SafetyinNumbers

-

Posts

1,622 -

Joined

-

Last visited

-

Days Won

7

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

My biggest add in the past 3 months is SCR.TO or Strathcona Resources. It’s buy and hold investment in oil which most people aren’t comfortable with but this is a growth and capital return story with top of class management. If you have a spare 48 minutes I suggest watching Adam Waterous present at the SCR Investor Day on Nov 14. The stock gapped up that day and has since pulled back below to where it started as oil markets have been a bit squishy and everything else was going up faster. https://www.strathconaresources.com/investors/#presentations

-

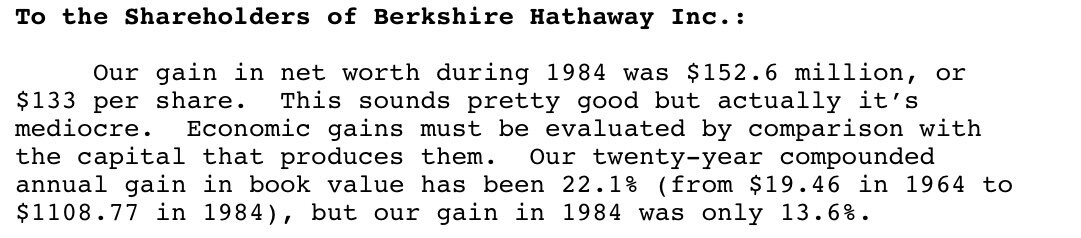

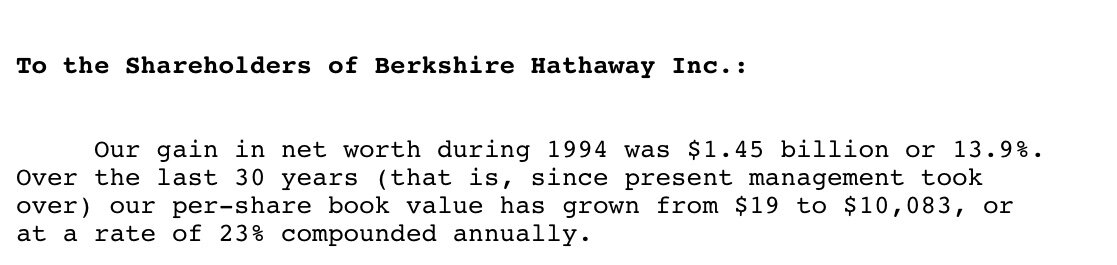

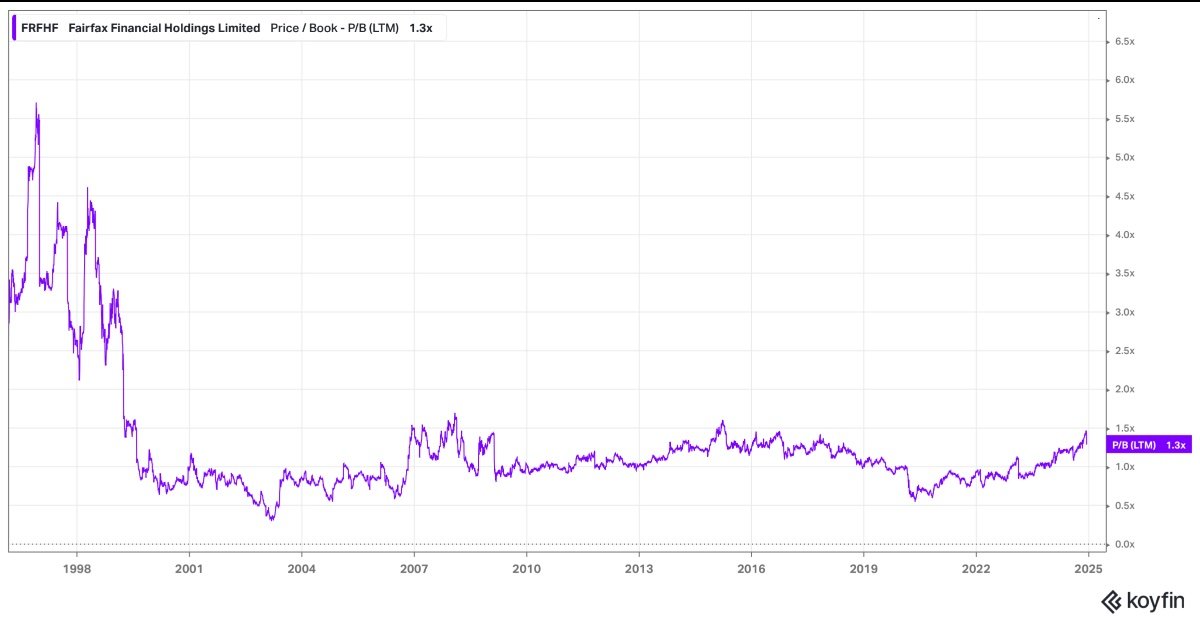

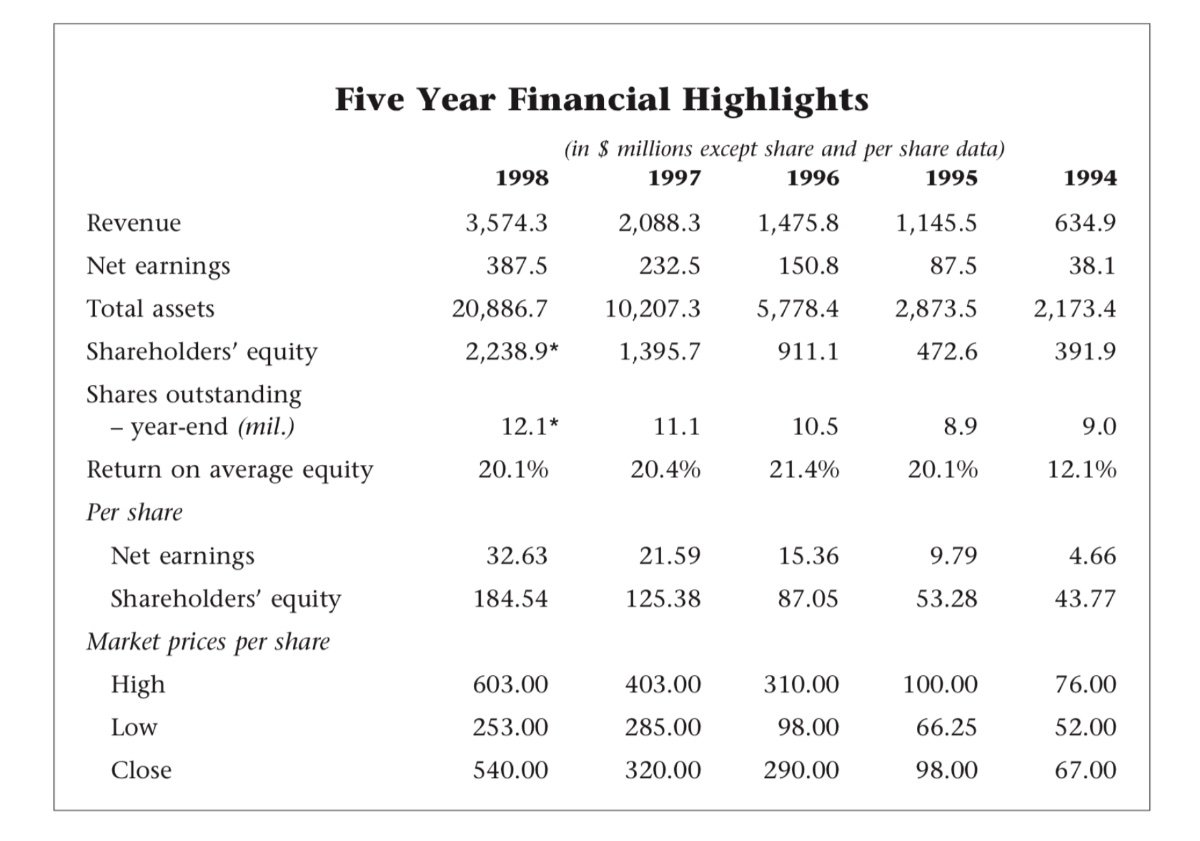

Thanks for sharing! I love these analogs because it opens my mind up to right tail potential. 1984-1994 is where a lot of the magic happened. BRK’s BV went from ~$1100 to ~$10000 or a ~25% CAGR and the multiple went from ~1.35x to ~2x. Combined that was a ~30% CAGR. Since then it’s been closer to ~12% which is still great but well below most quality investors hurdle rates. Fairfax is a lot bigger than BRK was in 1984 and is actually a lot closer to BRK’s size (market cap) at the end of 1994 but given the set up, it’s not out of the realm of possibility that FFH can match that decade over the next decade. My hurdle rate is 10% so to have that right tail potential with margin of safety is very compelling to me.

-

Very true. FFH has a much better set up that the companies ahead of it because it’s base ROE is very high as @dartmonkey highlighted and because it can surprise to the upside given the various right tails in the equity portfolio (BIAL, EUROB, KI etc…) and the optionality of the fixed income portfolio. The probability of FFH averaging >15% ROE over the next 5 years has to be very high. The true over/under on average ROE for the next 5 years is probably closer to 17.5%.

-

Very few stocks available that benefit from higher rates, a stronger USD and a sell off in quality stocks. FFH price might go down with it in the short term (as holders either need liquidity or think they are switching into something cheaper) but expected forward ROE is probably going up. It also looks there is a plan to IPO Ki. I don’t know it well but it seems like BX has 80% of the equity (Class B & C) but there are different classes with different rights. The Class C appear to be cheap leverage with an 8% preferred return that gets repaid at the listing price meaning they may result in a big increase in Brit/FFH’s equity stake. These are like OMERS shares in Brit which appear to be 6% and understated FFH’s economics. Ki might attract a very healthy multiple to book value and/or premiums given the nature of company (fast growth/AI) and the players (BX). Ki will likely do north of $1b in annual premiums soon so it could be material to FV over CV if it lists at 5-10x premiums. Ki Articles of Incorporation 9.23.20.pdf

-

I think FFH was mentioned in passing so I will go with my second biggest position Mako Mining MKO.V MAKOF. Mako is a gold producer trading < 3x OpCF and <1x 2028 OpCF. They are taking the FCF and investing it in exploration and building a new mine in Guyana. Gold companies are the furthest thing from quality but they enjoy enormous right tails given that the gold price also enjoys enormous right tail potential. I oversized Mako because I’m a big fan of the management team and the controlling shareholder Wexford Capital. Wexford also created Diamondback Energy (they like animal names) in 2007 and took it public in 2012 as their oil play. Since then it’s compounded at ~24%. Mako is their gold play and the cycle is just beginning. In full disclosure, I’m on the board of Sailfish Royalty FISH.V which spun out of Mako a few years ago and has a royalty/stream on Mako’s project in Nicaragua. FISH is also controlled by Wexford. I’m excited to see how Mako can compound over the next 5-10 years as every time the deal it will be accretive. The risk of course is on execution and geopolitical which is true for any gold stock.

-

Looks like Northbridge is putting up most of the cash for the buyout. I bought some at 7.5 cents when the deal was announced. Seemed like a low risk arb.

-

Looks like they made 6% on this one.

-

I agree but I did think this financing was more expensive. Happy to be wrong.

-

It’s interesting. Unless I did the math wrong, so far the dividends received by OMERS until the end of Q224 were ~19% of their initial investment and with the gain a total of ~21%. So not a huge return over 40 months. It’s possible there was also another dividend in the past 5 months which would add to it.

-

This Company Will Get Sold Thesis

SafetyinNumbers replied to spartansaver's topic in General Discussion

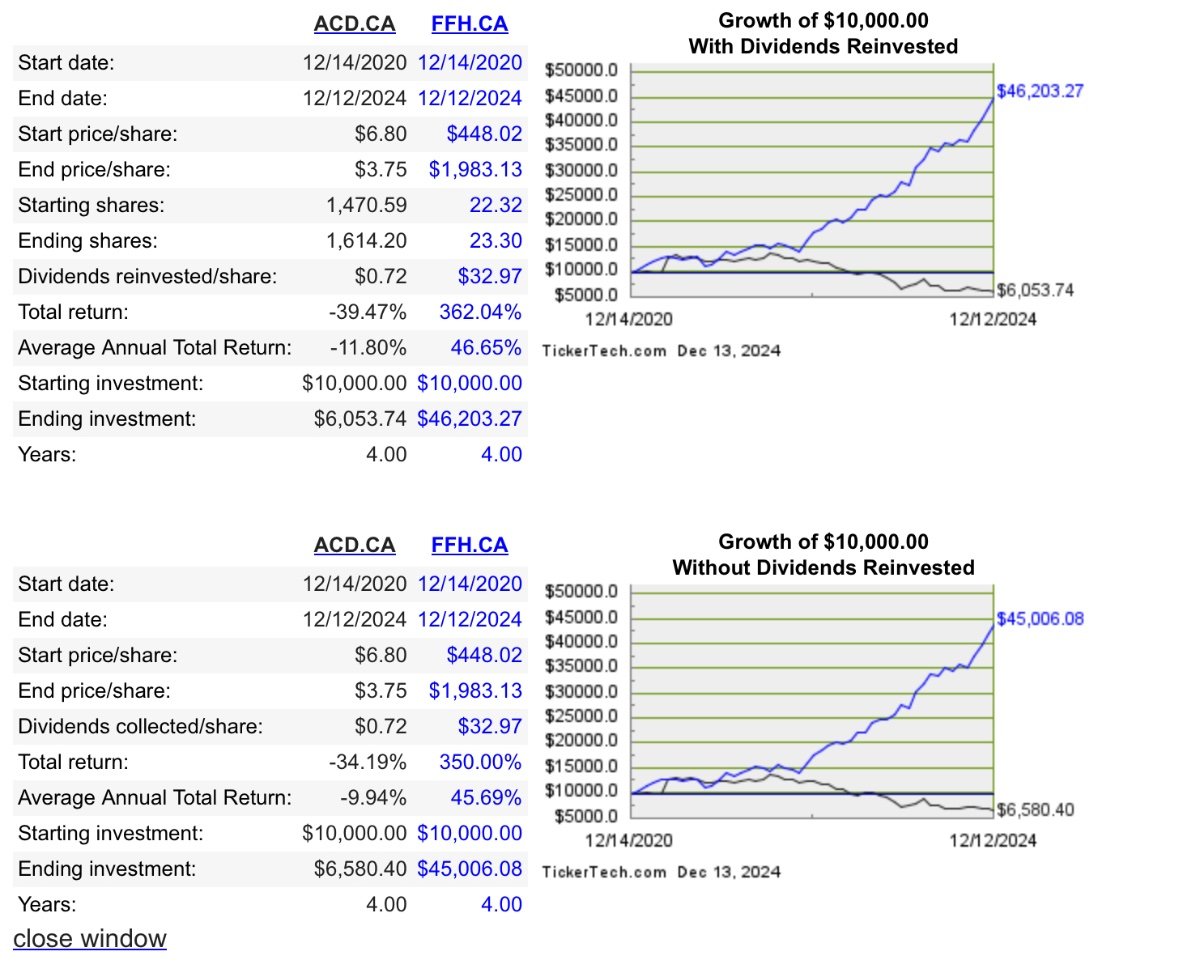

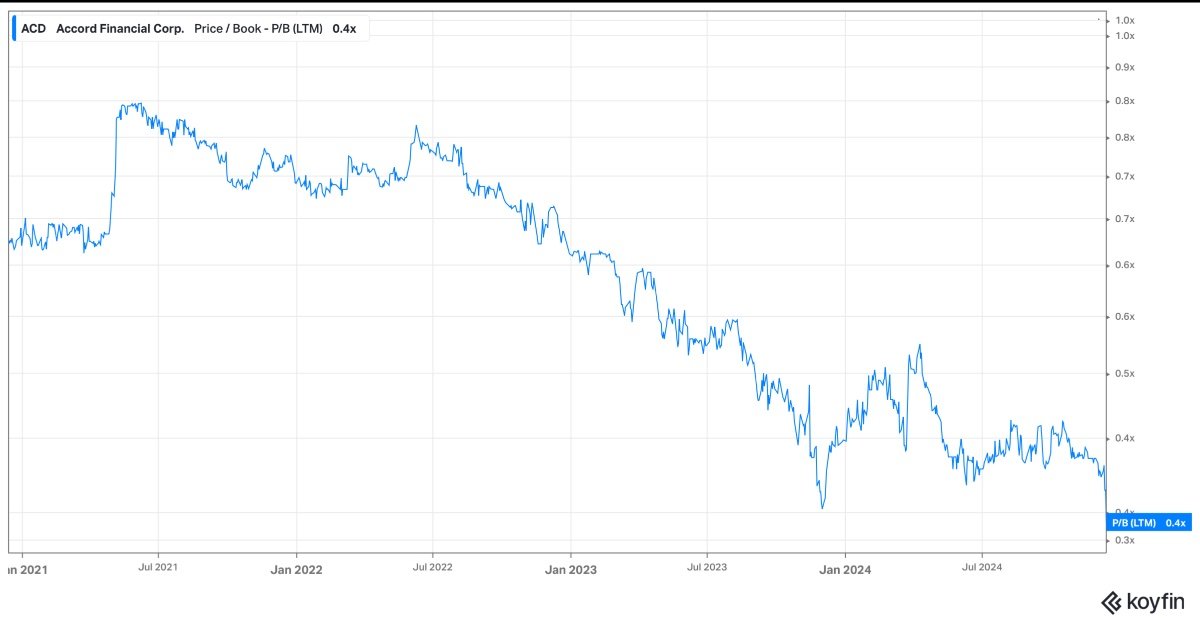

I bought some TTEC recently. CEO owns over 50% and is bidding for balance at $6.85. Company formed a special committee at the end of October so nothing has gone definitive and there might be financing risk. Usually one would expect a bump in these cases but the market is acting like there is no deal. It’s <1% position. I also think Accord Financial (ACD.TO) gets sold in the next 10 months. The market cap is < C$35m so very illiquid. The company has publicly stated it’s looking at strategic alternatives. It’s a lending business with 4 divisions remaining after selling the Chicago business a few months ago. I believe they want to hold onto the small business lending company in Vancouver and are combining the two asset backed lending businesses in Montreal and South Carolina. That leaves BondIt the LA based media finance business. It’s hard to sell because the BondIt management need to ok the buyers but I know they have been trying for a while. My timeline of 10 months is because they have a debenture due in Jan 2026 that they have already extended once. While they may be able to extend again at some cost, I don’t think they want to. The CEO’s and Chairman’s families and friends own the debentures as well as around 25% of the company each. In full disclosure, I own >2% of the company and have been adding some almost every day on what I assume is tax loss selling but there can always be information asymmetry with such a small company. Management tells me they have been restricted for over a year which is why they haven’t bought any but ultimately it’s a lending business so there is always balance sheet risk i.e. risk of a zero. I got long because it was obvious the business needed to be sold because its cost of capital is too high and private credit was exploding so there were lots of buyers. Usually my biggest investing mistakes have been because management didn’t make logical decisions for reasons I didn’t understand. In this case, I think the CEO wanted to sell for a big price instead of a fair price so he destroyed a lot of value trying to get scale and he didn’t appreciate that his cost of capital was going to keep going up. He assumed the stock would go back to trading at a premium to book and he was wrong. On top of that the profitability of the business was squeezed. My interpretation of events is a lot of me filling in gaps making assumptions how a reasonable board would act. I’ve had a chance to meet many of them over the years at the AGMs and plenty of interactions with the CEO and Chairman as I mentioned above. I think that along with my experience at UBS and an investor for 20 years gives me an informed interpretation but I’m wrong a third of the time and I have been wrong here so far. The entire loss for me so far has been multiple contraction but the opportunity cost has been huge. I could have owned more FFH instead!

-

Great point. Another way, FFH defers taxes besides deferring gains is by being aggressive on reserving. I think the next four years could be really interesting on reserve releases since those reserves are bigger when in a hard market but get released after four years if there are no unfavourable developments.

-

Fairfax is Canadian and I don’t think moving to the US is something Prem wants to do. I’m not advocating for the 60 add. It’s just something that’s going to happen.

-

I think that’s right, the key is the high quality insurance operations although I still find investors who don’t think FFH has high quality insurance businesses. It’s worth searching Buffett and float on YouTube. Lots of great clips from the AGMs over the years.

-

I think we can estimate float off of the quarterly balance sheet by taking insurance liabilities less reinsurance assets held. That was ~$39b at the end of Q3, up from ~$35b at end of 2023. On the float value, I agree with Buffett.

-

Using expensive paper helps with margin of safety, no question.

-

I’m curious when you did the exercise did you factor in the related float and how much the earnings were from that? I’m curious what the total return has been so far.

-

So he should have known better based on what he knew at the time and still went ahead?

-

You didn’t ask me but that has never stopped me before. I think this is a question that’s really about estimating intrinsic value. I use three methods to triangulate FFH’s intrinsic value range. 1. Normalized PE. 15x is generally considered a fair market multiple and FFH is a better than average business so 15x FTM EPS seems reasonable. While consensus is $155, it’s probably too low, it still gives us $2325 or ~66% above current prices around $1400. 2. Relative P/B multiple. There is an exponential relationship between P/B and ROE which makes sense. A high ROE compounds much faster so it makes sense to pay more than 2x for a 20% ROE vs a 10%. When looking at FFH peers, an ROE between 15-20% should command a P/B closer to 2.5x. With so much in the multiple we can just use trailing BV instead of making the adjustments to FV etc. 2.5x BV is ~$2585. 3. Buffett method. This is the sum of BVPS and float per share. Buffett has made it pretty clear that float in the hands of a high quality insurer is worth at least the amount of the float. This makes sense because the income associated with the float accrues to the insurer and consistently grows over time. For FFH this is ~$2800. That leaves me with an IV range of $2325-2800 which is wide but well above the current price offering large margin of safety.

-

It’s a pretty bifurcated market. Parts are inflated and parts are depressed. Although most people can never buy the depressed parts because of heuristics.

-

Perhaps they are considering an IPO if the valuations are favourable at some point?

-

This is resulting though isn’t it? Buffett issued expensive stock to buy Gen Re and clearly expected a better result than what he got. Execution is the hardest part of probabilistic investing. Everything I buy is clearly cheap if the companies execute as expected but about a third of the time they don’t. Thankfully the winners more than offset the losers over time (at least so far).

-

The 20% ROE for four years straight in the late 90s for FFH and BRK’s returns were based on very strong equity markets. That’s not the case for FFH right now. It has much higher earnings consistency now than it ever has because the float to equity ratio is so high and the insurance business so profitable. May/e we can’t achieve multiples like other high return insurance companies like KNSL or RLI because our earnings are too volatile but if the conditions ever existed to do it, it’s over the next 5 years. I’m not sure what the odds are but it’s better than none.

-

I’m not in accumulation mode. It’s 45% of my portfolio. I don’t want to keep adding but it keeps getting better and giving me chances. I’m also trying to encourage others to take a look and to appreciate the right tails and not assume that the risk/reward is not favourable to consider starting a position at this price. That being said maybe Parsad will be right and the forward return won’t meet their hurdle rate. My hurdle is only 10% so I have more margin of safety. I remembered the high end of the P/B being 6x on this chart but I think I rounded up. I didn’t pick a fantastic number for the sake of it. I based it on history. I’m not saying it’s going to happen again but I am saying it can. Which is why my sell criteria is growth based and not valuation based but I concede it will get difficult to hold on if multiples do start going north of where I’m comfortable adding if I didn’t own any but I’m certainly not going to complain about it.

-

All good points. Most market participants think markets are efficient. Premium analysis is used by investment banks and their corporate clients to justify the sale of a company well below intrinsic value. Companies also use overvalued paper often to raise cash or to buy companies. AOL/Time Warner is a classic example. FFH did the same thing Berkshire in the late 90s. They bought struggling insurance companies with high combined ratios and large floats by issuing equity. The shares outstanding went up by more than a third and more than half of book value growth was from issuing shares at a premium to growth. if we are business owners or if we are investors, why wouldn’t we want that to happen again?

-

That’s fine and maybe we all should even though it might be on its way to 6x BV. As Parsad said, the goal is to grow intrinsic value and it grows faster if issuing equity well above intrinsic value or if doing accretive things with the proceeds. Prem’s not selling and the company will be worth more if they take these actions. I just don’t understand why anyone would be disappointed if the multiple went up a lot from here but you both seem to be.