeds of $132.3 million, resulting in realized gains of $117.1 million. The remaining NSE shares were sold in April 2024.

- Net change in unrealized losses on investments of $410.9 million, driven mainly by market price declines of Public Indian Investments.2. Key Events:

- On March 4, 2024, IIFL Finance was ordered by the RBI to cease gold loan origination due to supervisory concerns, resulting in a 43% decline in IIFL Finance's share price in Q1.

- Subsequent to quarter-end, Fairfax India agreed to participate in IIFL Finance's rights issue and provide liquidity support along with Fairfax if needed.3.Valuation Impact:

- The fair values of Fairfax India's Private Indian Investments were negatively impacted in Q1, including a decrease in the fair value of Sanmar mainly due to a decline in the share price of its publicly listed subsidiary.

- The fair value of BIAL was relatively unchanged, supported by a transaction in 2023 where Fairfax India acquired an additional 10% equity interest in BIAL at an implied $2.5 billion valuation for the whole company.4.Liquidity:

- Fairfax India's cash and investments provide adequate liquidity to meet its obligations. Cash decreased to $29.4 million at March 31, 2024 mainly due to settlement of the performance fee payable.

- Proceeds from the NSE share sale in Q1 and Q2 2024 provide additional liquidity.In summary, Fairfax India experienced a challenging Q1 with significant unrealized investment losses, though its key holdings like BIAL remain resilient. The company maintains adequate liquidity supported by investment sales.

The airport

Based on the information provided in Fairfax India's Q1 2024 interim report, the following key insights can be gleaned about Bangalore International Airport Limited (BIAL):

1. Valuation Insight:

The fair value of Fairfax India's investment in BIAL remained relatively unchanged at approximately $1.6 billion as of March 31, 2024 compared to December 31, 2023. This valuation was supported by a transaction in 2023 where Fairfax India acquired an additional 10% equity interest in BIAL from Siemens. The transaction implied a fair value for 100% of BIAL of approximately $2.5 billion.2. Ownership:

As of March 31, 2024, Fairfax India held a 64.0% equity interest in BIAL. A portion of this interest (43.6%) is held through Anchorage, a consolidated subsidiary. This results in Fairfax India having an effective 59.0% fully-diluted equity interest in BIAL.3. Financial Commentary:

The interim report provides some high-level financial information for BIAL for the nine months ended December 31, 2023:- Revenues increased to $243.0 million from $167.3 million in the prior year period, reflecting higher aeronautical revenues from increased tariffs and passenger traffic.

- EBITDA increased to $158.7 million from $104.9 million, driven by the higher revenues, partially offset by increased expenses related to the new Terminal 2.

- BIAL reported a net loss of $9.0 million compared to net earnings of $5.8 million in the prior period, mainly due to higher depreciation and interest expenses from the operationalization of Terminal 2 during 2023.

So in summary, while BIAL's valuation remained steady, supported by a recent transaction, its financial results reflected a mix of positive revenue growth offset by higher costs and financing expenses related to its major expansion with the launch of Terminal 2. The management commentary indicates BIAL expects to see continued growth in passenger traffic.

-

2 hours ago, crs223 said:

After reading Warren’s letter I was left with the impression that we (BRK) are simply at the mercy of California/Oregon juries and regulators.

I loved hearing Greg (the bulldog) put the states on notice: we’re just gonna start shutting everything down when fire risks rise. And if you want us to add more capacity you can go fuck yourselves.

+1 to this. I also got the impression that we will drag this out in the courts until one of us is broke and it won’t be Berkshire.

-

Transcript attached and some Claude summaries from Wade’s comments and the Q&A

Wade Burton

- The investment portfolio stands at around $65 billion, including $9.3 billion in cash and short-term treasuries, $46 billion in fixed income, and $19 billion in equities (associates, limited partnerships, preferred and common stocks).

- The fixed income portfolio is built for safety, with government bonds making up the vast majority. It has a short duration of 2.8 years and yields 5%.

- The mortgage book stands at $4.8 billion, all first mortgages with duration under 2 years, yielding over 8.25%.

- Fairfax is watching inflation data closely and thinks it may be difficult for the Fed to drop rates if inflation stays above 3%. Higher rates could persist longer than expected.

- Of the $19 billion in equity and equity-like investments, associate investments (strategic/significant stakes like Eurobank and Poseidon) make up the bulk and are generally performing well and undervalued versus carrying value.

- Common stocks are a small portion at under $5 billion. Not seeing many opportunities currently with North American markets at high levels.

- Overall, the investment portfolio is structured to prioritize safety, with good locked-in interest income, little credit risk, and equity investments that are undervalued, soundly financed and performing well. It is positioned to handle uncertainty around interest rates and inflation.

Q&A Summary

1. Fairfax continues to hold total return swaps (TRS) on its own shares as it believes it's a good investment. The TRS contracts expire in 2025 and 2026 but can be extended. Fairfax also continues share buybacks, balancing it with maintaining financial strength and ratings.

2. Premium growth opportunities still exist in many lines despite the market not being as hard as in 2019-2023. Cyber, D&O and workers' comp are seeing rate decreases over 10%. Excluding Gulf Insurance, premiums grew 5% gross and 7% net in Q1. Fairfax's scale and diversification provide growth potential.3. The reinsurance market remains strong but not as robust as 2023. Odyssey had a higher base to grow from after taking advantage of the hard market in prior years. Allied World and Brit also have reinsurance opportunities.

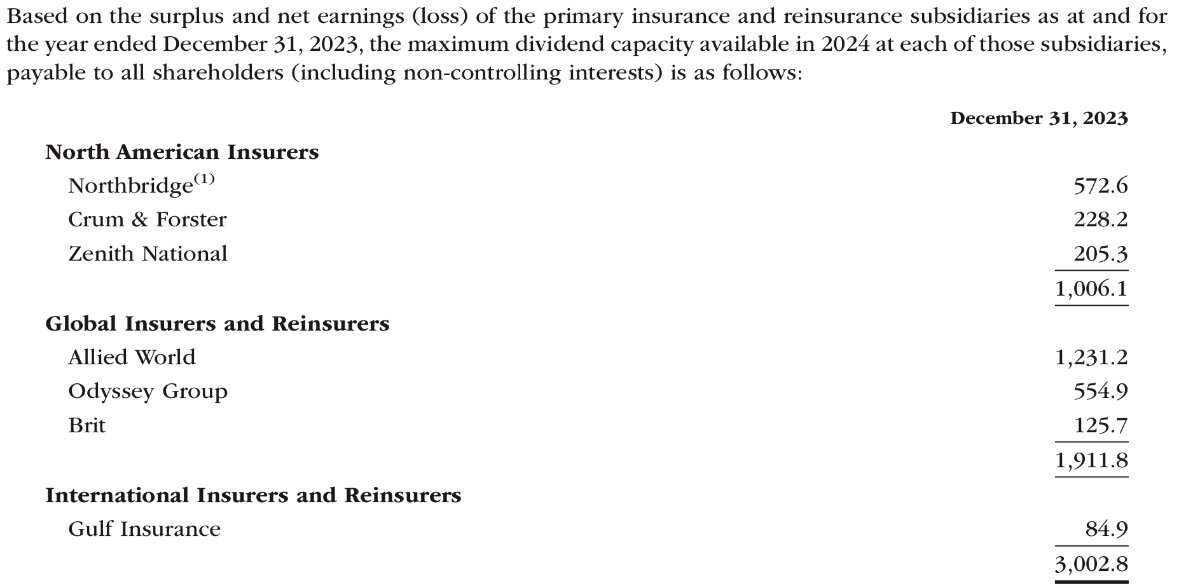

4. With premiums leveling off and earnings stabilizing, there is increased capacity to dividend funds from insurance subsidiaries to the holding company. In 2024, Fairfax can dividend $3 billion up based on statutory requirements. $451 million was dividended in Q1.

5. The consolidated expense ratio ticked up about 1 point in Q1 to 31.5% mainly due to the inclusion of Gulf Insurance which runs a higher expense ratio. Mix of business and continued investments in technology and people also contributed.

6. Fairfax has flexibility to reallocate from its defensive, liquid bond portfolio to equities if dislocations in the equity markets present attractive opportunities. -

Just got done listening to the CC. Great notes above by all. A couple of things that caught my attention

1. The callout by Wade on Grivallia.

2. The Dividend capacity by Jen captured in Note 19 and where it could come from

3. A shame that the last question got cut off on the amount that could be reallocated from bonds to equities in a market sell off. It would be nice to get an idea of the number. They have been pretty clear that it would be a move from treasuries to corporate debt but any further capacity for equities would have been an interesting insight.

4. In general great to hear from the “young guns”.

-

19 minutes ago, Viking said:

For me this is more qualitative/philosophical type thinking than quantitative/precise type thinking. And this makes it very hard to discuss/debate - because everyone comes at it in a very different way.

Pattern recognition springs to mind

-

Insurance companies are in good shape, Brit being a standout. The bond hit was a little higher than I expected. Looking forward to the CC

-

15 hours ago, petec said:

Why is the investment up 50% on net income growth of 20%, which would still put them way behind the guidance in that table? Did I miss something?

I figured he was basing the statement on on the 35% increase in “bullshit earnings” i.e EBITDA. Unfortunately not at the AGM so missed the tone.

As inferred above, I will be happy if this thing can be accretive and not some capital sink hole. Flipping APR sounds good. Given Sokol’s background if he can’t make it work (scale it) then ditch it. I get the impression it was forced upon them anyway.

Edit: clarification

-

16 minutes ago, SafetyinNumbers said:

Thanks! Many thanks to @NormR for helping so much with the editing and connecting me with his editor.

I’m so excited to see it in the paper when it gets delivered tomorrow. Long time subscriber, first time contributor

As you should be. It reads really well

-

Why Fairfax Financial should see an extraordinary run over the next decade

“Fairfax Financial is on the other side of an inflection point in its earnings and valuation that position it for an extraordinary run over the next decade. It’s following in the footsteps of Warren Buffett’s Berkshire Hathaway, which shot up 27 times after it reached the size Fairfax is now in 1995.”

@SafetyinNumbers nice work

-

6 hours ago, Hoodlum said:

It looks like a ratings upgrade may may be coming from Fitch, based on their Outlook switching from Stable to Positive.

Fitch Revises Fairfax's Outlook to Positive; Affirms RatingsVery good news indeed

-

6 minutes ago, gfp said:

I know I'm a broken record on that but watch the 2 year - at 5% buyers come flooding back in, which is unsurprising.

You have a pretty good handle on these things, so keep that record spinning

-

13 minutes ago, Luca said:

Great stuff, when will you do your first 8k? Maybe Cho Oyu? Seems to be the easiest one

I think you are being awfully kind. Perhaps if I had started 10 years earlier. Agree though Cho Oyu would be the starting point. At this stage I feel quite content gazing at the giants from a distance

-

43 minutes ago, Hoodlum said:

National Bank Analyst Jaeme Gloyn increased his target to $2100 Cdn.

https://www.theglobeandmail.com/investing/markets/inside-the-market/article-tuesdays-analyst-upgrades-and-downgrades-for-april-30/?login=trueThanks for posting the rump of the article

. Agree there will be a hit to the bond portfolio. My guesstimate is $40 per share but not phased +\-$10. It is all moving in the right direction.

-

20 hours ago, Xerxes said:

is there a specific peak or trail you would recommend for first timers in Nepal ? Which is more than a hill but not a killer.

Two come to mind

1. Everest Base Camp Trek - probably the most popular. The Khumbu Valley/Sagarmatha Nationa Park is truly stunning but busy.

2. Annapurna Circuit - not done this one but used to be the “go to”. Apparently not as popular now, as like a lot of Nepal, now have roads cut through to the villages.

3. if I was to do another trek there I would be looking at potentially a base camp such as Makalu or Kanchenjungain in the East.

We really enjoyed the trekking portion of this trip because it was a little off the beaten trek. The rural areas we passed through were stunning. A father and son working together to build their house was particularly memorable.

Nepal is full of the friendliest and most beautiful people on the planet. You will find it hard to go wrong

.

-

7974 Nintendo Co

-

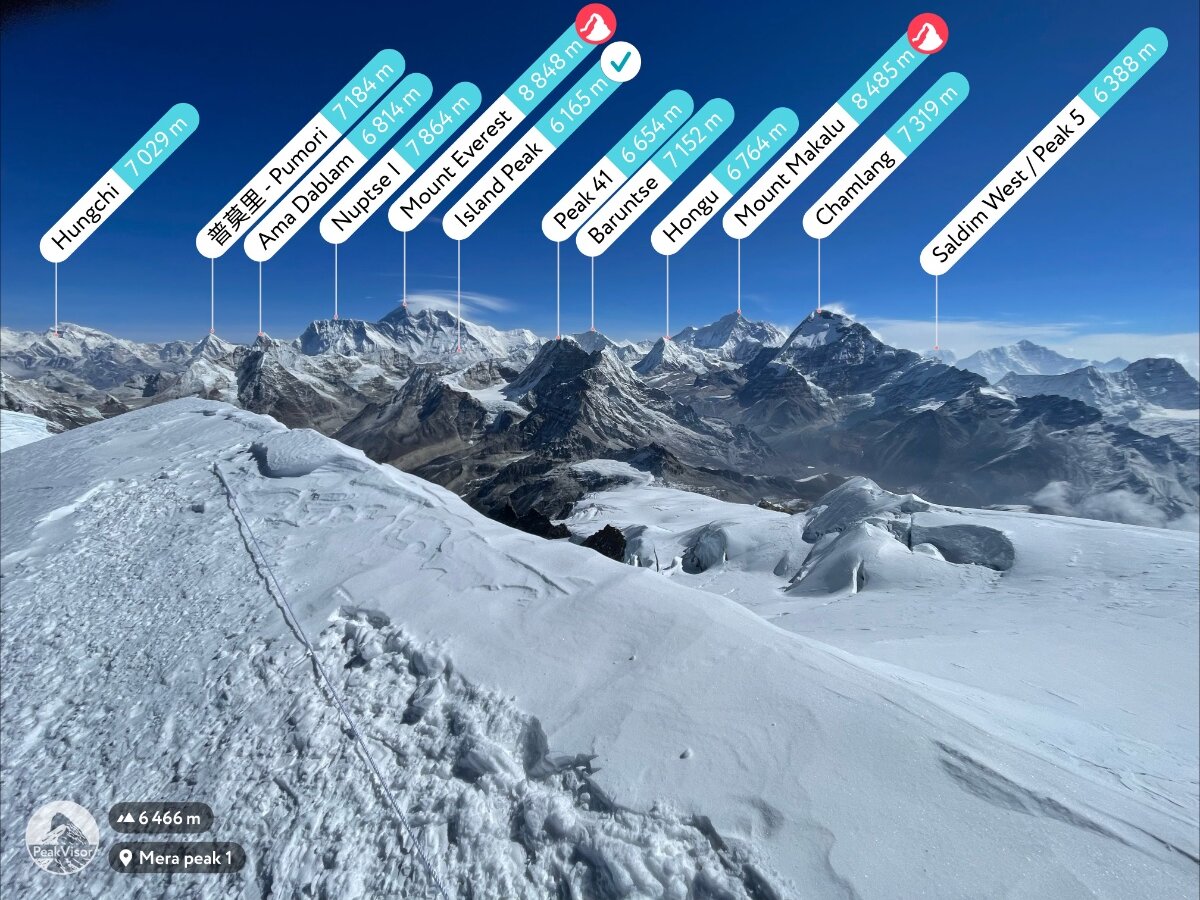

We are just back from trekking to Mera Peak (6476m) in Nepal. Despite its reputation as the highest but easiest of the “trekking peaks,” we still only got three out of our party of 12 to the top. Two dropped out on the way to base camp (5200m), and the rest made it to high camp (5900m), but a combination of cold and altitude took its toll. I considered our acclimatisation route to be very conservative, but altitude just affects everyone so differently.

I set out with my two boys and a friend’s son around 2am. Unfortunately my oldest son turned back due to the cold (-16C) but the youngest (16 YO) made it to the top. It was a great experience but reaffirmed that anything over 6000m is always going to be a challenge.

Digit

in Fairfax Financial

Posted

Cheers, big news if true. Here is the source