mattee2264

-

Posts

717 -

Joined

-

Last visited

-

Days Won

7

Content Type

Profiles

Forums

Events

Everything posted by mattee2264

-

If the AI bubble like the Internet, in what year are we now?

mattee2264 replied to james22's topic in General Discussion

If there is any truth to this then can't be good for NVIDIA as indicates chips may no longer be a limiting factor and a second hand market will soon develop as early start-ups with hugely expensive NVDIA GPU inventories may collapse unable to generate a sufficient return on their early investments, and latecomers have the advantage because they can buy cheaper and fewer chips and target niches. Monopolistic competition seems to be emerging and there will be a multitude of differentiated LLMs that make money in the short run but don't make any money in the long run. Just like autos and airlines. -

I was talking about the US economic outperformance not the US stock market outperformance (which I agree can mostly be explained by cloud/AI). When manufacturing is in recession and consumers are feeling the pinch then its been massively helpful to the US economy that the government is able to run multi-trillion fiscal deficits and helped the US avoid a post-COVID hangover and more than offset the contractionary effect of Fed monetary tightening. Trump clearly wants to run the US economy hot with the expectation that the AI revolution will increase productivity and increase the sustainable US growth rate.

-

There was a London Standard article on precisely that. The argument was that ceremony reveals where the power lies and the tech oligarchs were front and centre at the inauguration ceremony and are very much kingmakers. There were some signs the Biden administration were going to take some antitrust measures. But I imagine that Trump figures that national security is much more important than monopoly abuse and will do little to curtail Big Tech's dominance so long as they continue to spend hundreds of billions on AI.

-

If the AI bubble like the Internet, in what year are we now?

mattee2264 replied to james22's topic in General Discussion

So Trump adding fuel to the fire by promising deregulation and announcing the $500B Stargate initiative to expand data center capacity. Surely all of this adds a lot more fuel to the fire? Especially as the Trump administration isn't going to want the bubble to burst on their watch when they are now actively promoting it and supporting it. And so long as new money keeps coming in (whether that it capex or stock market inflows) then that continues to breathe air into the bubble. -

A big factor in the US outperformance in the post-COVID period has been the USA's ability to run multi-trillion dollar fiscal deficits. I am not convinced that is an entirely sustainable driver of exceptionalism. Although it is likely to continue for the foreseeable future. Open borders under Biden may have also helped offset the inflationary impact of such spending. The big pitch seems to be that AI will trigger a new industrial revolution and America will be at the forefront and cementing the Big Tech oligopoly is therefore a necessary evil not least if it helps us stay one step ahead of China's AI efforts. And so long as there is huge investment spend on AI every year that is going to keep the US economy booming the same way it did in the late 90s. Although there has been some scepticism about the much anticipated productivity benefits from AI e.g. the paper by Acemoglu the famous economist and Goldman Sachs also did a paper on that and so did Sequioa Capital. Although that doesn't really matter during the build-out/boom phase.

-

Trump's spent a good chunk of his career plastering his name over hotels, casinos, resi blocks, so hardly surprising he figured out he could make hay by doing the same with a memecoin. But it is absolutely shocking he's not even been inaugurated and already made $7BN from the coin after paving the way for another crypo bubble with his pro-crypto stance and promised financial deregulation. Public office becoming so ridiculously lucrative is yet another sign America is turning into a 3rd world country.

-

Lower taxes and lower interest rates will probably keep earnings going up. And so long as the likes of Microsoft, Amazon, Meta, Google continue to invest their prodigious cashflows into AI that will pump up semiconductor stocks and keep the AI story alive. No idea how long all of this can continue but probably longer than most people think. Aside from the AI bubble bursting the main risk is that the Trump administration economic policies backfire. He had a very pro-growth agenda in 2017 but it ran out of steam pretty quickly, a trade war was underway, and even before COVID hit the economy was slowing down considerably. And while in business cutting waste and restructuring pays off when it comes to government while beneficial in the long term in the short term it is going to hurt GDP.

-

Trump is a populist. And it is far easier to pump up the bitcoin price than the stock market. And easy for the US government to find some pretext to purchase a few million bitcoin.

-

Lot of wild predictions about Bitcoin future prices. Charles Schwab sees Bitcoin $500k-$1m. Chatter about Trump adopting Bitcoin as a reserve currency which seems to be driving the latest surge upwards. And if central banks, institutions, corporations and individuals are all loading up on bitcoin and there are only 22m coins in circulation then who knows how crazy things could get.

-

https://wealthmanagement.bnpparibas/en/insights/market-strategy/time-to-fade-the-magnificent-7.html Above article is a decent read. But as the article admits timing these things is difficult.

-

Wouldn't say they are low IQ. Hussman is a market statistician. Grantham is a market historian. And both approaches have severe limitations.

-

Seems like this could be the next big thing in technology. Alphabet caught a bid recently after releasing Willow. https://www.cnbc.com/2024/12/10/google-claims-quantum-milestone-but-cant-solve-real-world-problems-.html https://www.bbc.com/news/articles/c791ng0zvl3o https://www.bbc.com/news/articles/c79ngx01qvro I'm very much in the "not in my circle of competence" when it comes to technology but when technology stocks make up over 1/3 of the market and have accounted for the majority of the gains in the bull market that started around October 2022 it is interesting to follow from the sidelines.

-

Probably looking at 5 year performance (to include pre-pandemic) is a better guide as most stocks overshot in the COVID recovery because of the excessive policy response (ZIRP and fiscal handouts) and October 2021 was quite close to the peak of the last cycle. Agree with your point that they aren't as expensive as they were then because of build-up of retained earnings and the decrease in inflation-adjusted stock prices. But that isn't the same as saying they are bargains. And I think a lot of stocks are already pricing in quite a bit of optimism in relation to interest rate cuts and a soft landing and for this reason have recovered most if not all of their bear market losses. And there are also potential issues in the future to do with refinancing at higher interest rates and in the case of the banks commercial real estate problems. But yes if the economy can start improving and some of the AI productivity benefits start coming through then you'd expect from fairly average valuations that the rest of the market can produce healthy returns as a result of dividends + growth and there is room for valuations to go higher. The difference with Mag7 is the pandemic had lasting benefits as it accelerated the shift to cloud which has been a huge growth driver and the bear market also encouraged them to streamline their operations and improve their efficiency and they are also benefiting because the assumption is that Big Tech will also end up being Big AI.

-

Good article and Jeremy Grantham and colleagues have produced similar analysis in the past. Of course the main driver of stock returns second half of this cycle has been Mag7. They hardly pay any tax and even if interest rates stay around 4-5% cash and bonds aren't going to provide much competition so long as they can continue to grow at double digit rates and there is a lot more room for multiple expansion. Of course eventually their growth will slow down and that will hit their valuations and the rest of the market may struggle to pick up the slack with the headwinds of higher interest rates and tax rates the article mentioned. But in the short term that seems unlikely as public cloud spending is still growing at about 20% a year and AI will give another kicker to their returns and their market positions in the short term at least are unassailable and they have incredible pricing power.

-

If the AI bubble like the Internet, in what year are we now?

mattee2264 replied to james22's topic in General Discussion

Something I am trying to get my head around is the impact of all the AI spend on Mag7 profitability. For NVIDIA It is quite obvious. The AI capex of the other Mag7 members is NVIDIA's revenue and so long as they keep spending on NVIDIA chips at any price then NVIDIA will continue to enjoy insane margins and revenue growth. But I am wondering if there is also a benefit to the cloud divisions of Amazon Google and Microsoft. Presumably AI's insane computing and data requirements is increasing demand for cloud and therefore giving a boost to cloud growth? And cloud remains the biggest growth driver for Amazon Google and Microsoft who without it would be mature companies that would struggle to grow at double digit rates. If you look at the Q3 results of Mag7 members cloud growth is still incredibly strong and helping to justify multiples of around 40-50x earnings. And earning power is massive even without much in the way of contribution from nascent AI products. In the event that the AI investment boom turns to bust due to overcapacity and insufficient returns on all the associated capex then will the earning power of the other Mag7 members (as well as NVIDIA) take a hit? Or is this overwhelmed by the massive non-AI tailwind because over the world companies increasingly switch from on-premises software/hardware to cloud? -

I think there are a few reasons why US deficits have yet to be inflationary: -There's been a very beneficial supply side impact from cheap immigrant labour which has helped to avoid a wage-price spiral -Despite that massive stimulus the US economy isn't running hot by any means -Commodity prices have dropped off significantly because of China weakness and sluggish global economy ex USA generally -A lot of the spending has been very unproductive e.g. adding to government payroll, paying interest, various vanity projects so hasn't really been filtering into the real economy in the same way the stimulus checks (which contributed to the first wave of inflation) did -Full employment is a bit of a misleading concept because it ignores individuals who have dropped out of the labour force

-

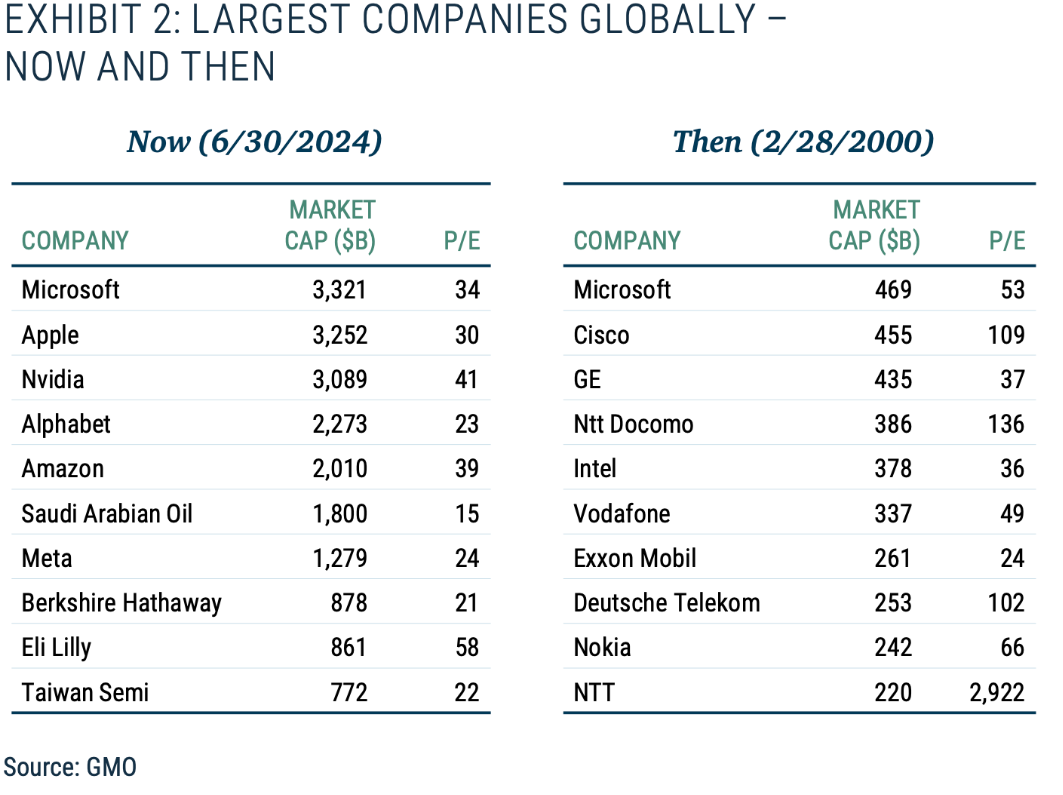

I think the lesson is that no-one should underestimate the ability of fiscal and monetary policymakers to help the stock market defy gravity or their willingness to do so. Global central banks are all on course to ease aggressively even though their economies are doing just fine all things considering. Whoever gets elected is going to continue to run huge fiscal deficits to juice the economy. An over-easy policy stance in theory is inflationary but because its impact just seems to find its way into asset prices rather than the real economy the main inflationary impact is going to be on asset prices. And so long as there is a free lunch or the price lies far ahead in the future policy makers aren't going to care. Also the AI ecosystem is incredibly circular so incredibly self-reinforcing. Big Tech are minting money so can afford to spend huge amounts in AI capex regardless of the state of the economy or interest rates or tax rates or whatever else. This in turn boosts the earnings of chip companies and reinforces AI enthusiasm. No one seems to consider the possibility that it could be mal-investment or overinvestment and the future returns might not be sufficient to justify them. Instead markets are hyped up on the near term growth of the chip makers and the assumed future growth both of Big Tech and their AI products and the rest of the market and the economy based on the assumed productivity/efficiency improvements AI will deliver. And as long as the articles of faith are that: -Policy makers can manage the economy so that deep long recessions and financial crises are a thing of the past -AI is going to allow trillion dollar companies to continue to grow at fast rates and result in a productivity miracle for the rest of the economy Then I really think the S&P 500 could rise an awful lot more from now. GMO have a nice table comparing 2000 and now. They claim the media PE was 60 in 2000 for the top 10 companies compared to a median of 27x now. So on that basis we could see markets double over the next few years before we hit a bubble peak. Of course there is a bit of a difference because the mega-caps are a much higher percentage of GDP and are more mature and while the pitch with the internet was that the new economy would replace the old economy e.g. e-commerce, digital advertising, with AI the idea is that it will allow companies to expand margins and cut costs and the resulting cost-savings will presumably be the AI companies revenue.

-

Short term at least I think US outperformance seems pretty darn likely. US economy continues to show resilience (although I think a lot of it is due to the trillion plus dollar deficits and government hiring spree) but the Fed seems determined to aggressively cut interest rates. I imagine all the AI capex is also probably having some multiplier effects in the same way the US economy accelerated during the dot com bubble. And a bubble cannot fully form without the impetus of easy credit and that's been the missing ingredient so far in the AI bubble as rising interest rates have been a headwind. I'm an AI sceptic but it is the stuff that bubbles are made of: a revolutionary technology that promises to boost productivity, cut costs, increase margins and extend the growth runway of the tech mega-caps. Big Tech CEOs feel forced to invest huge amounts which is propelling NVIDIA to the stratosphere and corporate CEOs will also feel forced to invest in whatever products Big Tech put out because they know all their competitors will be doing so and everyone likes to try out a new technology and the idea of automating mundane tasks allowing companies to lay off lots of workers is an easy sell. The problems probably arise a few years down the line if expending more and more computing power fails to bring about further advances in the technology and the AI products fail to deliver the hoped for benefits or the costs outweigh the benefits which would make it difficult for Big Tech to achieve payback on their huge investments let alone a return and if they then cut back on their spending that will hurt the semiconductor companies who are minting money at the moment.

-

Agreed. Although if the Fed is hell bent on easing then it has a pretty big runway to offset any disappointments in relation to earnings (both corporate and GDP).

-

I find it a bit disturbing how much both Chinese and US not to mention Japanese stock markets are moving in response to actual and expected policy announcements. Doesn't look like a sign of healthy economies.

-

Interesting thing though is if you look at that chart selling when forward PE ratios rose above 20x you'd have been well served to lighten up on stocks and had an opportunity within a year or two to get back into the market at close to an average valuation. And worth noting that over the last 30 years we've been in a pretty low interest rate environment which will have had a benefit to average forward valuations. Question is whether this time is different. Market does seem to be anticipating fast growth of Big Tech earnings both over the next 12m but also for many years after that. And Big Tech forward PE ratios are clearly well above the average for the market.

-

It is pretty stupid really. China want us to take their low-skill manufacturing jobs so they can move up the value chain and take advantage of the scientific and technological capabilities they've been building as well as their strategic resource base. I can't help feeling that long term China may well be an absolutely fantastic investment bet to the point that it probably doesn't matter whether it may be currently overbought on the assumption that the stimulus package (and assumed future stimulus packages) prevent an economic depression. Short term things seem murky though. A consumer economy is easy to stimulate with stimulus checks and low interest rates. But investment has been a huge driver of the Chinese economy and there is a massive overhang of malinvestment and even low interest rates and easier credit conditions are unlikely to be enough to stimulate investment. And if the government tries to replace the investment spending by making its own investments a further misallocation of capital is even more likely.

-

Annoying that the major China indices have bounced 50% off the bottom. But there was a similar bounce after the COVID intervention and a lot of people were expecting another leg down but the stimulus kept flowing and it never happened. And you are still paying only about 12x earnings which is over half the valuation of the US stock market. And with the US stock market you're already pricing in a resilient US economy and Big Tech dominance and a favourable low tax and low interest rate environment and many other positives which may not be sustainable. And even after the bounce the index is still trading at levels that were seen over a decade ago. Short term outlook isn't great but there are reasons to be optimistic about the long term prospects of the Chinese economy as they've made significant technological and scientific advances and are moving into higher-margin businesses.

-

True. Then again when gold has a good decade it can increase many multiples in price and for most of the last 15 years or so it has been trading in a range of $1000-$2000 only breaking out over the last year or two.

-

Yeah that is the problem really. The insurance premium can vary depending on how scared market participants are. And also because there is no intrinsic value then there will be a lot of performance chasing. The gold price has basically doubled from pre-COVID levels. To some extent that reflects inflation as the price level and the money supply is around 30% higher. But offsetting that inflation has come down significantly which diminishes its value as an inflation hedge and interest rates are a lot higher so the absence of any income becomes more of a negative factor. Understandably there are concerns about the path of US government debt but difficult to know to what extent such concerns are already priced in and whether if governments finally decide to address the problem whether that will hurt the gold price. To me the gold miners look more interesting. You are essentially buying gold at a discount so there are two ways to win (the discount closes or gold price increases). The industry is consolidating and the gap between costs and prices allows for some mismanagement.