SafetyinNumbers

-

Posts

2,818 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

I have built a 6% position in Strathacona Resources (SCR.TO) ahead of their expected capital return policy to be provided with Q2 results on August 14. The company is guiding to C$1b in free cash flow or ~C$4.50/share to be returned to shareholders at $80 WTI. They say they will have a base dividend that is sustainable if prices dip. My bet is that will be using $60 WTI which should support more than a 5% yield. They also have discussed variable dividends, SIB or NCIB. I’m a big fan of the management team. They certainly have skin in the game with Waterous fund owning 91% and have no dilutive securities (options etc..). They have a history of growing accretively through acquisition but want to use their stock now that they are public but the stock is too cheap. I think that makes them very motivated to close the NAV discount (~30-40%) as quickly as possible.

-

Thanks for tallying up the quarterly gains, @dartmonkey. This should make a decent difference to FFH’s Q2 results as well.

-

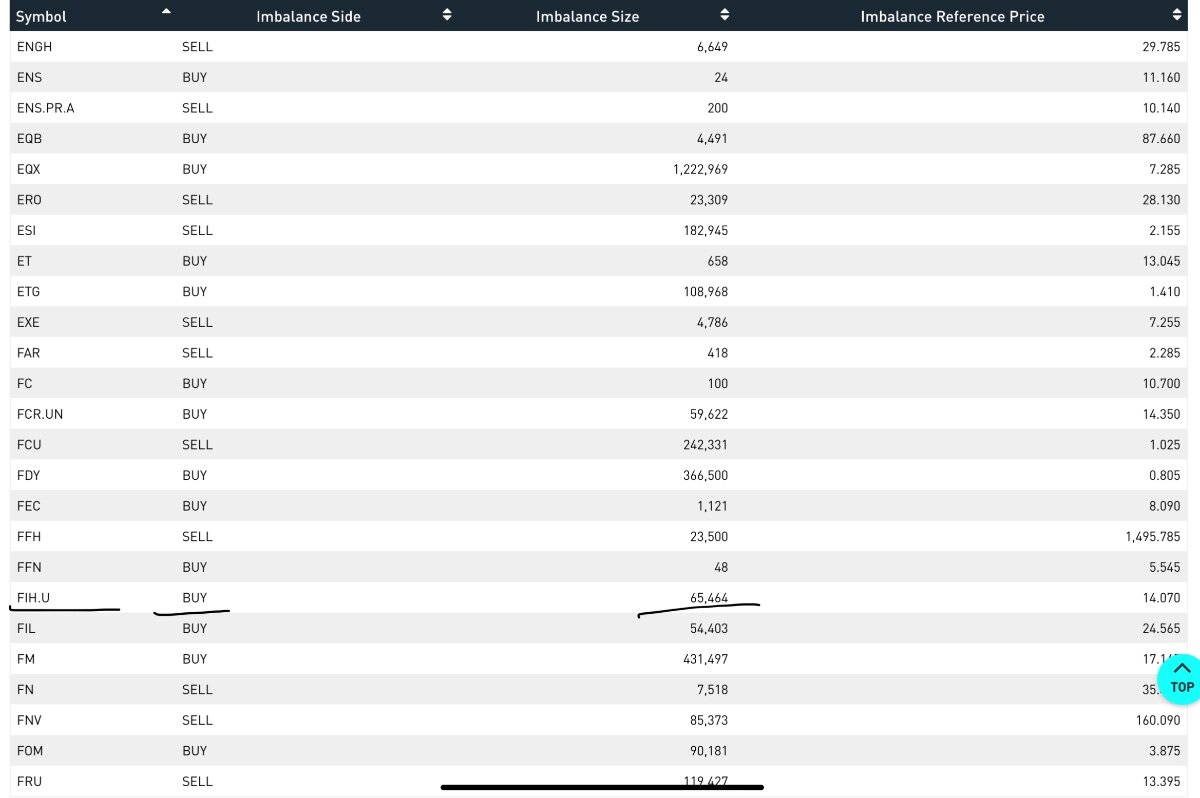

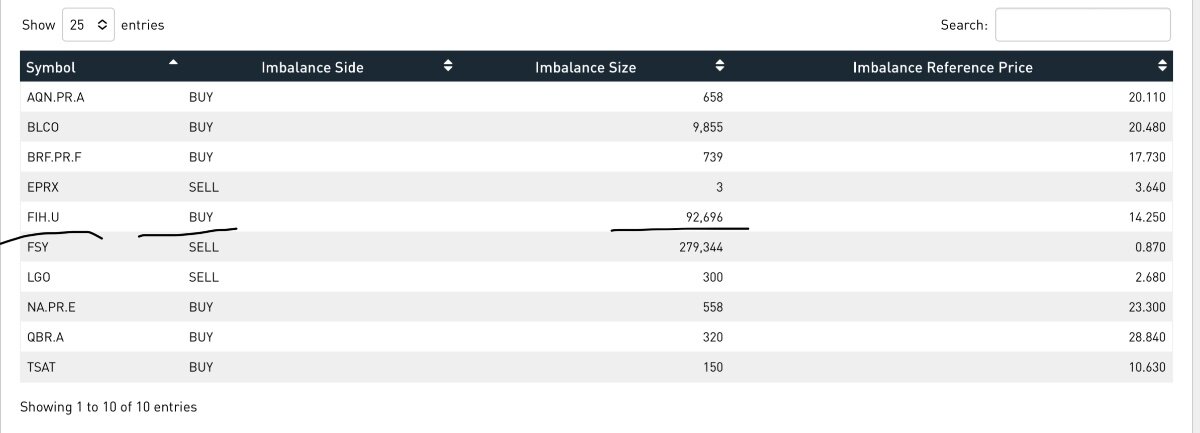

It looks like there was a Market On Close (MOC) imbalance at the close. I used to check these religiously when I was on the prop desk at UBS as it was brand new and there was a lot of edge available. Maybe I should again . The TSX publishes the imbalance at 3:40pm and brokers can enter orders in the MOC facility to offset the imbalance until the close. If the stock is going to move on the imbalance more than a certain percentage from the VWAP of the last 20 minutes of trading or the last price they publish a Price Movement Extension (PME). This allows brokers another opportunity to offset the imbalance. This afternoon had a buy imbalance on the MOC and it grew when they published the PME. Meaning investors saw there was an imbalance to buy and more added to it then provided an offset. The stock went up to 15.15 because that was the clearing price. The buy imbalance acts like a tender at the close. For a buy imbalance, the shares offered at the lowest price in the MOC facility and in the open market get priority but all trades clear at the price needed to satisfy the buying. i hope that’s explanation is helpful. I don’t remember all of the specifics but fairly certain on the mechanics. It has me wondering why someone decided to trade it this way and if they have more to buy.

-

Is there any analyst coverage yet? Maybe that will bring the quants in

-

Besides the resulting Xerxes is pointing out, the line of thinking ranimo presents suggests “the errors” were considered errors when they were entered into. In reality, FFH investors cheered the hedges and gave FFH a much higher valuation than it has now.

-

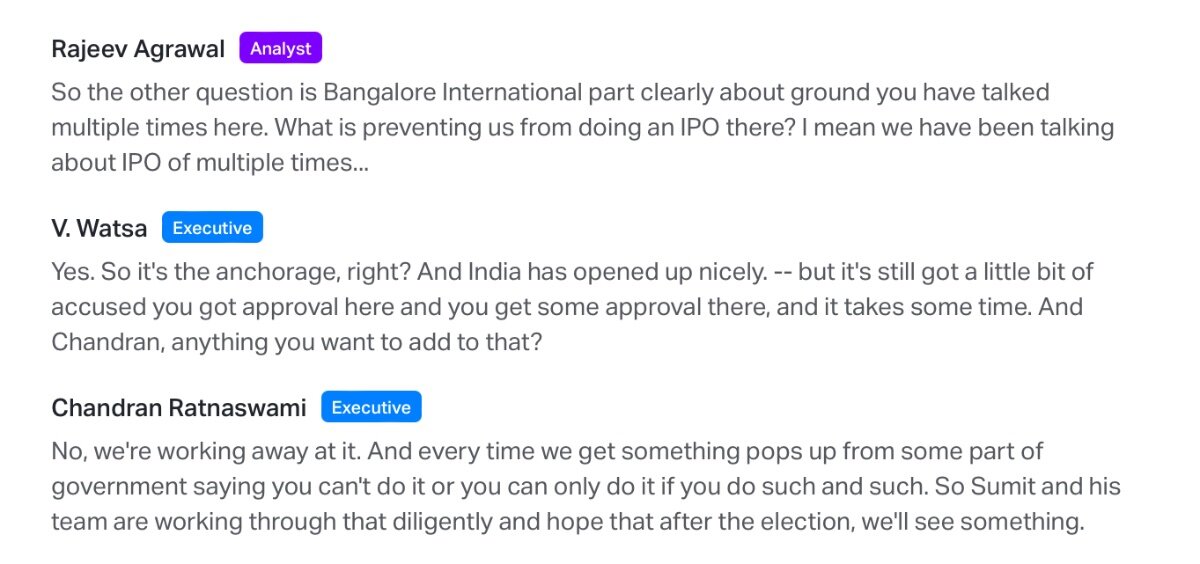

Thanks for sharing. My impression of the call is that Indian analysts are definitely more engaged on Digit than NA analysts are on Fairfax!

-

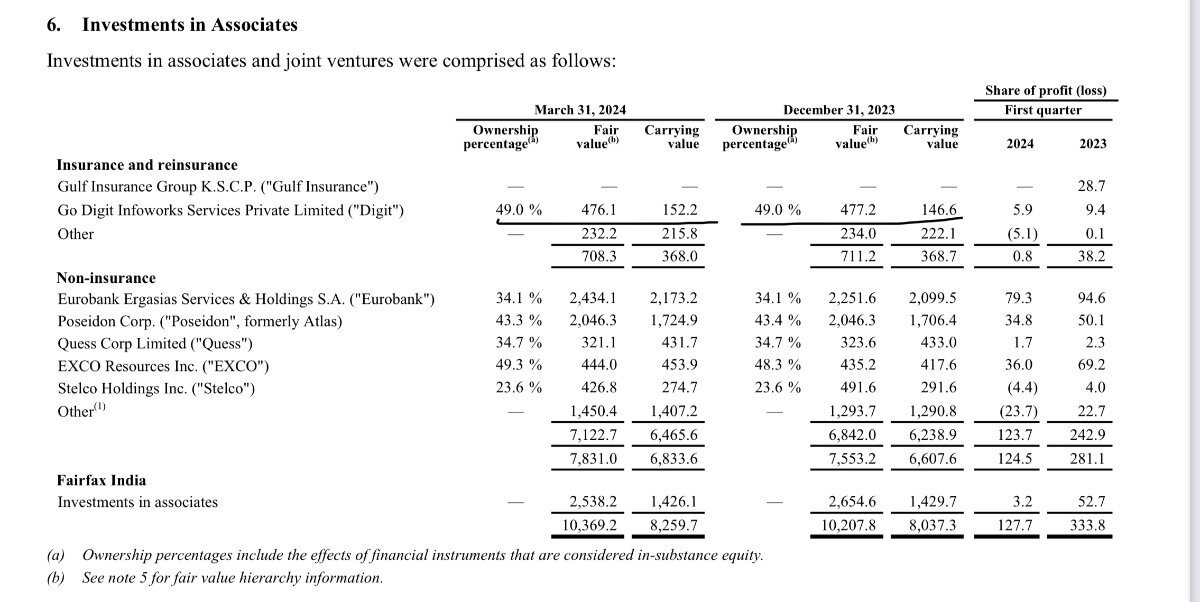

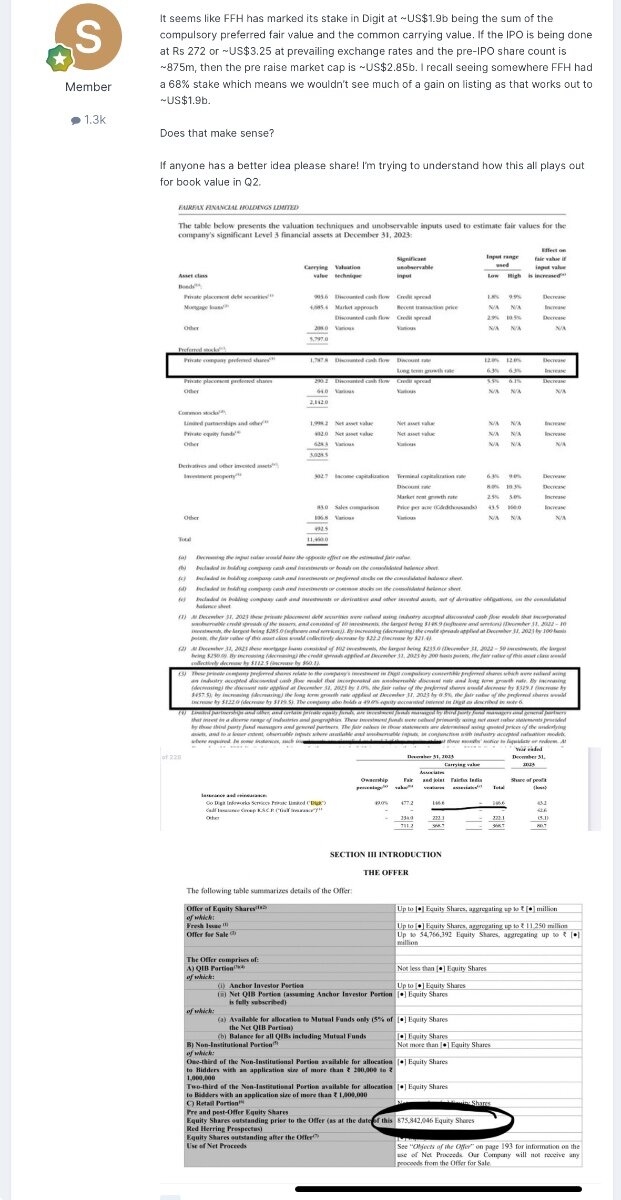

I used the pre-offering share count of 875m * 68% * Rs 272 / 83.5 to get an IPO valuation for FFH’s stake at ~1.938b which is where it’s marked. I don’t assume the stake changed so to value it now that would mean it’s worth $2.42b (i.e. up 25% from IPO at Rs 340 all else being equal). I don’t think they were allowed to mark up the equity but they wanted to reflect closer to what Digit was worth on the balance sheet so they used the preferred valuation to reflect it. Since they are compulsory preferred, I assume the thinking was it reflected the economic reality so useful to the users of financial statements.

-

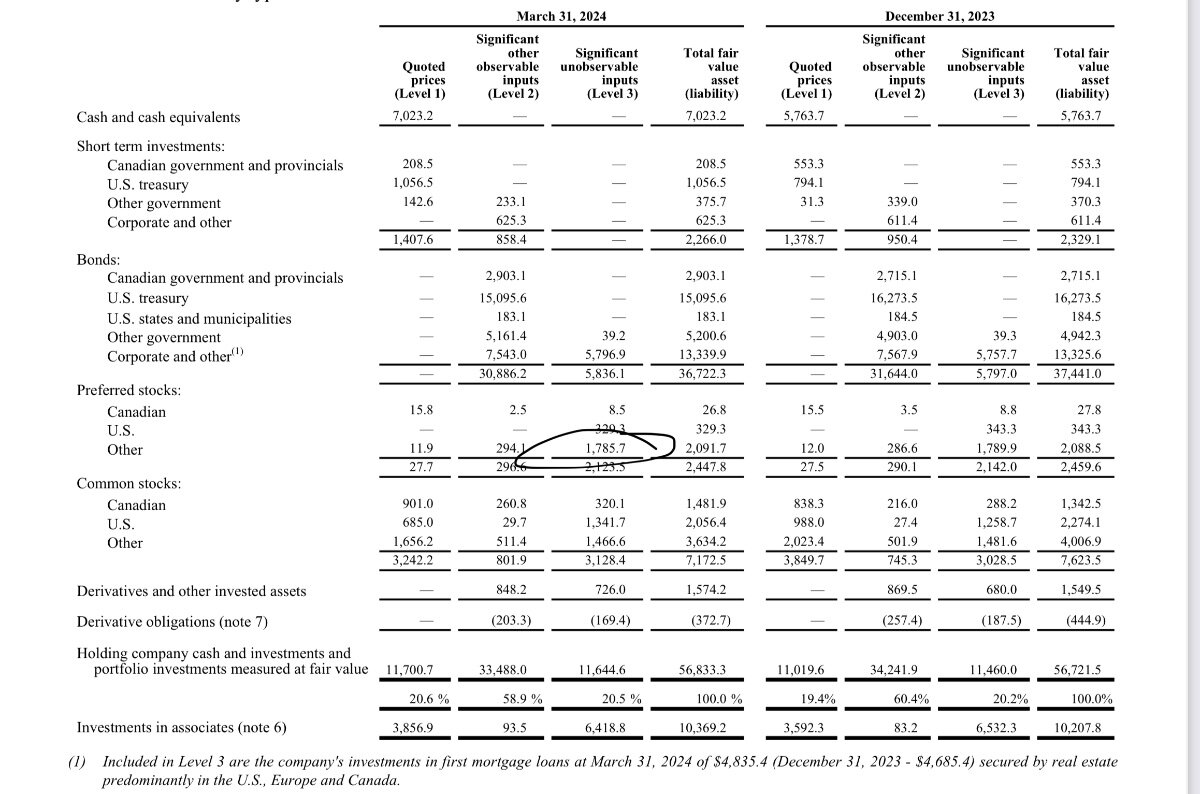

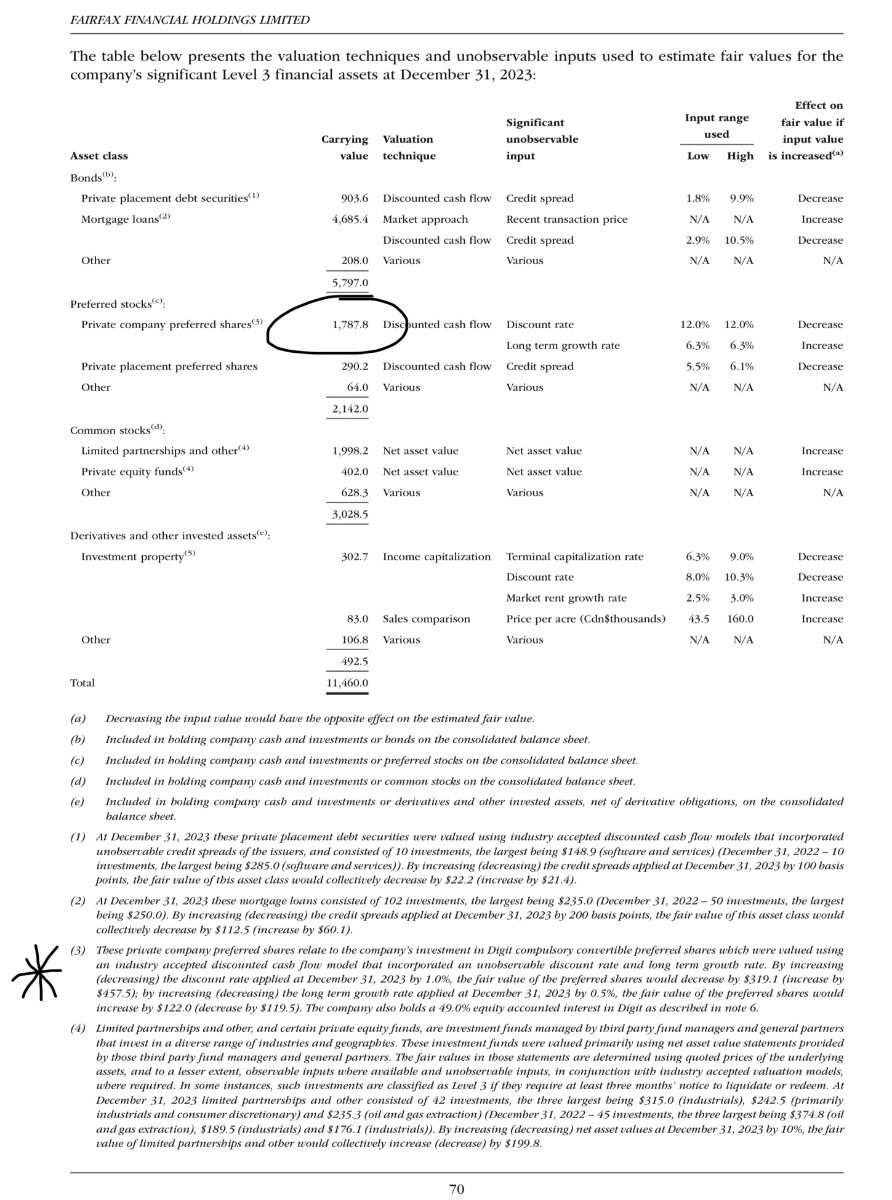

I think with Digit we have enough information to know where it was marked vs fair value. At YE23, if one takes the $2.265b FV for the entire position and deduct the $477m FV from the equity position disclosure it comes to the mark for the preferred ~$1.788b at year end. This means the whole position is marked at around $1.94b at the end of March which I think is pretty much the IPO price so I don’t expect a mark up on the IPO.

-

My assumption is that FIH would earn management and performance fees from the LP investors which would be worth more than zero. It’s certainly considered a negative from investors that FIH has to pay them to FFH, so presumably if FFH is paying fees to FIH, that will be a positive. I don’t have any idea if this is even being considered but I hope if they do it, it’s in a way that vastly reduces net fees that FIH pays. The exclusivity on investing outside of insurance in India for FFH is being valued negatively right now but if they do a deal like this, it would demonstrate its value.

-

I think it was me that raised that idea. Is your reason for not liking it because it’s complicated which in your opinion offsets the potential increase in intrinsic value?

-

Sounds transient. How big a dip below BV do you think is sustainable?

-

How much risk is there really in the swaps?

-

I got the impression at the AGM that the resistance is a negotiating tactic. I’m not sure how much is necessary to close the deal or if they have to make whole the previous sellers on a bump.

-

Terrific news, thanks for sharing. The stock seems to be trading above the tender price so I assume there will be a bump at some point. Did you see an expiry date on the offer?

-

I haven’t done it with Fairfax but I have with other companies. I usually contact IR or VP Corp Dev and ask them who their buyback broker is? I think for FFH it’s RBC or BMO.

-

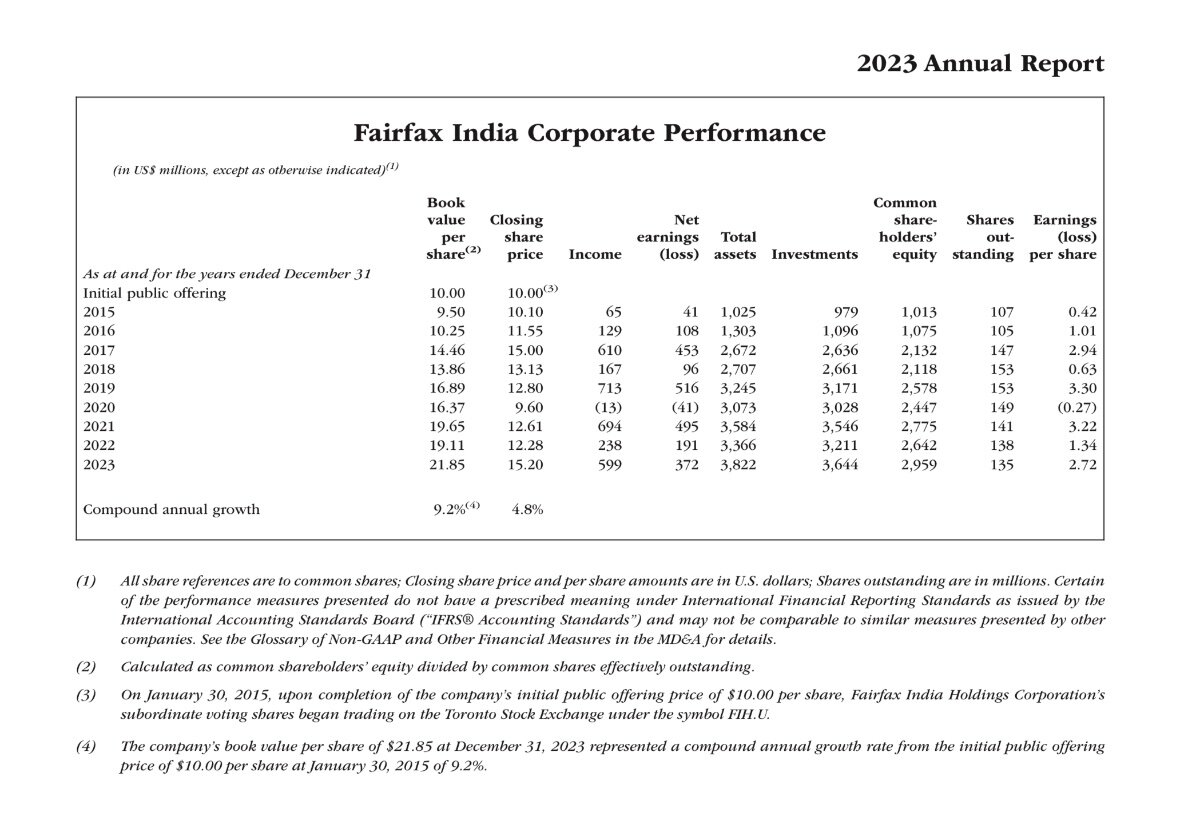

INDA started outperforming FIH when the NAV discount started expanding. It seems unlikely the discount grows significantly again from here although anything is possible. My key takeaway post FIH AGM was that the conclusion of the Indian election was a catalyst and the stock is now at its weakest point since the AGM. I can see two potential catalysts: 1) a transaction with respect to IDBI which will might highlight FIH’s value as the vehicle FFH is contractually required to use for any non-insurance Indian investments. Privatization is supposed to accelerate when the election is over even if they are unsuccessful on IDBI. Execution is a big risk but FIH might get lots of chances to swing. If they are successful, AUM could grow fast. It’s not clear how/if FIH shareholders would participate in the economics. 2) Traction on the Anchorage IPO. The recent DIGIT IPO was an interesting exercise. I can see how retail investors will be more excited about one of the best airports in the world than an insurance company they don’t understand. Between those two events, BV could be $28 in a short period of time, public assets could be the vast majority of investments held and the fees paid might be mitigated by fees earned from investments managed by FIH on behalf of outside investors. I have a long term view but I think the odds on these catalysts in the next 12 months is pretty high. For those with meaningful positions who want to liquidate, please call the company and cross the shares with the buyback.

-

All good points but it’s the EPS per share of $5+/quarter and growing that I really appreciate. Analysts for the most part expect Associates income to be flat or down. This increases the carrying value so effectively are the only gains FFH gets to include in book value.

-

This is what I came up with but I’m not 100% sure.

-

I assume we’ll see an increase in fair value over carrying value but for the most part investors don’t care about that yet.

-

The actual ceremony was very dramatic! A few songs (including the Indian national anthem), lots of speeches and a candle lighting ceremony. The replay is available in the link below.

-

I guess they don't think of it as quality which makes sense. It will be interesting if they are patient on buying quality and then sitting on their hands.

-

I think they are trying to get the buybacks in before FFH goes in the 60. It would be surprising if that didn’t bring along some multiple expansion especially when FFH passes IFC in benchmark weight.

-

I had the exact opposite take. My guess is odds are better than 50% it happens in the next 12 months. Perhaps a few other things too as the election seems to be a catalyst. The below is from the AGM transcript.

-

Q124 showed only $34.8m of income from Poseidon and that’s much closer to 43% of Q423 reported income (just eyeballing the difference between 2023FS and Q323 reported income). I assume the same is true for Eurobank which doesn’t report Q1 until next week and Helios which also hasn’t reported Q1 yet.

-

The higher the multiple is the better.