KCLarkin

-

Posts

2,453 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Everything posted by KCLarkin

-

AFAIK. When you borrow, the USD has a cost basis based on the current XE rate. Borrow $1000 USD (at $1.1 CAD) = 1100 CAD Repay $1000 USD (at $1.2 CAD) = 1200 CAD Capital Gain (Loss) = ($100) Buy 100 BAC @ $10USD (at $1.1 CAD) = 1100 CAD Sell 100 BAC @ $11 USD (at $1.2 CAD) = 1320 CAD Capital Gain = $220 Net Capital Gain = $120 CAD In this case, you are basically hedging out the FOREX so your gain calculation is pretty easy. The interest paid would complicate things slightly.

AFAIK. When you borrow, the USD has a cost basis based on the current XE rate. Borrow $1000 USD (at $1.1 CAD) = 1100 CAD Repay $1000 USD (at $1.2 CAD) = 1200 CAD Capital Gain (Loss) = ($100) Buy 100 BAC @ $10USD (at $1.1 CAD) = 1100 CAD Sell 100 BAC @ $11 USD (at $1.2 CAD) = 1320 CAD Capital Gain = $220 Net Capital Gain = $120 CAD In this case, you are basically hedging out the FOREX so your gain calculation is pretty easy. The interest paid would complicate things slightly. -

Tengen, your interpretation is correct (AFAIK), assuming that IT-95 still applies 35 years later. The key thing is that the USD cash you hold is subject to capital gains whenever a transaction occurs. So both the foreign cash you hold and the securities you buy have an ACB. When you buy a stock with foreign funds, you are selling US cash (at current exchange rate) and buying a US security (at current exchange rate).

-

As I understand it, at the end of the year you are supposed to declare the capital gains on any foreign currency held throughout the year. As you can imagine, this gets very ugly if do a lot of transactions.

-

Many tech companies have very wide moats. They just tend to have a shorter life expectancy.

-

I am working through the CB&I annual report right now. I think you are right to be skeptical about the cash balance. CBI, for example, has a very large negative working capital balance. Depending on the nature of the projects, the revenue, earnings, and ROE are all rough estimates at best. How long are the projects? What are the revenue recognition policies? One of the reasons why they might have decent ROE is that they have very large upfront payments, which would reduce capital needs. I would expect to see this as deferred revenue on the balance sheet.

-

He cherry-picked the 6.5 year stretch for this letter but his out-performance record goes back to 1999. That is two full cycles. Hope isn't really required because the share price reflected the hopelessness of the situation plus the new management was already making moves to unlock value. The stock is up over 60% since he started buying so I don't share your concern.

-

This would be noted in 13F as confidential disclosure (there were none in Q4).

-

They amended Q3 13F to show sizeable increase in Deere. They didn't ever sell Deere, just switched it to confidential disclosure, best as I can tell.

-

Deere, they have filed an amended 13F for Q3.

-

Canada has a duopoly. Air Canada still managed to lose money four years in a row just barely avoiding its second bankruptcy in less than 10 years. Even if the airlines remain rational (doubtful), fend off Low Cost airlines, and remain profitable, the unions will reassert their power. This remains a terrible industry with very strong cyclical tailwinds. Westjet is 5% of my portfolio but I put no faith in the "this time is different" mantra.

-

If you want to start a new airline, you basically just need to lease a plane (read Virgin story in Dhando Investor). It is essentially impossible to build a new railroad.

-

No asset has an absolute value. All values are relative.

-

Yes, real estate prices are elevated and are sensitive to rising rates or economic shock. But almost all asset prices are elevated and sensitive to rising rates. This doesn't mean there is a bubble -- it just means that low interest rates are creating dangerous distortions in the financial system.

-

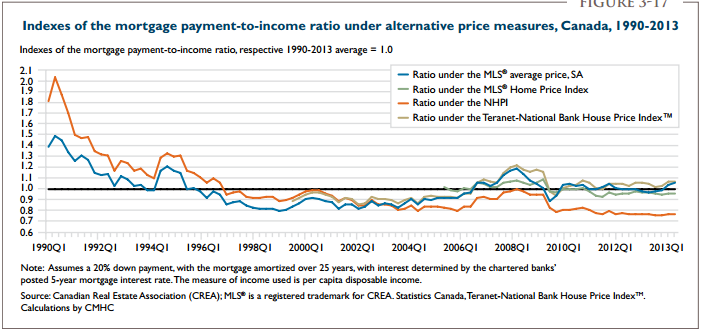

Mortgage affordability index from CMHC.

-

The median income in my neighborhood is more than 2x East Harlem.

-

Why do you think their houses are cheaper? https://financialpostbusiness.files.wordpress.com/2014/11/fp1106_world_property_markets_940_ab.jpeg?w=620&h=666

-

If I wanted to sell my detached house in Toronto (great neighborhood) and move to Manhattan, could I buy a similar house for the same price? Nope, I just looked on Trulia. If I want a townhouse in a nice neighborhood in Manhattan, I will need to sell 10 of my houses. There is a small vacant lot in East Harlem that is only 50% more than my house in Toronto, though.

-

I don't know what stats you are using but remember that averages are misleading. Average U.S. housing prices might appear cheaper but most of the cheap cities are not desirable. Anyone want to move from Toronto to Detroit, Buffalo, or Cleveland? The really desirable cities (San Francisco, LA, San Diego, NY, Miami) are expensive even after the housing meltdown. The other factor that people are ignoring is land use policies. Land is scarce in Vancouver and Toronto. In 2005, the Ontario government introduced the Places to Grow Act designed to promote intensification. This has limited the supply of single family homes (and resulted in a condo boom). Housing prices are certainly elevated but when you can control for supply constraints and interest rates, I don't know that we can be certain there is a bubble. We will only know in retrospect.

-

http://b-i.forbesimg.com/jessecolombo/files/2014/01/united-states-interest-rate.png

-

Before the housing crashes in Netherlands, Spain, US, Japan interest rates were rising. Also, did the housing market crash because of the recession? Or was the recession caused by the housing crash?

-

There is absolutely no evidence to backup any of your assumptions.

-

Mutual funds suffer from the constraints you list above but individual investors do not.

-

Rob Arnott has a couple good articles on this: http://www.riabiz.com/a/5814459/is-your-alpha-big-enough-to-cover-its-taxes-a-classic-journal-article-revisited

-

I'm not sure how seriously we should accept these researchers's interpretations. Negative correlations in the 0.03 to 0.32 ranges would be laughed at by physicists, chemists, and engineers. These are extremely small and weak correlations. You've all seen random scatterplot diagrams in which some statistician draws a line through the mist and says there's a correlation. Generally speaking, correlations of at least 0.70 - 0.80 are considered strong in the social sciences. Moreover, the P-value in Ritter's paper was 0.16, i.e., not statistically significant. If I remember my probability/statistics classes correctly, the statisticians square the correlation coefficients ® to come up with an R-square number, which represents how much of the variance in one variable explains the variance in the other. So GDP growth "explains" only 0.09% - 10% of the subsequent stock returns. Another illustration of the gulf between the physical science and economic/social science. I think the most that can be made of this is that economic growth is not meaningfully associated with equity returns. In the quote, he is pretty clear that it seems unrelated for all the reasons you mentioned. The potential country level dataset is too small to have any definitive conclusions,

-

You have two companies with the following stable profiles: China Inc Growth = 10% ROE = 5% P/B = 1 America Inc Growth = 5% ROE = 10% P/B = 1 Which one will have higher total stock returns? "All else equal" means holding margins fixed. Okay, which of these will produce better returns? China Inc Growth = 10% ROE = 5% P/B = 1 Canada Inc Growth = 5% ROE = 5% P/B = 1