ni-co

-

Posts

978 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by ni-co

-

I don't know. Look at a 5 year S&P500 chart: it's a straight line; pretty hard to beat as a mutual fund manager, I guess. Sometimes I wonder whether indexing has anything to do with this. BB missed 2011 but he saw 2007 coming. Sometimes it's just good/bad luck how your performance is looking – even over a larger time frame. Anyway, other advantages you have: you can buy options, go short, go into commodities, illiquid small caps etc.

-

I found this interesting: http://www.zerohedge.com/news/2015-01-27/equities-will-be-devastated-crispin-odey-warns-looming-recession-will-be-remembered- (ZH… – I know, I know. Yet, in contrast to ZH, Odey is no "perma-bear" and they had the most comprehensive excerpts from his investor letter)

-

If you want to read about how assets performed in other deleveragings Ray Dalio's website (and Bridgewater's excellent research paper there) would be my first point of reference. I'd be very careful with James Grant's opinions, though. They are interesting and unconventional but they are also quite quirky, to say the least. Dalio's ideas aren't mainstream either but he has been testing them intensely – not in phantasy land but in the markets – and they've been proving their value so far.

-

Stocks you own but NOT discussed on board - yet

ni-co replied to KinAlberta's topic in General Discussion

Innotec TSS AG – a German small cap construction material producer that gives me a 10% FCF yield with 0 debt. -

Jeffrey Gundlach: "This Time It's Different" Webcast

ni-co replied to ni-co's topic in General Discussion

original mungerville, I did a little analysis on hedging, it seems to me that buying puts is very expensive and the payoff does not seem all that attractive. I would love to hear your opinion on a short half page analysis that I am attaching below. Basically, you need to put nearly 16% of your portfolio into put options to be able to hedge your portfolio completely against a 40% loss. That means we can invest only 84% into stocks. I might be missing something and any feedback would be most welcome. Thank you! Vinod There is a cost effective way: You could short futures on an index, the Russell 2000 for example. The only problem with this solution is that you have to take exposure in $80k (Nasdaq 100) to $130k (Russell 2000) increments. -

Jeffrey Gundlach: "This Time It's Different" Webcast

ni-co replied to ni-co's topic in General Discussion

Gundlach's further market outlook for 2015 – "V": https://event.webcasts.com/starthere.jsp?ei=1048843 -

You can. but you might not want to. The part you don't mention is that when people borrow to consume, someone somewhere borrows to build the plants to make the things that the consumers are consuming. You might call this the "levering phase" and it works very well until the consumers, encumbered with debt, slow down their consumption. Then neither group has the cash flows to pay off the loans. Consumers consumer less and start paying down loans. Producers keep producing more and more to try to service their loans, but in the absence of demand they have to cut prices, and you get deflation. You might call this the "delevering phase". If they're badly run the consuming countries will lower interest rates more and more and more to try to "stimulate demand", aka get levered consumers (or if that fails, governments) to lever more and spend more on more stuff that (mostly) doesn't produce an income. If they're badly run the producing countries will borrow more and more to build more and more to keep headline GDP growing. That's what China has spent the last few years doing. Both policies just make the situation worse: more debt, more overcapacity, but no more demand. It's extraordinary to think that global GDP has gone from 175% in 2007 to 215% now. The globe as a whole is not delevering, but the levering might be in its final phase. I realise I'm drifting off topic here! What is really interesting is whether Americans will spend their oil windfall, or use it to delever. +1 This the right framework and exactly the right question.

-

This was my first reaction, too. But, referring to REITs and deflation, take a look at this: http://www.smtri.jp/en/JREIT_Index/img/J-REIT_Index_graph_e.pdf

-

can you explain how a high multiple levered real estate company with short lease terms is a deflation hedge? This is not a general statement. Everything with stable cash flows in a low growth environment is a deflation hedge. This is not true for every REIT but refers to EQR's assets: apartments in prime locations. Currently, rents there are growing at multiples of CPI rates and I think the current rent level is (at least) sustainable for a few years because of 1. demographic developments, 2. urbanization and 3. the growing number of rich people worldwide (wanting to rent/own an apartment in NYC, for example). If EQR's cash flows are stable, it will be much more comparable to a long term government bond than to the equity market. Long term government bonds are deflation hedges. But EQR is also able to raise its coupon. I think it should trade at a premium to the 30y government bond – even in a deflationary environment and it trades at an (albeit shrinking) discount. I think there is a widespread misconception of levered assets in deflationary/slow growth environments. Leverage is only problematic when you're facing shrinking cash flows.

-

LBTYA DVA Very strong underlying cash flow growth that should be more or less recession proof. If you buy the mid term deflation thesis I'd also add EQR. Looks very expensive and Sam Zell sold $150m worth of shares back in July. But it's a hedge against inflation and deflation at the same time, and provides a higher yield than the 30y US government bond.

-

Might not be exactly what you're looking for but I very much enjoy http://www.bloomberg.com/podcasts/masters-in-business/ and http://wealthtrack.com – which is also available as podcast.

-

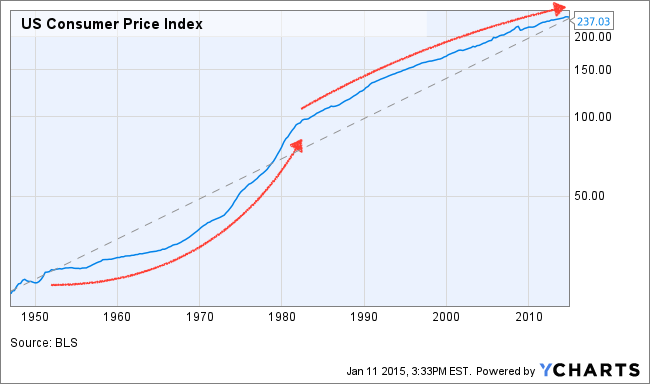

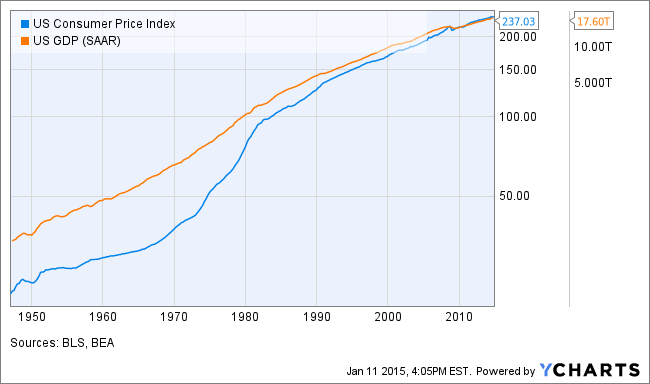

I played around with Y-Charts and thereby noticed that I'd never looked at a long-term CPI chart on a logarithmic scale. Take a look. Seems to me very hard to make an argument against a deflationary tendency here. I've read Gary Shilling's book "Age of Deleveraging" for the last two weeks and I think he nailed it. Some people say that he's been "wrong" about deflation for 30 years now. I think he's been right for 30 years. He doesn't make an argument for immediate deflation but for the tendency. This also fits nicely into Ray Dalio's theory of long-term super-cycles (see p. 6-9 – the US is in stage 5, I guess). It's quite interesting to think about Buffett's investing career from a compounding perspective – he surfed the curve perfectly. EDIT: What this also shows is that the usual FED critique is kind of unfair. Yes, the FED might have created asset bubbles. Yet, what they've done first and foremost is to stem the US economy against this long-term tide and thereby trying to dampen its impact. Imagine what could have happened if the deleveraging had accelerated with similar speeds like the expansionary phase in the 70s and 80s. It also shows very nicely the lessing impact of the FED's monetary measures. The curve really has begun flattening out in spite of ZIRP and QE.

-

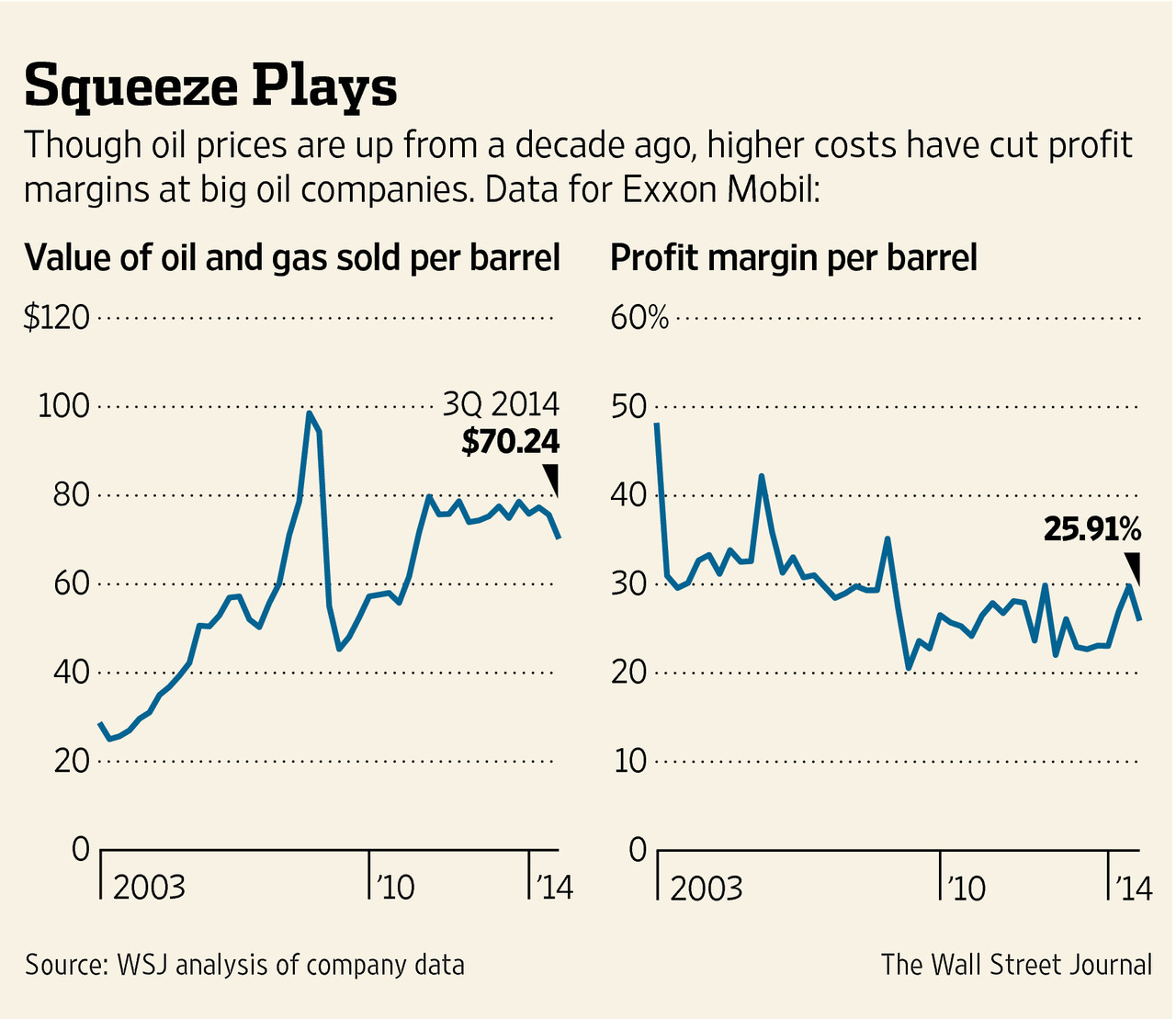

With this time horizon, I agree. What makes me wonder is that Mr Market – who's not known for looking several years into the future – takes this perspective with the major oil companies right now. My theory is that it has much more to do with reaching for yield than with either short or long term fundamentals. Completely disagree with this one. How high is this "natural hedge"? 75% of XOM's business still is selling oil. If oil prices stay low or go lower for some time, something's got to give: they will either have to kill larger exploration projects or cut down their dividend or both. We'll see. My bet is that XOM is not going to outperform the market for the next 1-2 years. I shorted it to hedge other portfolio long positions.

-

We've seen this story before. Maybe this time is different but you're going to have to prove it. In 1990 the price per barrel of oil averaged $23 due to the gulf war. Over the next few years the average price fluctuated between $15-$20 -- in 1997 the price per barrel was $19. The next year Oil prices plummeted, with the average oil price at $11.91. We had articles like these : http://www.economist.com/node/188181 http://money.cnn.com/1998/11/30/economy/oilprices/ Sound familiar? Oil was heading to $5 a barrel. I remember hearing about how technology would leave oil worthless and useless. Funny thing we're still using oil. How did Exxon Mobil do during this time? It was roughly up 350% including dividends. How did it perform during the drop between Jan 1997 to Jan 1 1999? It was up 50%. Drillers and the oil equipment companies were bloodied... just like they are now. There is a big difference: margins have been squeezed for the last 10 years even with crude at USD 100. Oil majors aren't the cash cows they were in the 90s – they are slowly deteriorating. I'm not arguing that oil will be up again sometime, I'm arguing that oil majors will face serious cash flow reductions. Everybody is essentially speculating that oil is going to shoot up within a very short timespan and that oil majors can therefore keep their high dividend payout ratios.

-

Can anybody please explain to me why oil majors like XOM and CVX move in tandem with the S&P 500 and more or less independently from crude prices? It almost seems like they'd have nothing to do with the oil industry. The price for oil halved and XOM is within 15% of its all time high. I don't get it.

-

I've read the "buy companies with low debt loads" advice in several places but I don't quite understand it. This seems to be too broad a statement and only applies to companies without pricing power. Yes, real debt isn't reduced by deflation (or might even rise) but at the same time capex requirements should go down in a deflationary environment. Credit should remain cheap (i.e. low nominal rates). So, as long as companies have really stable cash flows (in nominal terms, i.e. they grow them in real terms) even large debt burdens shouldn't be a problem – they will be able to roll it over at even lower rates.

-

I've been thinking about this for a while: You want stable cash flows – a stable rate of return and ideally the possibility to reinvest those cash flows at this high rate of return. Key is that the cash flows have to be sustainable in a low growth environment (and even then you have to be concerned with "reinvestment risk"): Health stocks, utilities, certain kinds of real estate, zero-coupon bonds etc. People keep focusing on dividends – but this is plain wrong. Dividends only matter if and when they can be sustained. It amazes me to no end that XOM is so stable compared to the oil price because people only think in dividend yields. How will XOM earn this dividend in a low growth environment? In a deflationary environment, oil majors will become real value traps. ps: Gary Shilling has a whole chapter on this in his book "The Age of Deleveraging: Investment Strategies for a Decade of Slow Growth and Deflation"

-

I'm referring to these charts in the article.

-

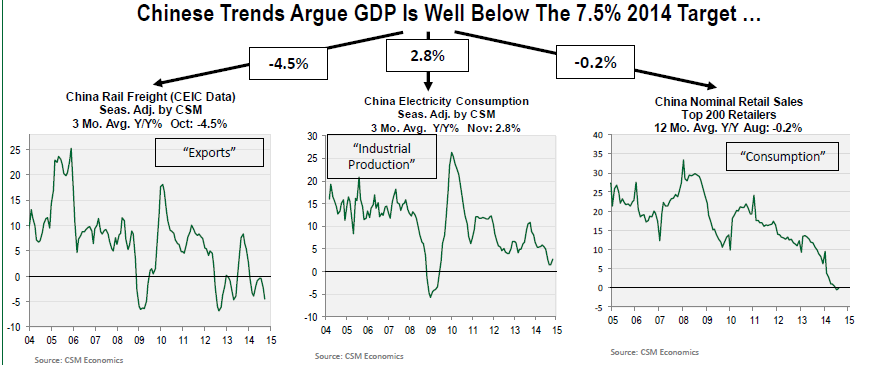

Look at those trends Cornerstone put into their latest reports: http://www.valuewalk.com/2015/01/cornerstone-macro-bearish/ For sure this would explain the drop in oil prices…

-

Jeffrey Gundlach: "This Time It's Different" Webcast

ni-co replied to ni-co's topic in General Discussion

Bill Gross chimes in: https://www.janus.com/bill-gross-investment-outlook -

Jeffrey Gundlach: "This Time It's Different" Webcast

ni-co replied to ni-co's topic in General Discussion

Another great sign for 2015: Not a single "strategist" is forecasting falling equity markets in 2015… WSJ (via google) -

Jeffrey Gundlach: "This Time It's Different" Webcast

ni-co replied to ni-co's topic in General Discussion

It doesn't matter whether he's been wrong in the past or whether he's a superstar. There are always "superstars" out there contradicting each other (think of David Tepper's recent comments for example) – so whom to pick? The reason I like to listen every time Gundlach is making a comment is that he is a highly idiosyncratic thinker and I really enjoy listening to such people. If they are right at times when almost everybody else is wrong this can be very profitable. Yes, it can be really painful when they are wrong. In the end, it pays to listen to the arguments. Ray Dalio says that having thoughtful people disagree is the way to gain the most valuable insights. I think, this time, Gundlach's arguments are very good and I also think that the consensus's (and Tepper's) argument for a prolonged bull market is weak. Nobody – nobody – argues with a fundamentally improving outlook for businesses. In a nutshell, the argument is: Compared to interest rates, stocks are not expensive but reasonably priced and since interest rates won't go up (all that much) in the near to mid term, stocks won't go down. I think this relative value argument is very dangerous, because there is no margin of safety. Either it's true, then you don't win all that much, or it's false then you're going to lose substantially. This is not a good risk/reward scenario. There are two ways for earnings yields to come down (i.e. P/Es to go up): stocks can rise or earnings can fall. A S&P 500 PE of 20 is only "cheap" (relatively, i.e. compared to interest rates) if you think that the earnings per share are at least stable. How did companies, in the aggregate, grow their earnings last year? With share buybacks! The economy hasn't really been growing much for years. So, what's the difference to 2011? Valuations and market outlook. I listened to Gundlach in 2011 and his view on the stock market – which was also the consensus view at the time – didn't convince me at all. Stocks were cheap, balance sheets were in great shape and the present state of the economy was not that great – meaning: room for improvement. Now, stocks are pricy on frothy earnings, balance sheets are deteriorating and the economy is still in a recovering state. If this recovery stops, hell will break loose in the equity markets. This is a completely different situation from 2011. If you buy/hold the S&P 500 at a 20 PE you have to be really convinced that earnings are on their way up – and I just can't see that. That's why I became more and more cautious towards the end of last year. -

Jeffrey Gundlach: "This Time It's Different" Webcast

ni-co replied to ni-co's topic in General Discussion

I agree with US assets. I've been holding all of my and my wife's assets in USD since 2012 and I can't see any argument why to change that. Have there ever been no/almost no signs for real problems? I stopped worrying (and learned to love the bomb). There are always going to be shit storms and I'd rather own super cheap stuff in the eye of it (Greece baby!) than pay up (US now) for clear weather. Yes, there have been signs. All I can say is that 1. the signs got a lot clearer to me, 2. the stock markets worldwide have become a lot more expensive, 3. if something cannot go on forever, it will stop. Does it have to stop this year? No. Maybe we continue this rally, but I won't participate. I hedged my portfolio to market neutral and I'm going to wait and see. Could you tell me why it wouldn't be a boon? What exactly happens? I know next to nothing about macro. We as a couple are already spending 3-4% less of our monthly income on gas, and that is only after a 25-30% drop in prices (taxes sadly don't drop as much) and with one car. Living in one of the world's best scoring countries for redividing wealth, I'm unlikely to get many yearly net raises of 4% or a 4% tax cut (we also win that category...) so I welcome it with open arms. The gas bill in many countries is a lot higher than in the US and I don't see how it could be anything other than an incredible general boost to consumers and businesses. Add a weakening Euro and you got yourself a party. The question is: Are you going to consume it or save it? If you save it, it does nothing for the economy. And at this moment, US consumers, Europeans, Japanese and Chinese – they all want to save it. -

Jeffrey Gundlach: "This Time It's Different" Webcast

ni-co replied to ni-co's topic in General Discussion

This is about the most recent data I could find: http://www.eia.gov/forecasts/steo/report/global_oil.cfm …and it ends right where it becomes interesting. Anyway, even if there were higher consumption in 2014: The futures market is about today's demand/future consumption – not today's consumption. You're going to see futures prices fall and then consumption to weaken – not the other way around. -

Jeffrey Gundlach: "This Time It's Different" Webcast

ni-co replied to ni-co's topic in General Discussion

Are we talking about estimates or real consumption for 2014? I think that staying out of the market – wholly or partly – is not a problem in a deflationary environment. What's the worst that can happen? You "lose out" on some equity gains but keep your money in real terms. Cash is only "dangerous" because of inflation. Keeping your money in USD seems to me the right thing to do. But I certainly don't think that I have to own stocks right now.