KCLarkin

-

Posts

2,453 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Everything posted by KCLarkin

-

Possibly this one? https://en.m.wikipedia.org/wiki/The_Great_Crash,_1929

-

Young people don't live in detached houses in London, Manhattan, or many other cities. It isn't an inalienable right. The land use policies are designed to encourage more people to live in high density housing.

-

Very good rebuttal on Picketty and socialism

KCLarkin replied to yadayada's topic in General Discussion

This is perhaps the most un-intentionaly stupid thing ever written. Yes, capital can't forever become concentrated into a few hands. But the usual way to correct this natural accumulation is revolution, war, theft, and assassination. What happened to the Russian Czars? As a capitalist, I think the conclusion from Picketty is not that socialism is bad (or good). But that moderate socialism might be preferable to the guillotine and the bayonet. -

Forbes on Buffett.....this stuff is just too good.

KCLarkin replied to doughishere's topic in General Discussion

longbets.org But like a charlatan or astrologer, the predictor made his predictions so vague to make them meaningless. Future self: I am shocked that Buffett secretly developed a cure for cancer in his spare time! Future Oddball: See! I said you would be shocked at what comes out once Buffett dies! I win! -

What were some of the major blow ups in this sub-category?

KCLarkin replied to opihiman2's topic in General Discussion

I am currently reading a book called "The Art of Execution". The author managed a "best ideas" portfolio where he had several prominent investors manage a portion of the portfolio. 50% of ideas lost money. The key to successful investment wasn't the "ideas", it was execution. This wasn't a scientific study, but I think the conclusions are reasonably accurate. This is why cloning can be dangerous. If you blindly follow an famous investor into an idea, you won't be able to make key execution decisions. Zinc is down 30%. Do I sell or double down? Valeant is up 120% in a year. Do I sell or buy on strength? The interesting thing about the high-profile blow-ups this year is that most of the failures were execution failures: - Pabrai made a great bet on ZINC (if he sold in 2014). Or he could have cut losses as the risk of bankruptcy became apparent - Sequoia would have had one of the greatest investments of all time, if they had sold Valeant in August when it was clearly over-priced. Instead, Goldfarb's career is over. - Ackman should have sold Valeant in October/November. It is very clear that he sensed the risk of a death spiral. This isn't to criticize any of those investors. They simply fell prey to human biases. But stock "Ideas" are a commodity. Good execution is rare, challenging, and valuable. -

Forbes on Buffett.....this stuff is just too good.

KCLarkin replied to doughishere's topic in General Discussion

You need to read that in context of the date of the article (1969). This was the end of the "conglomerate boom". The conglomerates were the FANG of that era. Teledyne had an 89% peak-to-trough drop. The "good" teledyne came after. I thought KFC was a more interesting example since this would be in Buffett's core competency. But there was also a "franchise" boom during the 60s, so it makes sense in context. -

Berkshire Hathaway 2016 Meeting - Live Stream / Saturday

KCLarkin replied to tooskinneejs's topic in Berkshire Hathaway

http://finance.yahoo.com/brklivestream -

Berkshire Hathaway 2016 Meeting - Live Stream / Saturday

KCLarkin replied to tooskinneejs's topic in Berkshire Hathaway

The real issue is not a can of coke. A can is a reasonable serving size. But I assume most of the volume of Coke in America is not drunk from a can: http://jbawm.com/wp-content/uploads/2012/07/Michael-Bloomberg.jpg The moral argument is a red herring. The question is whether the new science that links Coke (and other sugary diseases) to heart disease, cancer, and diabetes will significantly reduce consumption. When I grew up, sugar was just considered "empty calories". Buffett seems to still believe this theory. But science is finding out that sugar is much worse than previously believed. -

No. This is briefly addressed in the CSU 2016 letter. This only works as a proxy for intrinsic value creation in very specific edge cases. If you paid out 100% of ROIC and Organic Rev doesn't require any incremental capital, your expected TSR would be organic growth + dividend yield. CSU is valuable because they can reinvest in very high ROIC acquisitions. This is only a rough proxy for Intrinsic Value creation and it only applies in very specific circumstances. (100% of IC is for acquisitions, incremental margins = 100%, organic growth requires zero IC, organic growth is disclosed in a useful manner). These happen to be roughly true for CSU. But likely won't be true in the future. But frankly, you are focusing on the calculation and missing the insight. The insight is that organic revenue growth is "free" since it requires zero capital. In fact, organic growth can generate "float" to fund acquisitions. If you haven't read the 2016 CSU letter, you should.

-

This might be true if there was a source of perpetual, costless, non-callable leverage. But the leverage available to retail investors tends to convert temporary volatility into permanent loss of capital. There is also a psychological and practical asymmetry between gains and losses. "Never risk what you have and need for what we don’t have and don’t need.” – Warren Buffett

-

http://www.osam.com/pdf/commentary_mar12.pdf

-

I was in Mexico last week. I overheard two people discussing the Vancouver real estate market. I officially agree that Vancouver Real Estate market is a bubble. I'm still not sure that Toronto is in a bubble.

-

http://www.fastcoexist.com/1679594/watch-las-vegass-growing-sprawl-from-space http://urbantoronto.ca/news/2013/05/examining-urban-sprawl-through-satellite-timelapse-imagery

-

Looks like Toronto CMA includes suburbs and is roughly same as GTA. Barrie, Oshawa, and Hamilton are outside the CMA. Population grew 9.2% from 2006 to 2011.

-

This is an interesting graph: http://www.statcan.gc.ca/pub/16-201-x/2016000/c-g/c-g02-4-eng.htm If I am interpreting correctly: - in the 10 years from 1991 to 2001, Toronto's "footprint" grew 369 square kilometres - in the 10 years from 2001 to 2011, Toronto's "footprint" grew 102 square kilometres - in the 10 years from 1991 to 2001, Vancouver's "footprint" grew 159 square kilometres - in the 10 years from 2001 to 2011, Vancouver's "footprint" grew 35 square kilometres There is a severe deceleration in urban "sprawl"

-

Winners (e.g. SAVE) might re-price quickly Value Traps (Sears) tend to drag

-

I haven't followed LUK closely. But: - Arlington previously owned JEF in 2011. He was a fan of Rich Handler. - Ben, Allan's partner used to work at LUK - Jefferies is the prime broker So they should be very familiar with both LUK and JEF. Big name value investors are dumping it. Everyone hates it. Not something I'm interest in, but I think they will do well on LUK.

-

He takes advantage of the volatility when starting these positions. Off the top of my head, CHEF, CMPR, and MSM all traded down to 15x operating earnings this year. BRK basically touched the 1.2x P/B "put". If you pay market-level prices for above average businesses, you are getting good value. LUK, OUTR, and SNE are more classical value plays. DNOW was pricey (for a cyclical) when he bought it but traded at ~ book value more recently I think the steady inflows of cash are wreaking havoc on his discipline though. It becomes harder to take advantage of market volatility when you have a steady stream of cash piling up.

-

It's because when 3/4 of people own homes/mortgages, and most of these people have their whole net worth tied to those assets (even when the net worth is deeply negative), you don't win votes by doing anything that might stop the rapid inflation of that asset. All the timid measures are to hope for a slow leveling off and plateauing, but the longer they kick the can down the road (hopefully to the next government, is their thinking), the more delicate things become. A few more years of this and the median house in Canada will be $600k+, an then what? A few more years and it's $800k? $1m? How fast are incomes rising? How fast are debt levels rising? I'd say that over 98% of home owners in Canada are decidedly not wealthy chinese princelings, so what next? Politics is less an issue in Canada than it was in the U.S. The bigger worry is that they will cause a hard-landing by tightening too quickly. The main problem is that the tools that would be most effective (higher interest rates) would have a broader impact on the economy. It would also hurt weak markets like Alberta. The other problem is that most of the really nasty shenanigans are happening outside the federal regulatory regime.

-

The Mistakes Made in Value Investing By The BigWigs and Ourselves

KCLarkin replied to AzCactus's topic in General Discussion

At my tax rate, BRK at 8-9% is probably equivalent to a bond yielding 15%. -

The Mistakes Made in Value Investing By The BigWigs and Ourselves

KCLarkin replied to AzCactus's topic in General Discussion

BRK and KO are "equity bonds" and should be compared to bonds. Not speculative stocks. Most investors should not expect returns higher than 9% with current interest rates. -

I think the opposite. The US is the least distorted housing market. Although I still regard the US market as hugely distorted. To me, 30 year mortgages are a ridiculous concept. And 3% mortgage rates even more ridiculous. How many other consumption or even investment markets are there which involve so much OPM and with such generous terms. I define a non-distorted housing market as the one that existed before the Great Depression where mortgage financing was minimal. To you I guess its the exact opposite...a non-distorted housing market is one that involves maximum mortgage financing. Bernake drops a bomb. It causes a Tsunami in Canadian housing prices. It doesn't cause a ripple in U.S. prices. You're right that the Canadian market is more distorted. But it should be distorted.

-

I'd argue that your endpoint for the U.S. is skewing the data. The housing market in the U.S. is not functioning properly. So you can say that Canada is overvalued, relative to the U.S. But it might be more accurate to say the U.S. is undervalued, relative to Canada. Both are probably true but using the U.S. as your measuring stick exaggerates the overvaluation.

-

Over those 25 years (using year-end dates not peak), your annualized return was 7%!

-

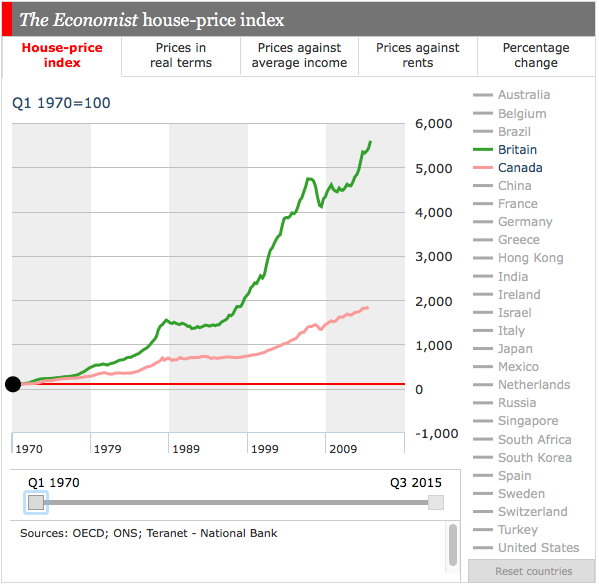

Comparing Canada to Britain, Sweden, Australia using that Economist data gives a very different picture.