Graham Osborn

-

Posts

350 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by Graham Osborn

-

Berkshire Annual Meeting 2017 - Live Stream Discussion

Graham Osborn replied to Graham Osborn's topic in Berkshire Hathaway

Just some random impressions/ highlights from my trip this far: - I came to OMA from ATL. The flight attendant there was shocked at how many people "just happened" to want to go to Omaha for Cinco de Mayo weekend. - A lady I met on the plane had just moved to Omaha and had never heard of Berkshire/ was also astonished at how packed the plane was (I did get kicked out of my seat by a mom and her screaming kids, but they gave me a $100 voucher so I didn't raise hell like that United passenger). I was nice and gave her an extra ticket. - My Uber driver from the hotel had a son who used to work in Ajit's division but wanted to manage money. Buffett refused, so he went and started his own PE fund which is based here in Omaha. - I took a stroll by Borsheim's. I asked whether Munger would be signing purchase slips this year but apparently Buffett does it himself now. The kicker - Sunday only, and your purchase must be 100K or more. The "Buffett signature" pearls didn't look quite THAT attractive to me. - I swung by Kiewit Plaza. Talk about a nondescript part of town in the middle of a dust bowl. I thought I might catch anthrax from a rotting cow or get steamrolled by a tumbleweed walking down Farnam Street. - I went to Whitney Tilson and Chuck Gillman's party at the Hilton for the first time this year. A credit to both of these guys for creating a community here that would otherwise exist only in the clouds. My one suggestion - do we really need so many Snicker's bars? - I overslept this morning in usual and arrived 15 min before the meeting after getting locked out of my Quality Inn hotel room twice. At least this year I got a seat (all the way at the back) vs sitting on the stairs last year. Finally moving up in the world! -

Berkshire Annual Meeting 2017 - Live Stream Discussion

Graham Osborn replied to Graham Osborn's topic in Berkshire Hathaway

Sorry, I didn't want to poison the well early - Trump. -

Since the other thread was more logistics-related I wanted to kick off a thread like we had last year to discuss the content of the meeting in real time. Some much to discuss, from AIG to the T-word to property-casualty tightening!

-

Do you have a short (1 para) investment case for EBN.V? No I'm actually long. I'm aware of the historical short thesis but I don't agree. I actually like the stock very much. I haven't been shorting much lately but I would only short a large cap - regardless of your views shorting a microcap is really risky.

-

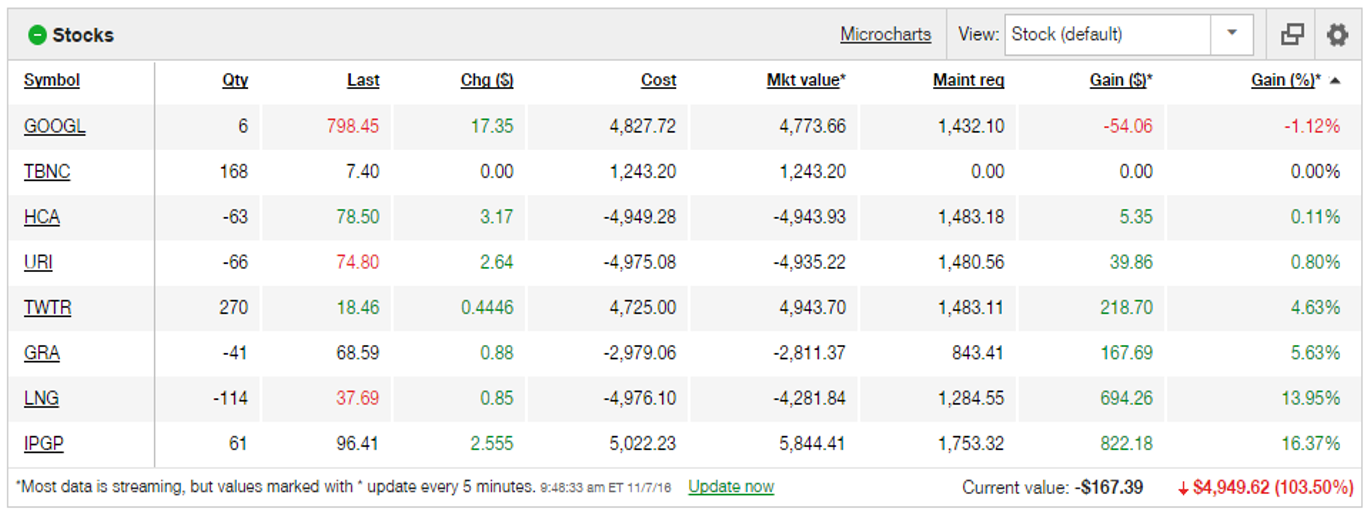

Currently: CTSH SAFM USNU SMCI EBN.V IPGP GOOGL SRMC AGN (short) IEHC PHO.V

-

OK guys, way to spoil it for the rest of us. It's like watching the pope from St. Peter's square vs on TV - not quite the same. The trip ain't exactly cheap, but it's cheaper than just about other annual meeting you might go to if you're willing to book a discount airline and hotel 15 minutes away from downtown.

-

I'll be there (year #2). Anyone want to form a COBAF seating section on Saturday? Last year a number of us were posting live commentary from the meeting.

-

We could debate the discount rate, but it isn't really the point of the calculation. I think we can agree a discount rate of 15% is above average. The general trend of the graph would actually be accentuated if you had lower discount rates some years. If you want to adjust that in the spreadsheet to what you think it should be I'd certainly be interested to view the result.

-

People often phrase EMH as "all the info is already priced in," meaning TRs like Buffett's are a statistical anamoly. Of course not everyone thinks this since EMH is really a spectrum of theories depending on input parameters. But the concept is that intrinsic value can logically and consistently increase even in a world of perfect foresight re cash flows.

-

In case anyone finds this interesting, I did a simulation illustrating why Buffett defies the efficient market hypothesis. Even if one knew the future free cash flows of Company X precisely, the intrinsic value of the company according to a DCF analysis fluctuates over time. Therefore, if one buys a company where the future free cash flows can be predicted to increase for a number of years, the stock should rise significantly over the coming years even when all information has been discounted, as the graph shows. One can also see that once FCF stops growing, intrinsic value will stop growing as well. The decline in intrinsic value shown here would only happen if the company started dying, which many companies do sooner or later if they are too big to be acquired. DCF_simulation.xlsx

-

Aye, therein lies the rub. Even if you could/ can predict the outcome of elections, I'm not sure what the relevance would be to market participants. By reflexivity, the only absolute truths are unactionable (at least from a profitability standpoint). This is one reason I think there might be predictive value to SOME test, even if not this one. Clearly, using such a test as a basis for trading would have been poorly advised if you simultaneously subscribed to the second incorrect prognostication, i.e. that Trump would crack the indices.

-

Not if you only test 1 indicator (as opposed to data mining). In this case the probability of the indicator agreeing with the results by chance is about 6%. On the face of it one would think that this should be more correlated with the popular than the electoral vote, but it's actually more nuanced than that if you start thinking about the many drivers behind search selection and search intensity. While electoral models are more complex/ nuanced they also tend to be riddled with false assumptions. For fun, we'll give it another try on some other upcoming international elections.

-

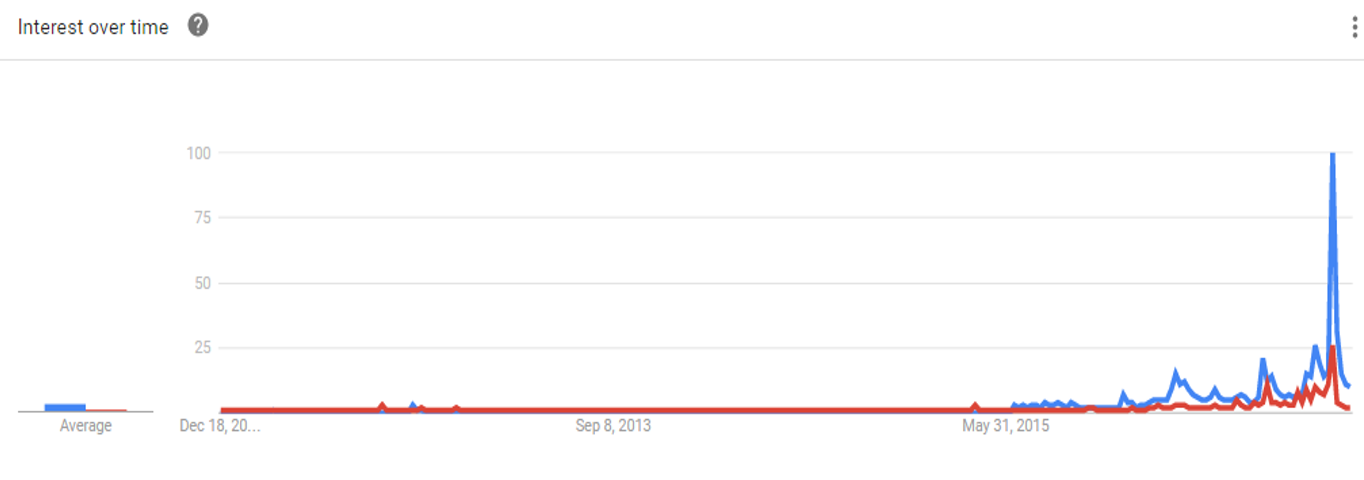

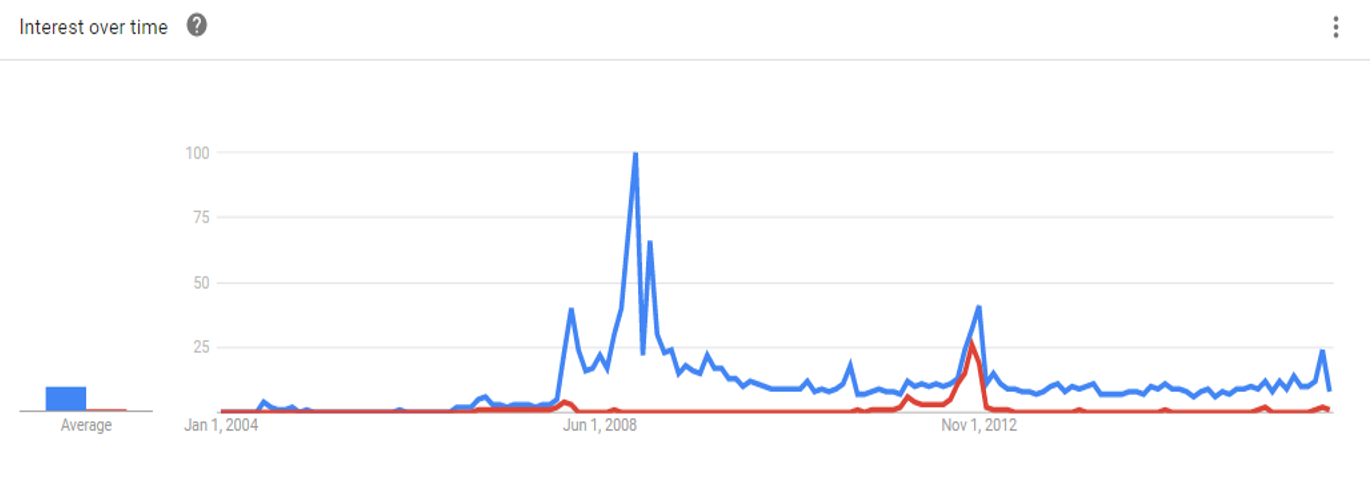

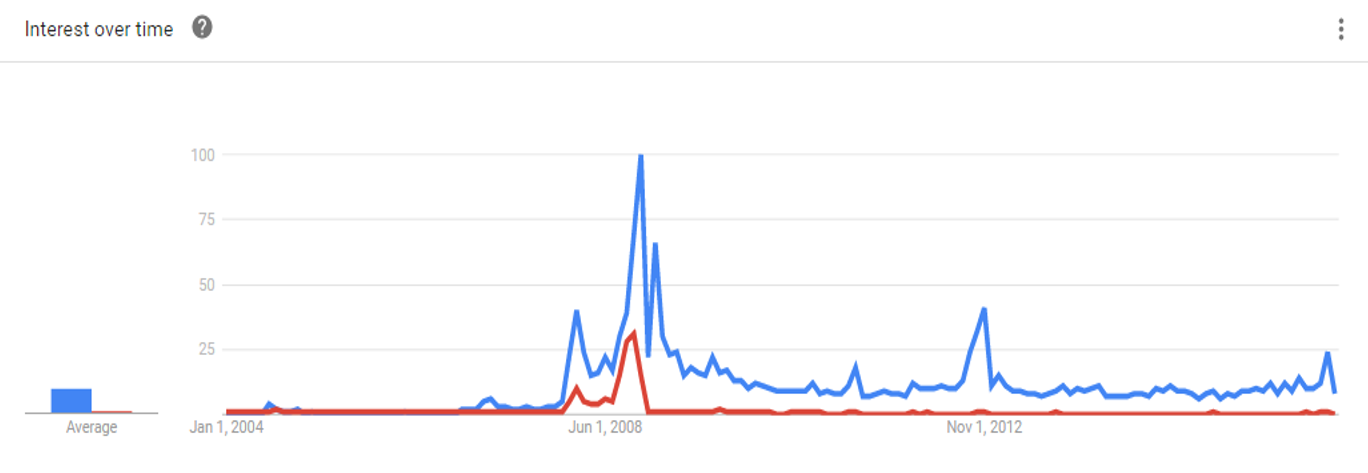

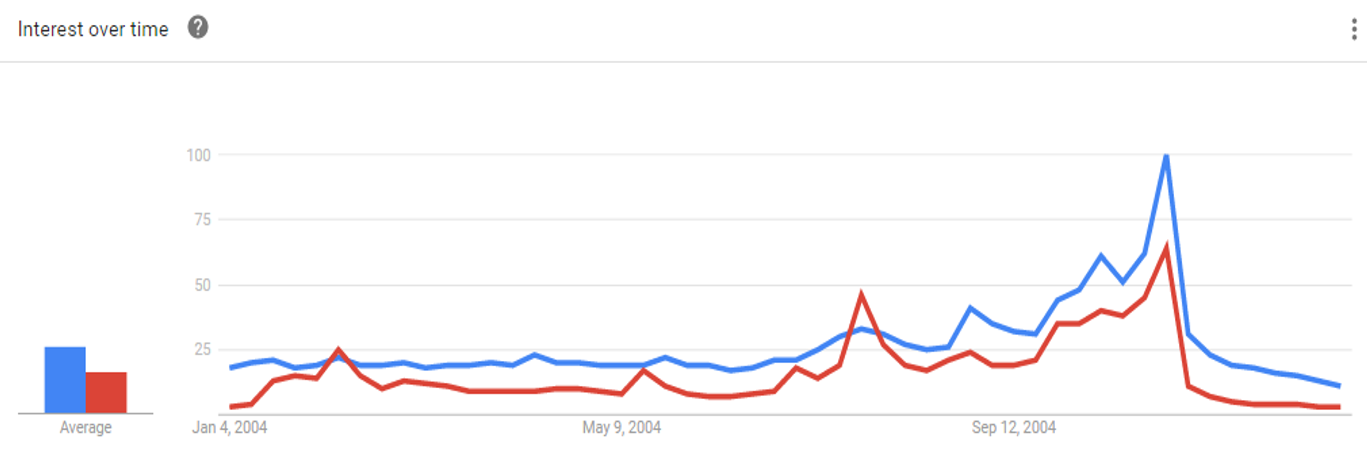

It's funny how given all the polls and meta-polls conducted prior to the election, noone ran a simple Google Trends search of "Trump" vs "Clinton." The outcome was clear for months in advance (see attachment 1). This pattern also held for "Obama" vs "Romney" in 2012 (see attachment 2) and for "Obama" vs "McCain" in 2008 (attachment 3) and "Bush" vs "Kerry" in 2004 (attachment 4). The last comparison, I concede, could be confounded by other meanings of the word "bush."

-

Ray Dalio on the Future of Monetary Policy

Graham Osborn replied to ni-co's topic in General Discussion

Just wanted to repost this: https://www.linkedin.com/pulse/reflections-trump-presidency-one-week-after-election-ray-dalio?trk=eml-b2_content_ecosystem_digest-hero-22-null&midToken=AQHZPFDtyrSUUw&fromEmail=fromEmail&ut=0x4FnqDgcveDw1 Ray's views on a post-Trump world. If anyone has seen anything more extensive out of Bridgewater please post as well. -

List of businesses that can be run by idiots

Graham Osborn replied to randallchsu's topic in General Discussion

+1. Buffett's view while attractive is hard to build a consistent case for. In particular, a high-margin low-capital business like KO or See's or DVA is just so darn tempting to lever up. So I would say that a great CEO can't make a great business out of one with unfavorable economics, but a poor CEO can definitely screw up a business with great economics. Then you need a new CEO (and new investors) to come in and clean up :) For sure that even a great business will no do as well under a poor CEO as it would under a good one. The difference is that a great business can be put back on track when a new CEO comes in to clean up the mess. For a mediocre business a poor CEO is a life threatening event. Either way, unless your holding period is "forever" and/ or you're buying whole businesses to turn them around, you're probably still going to lose money on the investment. But yes - if you buy a great franchise after the mismanagement phase has runs its course and have a compelling case for a turnaround, go for it. -

List of businesses that can be run by idiots

Graham Osborn replied to randallchsu's topic in General Discussion

+1. Buffett's view while attractive is hard to build a consistent case for. In particular, a high-margin low-capital business like KO or See's or DVA is just so darn tempting to lever up. So I would say that a great CEO can't make a great business out of one with unfavorable economics, but a poor CEO can definitely screw up a business with great economics. Then you need a new CEO (and new investors) to come in and clean up :). As an owner, Buffett controls all the capital allocation decisions, hence you don't see rabid empire-building. -

My neither. And I just shorted HCA. Should have shorted CYH but I had refrigerator blindness on that one. If this portfolio is representative of what he is doing in aggregate, his investment philosophy seems to have departed from the kind of conservatism he championed in the early and pre-Scion days. But if so, he wouldn't be the only one - DVA which is a major BRK holding is thematically similar to DVA. There is something about being in a depression that causes great investment minds to make serious mistakes - Graham buying stocks on margin in the early Depression being a prime example.

-

Given the reported voting tendencies on the board, I would imagine many of posters on this thread were confident of a Clinton victory 1 week ago. And many of them were probably equally confident that the market would react negatively to a Trump victory. These same speculators now have Trump's economic plan and its consequences worked out to 3rd order. It's always hard for people to admit that they don't have a clue what's going to happen - but doing so is critical to generating good risk-adjusted returns. I prophecy: 1. The market could go up a lot. 2. The market could go down a lot. 3. The market might not do a damn thing. My portfolio and I will be equally happy with any of these scenarios. If I were long-only, yes, I would probably have a sizable cash cushion - but that would have been true for most of the past 15 years.

-

Here's my updates as of today: This model portfolio is +12%ish since July 1 when I started it - whatever that means lol. This apparent good luck may be short-lived, but the Sharpe ratio seem OK and it seems insulated against a range of wacky central-bank scenarios. We'll see. I hope to have the opportunity to liquidate the majority of my external options portfolio (which is far more volatile) and beef this portfolio up to ~20 positions in the next few months. No longer appearing here is AGN which I covered at my target and GBX which I sold at a small loss since the technical picture seemed to have changed. PS: covered HCA a few minutes after entering the trade, going to wait.

-

Lol, a silly question deserves a silly answer. It's not a question of hedging, but rather of whether your portfolio's success should hinge on the outcome of an election (or any other "dramatic" event).

-

Since I tried to emulate Buffett's "50%" strategy last year I can say that it is not amenable to conditions of anemic GDP growth (as opposed to the 1950s). There are guys like Lazarus over on the Silicon Investor value thread who may well be doing 30-50% some years, but you need to be willing to diversify and stomach some real short-term pain to use this strategy. I believe Buffett could have succeeded at it today, but he would not have had 50% returns and would probably have had some big losing years as well. Quantum used leverage and exceeded Buffett's TR (they were doing 100% some years) but again, they were abetted by the tremendous bull market in equities since the 1950s. I've made a personal decision not to shoot for the stars with microcap investing if I can get maybe 20% with better liquidity. We are currently at the start of a depression anesthetized with QE, and I have zero interest in being long-only in a bunch of illiquid microcaps when the specter of rampant inflation rears its ugly head. When the average PE of the market is say 5-10, I will certainly give due consideration to Buffett's method. OT: This certainly won't be the first time I've thumbed my nose at Buffett, or more accurately Ted Weschler. I'm currently looking at shorting DVA, which is a major BRK holding and apparently hand-picked by Ted. And I'm short GRA, which Ted helped turn around. The thought of that idiot running a significant chunk of BRK's investment portfolio makes my blood curdle. He apparently has no fear of leverage.

-

Ray Dalio on the Future of Monetary Policy

Graham Osborn replied to ni-co's topic in General Discussion

Is it just me or does Trump's 1T infrastructure spending plan sound an awful lot like monetization? -

Imagine if you had done that in Japan around 1990. The basic premise of indexing is you diversify away single-security risk, enabling sector or market performance to shine through. Buying sector indices without due sector analysis is incredibly dumb; buying market indices without market analysis is less dumb, but still dumb. The reason is that no trend lasts forever - virtually all systems exhibit periodicity at some point. This applies to what the S&P has done over the past 100 years. Think about that - 3 generations of deeply ingrained belief that the trend will always be maintained. For such people only 3 things in life are guaranteed - death, taxes, and ultimately rising US equity markets. As other posters have noted, index funds get pumped up in mature bull markets, driving trillions into blue-chip favorites. That's one reasons outside of fundamentals I bought GOOGL a few months ago - I remembered what happened to MSFT in the late 90s thanks to the magic of indexing. And don't forget what happened with ETFs in October 2015. Funny how index funds can (and do) underperform their indices.

-

It depends on your strategy. For example, if the equities in your portfolio are highly levered, you can tolerate less margin. Illiquidity can function like leverage in some ways, hence the same is true of small cap/ microcap trading (most brokers already have speed bumps built in for this). I usually don't exceed 15-20% of equity - that is with low-leverage longs and generally high-leverage shorts roughly 50/50 (currently). Like credit card debt, it should be considered bad as a general rule. Lots of people lost 50% in 2008-9 with no margin.

-

I was just listening to Obama speaking in Nevada and was surprised to hear him say (essentially) that he fixed the economy after Bush destroyed it. In true Taleb spirit, I decided to measure the "return" for presidents bracketing the 4 biggest crashes of the last 100 years: Hoover/ March 4, 1929 – March 4, 1933/ 356-110 (-70%) Roosevelt/ March 4, 1933 – April 12, 1945/ 110-198 (25%) Nixon/ January 20, 1969 – August 9, 1974/ 686-342 (-50%) Ford/ August 9, 1974 – January 20, 1977/ 342-414 (21%) Clinton/ January 20, 1993 – January 20, 2001/ 730-1850 (153%) Bush/ January 20, 2001 – January 20, 2009/ 1850-927 (-50%) Bush/ January 20, 2001 – January 20, 2009/ 1850-927 (-50%) Obama/ January 20, 2009 – October 23, 2016/ 927-2141 (131%) It would seem that for presidents as for investors it's all about timing. If only Bush had gotten out a year earlier ;) Clinton gets the award for a well-timed exit.