DanielGMask

-

Posts

195 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by DanielGMask

-

Here it is! BRK_2019.pdf

-

Movies and TV shows (general recommendation thread)

DanielGMask replied to Liberty's topic in General Discussion

Just finished it. I watched it because of your post and I totally agree with you! Great recommendation. -

Buffett buybacks: Could Berkshire tender stock?

DanielGMask replied to alwaysinvert's topic in Berkshire Hathaway

This kind of talk is what I call to crimp the curl! 1) Buffett has been clear about how to calculate BRK's value. 2) He has clearly stated that buybacks could and would be done under IV if that is the best use of capital. 3) He has clearly stated that buybacks are a smarter use of capital than dividends. So it's logical that everybody here is asking why he is not buying. -

I haven't had a chance to watch the CNBC interviews yet but from what I've read, it doesn't sound like he's explicitly saying Berkshire didn't buy more Apple at the beginning of January when it spend a little time in the $140s, I think he probably said he's not buying NOW (meaning around $172), and we don't have much firm evidence of Berkshire buying much at prices above $180 or so even in 2018Q3. I certainly recall thinking they probably added most of their Q2 buys in the dips into the $150s, even though AAPL ended Q2 much higher. In December, AAPL spent only about 10 trading days below $160 and only broke below $170 around 7th December. I was thinking about at what price I'd buy back into AAPL in January, and I decided that based on opportunities elsewhere, it would probably need to be $125-$135 for me to have enough margin of safety for a large high conviction position, which would also have bagged me an extra 10-15% or so of return if those prices had come about, compared to the $145 or so it was selling for at the time for a day or two. I think it's possible that Berkshire could have bought a little more AAPL early this quarter, though the lowest prices were only available for a short period right at the start of January, not allowing Berkshire to buy a lot, and we're probably not going to find out roughly how much (if any) until 4th May, and exactly how much on 15th May. You are correct! He clearly stated that if it were cheaper he would be buying it. He said BRK's avg cost is around $140.

-

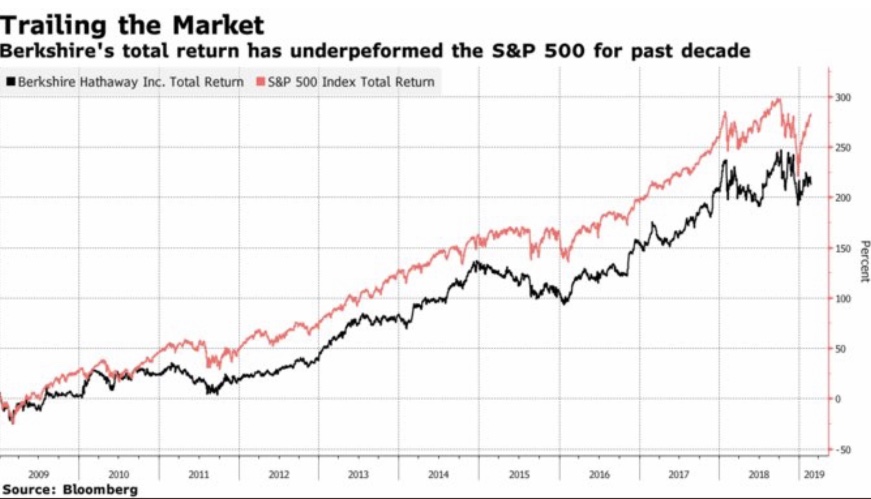

Berkshire's total return has underperformed the S&P for the last decade. Graphic attached.

-

Central Securities Corporation

DanielGMask replied to OracleofCarolina's topic in General Discussion

Are you a shareholder? Are you familiar with the company? -

+0.20% before dividends.

-

Is Molson Coords Brewing really trading at 6x FCF? I’m not familiar with the company, but what about this trend? Icehouse > Sales change (2012-2017): -8.9% > Barrels shipped in 2017: 1.3 million > Market share: 0.6% Coors Light > Sales change (2012-2017): -11.1% > Barrels shipped in 2017: 15.9 million > Market share: 7.6% Miller Lite > Sales change (2012-2017): -12.3% > Barrels shipped in 2017: 12.8 million > Market share: 6.2% Keystone Light > Sales change (2012-2017): -15.1% > Barrels shipped in 2017: 3.5 million > Market share: 1.7% Milwaukee’s Best Ice > Sales change (2012-2017): -16.8% > Barrels shipped in 2017: 1.2 million > Market share: 0.6% Miller High Life > Sales change (2012-2017): -21.5% > Barrels shipped in 2017: 3.5 million > Market share: 1.7% Milwaukee’s Best Light > Sales change (2012-2017): -43.7% > Barrels shipped in 2017: 625,000 > Market share: 0.3% Miller Genuine Draft > Sales change (2012-2017): -50.5% > Barrels shipped in 2017: 680,000 > Market share: 0.3% Source: https://247wallst.com/special-report/2018/12/21/beers-americans-no-longer-drink-5/2/

-

An Evolve-or-Die Moment for the World's Great Investors

DanielGMask replied to saltybit's topic in General Discussion

None of the faang stocks were born as of 2001 besides Amazon? Apple has been around for decades (publicly traded). Google was founded in 1998 and Netflix in 1997. So the only one that wasn't "born" was Facebook. Let's assume that interest rates didn't drop in 2000-2002 (from a high of 6.79% to 3.61% in 2002.). It's probably safe to assume the market wouldn't have hit a new high so quickly (the market recovered from a 50% drop in roughly 6 years). If the market didn't recover (and people were still licking their wounds) it's plausible, if not likely that the most of the faangs wouldn't have received the venture capital that they did and wouldn't be around today. How's that not a bailout? This line of thinking is completely wrong! The correct way is clearly stated by Spekulatius: “Bailing out an economy us very different than bailing out specific companies. Investors in overvalued tech companies were never bailed outend neither were employees who lost their job.” FAANG stocks are creating a lot of jobs and innovating in many fronts. If what FAANG offer is not of use or if there’s is something better out there, users will vote stop using their services without the need of governments telling/helping them to do so, but if users like the service then no matter what they will keep using it, and that’s exactly what defines a free market and what makes the US such a strong economy. -

An Evolve-or-Die Moment for the World's Great Investors

DanielGMask replied to saltybit's topic in General Discussion

FB and Google are not monopolies because they are partnering with other companies to be on top of their competitors, nor because they can pay more than others or because they are the only toll bridge communicating the island. They are good at what they do and people go to them instead of going somewhere else. Talking about breaking up a company just because it’s big is not a capitalist view of the world, actually that’s a dangerous view of the world! -

11 Reasons to Short Berkshire Hathaway

DanielGMask replied to DooDiligence's topic in Berkshire Hathaway

Nice historical perspective. Thanks for doing the work. I don’t agree with the statement BRK’s risk is below the S&P. I define risk as the possibility of loss of principal and I consider the probability of BRK going to zero much bigger than the S&P. Having said that, I don’t have any investment in the index and more than 50% of my portfolio in BRK. Shorting is risky business and shorting something as profitable and solid as BRK more so. The right question is not if this is the right time to short Berkshire, I think it’s not. The appropiate question is if BRK may suffer as a company once WEB is no longer at the helm or alive, and that probably is going to happen during the next 10 years. BRK is less attractive because is huge and compounding at this size is not that easy, but those who are familiar with the concept of antifragility will conclude that this is as antifragile as a public company may get! -

11 Reasons to Short Berkshire Hathaway

DanielGMask replied to DooDiligence's topic in Berkshire Hathaway

He didn’t get invited back after that. I sense that Greg Warren of Morningstar is on the Dias as somewhat of a bear(I feel that way about him). He gets into a lot of detail with his six allotted questions but imo ends up in the “precisely wrong “ category. I am also looking for someone who can ask the tough longer term questions that will get Buffett talking about things he would rather not. The format of the q&a during the AM makes it impossible to get direct responses. A complex question usually needs follow up questions, more so when the person answering is capable of directing attention to what he wants to teach. Because of this format people pack their questions with lots of information and WEB usually gives vague responses. -

BRK Surplus Cash- Optics of a Buyback

DanielGMask replied to nickenumbers's topic in Berkshire Hathaway

Daniel, Several CoBF board members haven't considered Berkshire fairly valued recently, and have been adding to their positions. I am aware, I’ve read their posts. -

BRK Surplus Cash- Optics of a Buyback

DanielGMask replied to nickenumbers's topic in Berkshire Hathaway

Interesting news! The Board of Directors of Berkshire Hathaway Inc. has today authorized an amendment to Berkshire’s share repurchase program. The earlier share repurchase program provided that the price paid for repurchases would not exceed a 20% premium over the then-current book value of such shares. Under the amendment adopted by the Board of Directors, share repurchases can be made at any time that both Warren Buffett, Berkshire’s Chairman and CEO, and Charlie Munger, a Berkshire Vice Chairman, believe that the repurchase price is below Berkshire’s intrinsic value, conservatively determined. -

BRK Surplus Cash- Optics of a Buyback

DanielGMask replied to nickenumbers's topic in Berkshire Hathaway

Berkshire has a daily volume of about 700 millions on the B shares (3 months avg) so he could purchase 30-35% of that for 3 months in a row without the need of having to report it before the next filing and that will easily take out more than 20 billions. I don’t think he’s not purchasing it for any specific reason other than thinking about the best alternative available and he clearly sees Apple and cash as a better alternative right now. BRK seems fairly valued and it may certainly become cheaper, in which case he better be prepared, though he will probably find something even cheaper in that case! -

Seems dangerous! I live in Mexico and we are about to elect a new president and part of congress. The candidate that’s leading (by a lot!) is clearly socialist and against market systems. This doesn’t mean that if he wins he is going to nationalize private companies or move against industry, nor that congress will approve such decisions, but he may control an important part of congress and indeed make some moves against free markets. The peso is reflecting some of these fears and if I were to bet (I’m not), I would bet against the peso! I base my investment decisions on facts, not on news or emotions. But hey, that makes a market. Maybe i am wrong. Currency speculation is precisely that, speculation. And facts tend to be deceiving when dealing in an speculating environment, but seems you are comfortable and convinced of what you are doing. I was just trying to point you in the direction of some “facts” you consider news or emotions, so be my guest!

-

Seems dangerous! I live in Mexico and we are about to elect a new president and part of congress. The candidate that’s leading (by a lot!) is clearly socialist and against market systems. This doesn’t mean that if he wins he is going to nationalize private companies or move against industry, nor that congress will approve such decisions, but he may control an important part of congress and indeed make some moves against free markets. The peso is reflecting some of these fears and if I were to bet (I’m not), I would bet against the peso!

-

beating the market - not what it used to be

DanielGMask replied to tede02's topic in General Discussion

Never in my life have I owned 30 stocks [*edit* at any one time]. But, then what do I know? SJ I currently have 10 different stocks (1 representing 40%) and this is the time with most holdings in my investing lifetime. I think 30 positions is a huge number for anybody to understand and focus on his/her holdings. -

Call me Ted by Ted Turner Einstein by Walter Isaacson

-

Foundation series by Isaac Asimov Atlas Shrugged by Ayn Rand Kane and Abel by Jeffrey Archer

-

Everybody is fallible, including Buffett. But I don’t think that passing on AMZN, GOOG or FB is equivalent to making a mistake. Those companies weren’t sure things when they were smaller/cheaper, and putting money into something where the price to owner’s earnings is ridiculously high because the market assumes it will grow and grow is more of a guessing game than investing. Moats used to be way more stable and difficult to overcome. Technology disruption changed that and the likes of Buffett (myself included though much younger) are adapting to this new paradigm of assets-light companies with ever-changing moats. Anyway, I don’t think we will ever see another investor with the capacity to achieve such great results for more than 60 years while maintaining an honest and humble attitude. It really doesn’t matter if he missed the likes of Intel, Wal-mart or Facebook, on the contrary, what’s incredible is that he achieved the impossible even after missing those great companies! I'm not saying those were his mistakes? Are you all purposefully trying to misread my posts? ;) Or are you replying to ScottHall? I'm basically saying the same as you, DanielGMask. Not buying MSFT since the nineties is an example of an error of omission in my opinion. So I have a different view of what his mistakes are than ScottHall. Would be ridiculous to assume there is an investor out there that doesn't make mistakes anyway. I’m not trying to misread you and I was indeed answering the previous comment. Still I don’t totally agree with the statement that not investing in MSFT since the nineties was a mistake. From my observations on Buffett I conclude that he invests when he thinks he can asses the future cash flow of a business and that number makes sense when compared to the actual share price. I think that’s the reason he is now investing in AAPL but didn’t invest in MSFT during the nineties. It wasn’t a mistake but a lack of understanding MSFT’s potential or a consequence of his personal relation with Gates. According to my point of view, the IBM investment is an example of one of Buffett’s mistakes.

-

Good of him to own up to this. He has cost shareholders a lot in terms of opportunity cost the past decade, hate to say it but it's true. Outside the GFC Berkshire has done nothing impressive and TBH even considering that opportunity returns have not been that impressive compared to what they should have been with the "world's greatest investor" at the helm. Munger says Buffett keeps getting better with age. I don't see it, honestly. He's still very good but I don't get the impression he or Berkshire have morphed with the times in the way that is sold. It's cool he's trying new things with Apple, maybe he'll get his old groove back sooner or later. I'd say that is a little too negative considering size, market conditions and cash position. Ask Prem Watsa about true opportunity costs... Hell, ask most decent fund managers with a strong value bent. They'll come back in vogue at some point too. Buffett was buying in 08/09 while many were trembling with fear. And he still did some decent deals like you said. That's more than most can say. Nothing mindblowing but he has still kept up with the market and its soaring tech stocks with enormous cash levels. Maybe he got better with age but certain conditions make it very hard to see this. I'd love to see what happens if the S&P500 drops two or three years in a row! Also, selecting Todd and Ted, who both seem to be beating the market, is impressive in itself imo. They are not managing a few hunderd million... So easy to say in hindsight that BRK did poor vs broader market. Maybe one of his biggest mistakes is not buying MSFT a few years back and going after IBM. (With IBM he fell prey to a backwards looking fallacy as someone else put it here. "They have always reinvented themselves thus they will do it again.") But who would have guessed Amazon, Google, Apple, Netflix, Facebook, ... would be where they are today. Five years ago, 99%+ of analysts, investors etc would have called you insane if you dared to predict this outcome. Do you know about many fund managers who got extraordinary outperformance vs the market? In any case, I would have slept better owning 100% BRK than 100% S&P500 in the last 9 years. For the last 20 years, BRK has been a great stock to own in size at certain points in time. Good investors were best to trade around that. Early 2000 and 2011/2012 were two such occasions where the investment case was a no-brainer. Many didn't see it in 2000 and 2011 and I'm sure Mr Market will be blinded once again in the future. I really don't think that's true. I and many others have made very good returns on Facebook, Amazon and Google over the past five years. I sold out of Facebook recently - I will buy back in - held it since 2014 and had 137% gain on the position. Still have AMZN and GOOG. I didn't miss these stocks and a lot of people on these forums think I'm one of the biggest idiots on here. I beat Buffett at growth investing, so did a lot of others on this forum TBH. He owns up to his mistake and there's no shame in making mistakes, but to say that 99% of people couldn't figure those stocks out seems a little silly to me. Maybe I didn't make clear enough what I meant exactly. There is a difference between figuring some of these stocks out and predicting that they would be 5-10 baggers from 2013 levels. I'm not stating that 99% didn't figure these out, I'm saying that most people would have laughed in your face when you would have claimed, for instance, that Netflix would have a $140B market cap in early 2018. 99% seems about right to me, but the number was meant more to make a point. Could be 95%+ just the same. My point is that sentiment was véry different back then and that it was not easy to predict this outcome. If you and others did, you guys are eithers very bright or very lucky. I remember you buying FB a few years back, so congratz! (As an aside: I wouldn't assume the average money manager is on par with the brighest on this forum tbh. Or they might be but have various reasons (career risk etc) not to act on it.) Would love to see if we could find more than a handful of fund managers who have, in the last 9 years, either: 1) trailed the S&P500 with an equal cash balance on average; 2) outperformed the S&P500 with >10b in assets. I'm also very interested to see how these managers will fare from now until after the next stock market slump versus Buffett, Todd and Ted. Somehow I feel I already know the answer. Anyway, I think we both agree that Buffett is still very good but that he made some mistakes. So not really a big difference in opinion. Given the circumstances I just believe these mistakes are understandable and minor. Buffett isn't omniscient. Everybody is fallible, including Buffett. But I don’t think that passing on AMZN, GOOG or FB is equivalent to making a mistake. Those companies weren’t sure things when they were smaller/cheaper, and putting money into something where the price to owner’s earnings is ridiculously high because the market assumes it will grow and grow is more of a guessing game than investing. Moats used to be way more stable and difficult to overcome. Technology disruption changed that and the likes of Buffett (myself included though much younger) are adapting to this new paradigm of assets-light companies with ever-changing moats. Anyway, I don’t think we will ever see another investor with the capacity to achieve such great results for more than 60 years while maintaining an honest and humble attitude. It really doesn’t matter if he missed the likes of Intel, Wal-mart or Facebook, on the contrary, what’s incredible is that he achieved the impossible even after missing those great companies!

-

“If you don't feel comfortable owning something for 10 years, then don't own it for 10 minutes.” “Charlie and I look for companies that have a) a business we understand; b) favorable long-term economics; c) able and trustworthy management, and d) a sensible price tag.” Both Buffett quotes. I don’t think Biglari is an investment you should feel comfortable owning long-term, nor Sardar a trustworthy partner! I think people are interpreting Buffett way too literally. His Korean stock purchases clearly do not meet the criteria above as well. But Buffett still did that trade and made it a point to highlight that. treasurehunt has a rationale for why the business could be mispriced due to structural factors, understands management factor and seems to think there is enough margin of safety to make a profitable trade. That to me is the essence of value investing. Whether it works or not is a separate issue. Vinod I quoted Buffett because I agree with the quote, completely! If you put your money in the hands of somebody that’s not trustworthy you’re on a ride you shouldn’t be. That to me is the essence of a bad investment, whether it works or not. All I am saying is, by being less dogmatic and our returns would be much better. If you draw a line in the sand and say if there is a question of management integrity, you would not invest. I can understand that. We all have to draw the line somewhere. When Buffett invested in Korean stocks, he had no idea about the management. The margin of safety is so high, he can ignore it and still expect good results. There are many approaches that work in investing. No need for a value investing Jihad on the one right approach. It is not like what Buffett says is the scripture. There is always more nuance. What you quote makes perfect sense. I agree too. But you also need to understand the context and where it is applicable. Here a person is not investing in a business with the intent to hold long term. Walter Schloss did alright with a different approach. I would buy BH too if the discount to IV is large enough. It is not there for me. Vinod I agree with you except on the part “I would buy BH too if the discount to IV is large enough...”. It’s very different to invest in something you have no negatives about management’s integrity, even though you may not know anything positive either (Korean stocks), to investing in something you already know several negatives about management (Biglari). That’s thumb sucking and it has nothing to do with being dogmatic. There are several companies where to invest, people should avoid companies where management is not trustworthy.

-

You’ll find two kind of persons in your life, those you enjoy and those you don’t. For business’ you’ll find those that are trustworthy and those that are not. Avoid the second no matter of price and you’ll never find yourself in a position you may regret. If management (founder, CEO, etc..) is not trustworthy I don’t even look at the numbers. And no, I don’t think that Biglari will be the opportunity of a lifetime at any price because the CEO may make this a bad investment no matter the price.

-

“If you don't feel comfortable owning something for 10 years, then don't own it for 10 minutes.” “Charlie and I look for companies that have a) a business we understand; b) favorable long-term economics; c) able and trustworthy management, and d) a sensible price tag.” Both Buffett quotes. I don’t think Biglari is an investment you should feel comfortable owning long-term, nor Sardar a trustworthy partner! I think people are interpreting Buffett way too literally. His Korean stock purchases clearly do not meet the criteria above as well. But Buffett still did that trade and made it a point to highlight that. treasurehunt has a rationale for why the business could be mispriced due to structural factors, understands management factor and seems to think there is enough margin of safety to make a profitable trade. That to me is the essence of value investing. Whether it works or not is a separate issue. Vinod I quoted Buffett because I agree with the quote, completely! If you put your money in the hands of somebody that’s not trustworthy you’re on a ride you shouldn’t be. That to me is the essence of a bad investment, whether it works or not.