Graham Osborn

-

Posts

350 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by Graham Osborn

-

Curious on your criteria for longs and for shorts. Of your picks, DVA on the face of it seems like the most compelling short candidate (although I admit KO is starting to look interesting fundamentally, not much technical weakness yet). Thoughts appreciated.

-

If you fail to establish a track record with a ~$100k portfolio you lose one year of your life? Please, keep things in perspective. If you're a full-time investor and you blow up you might have to sell your house, can't take care of your family, can't afford a retirement home and/or a good school for your children, just to name a few things. On the other hand, how your portfolio performs the next few years is mostly irrelevant in the greater scheme of things because the vast majority of your future net worth will come from labour, not capital. You can blow up $100k once or twice and still get a great job, your quality of life wouldn't be affected. You say you can 'earn it back quicker' after a blow up but a retiree can't earn it back at all. That's a great point. Stakes are way more important in investing especially when you are evaluating a portfolio manager. I wouldn't consider anyone who doesn't have his whole net worth in line for multiple years. Skills are way overrated and its hard to distinguish them from luck.I understand Buffet now when he says its easy to compound small amounts. Not because you can find more opportunities but the psychology starts to take over when stakes are raised.I would be extremely wealthy had my success in monopoly translated into real life. Great post. Amen.

-

TWTR ? Why? Here's a couple links: http://www.siliconinvestor.com/readmsg.aspx?msgid=30693403 (loop back for previous posts) http://www.cornerofberkshireandfairfax.ca/forum/investment-ideas/twtr-twitter-inc/90/

-

Guys, these are interesting discussions, but I recommend starting a new thread to organize them. Portfolios or updated portfolios are more relevant here. For me - added IPGP and TWTR in past week.

-

I don't know who you are or where you're coming from, and I assume the converse is true. But one of the biggest reasons Buffett got to where he is today is that he regarded his savings as more sacred than a retirement account from a very young age. True - young people have more room to make stupid decisions and still avoid working at Walmart into their 70s (theoretically). But there is a real opportunity cost to each and every blunder - namely the age at which you retire. Buffett was a self-proclaimed retiree in his early 20s. It's more about mindset than chronological age. Whether you are a laborer or a capitalist is a personal decision, but poor risk management will forever confine you to the former category. But I digress. Let's return to the thread topic.

-

This might be oversimplistic. There have been times in history when investors have favored dissolution and others where they have favored consolidation. Owing to the cheapness of borrowing I tend to think the present categorizes more as the latter (similar to the conglomerate boom but with nonidentical reasons). The general principles of value should hold in any market environment, but more specialized strategies like "buy spinoffs" may not always be advisable. I can say personally that many of the spinoffs I have looked at have a ton of debt, so this strategy would lead you to a rather leveraged portfolio. I believe that is true of some of the Liberties.

-

I am a big wuss too. I have ~30 core positions and 10-20 small positions on the side. I do a basket approach in some areas, if you group those together the number goes down somewhat but I can't imagine going below 20 positions. I'd rather err on the side of caution (i.e. not outperforming) than risk blowing up. Additional upside: it prevents me from getting bored. It's the Walter Schloss approach. And yes, I think quite a few of the concentrated posters here are young, early in their career and run small portfolios (not that there is anything wrong with that). Anecdotal evidence: the topicstarter owns 6 shares of Google. Concentrating is easy for you, you run OPM. Gotta gamble it up! 20 positions seems reasonable. It may be true that with a smaller portfolio you can earn it back quicker, so you might be encouraged to take more risk. But in my case, I'm running this portfolio to establish a track record - so if it blows up I just lost a year of my life. FWIW, I've had substantially all my assets (5-6 figs) in the market for the past 4 years. I've made dumb mistakes (sometimes in the process of trying to avoid other dumb mistakes) and learned from them. So I have just as much fear (if not more) of losing money as the retirees or personal managers on this thread. 0% can be an excellent risk-adjusted return under some scenarios.

-

I think this is correct (it is in my case, 6 digits nearly 50% in my top 3 holdings). Maybe we should define a set of portfolio value ranges (predefined, to keep some privacy) to specify next to your holdings to make a topic such as this a bit more meaningful? Sorry if that creates confusion. I have a second external portfolio largely of options that I am in the process of liquidating (if liquidity weren't an issue I'd transfer the assets today). Once that is done and this portfolio is fully "stocked out" it will be a six figure portfolio of probably 20-25 positions. Hope that helps.

-

The HRG setup is interesting. The co looks kind of like a rollup which I guess partly explains the yields and hedging. What's your "effective" yield after the hedge?

-

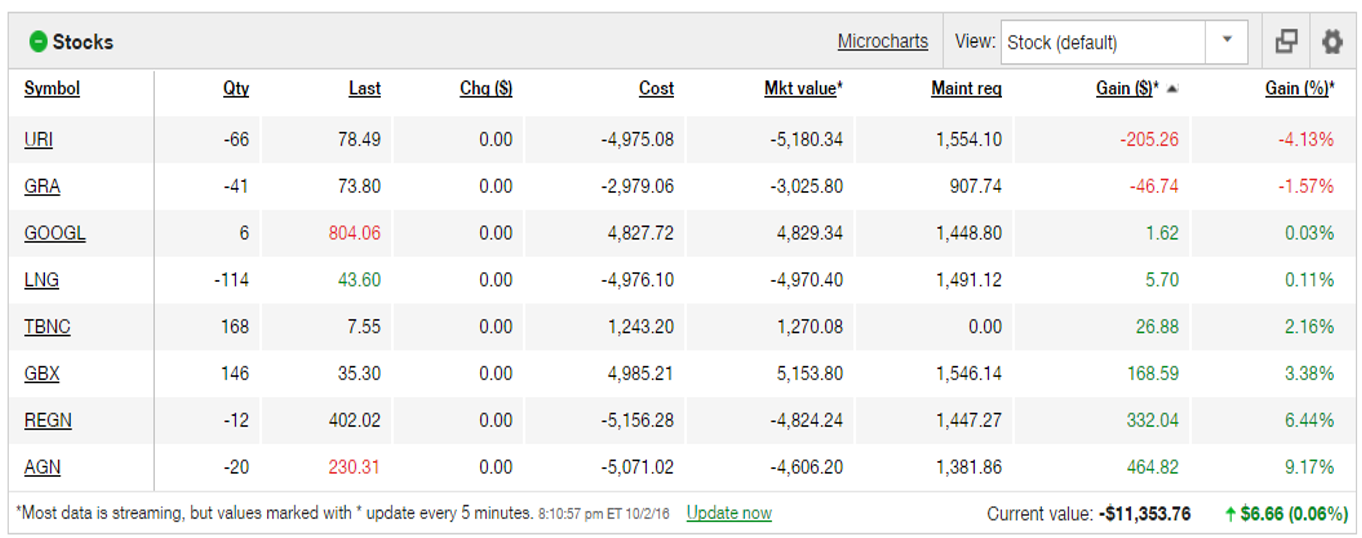

Here's mine:

-

I wouldn't trust Trump to run Berkshire.. but I'm not sure I trust the 3 T's to run Berkshire either. They've made some pretty sketchy buys the last few years. And if Buffett approved those purchases, I'm not sure I trust the octogenarian Buffett to run Berkshire either. Lol - once Buffett's stake gets sprinkled over the planet via the giving pledge, I expect the empire to go the way of the typical American conglomerate. Such things are not meant to last.

-

Negative Equity and Negative Working Capital

Graham Osborn replied to Sleepwell's topic in General Discussion

I'm not sure either of us is trying to make a specific point, but just a few comments on the above: 1. WMT was indeed capital constrained early in its growth, not because of anything special about its capital structure but rather that it was a small business unfamiliar to Wall Street banks and hence Walton was trying to cross-finance off regional banks which was a source of significant personal anguish. After the IPO so far as I know financing was less of an issue. 2. Using ROE to measure a business's ability to grow using existing capital (except perhaps for businesses like GOOGL with very little debt or goodwill/ intangibles) seems a bit naive. Give me any business in any industry and I can give you a capitalization such that ROE is infinite. That's why Mike Burry called ROE "deceptive and dangerous" except in very special cases. 3. I think you may be glorifying AMZN as a retailer a bit over-much. It may be true that a company that can conduct a large volume of business with little capital can generate fabulous returns (like currency traders), but leverage cuts both ways. People always forget that until a little competition comes along, the economy tanks a little, or whatever. Until AMZN starts converting their revenues into cash, which they are doing much more poorly than a GOOGL for example (except maybe AWS), they are worth far less than the 2000 and current valuations would suggest IMO. -

Negative Equity and Negative Working Capital

Graham Osborn replied to Sleepwell's topic in General Discussion

Nice post, however I do find your comments on AMZN (as opposed to WMT) a bit confusing. You seem to be arguing there is some kind of fundamental distinction between the 2 businesses which justifies a different capitalization. ROA is where the money is, and WMT's is about double AMZN's. WMT has a higher ROIC as well. Of course, you can argue that part of AMZN's return is "intangible," e.g. wider moat/ market dominance/ whatever. AMZN's valuation is based on its presumed ability to be a good business with stable returns (like WMT currently) in the future, not on some sort of redefinition of the valuation standards for a retail operation (IMO). One you abandon the idea that the value of a business is what it could be liquidated for in cash at *some* point in the future, I think the process of valuation gets a bit dicey. -

Negative Equity and Negative Working Capital

Graham Osborn replied to Sleepwell's topic in General Discussion

It's a common misperception that you can ignore leverage if EBITDA or interest coverage are high enough. It's like thinking a woman can be more or less pregnant depending on the dress she is wearing - it's semantic. Leverage is a balance sheet definition, and it entails certain risks (as laid out in the indenture) even with zero-coupon bonds. What is the risk? Suppose you buy an asset for X with borrowed funds and the asset value falls to Y. Now you have a shortfall of X-Y which may or not be be covered by the cash flows of the asset. Worse, the repayment date may be a function of the asset value. That's reflexivity. Negative working capital certainly isn't something to brag about. It's like have a high credit limit - it's useful in various situations, but the fact that you need it in the first place suggests certain business risks. Walmart is a company that was borrowed to the hilt from the early days, and the fact that they could/ can operate with negative working capital is a reflection of generous credit terms with suppliers (because, historically, WMT had the stronger hand). Does WMT carry increased risk as a result of this short-term leverage? You bet. Look at the Hanjin bankruptcy as a mini-example. The companies you cite are highly leveraged - the appropriate measure is the D/ E (or D/ tangible book). Don't get caught up in the "new era" definitions promulgated by central banks and the debt-laden blue chips they feed. Someday people will look back on ZIRP as something both insane and transient. -

One of many potential catalysts for popping the bubble is higher oil prices, or anything else that forces up the CAD/ USD. With so many foreign buyers, the relative strength of the dollar pushes up demand.

-

Young Hedge Fund Manager Cracks The Private Equity Code

Graham Osborn replied to Parsad's topic in General Discussion

Buying levered microcaps ranks one rung above buying unlevered microcaps on leverage in my book. Even if you survive, you'll probably wish you hadn't ;) You'll never feel diversified, and forget about publishing your Sharpe ratio. -

Lol. That's going to be my problem. I get carsick unless I'm in the front seat. Unless they develop some technology to eliminate inertia, I am never going to be productive in the car - driver or not ;)

-

Seriously, why does the market as a whole go up?

Graham Osborn replied to whiterose's topic in General Discussion

I agree. If you look at the S&P, the value has increased because of: 1) Observation bias. The largest companies which qualify have gotten larger due to globalization heavily aided by technology/ consolidation. 2) The EV/ Rev denominator/ GDP/ population growth. No one could have foreseen that the US would enjoy the kind of GDP growth we have enjoyed 100 years ago. NOONE. Suppose Hitler had developed the nuclear bomb first? 3) The EV/ Rev numerator/ MC. There have been organic (tech/ globalization at unprecedented scale, a perception of greater political stability which lowers the discount rate) and inorganic (artificially low interest rate/ QE) reasons for this. Contrary to some, I believe #3 is more a kinetic that steady-state effect. Americans think that markets go up indefinitely because they've never seen anything different in their lifetimes or those of their indigent parents/ grandparents. In other words, they have *unconcious* optimism. People think that Buffett and Lynch returns are a function of the person rather than the investment opportunities - idiots. Could Buffett or Lynch achieve their historical results today? Absolutely not. Oh yeah, and I forgot the most important one: 4) RAMPANT INFLATION. The long bond markets should get interesting when folks figure that one out ;). If you don't know what I'm talking about, visit the S&P/ Gold thread. -

Wha? How do you figure that? Maybe if you distributed the demand across the entire day. But that's not an accurate way to look at it. Most people need transportation at roughly the same time as most other people. Commuting to work, commuting back from work are the two main times that come to mind. How are you supposed to spread your 3 cars across 30-40 people for a morning commute? Simply doesn't make sense. Also, you're assuming that once autonomous cars hit mainstream, everyone will want to car-share. Huge assumption that I simply don't think will be the case. I think plenty of people will still want to own their own car. I also think your longevity assumptions of 600k to 1mm miles are way out of whack. I think your assumptions and the conclusion you've drawn are absolutely insane. Ya I kinda echo your thoughts. Now I haven't read all of this thread, but where did this the rationale that we will want to own less cars come from? Are you saying empty driverless cars will come pick up passengers? I am a carless person. But I will buy a car if it is driverless and economical. So me as a datapoint says that cars will increase. The fundemental change of driverless cars is it allows people to drive who cannot or don't want to drive. So it will mean more cars on the road. How can there be more cars on the road and less cars? The main benefits of driverless cars are cost (don't need to pay a driver), safety (lower error rate than human), and cloud control (efficient swarm management). Progress toward these goals has already been achieved by ride-hailing services. I think that car ownership WILL decline significantly in the future. There's no reason for a vehicle to sit parked in a garage when it could be doing useful work. Let's face it - if you could satisfy your transportation needs for $5-10 per day without owning a car, why would you own one? In some cities people are already close to this, but the problem is if you want to take a road trip or drive to the airport you still need a car. It's a bit like the US road system before the interstates were built - we don't have uniform service. The cost of service is still too high for some Uber driver to be wandering out in rural Kentucky. Once vehicles are driverless, the cost may well be low enough.

-

Why don't ya marry him - looks like he's available ;) Hopefully this thread doesn't go the way of the Elizabeth Holmes thread.

-

What is the connection between IRR and growth rate?

Graham Osborn replied to scorpioncapital's topic in General Discussion

I've never found IRR that useful at the company level, I see it more as a marketing tool for companies like Valeant to pitch stupid capital allocation strategies. Like DCF, IRR depends on the prediction of cash flows (unless it's a historical project which has already earned a positive return) - meaning it is useless without a crystal ball. So let me answer this question a different way but with a CAPM flavor (which I don't totally agree or disagree with). If you borrow 1T you are going to have some associated cost of capital. If we assume that cost is "risk free," the only totally safe thing to do is take the cash and reinvest at the risk free rate. But if you do that you're not earning anything. So you need to take some risk to earn a return above your cost, and pocket the spread. The trouble is your rate it no longer risk-free, which means you might earn a net negative return on capital. So you might be losing money and/ or violating debt covenants a la your investment. In fact, given a long enough period, you're guaranteed to do both of those things (like Valeant). Owning the cash you invest ensures you don't get inordinately penalized for poor returns on invested capital or for loss of principal. -

Can people describe the steps they take in bank valuation? On the one hand cash flows are volatile, on the other hand portfolio may be less mark-to-market than one would like. Applying any sort of "steady state" assumption based on historical returns seems difficult particularly with the roller-coaster ride of the past 15 years. Are people just looking for a sufficient discount to book with a sufficiently conservative loan portfolio? Help!

-

What Business do you admire and why?

Graham Osborn replied to LongHaul's topic in General Discussion

The topic is kind of ambiguously defined. For example, I like Star Wars but would not want to own DIS. You can have a great product and a lousy business. What I think is of interest to many is the "great business" as defined by Munger, which has a very specific connotation. You can look up Munger's definition, but I look for conpanies consistently growing their revenues and current assets by 15%+. As some mentioned, GOOGL fits the bill in most ways except that it is obvious, which invites competition and margin pressure. WMT used to be one, as was AAPL. MSFT. Standard Oil. KO. The difficult think is not finding them, but finding them before they are generally recognized and overpriced or mired in competition. -

Hi Fred, if you don't mind my asking, who is/ how are they selecting the companies to present?

-

Does anyone look at the structure of employee stock awards when trying to estimate dilution? The obvious issue is for a company like GOOGL - or any tech company really - the size of stock awards could increase significantly if the stock does well in a year. The analysis would be similar to a convertible preferred issue in some ways I'd imagine. Appreciate any thoughts as I haven't seen the actual structure of the incentive plan often factored into this type of analysis although it seems relevant.