nwoodman

-

Posts

1,479 -

Joined

-

Last visited

-

Days Won

8

3 Followers

.thumb.png.e9643dd797bb6bfa93083ce1311ba74d.png)

Recent Profile Visitors

8,068 profile views

nwoodman's Achievements

")

-

Timely article from Mauboussin at MS entitled Probabilities and Payoffs: The Practicalities and Psychology of Expected Value (attached). Nothing new for the value investors here, but it did get me thinking about why I am happy with concentrated positions in Berkshire and Fairfax. Everyone’s risk tolerance is different but for me the key touch points in the article are: Fairfax Thinks in Expected Value Terms • Investing success is about payoffs, not just probabilities—Fairfax inherently applies this through its insurance and investment approach. • They take asymmetric bets—protecting the downside while positioning for large potential gains. Internally Diversified, Reducing Risk (the big one for me) • Insurance float provides stable capital for investing. • Investment portfolio spans equities, fixed income, and alternative assets. • Global presence and non-insurance subsidiaries offer further diversification. Aligned with Kelly Criterion & Position Sizing • If an investment has an edge, capital should be allocated accordingly—but not overbet. • Fairfax’s focus on capital preservation ensures it avoids wipeout while allowing compounding. Embracing Volatility While Managing Drawdowns • Hedging and contrarian investing have helped them profit in downturns (e.g., 2008). Sometimes this has come with opportunity cost but overall no significant capital loss. • Low correlated leverage prevents forced asset sales during stress periods. Even when seemingly cash strapped they have a remarkable ability to pull a deal together via their extensive and ever growing network. Final Thoughts • Risk management is their business, making them an ideal concentrated bet. • Their ability to capitalize on market inefficiencies aligns with a long-term compounding strategy. • Tax is a consideration for me, so an acceptable return while leveraging an unrealised tax liability works well for me. I think Prem’s aspiration to build the 100 year company along with the tenure of key personnel and the resultant culture are key factors for me. The article is worth a read, just to reinforce probabilisitic reasoning. Authors: Michael J. Mauboussin – Head of Consilient Research at Counterpoint Global, Morgan Stanley Dan Callahan, CFA – Member of the research team at Counterpoint Global, Morgan Stanley Mauboussin is well-known for his work on decision-making, behavioral finance, and the application of probability and expected value in investing. His background makes this report particularly relevant for investors who focus on risk management, capital allocation, and probabilistic thinking. article_probabilitiesandpayoffs.pdf

-

These are important points, and the second one is something I’ve been thinking about a lot since the CC. This deal gives a glimpse into the kind of earnings power that comes from shifting a portion of the fixed-income portfolio from safe treasuries into higher-yield corporates. They have been telegraphing this intent for a couple of years now. I’m not saying that shift has fully started yet—you probably need some real stress in credit markets for that to accelerate—and even then, it’s only ever going to be a portion (maybe 25% at most?) of the FI portfolio, given RBC constraints and regulatory capital rules. That said, it illustrates how much earnings power can change under these conditions. As you pointed out, it’s easy to be anchored to a decade of low rates, but these yields aren't necessarily outliers in an HFL (higher-for-longer) environment. I still don’t think that kind of optionality is being priced in. If Fairfax continues to lean into private credit and structured high-yield deals like this, the long-term earnings profile of the fixed-income book could look very different from what the market is currently expecting.

-

MS with a breakdown by non-life insurance sector. It looks like Digit’s speeding ticket is still intact INDIA_20250214_1507.pdf

-

MS with a positive spin (see attached) “The broad market is drawing down rapidly as the bid has faded despite improving fundamentals. While catching the bottom is difficult, we think buying Indian equities could prove rewarding.” INDIA_20250217_1001.pdf

-

Thanks @Viking. Agree with all your points. There is a degree of sophistication to the way Fairfax is going about things that I wish I had appreciated more. There is also a frankness in the CC’s that is quite refreshing “Peter Clarke Right. Yes, no, that's -- the TRS on Fairfax, that's strictly an investment for us. We put it back on in 2021 or thereabouts and it's performed extremely well and we think it will continue to perform very well. As we said, we can see strong underwriting results going forward. Our interest in dividend income is strong, our associate income is strong. But we feel we'll be able to continue to compound book value at a very high rate or acceptable rate, and our share price will follow. You know, we're not trading at a high multiple if you look at our peers and so for us, it's still an investment, we very much like.” The thing that make’s my head spin a little is their short and medium term opportunity set. $835m of timeshare financing at an aggregate >10% was not on my bingo card for January. For a while I have felt they have/perceive more opportunities than they have available cash. Just hope they don’t get over their skis but so far, so good.

-

Not sure, other than their debt raises, there aren’t too many details available on their instruments of choice, but interesting point about the FX implication. CAD would definitely help the cause . I thought you might have had a handle on who the Total Return Payer was, pretty sure you figured it was one of the Canadian Banks so I think there is a high probability it is in CAD. Anyway some notes attached, it’s definitely floating rather fixed as they have discussed a “ higher TRS expense” previously that coincided with rising rates. Fairfax Financial’s Total Return Swaps on Its Own Shares.pdf

-

While that would be awesome, surely this is at the prevailing rate, SOFR + spread. Cheap compared to IV growth, but unlikely to be locked in. I am tipping 4.75%+2%=6.75%.

-

I am a Fairfax investor, so it crossed my mind of course. Vacatia is obviously the price taker here and Fairfax didn’t have to do the deal. There needs to be enough cashflow to service the 80m of financing (unless there is a PIK provision to the note) and whatever Vacatia needs to set up their system at Berkeley to start clipping tickets. You would hope the assets were some way to this target and then Vacatia generates the rest through the overnight rental market plus some asset sprucing. In the pdf I outlined some thoughts on how it might work but it’s speculation. If it goes tits up then you hope that the Berkley assets can be sold at cost. My only other thoughts are Wade Burton’s tie ins with KW and Eurobank, he seems to like (tourism) property but as @petec said there has been a few flops or works-in-progress depending on your timing. As I said above I would love to know how this originated and whether it came via KW or an associate. Out of the blue seems unlikely but possible. Will be watching this one with great interest due to the quantum but also an insight into Wade’s deal making and risk management. In both areas I think he excels BTW. Always difficult due to the way Fairfax allocates capital to attribute a decision to one person though.

-

Indeed, as you pointed out above if it works the leverage will be pretty phenomenal albeit on $25m of equity. It will be interesting to get some color on the terms of the note, perhaps AR or at least Q1.

-

Sensex down 3,000 points in 9 days. Is it just the beginning of bear market? Quite the blow off in Indian markets. On the updside, IDBI is down 30% since its peak in July 24. At the current market capitalization of INR 775 billion, the 60.72% stake being put up for sale is worth approximately $5.42 billion USD.

-

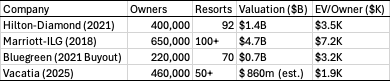

Corrected in V3 above, it should have read Vacatia contribute their business model to the Vacatia Blizzard JV. Vacatia is definitely still a stand-alone. I also corrected the EV/Owner table on the basis that Berkley got done at $835m (Fairfax) and $25m (Vacatia)=$860m. We don't know this for sure (chance of financing outside of Fairfax), but on face value it does seem like a decent margin on safety. However I know SFA about the the timeshare industry so take it with a pinch of salt. The Vacatia business model of timeshare plus overnight rentals isn't unique but might make a real difference to legacy assets like Berkley. I guess that's Vacatia's bet and if it doesn't turn out well Fairfax flips the underlying assets. Each year Fairfaxearns $80+m so the margin of safety improves. I would love to know how this deal orginated, perhaps yet another question for the AGM. Wade Burton from the CC " Second, I wanted to discuss an investment that closed just after year-end 2024. We invested in the largest independent timeshare company in America called the Berkeley Group. Caroline Shin and her team at Vacatia are Fairfax partners here. The investment is underpinned by asset value, where we directly own 4,950 full-service vacation units mostly located in Las Vegas, Orlando, and other high-traffic vacation areas in the U.S. The opportunity here is for Caroline and her team to generate overnight rental income from the huge stock of nightly vacancies. Her experience designing Hotwire online booking software and then as an executive at Starwood is perfect for what Vacatia is trying to do with Berkeley. In fact, prior to this acquisition, her group at Vacatia made investments in five smaller timeshare assets from 2019 to 2024, and in each case, they were very successful at significantly growing EBITDA in a short period of time. The total deal was $835 million, which we funded with a $275 million five-year preferred note at 13.5%, a $365 million seven-year senior secured note at 9.5%, and $170 million mortgage warehouse loan with a five-year maturity at SOFR plus 400. The $50 million equity is funded 50% by Fairfax and 50% by Caroline and her partners. We are absolutely thrilled to be her partner on this."

-

Hopefully it plays out something like this: “1. PVC Price Recovery and Demand Growth (Mid-to-Late 2025 Onward) • The PVC market is showing early signs of stabilization, with prices bottoming out in late 2023. • Industry experts predict higher global PVC demand in late 2025 and 2026, driven by a rebound in construction and infrastructure spending, particularly in India and Southeast Asia. • India’s PVC consumption is expected to grow at 8% CAGR, creating a structural demand tailwind for Sanmar’s Chemplast Sanmar unit. • Timing: Expect a gradual price recovery from mid-2025, with stronger margins by 2026. 2. Anti-Dumping Measures in India to Support Domestic Pricing (Q2 2025 Onward) • The Indian government is advancing anti-dumping duties on paste PVC and suspension PVC imports, particularly from China, South Korea, and the EU. • If finalized, these duties would reduce import pressure and improve pricing power for domestic producers like Chemplast Sanmar. • The PVC Quality Control Order (QCO), set to take effect by June 2025, will further limit low-quality imports, benefiting domestic manufacturers. • Timing: Once anti-dumping measures are officially imposed (likely Q2-Q3 2025), expect price support and margin recovery for Sanmar. 3. Full Utilization of Expanded Capacity and Operational Efficiency Gains (Q3 2025 Onward) • Sanmar has completed major capacity expansions (e.g., 41,000 TPA specialty PVC addition and full ramp-up of TCI Sanmar’s 400,000 TPA Egypt plant). • Efficiency improvements and higher utilization at TCI Sanmar (Egypt) should significantly boost profitability once PVC prices stabilize. • Timing: Efficiency-driven profitability improvement from Q3 2025, with full impact in 2026. 4. Diversification into Higher-Margin Specialty Chemicals (Late 2025–2026) • Sanmar is expanding its Custom Manufactured Chemicals Division (CMCD) to cater to high-value agrochemical and pharma markets. • Five new contracts signed for specialty chemical intermediates, with a second-phase expansion of the new plant planned in 2025. • This shifts revenue mix away from commodity PVC toward less cyclical, higher-margin products. • Timing: Specialty chemicals’ revenue contribution will increase meaningfully from late 2025. 5. Stronger Financial Position and Lower Debt Burden (Q4 2025 Onward) • After the 2021 IPO and debt repayments, Sanmar significantly reduced its financial leverage, lowering interest costs. • Fairfax India remains a long-term supportive investor, providing stability. • Recent cost control measures and cash preservation efforts position the company for profitability in the next market upturn. • Timing: Lower financial costs and improved cash flows from Q4 2025, supporting sustained profitability. Expected Timing for Sanmar’s Return to Profitability • Short-Term (H1 2025): Limited profitability improvement, awaiting pricing recovery and regulatory actions. • Mid-Term (H2 2025): Anti-dumping duties, demand recovery, and full plant utilization start boosting margins. • Long-Term (2026): Stronger profitability driven by higher PVC prices, specialty chemicals growth, and cost efficiencies.” We shall see. Fairfax seems happy to wait it out, so that’s good enough for me.

-

Love your work. Didn’t realise or had forgotten that there was a sunrise on that deal. I always figured that they would buy this in first. That color explains it.

-

Don’t disagree but the thesis is the airport. Sanmar is going to be a drag for the next year but should start working from 2026 onwards.

-

I've attached some notes on Vacatia. I sound like a broken record, but I love these structured deals. I doubt its lost on anyone here but this is such a sweet spot for Fairfax. There seems to be no shortage of deals to be done. Hopefully we hear some more color from the Fairfax team in a few hours time. Caroline Shin Bio: Caroline Shin is a seasoned tech entrepreneur and hospitality executive best known for co-founding Vacatia, a platform modernizing timeshare management. Key highlights of her career: • Built and sold Hotwire: As a founding team member, she helped scale the travel site before its $685 million sale to InterActiveCorp in 2003. • Led Starwood Hotels’ CRM strategy: Boosted market share by 20–40% for top properties through data-driven pricing and loyalty programs. • Founded Vacatia (2015): Created a tech platform serving 750+ resorts, helping owners rent/sell timeshares and manage operations digitally. • Launched Vacatia Partner Services (2023): Expanded into hands-on resort management, now overseeing 4,750+ units across the U.S.. • Co-founded Store Vantage: A SaaS tool optimizing staffing and customer relationships for small businesses. Trained as a nuclear engineer at MIT, she applies analytical rigor to solving hospitality challenges. Outside Vacatia, she runs a pet grooming business and advocates for Korean American community initiatives. Edit: Updated following Q4 24 CC, very good of Wade to break it out *Note: actual interest on the $170M warehouse will vary with SOFR. At a 5% base rate, SOFR+4% = 9% (≈$15.3M/year). If rates decline, interest expense will fall (and vice versa). The Secured Overnight Financing Rate (SOFR) is a benchmark interest rate that reflects the cost of borrowing cash overnight using U.S. Treasury securities as collateral. It is widely used in financial markets as a replacement for LIBOR (London Interbank Offered Rate) for pricing loan bonds and derivatives. Weighted Average Yield: Fairfax's weighted average cash yield is robust based on the structured notes alone (excluding equity). On $810M of combined loan investment, the annual interest of ~$87M equates to roughly a 10.7% blended yield. Including the floating portion at current rates, the overall yield is in the low double-digits, which is very attractive for a secured, asset-backed investment. This reflects the risk profile (timeshare assets are somewhat niche and less liquid), but Fairfax negotiated rich terms. Company Comps Vacatia and Blizzard Vacatia: Company Analysis V3.pdf