tede02

-

Posts

707 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by tede02

-

When the growth stops - global population peak and decline

tede02 replied to tede02's topic in General Discussion

The point around the birth rate slipping to 1 child per couple is well taken. It illustrates how quickly a shift could occur. Even if the birth rate slides to 1.5 children per couple, that causes a 25% reduction in global population. What's kind of crazy is over half of all countries already have a birth rate below 2 according tothe CIA world factbook. https://www.cia.gov/the-world-factbook/field/total-fertility-rate/country-comparison -

The inflation topic is interesting. It is weird that as a consumer, one sees inflation everywhere, and yet the CPI figures are still hanging around 2%. It seems like the bigger question is whether the inflation is here to stay. Is most of the inflation due to demand build up and supply constraints related to the pandemic? Does all this get resolved over 12-24 months? Or are we setting up for an extended period of growth and higher prices globally? There's smart people on both sides of this debate.

-

When the growth stops - global population peak and decline

tede02 replied to tede02's topic in General Discussion

I appreciate the comments. Was thinking about this further in the context of more immediate implications. In the US, there's a growing fear of China's ascent. In terms of population growth, China is expected to top out by the middle of this decade. It will be quite interesting to see how this impacts growth as the population ages and starts to decline over the coming 20 years. Will the Chinese face the same challenges with growth as basically all the other advanced economies with similar demographic issues (Japan, many European countries, etc.), and therefore all this fear in the west turns out to be over-blown? They still have a much lower GDP per capita so perhaps they can continue ramping that up for decades, but I simply wonder how big of a headwind these demographics will be. -

Curious if anyone else is as fascinated with the subject of global population as me. There are different aspects of this subject that are intriguing. As a sportsman, I always wonder what it would have been like to travel North America pre-European settlement. Just to see the mostly virgin land and amount of wild game must have been amazing. As an investor, I always think about what happens when the global population starts to decline. Basically all estimates conclude the world population will peak by the end of this century. Some developed world countries are already shrinking. This BBC article was striking in highlighting a number of countries that could see their populations halved by 2100 (Japan, Italy and Spain in particular). https://www.bbc.com/news/health-53409521 It seems obvious this will lead to massive economic problems. The world economy is based on growth in every respect. What happens when there are empty buildings and houses everywhere because there literally is no one to occupy them? There won't be enough taxpayers to support infrastructure, entitlements, etc. The list just goes on. I don't expect any good answers but it's just a mind-blowing idea to me that we're presently living on the J-curve of the good times but the end of this economic goldilocks period may not be too far off. I think my kids and future grandkids likely won't have to deal with these issues. But my great and great, great grandkids likely will. Side-note - I've also been thinking a lot about the Fermi Paradox. Perhaps the answer is advanced civilizations all eventually implode because they quit reproducing!

-

I appreciate the comment. The internet analogy resonates with me. I really struggle to see where this is going beyond what looks like wild speculation. But I'm sure many people felt the same in the mid to late nineties regarding the internet. I've spent a fair amount of time reading about crypto to keep an open mind and understand it better. The more I learn the more questions I have. Digital central bank currencies and good old fashion regulation appear to pose some real hurdles. But the blockchain technology itself is interesting and seems to have utility even outside of finance.

-

Question - Aren't exchanges, like Coinbase, in conflict with the concept of peer to peer/decentralized finance? Aren't these exchanges very much centralized and just more big financial intermediaries that crypto was supposed to displace?

-

Visa and Mastercard have got to be pretty nervous.

-

Listened to the Coinbase CEO on CNBC this morning. He had some interesting things to say. For example, his view is most countries will roll out their own digital currencies over time and crypto will be complimentary to them. He also talked about his expectation that governments will regulate as they normally do to maintain control of their respective monetary systems. I'm curious what crypto advocates see for the future? Do people envision going into an ice cream shop or car dealership and having the option to pay in digital dollar, digital yuan, digital euro, bitcoin, ether, etc.? Do people see other means of digital payments as likely (such as paying for things in shares of common stock)? Eliminating intermediaries and instant settlement seem like very important things. But I struggle to see all of these different units being used/accepted for payments ubiquitously. It seems like it would be very complicated administratively and there would be lots of "currency" risk. Alternatively I keep contemplating as to whether crypto currencies end up as more of a trading unit like precious metals and never really take hold as a system of payment. Thanks for any comments. This is an intriguing topic.

-

I'm surprised there was no discussion about the lengthy article in WSJ about China's rollout of digital currency: https://www.wsj.com/articles/china-creates-its-own-digital-currency-a-first-for-major-economy-11617634118?mod=trending_now_news_pos1 It was a very interesting read. Brings up a number of points of how crypto threatens the control a country has over its monetary system and sovereignty more generally. Also discusses how much leverage the US presently has over foreign governments, businesses and individuals by being able to freeze them out of the global financial system. This leverage could be totally undermined obviously if transactions start settling in other currencies, soverign or defi crypto. The article says 60 countries globally are evaluating the prospects for issuing digital currencies. My takeaway was there is growing pressure for central banks to move forward with digital offerings because of the issues mentioned above. There's also obviously growing competition between the US and China in all kinds of respects, including dominance over the global financial system. The article generates the narrative that western nations are feeling more urgency to get into the game. Lets just say within 10 years, every major nation has a digital currency. What does this mean for crypto and defi? Don't soverign digital currencies present a major threat to non-soverign cryptocurrencies? Are there reasons why soverign and non-soverign would co-exist?

-

There was an article in the WSJ within the last week that I thought said it best...ultimatley bitcoin is software. More specifically, it is a decentralized account ledger that tracks the finite digital coins & transactions within the network.

-

Sir I beg to differ. I bought a very average honda suv for $26k, including added after market self driving. If we go back in time to 1990, how much would such a car be worth? I mean it can almost drive itself on hwy. Based on the inflation calculator prices have doubled from 1990 to now. So can I buy a smiilar car for $13k then? I wouldn't think so, so there..... in terms of suvs the price real costs have gone down. In terms of computers, I can buy a minimalist non-laptop computer with a basic monitor for about $200. In 1990, that computer would cost 2-3k? Cell-phones? they didn't exist. Jeans, I remember I had to work hard to save $50 to pay a decent pair of jeans, now? $20! I was a kid and we weren't wealthy and I wanted a chess clock (the type you see on the Queen's Gambit on neflix), those cost $50-80, I had to deliver papers to save up to pay for it. Now? we got the digital chess clocks that are much better, and they are $35, so now I can get a better quality product for less than 1/2 price. Travelling by airlines was a luxury, now it is so common it is like taking a bus. I feel we all just too easily fall into groupthink and don't challenge the complaints and negativity in the media. Inflation index calculates the average living expenses and for the most part I feel it is an accurate reflection but the cost of really long term assets like land and money generating assets, have gone to absurd levels..... cough cough hmmmm tesla cough hmmmmm. All very good points. I was trying to think of where we have experienced inflation. The ones that come to mind are: 1. healthcare 2. childcare 3. education 4. housing The whole debate about inflation vs. deflation is interesting. I heard about a study that valued Google's "free" services (search, email, storage, etc.) at over $20k per year per person. I have no idea of the methodology used. But the greater point is all these things that the internet provides for no-out-of-pocket to consumers definitely does appear deflationary. I heard someone say just this morning that the "inflation animal" that economists are trying to measure today is one that no one has ever seen in the wild. The point this person was making is there are all these online services that are virtually impossible to measure so no one really knows where the hell things are at. That resonated with me.

-

What would be so bad about that? I rather Central Bank's focus on the real economy and less on boosting financial assets. If main street is doing well with higher wages, better quality of life, and less inequity while stock markets are going down, I'm perfectly okay with that. But we don't really see that anymore. We can't withstand prolonged pain in the financial markets anymore. After some signs of distress, CB's come in with their massive rate cuts and QE infinity. I don't really disagree. My worries are mostly for my clients, many of whom are just regular retirees living off of a retirement portfolio. If we went through a 10-year period of no returns, that could create some major financial stress for a lot of people. The Fed surely knows this too which puts further pressure on policy makers. They also have to wonder (like me) if they are setting the stage for some major blow-up or extended period of stagflation.

-

This is a fascinating subject that I think about all the time. What will the Fed do? They've kind of put themselves in a corner. They surely know if rates jump 100-200 bps, that is going to have some real impact on assets prices across the board which could leak into the real economy. But they've explicitly said they want to keep rates low because the economy isn't where they want it to be. Therefore, it seems they plan to keep the fire hose on (to keep rates down) with indefinite asset purchases until something breaks. One of my worries is that few individual investors recognize how much stock market returns have been driven by low rates and QE. The sentiment is "investing is easy" without appreciating this HUGE tailwind. I worry we could experience a multi-year period of negative returns due to problems with inflation, rising rates and the money-out-flow negative feed-back loop that would probably be created.

-

I appreciate this perspective, particularly around negative yields in Europe which we've never had to deal with in the US. Maybe I would think about alternative currencies differently if I had to face negative yields. I'm currently reading a biography on JP Morgan. There's a lot of interesting history that seems relevant to the current crypto debate. There was no central bank in the US until the year of his death. So I'm learning a lot about the challenges of maintaining a currency, capital flight and the inherent tension between parties that want a strong currency vs. those who want easy money. It certainly isn't cut and dry.

-

Fed chair said today that they are looking very closely at issuing a digital dollar. If central banks issue digital currencies, does that upend BTC and everything esle? Or are people attracted to crypto because of its decentralized nature and supposed anonymity? I struggle to understand the bull case for crypto. The ledger technology seems to have real utility but I don't really grasp how these are solving a lot of problems unless one really fears inflation. I work with a lot of retail investors. My totally subjective view is the fervor for crypto is similar to 2017, maybe slightly dampened because there have been other hot assets running up simultaneously. You know its crazy when construction workers start asking about it... LOL (and I've had several).

-

I was thinking about this most recently. Just the cash on the balance sheet plus the AAPL position are worth nearly half the market cap.

-

I hope it's more than a moment! LOL. Been a long slog for value guys.

-

My wife, who is in healthcare, is getting hers today. I'll get one as soon as it's available. I understand some who have legitimate concerns regarding the newness of the vaccine. But there is real risk in contracting COVID too and the long-term effects of the virus will not be known for years either.

-

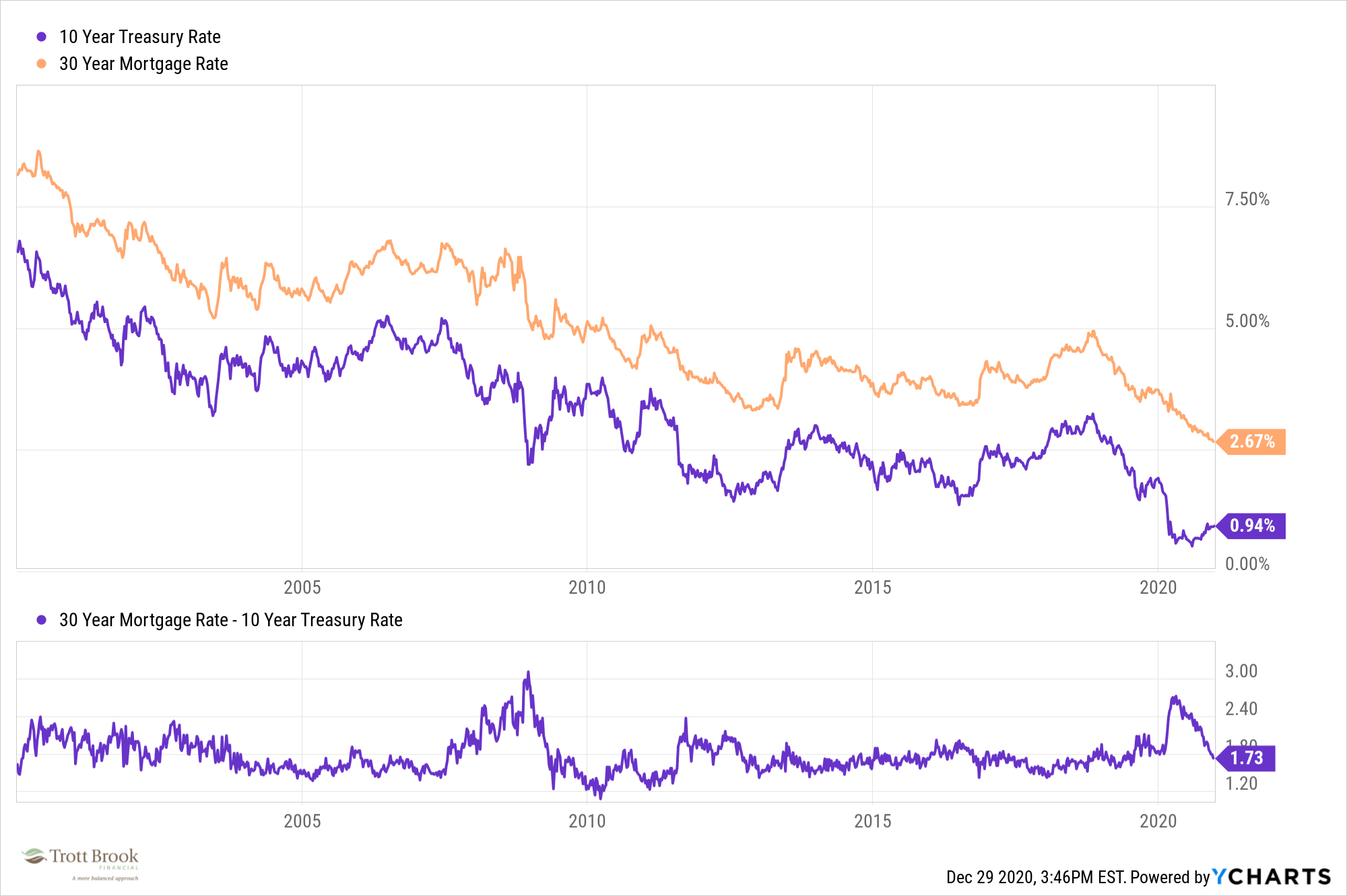

Jeffrey Gundlach has expressed a view that he believes the Fed is in-fact manipulating long-term rates via open market purchases. It's an interesting question whether or not long rates could go higher if the Fed doesn't want them to. You would think at some point, if inflation started heating up for example, that market forces would over-power the Fed's actions. One interesting relationship I've spent more time on this year is betweeen the 10 year Treasury and 30 year mortgage. The correlation between the two is nearly 1. My understanding of this is most mortgages are guaranteed via Fannie/Freddie, and therefore ultimately by taxpayers. Thus the market views Fannie/Freddie mortgages (and ultimately mortgage backed securities) as similar credit risk as Treasurys. But if you look at this relationship, the long-term average spread between the 10 year Treasury and 30 year mortgage is about 1.5%. I'm not an expert in this area by any means but one of the main reasons cited for the 1.5% spread over the 10 year is the pre-payment risk that comes with mortgage bonds. Watching the spread seems to be one of the best ways to determine how attractive mortgage rates are. For instance the spread gapped out last spring when the 10 year cratered all the way down to like 0.50%. Even now, the spread over treasurys is higher than average which suggests rates could be lower. Attached is a chart I keep on spreads. Couldn't figure out how to get it into message body.

-

This is a great book. It was the first large biography I ever read as a young adult in the mid 2000s. It definitely influenced me. You can't forget some of "Poor Richard's" one-liners like, "Early to bed, early to rise...!" I'd like to re-read this in the future. Will certainly read differently with accumulated knowledge vs. when I was 18 or 20.

-

If you're over the income limits, the "back door" strategy is the work-around to make Roth contributions regardless of your earnings. However, by establishing a pre-tax IRA, you'll eliminate your ability to execute this strategy due to the IRA aggregation/pro rata rules. I've seen people get tripped up by this. It can be a surprise at tax time and complicates the record keeping of pre/after tax dollars within an IRA. If you're not using the back door strategy, and never plan to, having a pre-tax IRA is no issue at all. The other thing I would add is if you retire at age 55, you can take distributions from a 401k without penalty. If the money is rolled over to IRA, penalty free withdrawals are age 59.5. If neither of these are an issue, rollover is a good deal. Few people know that they are paying fees inside 401k plans. The fees are usually built in to higher fund expenses so you never see them. The fees are generally lower in large-company plans. The flexiblity of IRAs is nice and the costs are hard to beat at the discount brokers.

-

I've had a Surface Pro 4 for several years. There are two things I don't like about. First is the "kick stand" support. I like sitting in a recliner and it just doesn't rest well on my legs like a regular laptop. Second, the touch screen has alway been problematic. Tends to freeze up the device somewhat regularly.

-

If you don't already have a pre-tax IRA, establishing one via a rollover will limit your ability to execute a back-door Roth conversion strategy due to the pro-rata rule. If you don't care about making Roth contributions via a non-deductible IRA, this won't be an issue for you.

-

LMAO! Ed Thorpe is the man. His autobiography is one of my favorite books.

-

We've been happy with Fidelity. Almost went with Schwab, but our firm uses eMoney financial planning software which Fidelity owns. That integration was important for us. I do like the fact that Fidelity is privately held. I think it give them more flexibility in making long-term decisions. But, Schwab has a good reputation in the RIA space. I'm sure you'll be fine either way. One strike against IB, in my opinion, is their website. I have a separate account there that someone on this board manages. I just find the website clumsey to navigate. Schwab and Fidelity seem to have far better platforms particularly for non-savvy retail investors.